Western Digital Corporation has announced financial results for Q4 and the full year 2024 that show Q4 revenue up 41% year-on-year (compared to Q4 FY2023 and 9% sequentially). Full year data shows a 5.6% increase in revenue and close to break even on profitability. Does this data signal Western Digital is on the road to recovery?

Background

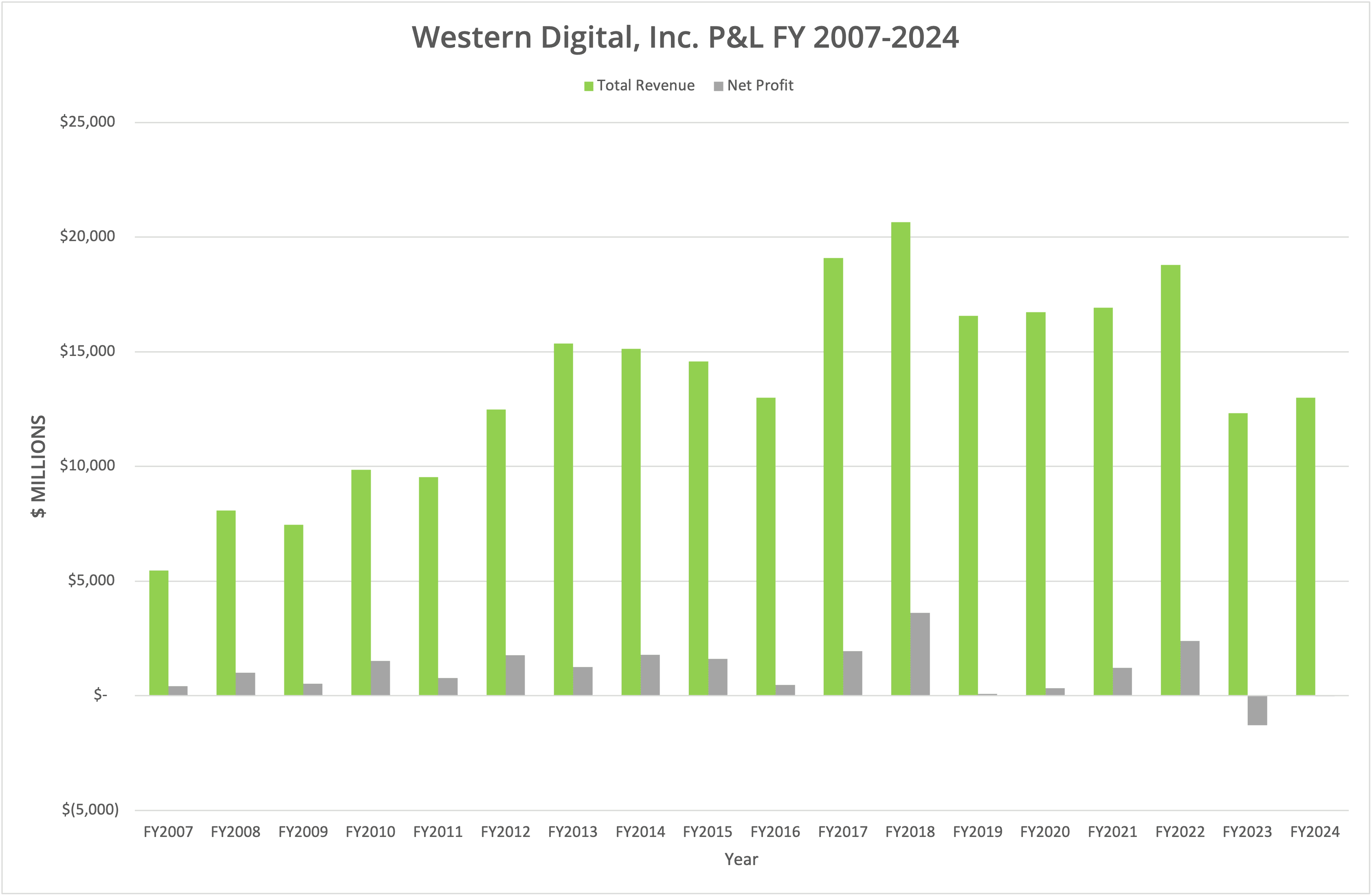

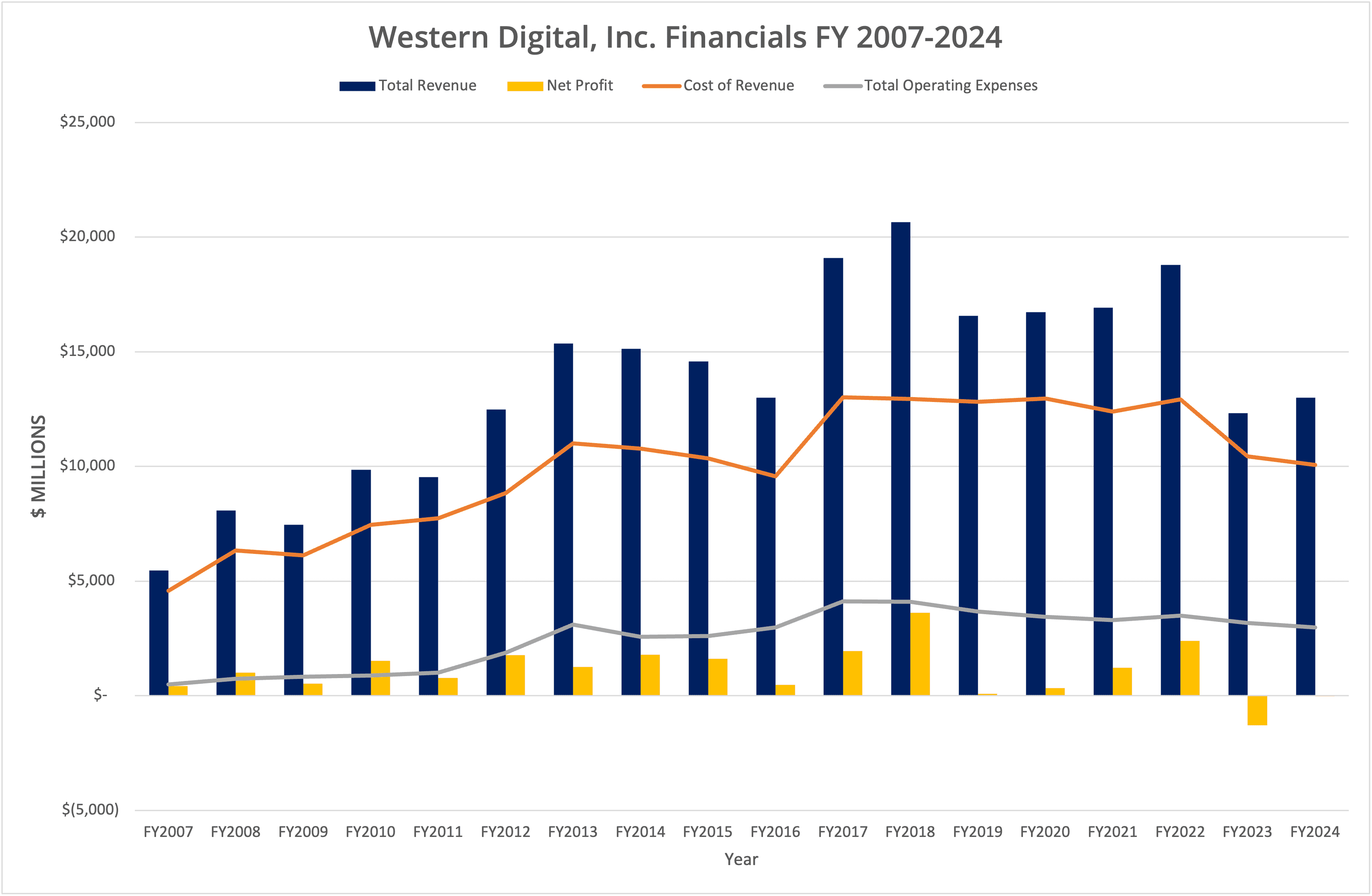

Western Digital Corporation published Q4 and full year FY2024 financial results on 31st July 2024. The data shows a sequential increase in revenue of 8.8% over Q3 FY2024 and 41% increase compared to Q4 FY2023. Full-year data shows an increase of 5.6% in revenue and crucially, close to break-even in profitability compared to a $1.29 billion loss in FY2023.

We have shown the financial data in four graphs labelled Figures 1 to 4.

