Intel Corporation has announced financial results for Q2 FY2024, the period ending 29 June 2024. Revenue was down 1% at $12.8 billion, mainly due to the non-core businesses including Altera and Mobileye. However, Intel also announced 15,000 job losses as it attempts to radically cut costs.

Background

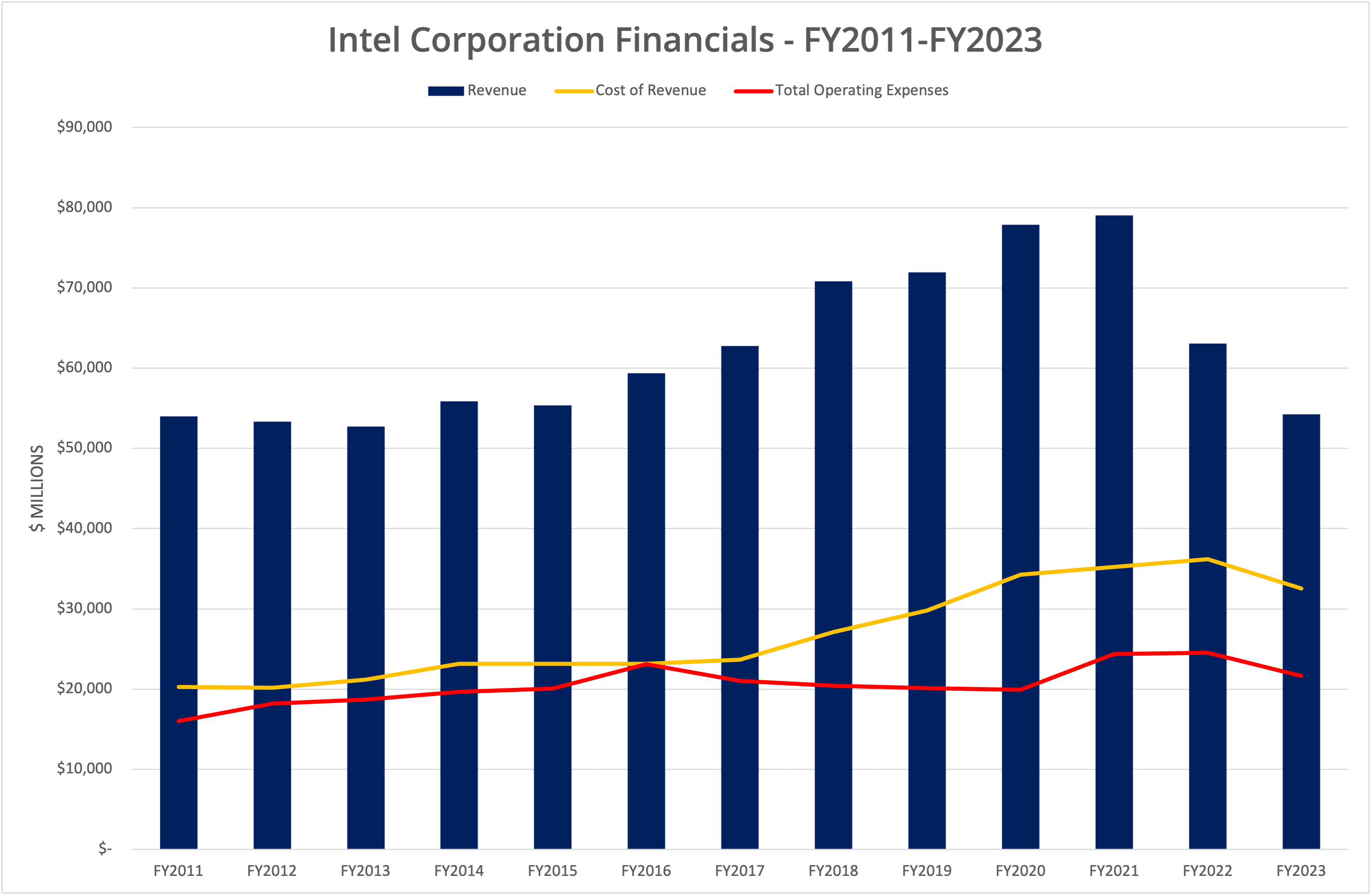

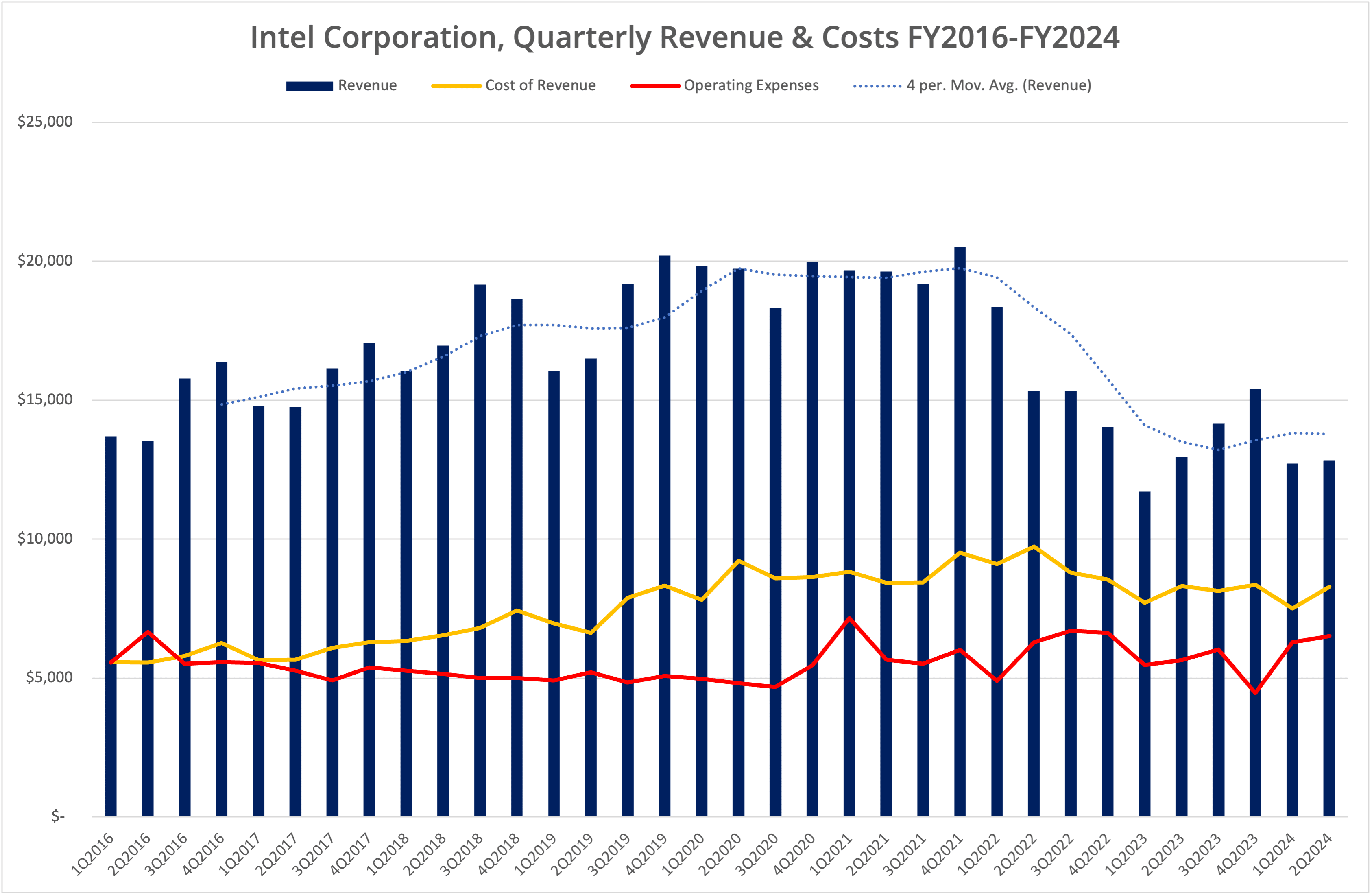

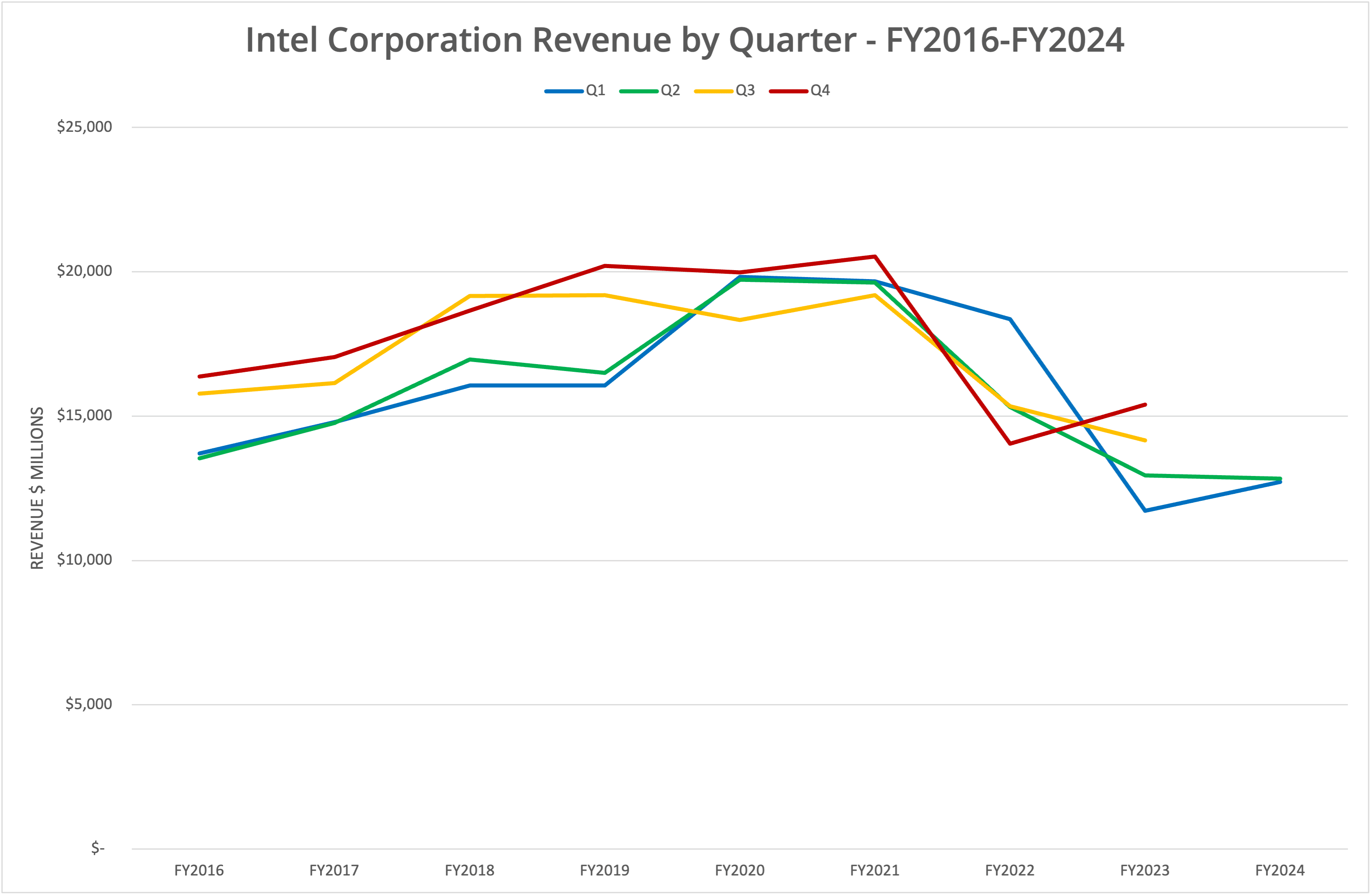

Intel has announced financial data for Q2 FY2024, which shows a 1% decline in overall revenue, year-on-year (YoY), driven mainly by non-core businesses, including Altera and Mobileye. Intel Products revenue increased 4.4% YoY, while the Foundry business increased 3.5%. However, this financial data represented a revenue target miss, with the strategic area of Data Centre & AI down 3.5%.

