Intel Corporation has announced a restating of accounts as part of the transition to a separate Foundry business. In addition, the Programmable Solutions Group has now been spun out as Altera. We take a look at the new financials and what insights they show for the future of the company.

Background

In February 2024, Intel announced plans to divide the company into two distinct operating segments called Intel Products and Intel Foundry. The goal of the separation is to build an independent chip manufacturing and packaging business that can compete against the current leaders in the market, including TSMC and Samsung. By providing transparent accounting, Intel hopes to attract customers to use the Foundry services, even if those customers may be seen as potential competitors to the Products business.

IDM 2.0

On 2 April 2024, Intel released revised financials, which show the effect of carving out costs of the Foundry business into an independent entity. We will return to the data in a moment. However, it’s worth touching on the strategy that reached this point.

During a webinar that announced the new financial data, CEO Pat Gelsinger admitted to mistakes Intel has made in the past and his goals to rectify them. Intel fell behind on process and manufacturing improvements, so it established the IDM 2.0 strategy, which includes “5 nodes in 4 years” – effectively catching up with the rest of the industry on scaling improvements. You can read about the details in this Research Note we published in February 2024.

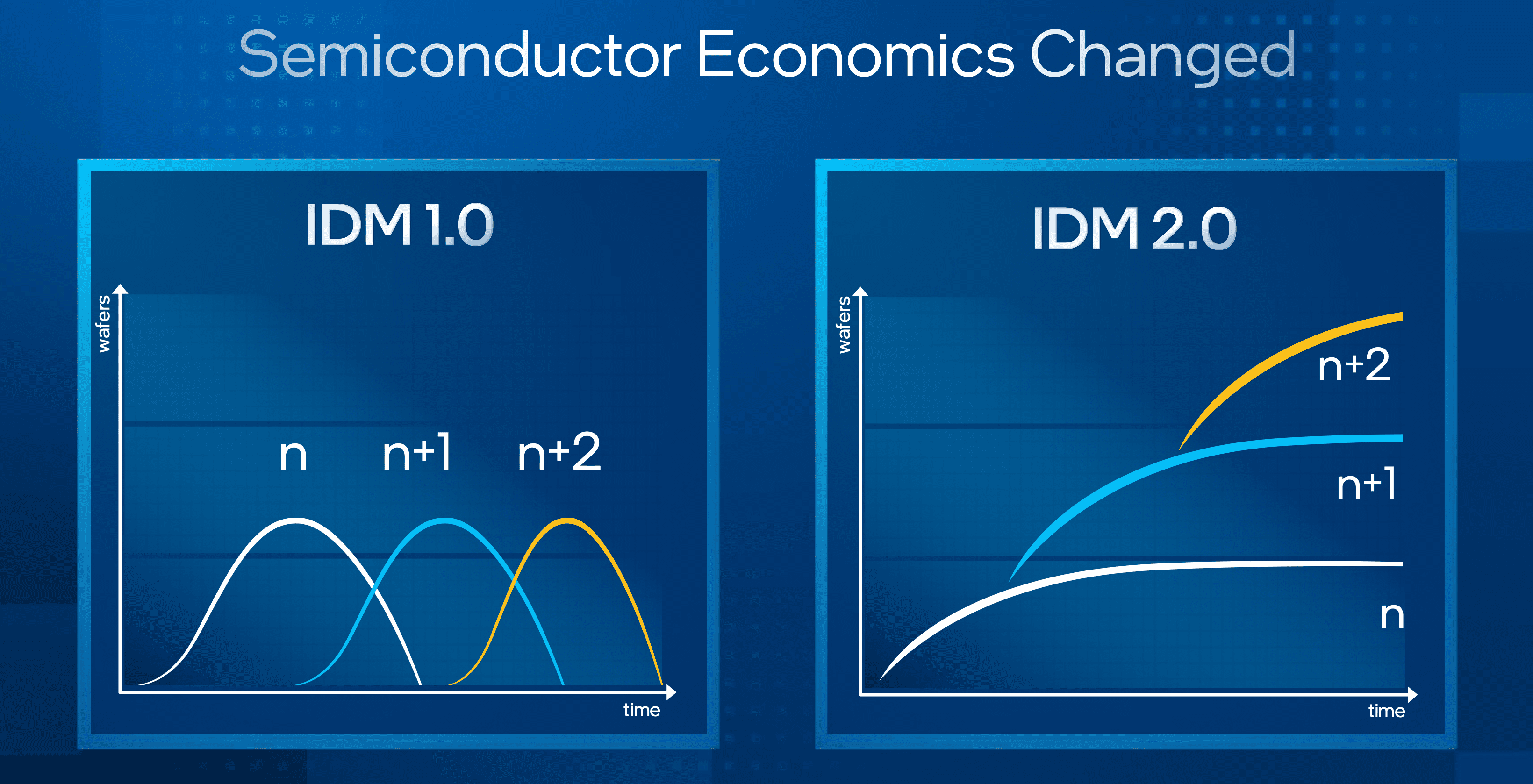

The “5N4Y” strategy is almost complete, after which Intel expects to return to a typical two-year cadence for improvements. However, this rapid process transition is unlikely to continue, with Gelsinger highlighting the need to exploit existing processes further rather than moving from one to another in quick succession (what was previously known as process/architecture/optimisation, an evolution of the tick-tock production model).