Transformation

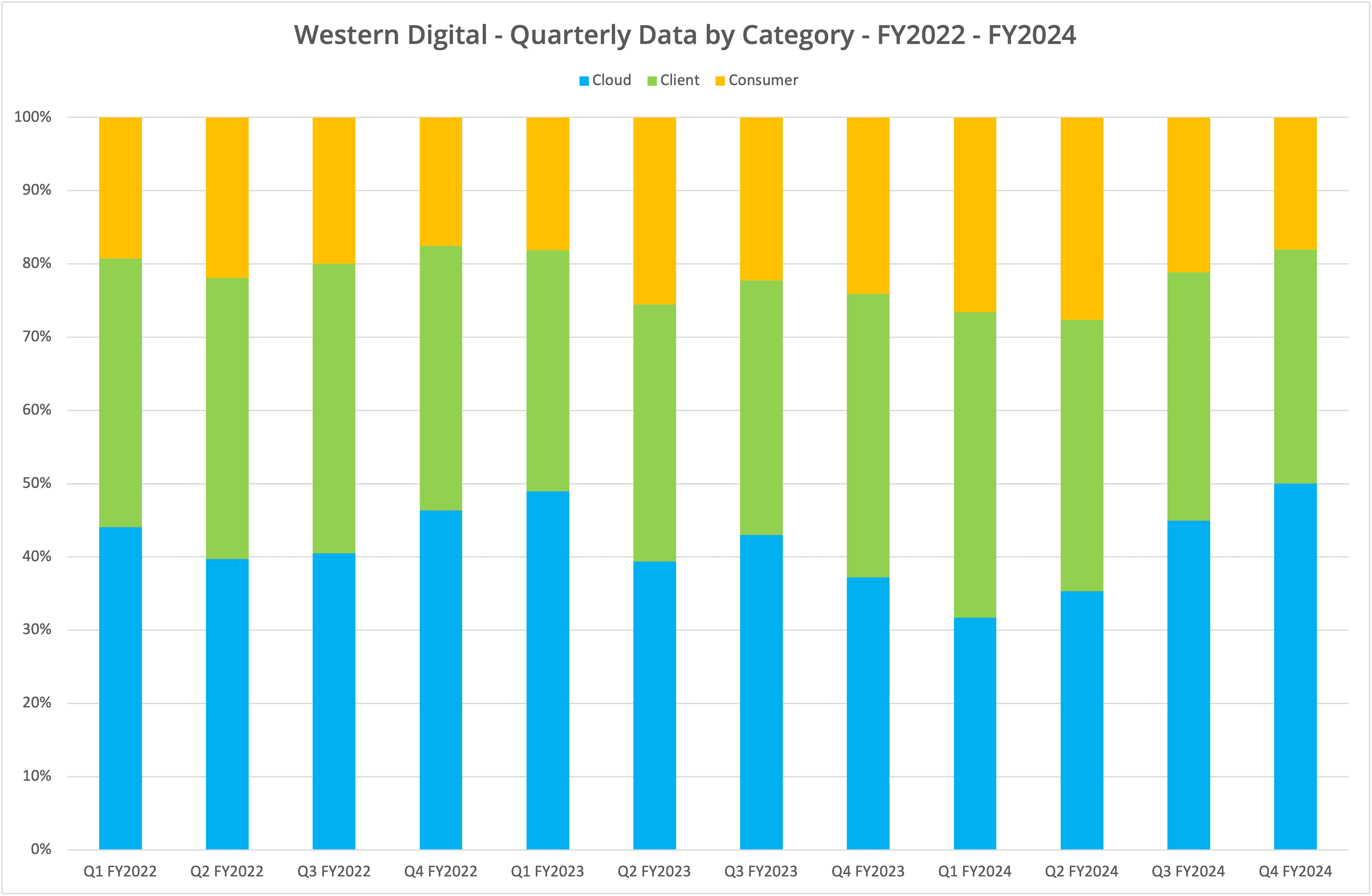

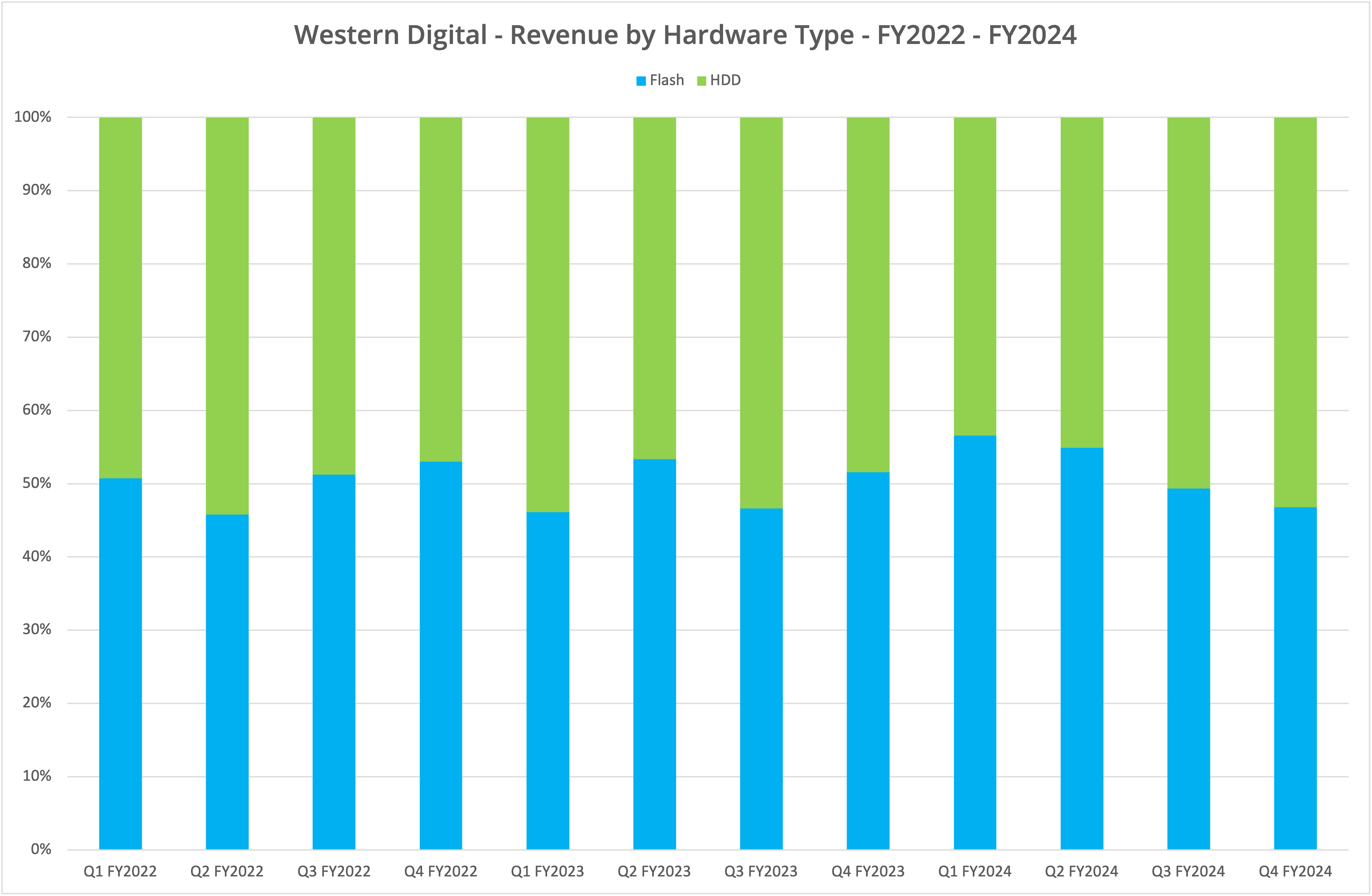

Western Digital breaks revenue figures down by both physical medium and usage category. Figure 4 shows revenue by hardware type, specifically flash and hard disk drives. We can see that the ratio of SSD to HDD has been slowly moving in favour of hard drive sales.

Figure 3 breaks down the data across three segments. These are Cloud (public cloud & enterprise deployments), Client (devices – PCs and laptops) and Consumer (retail). We can see that the revenue generated from both Consumer and Client has reduced (as a percentage), while Cloud sales continue to increase relative to the other categories.

WD highlights the growing demand for higher-capacity drives in the Cloud market, including increased SSD shipments. Only the Consumer segment seems to be declining, although the company pointed to improved average selling price (ASP) for consumer flash.

AI

Of course, every business is currently being buoyed by the adoption of artificial intelligence and the storage industry is no different. At present, the public cloud vendors clearly see HDDs as being the most cost-optimised solution that still has a use-case for enterprise customers. This stance isn’t surprising, as the majority of data sits inactive and is generally moved to faster media (such as NVMe drives) to be processed.

Using S3 as an example, back in 2019, we highlighted that AWS wasn’t passing on $/GB price reductions in media to customers. The baseline cost of S3 Standard in 2015 was $0.023/GB per month, where it remains today (instead, new services at a lower cost were introduced). However, the maximum drive capacity was only 10TB (typically 8TB), whereas today, we have models with 3x that capacity, which are typically sold at a similar price to the 2015 models.