Intel has announced a reduction in headcount of approximately 15,000, or 15% of the workforce, to be completed by the end of 2024. This is an attempt to reduce costs and save $10 billion in 2025.

We have shown the current financials in a set of 3 graphs labelled Figures 1 to 3.

Efficiencies

In a statement from CEO Pat Gelsinger, the underlying message is clear; the company isn’t making enough money and costs are too high. The result appears to be a root-and-branch review of every department and process, slashing costs and improving efficiency. The IDM 2.0 strategy will continue as before, however share dividends will be suspended going forwards.

Intel Under Pressure

A few years ago, we added monitoring of the processor market to our data centre reporting and analysis. At the time, we highlighted a potential challenge for Intel as NVIDIA announced the Grace CPU, integrating Arm CPU cores with GPUs and high-bandwidth memory. Since then, the market has exploded, with massive demand for NVIDIA H100 and soon B100 GPUs.

However, there were many other red flags we identified, including the discontinuance of Optane, the increasing use of Arm in the data centre (by Public Cloud platforms) and other spinouts from Intel, including PSG (Programmable Solutions Group).

AI PC

Probably the greatest disappointment so far has been the AI PC, or essentially a PC where the processor has an AI-friendly co-processor or NPU. The first batch of Intel-based mobile devices failed to meet Microsoft’s minimum standards for Copilot, while competitors seized the advantage and introduced Arm-based solutions which could meet the specifications (albeit with limited AI functionality). Recent news on 13th and 14th Generation processors suffering from power issues that result in permanent damage is certainly not helping Intel’s reputation.

Defending Multiple Fronts

Unfortunately, Intel is trying to defend itself in many different aspects. Firstly, AMD is experiencing somewhat of a revival with both data centre and consumer CPUs. The latest Zen 5 architecture processors are outperforming Intel Xeons, while we have seen evidence of vendors moving to AMD for better scalability. Intel has invested heavily in catching up with the market with the 5N4Y strategy, but there is still work to do.

The GPU market is currently dominated by NVIDIA and unlikely to change much, as this is a market perception issue, as much as which product is the better choice. NVIDIA arguably have a better software ecosystem with CUDA.

On the desktop front, Arm is making progress with Snapdragon X. In the data centre, Arm is gaining adoption by the public cloud platforms, the top three of which all have their own processors in general availability or development. For many workloads, Arm looks more cost-efficient than x86. With suitable application and library support, Arm-based instances offer customers the chance to make real cost savings.

IDM 2.0

We’ve also seen some issues with the IDM 2.0 strategy and the move to become a leading foundry and manufacturer. Investments in Italy and France have been suspended (link), while construction in Germany has been delayed (link). Earlier this year, Intel announced that its Ohio plant would be delayed by two years (link).

The Foundry business will undoubtedly eventually reach maturity, but not for many years longer than initially envisaged. This means the benefits won’t impact the top and bottom lines for quite some time.

The Architect’s View®

Intel is a strong brand with a rich history in the development of core computing solutions. The company has disrupted itself before, exiting the DRAM business in 1985 to focus on microprocessors. That transition gave us the x86 era, which evolved from personal computers to the servers that power most of the computing world today.

But times are changing, as they always do in the IT world. AMD has reinvented itself and directly challenges Intel in the x86 market. The rise of the public cloud has enabled end users to consume the most efficient technology and for the public cloud vendors to build bespoke solutions (based on Arm) due to their economies of scale.

The rise of AI looks to be a boon for Intel, but NVIDIA dominates the AI zeitgeist, while the benefits of the AI PC have failed to materialise. The road back to data centre dominance looks increasingly rocky for Intel, one that may not be achievable anytime soon.

Related Content

- Commentary: The rise of Arm in the desktop spells trouble for Intel

- Research Note: Google Cloud unveils Axion custom Arm processors

- Are ARM Processors Ready for Data Centre Primetime?

- Research Note: Intel Vision 2024 previews Gaudi 3, Xeon 6 and Lunar Lake Processors

- Research Note: Intel restates accounts to separate Intel Foundry and Intel Products segments

Copyright (c) 2007-2024 – Post #0ace – Brookend Limited, first published on https://www.architecting.it/blog, do not reproduce without permission.