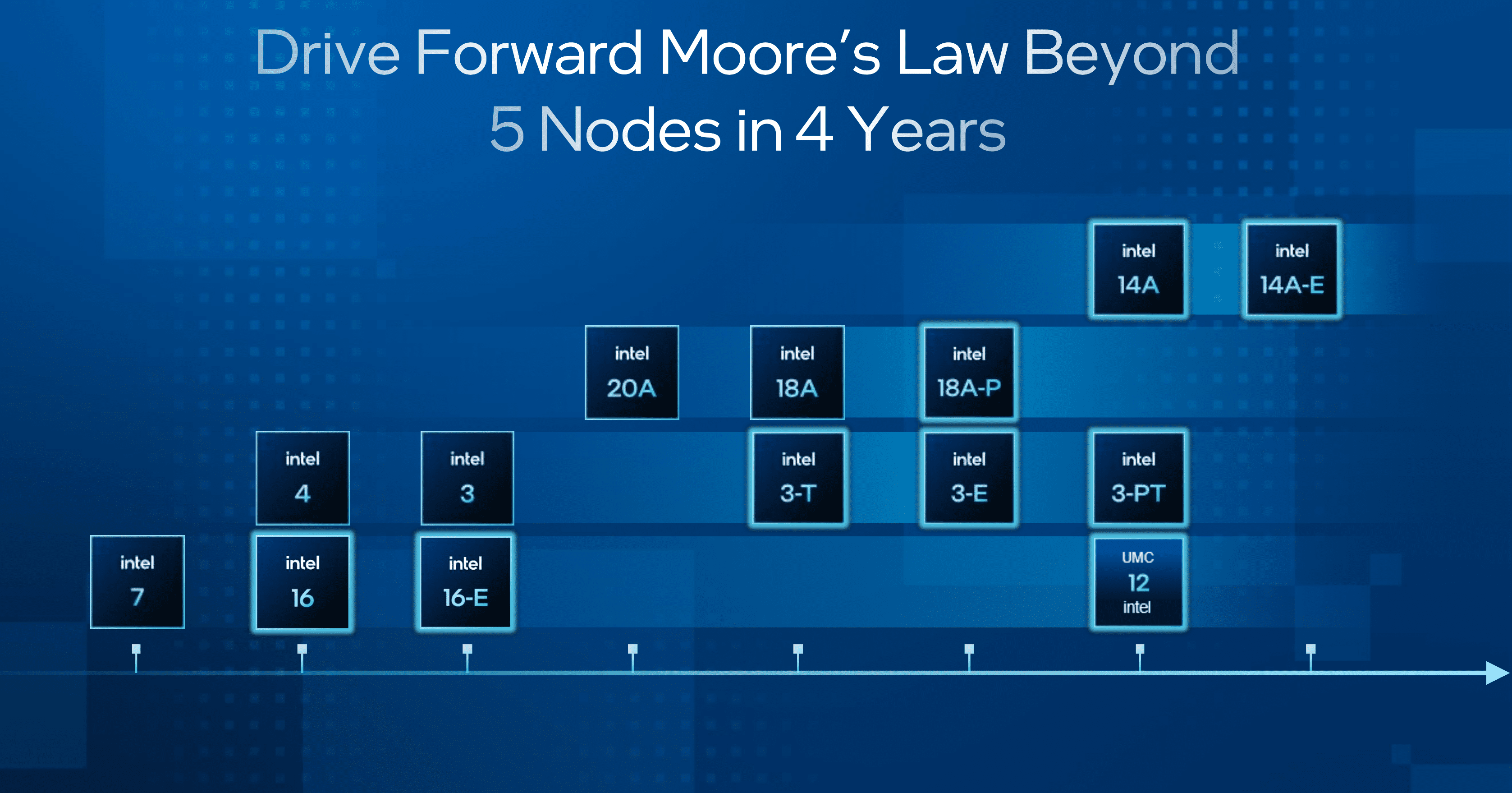

Intel highlights the change in strategy with the graphic shown in Figure 1. Process and optimisation improvements will come from the aggregate benefits on existing platforms rather than bringing new solutions to market. Figure 2 highlights this further, showing a diversity of products that will start to appear, based on the 5N4Y architectures and beyond. One good example here is the use of the chiplet design, combining multiple dies into a single product, where each chiplet could be based on a different manufacturing process.