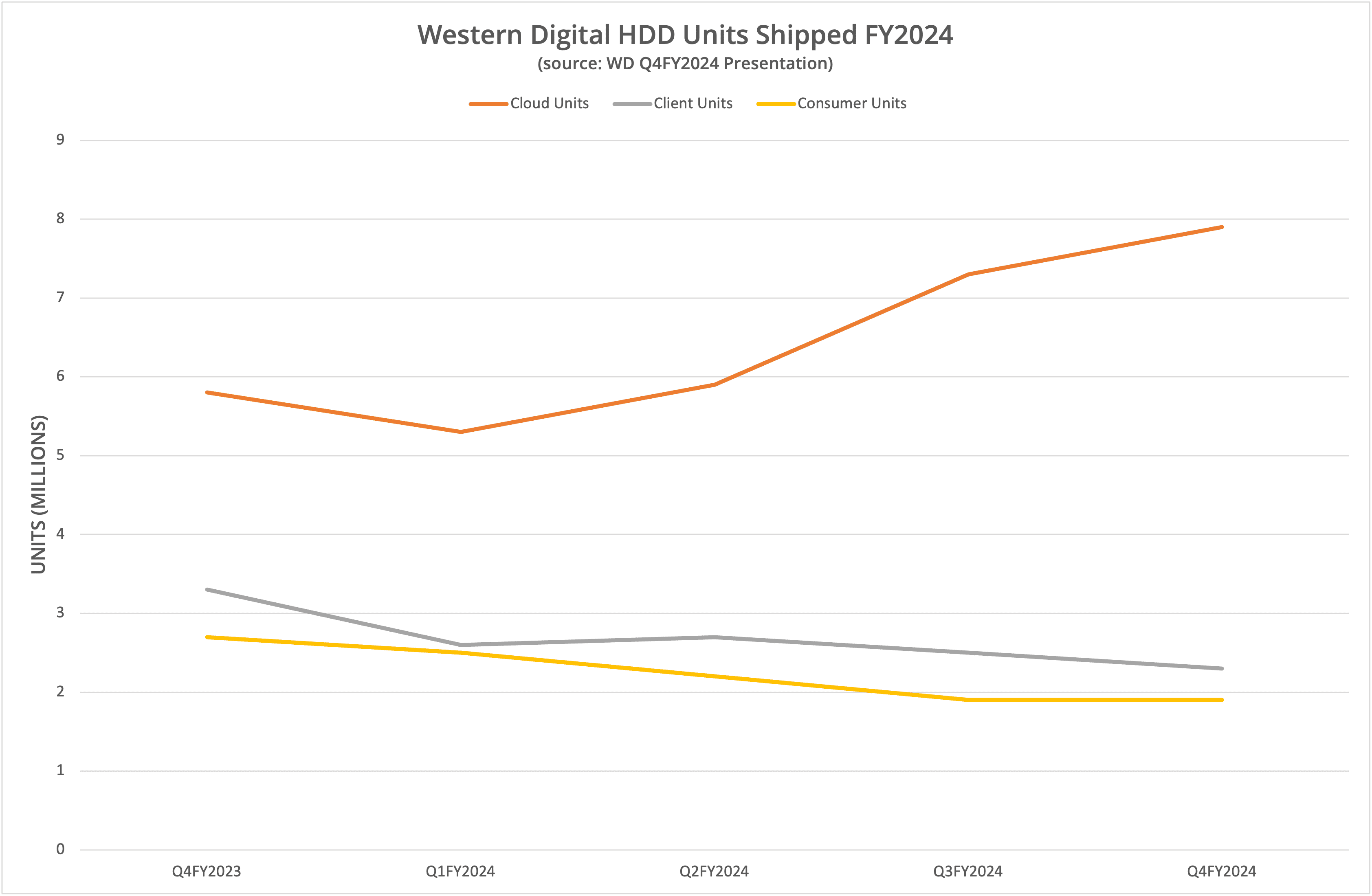

Western Digital (and Seagate) are benefiting from an upswing in the standard cycle for media replacement. As Figure 5 shows, the quarterly sales of Cloud units have steadily increased over FY2024, while Client units have declined slightly, and Consumer units have stagnated.

The Architect’s View®

Over the next few years, the demand for HDDs will be driven by the public cloud vendor’s desire to refactor onto cheaper (by $/GB) media and manage the growth of unstructured data, particularly that being retained for AI training. HDD exabytes shipped are increasing, while Flash exabytes are decreasing.

This change is interesting for the Western Digital split, which is due in the second half of this year. We might have imagined the SSD business growing more (especially with enterprise customers), but currently, based on the last four quarters, the growth (relatively) is in HDDs.

It appears that in the short-term at least, Western Digital will benefit from the HDD demand driven by the cloud platforms. Where does this market go next? Pure Storage would like us to believe that the HDD will be dead within five years (although we think that this means no new designs, not an end to shipments). This could be true in the enterprise but appears less likely in the public cloud.

For Western Digital as a whole, this position is positive. However, we can envisage that the public cloud vendors’ next hardware evolution will be to build custom SSDs, buying NAND and controllers directly from the manufacturers (or even buying a controller vendor). If this happened, the market for SSDs in the cloud could quickly dry up, but HDDs would still have a place. Perversely, the HDD could live on for a lot longer than we expect if this scenario plays out.

Copyright (c) 2007-2024 – Post #cd22 – Brookend Limited, first published on https://www.architecting.it/blog, do not reproduce without permission.