Leadership

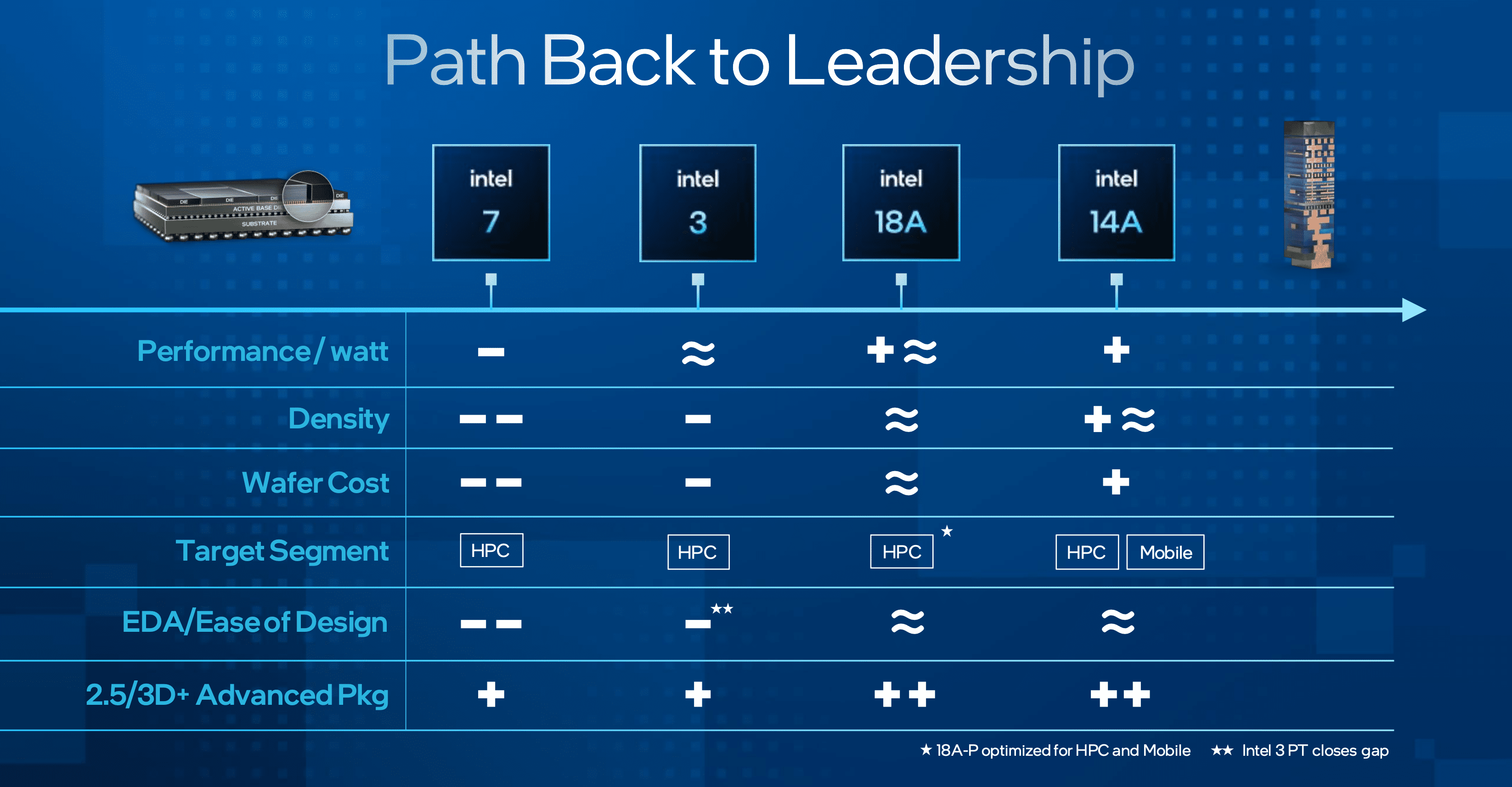

Intel believes that the 18A process will be the point at which the company catches up with the rest of the industry and starts to overtake its competitors. See Figure 3 as an example of this, where metrics such as performance efficiency, density, and cost start to become differentiators.

Another tipping point is the ability to use new technology such as EUV (extreme ultra-violet) and High-NA lithography. In December 2023, ASML shipped the first High-NA system to Intel in Oregon. In contrast, it has been reported that TSMC may not use High-NA technology until at least 2030. However, simply reducing the aperture size doesn’t result in better products, as the exposure field, for example, is reduced when moving from Low-NA to High-NA (low to high numerical aperture). This is one reason why the chiplet concept and interconnects could prove highly important in future designs.

Financials

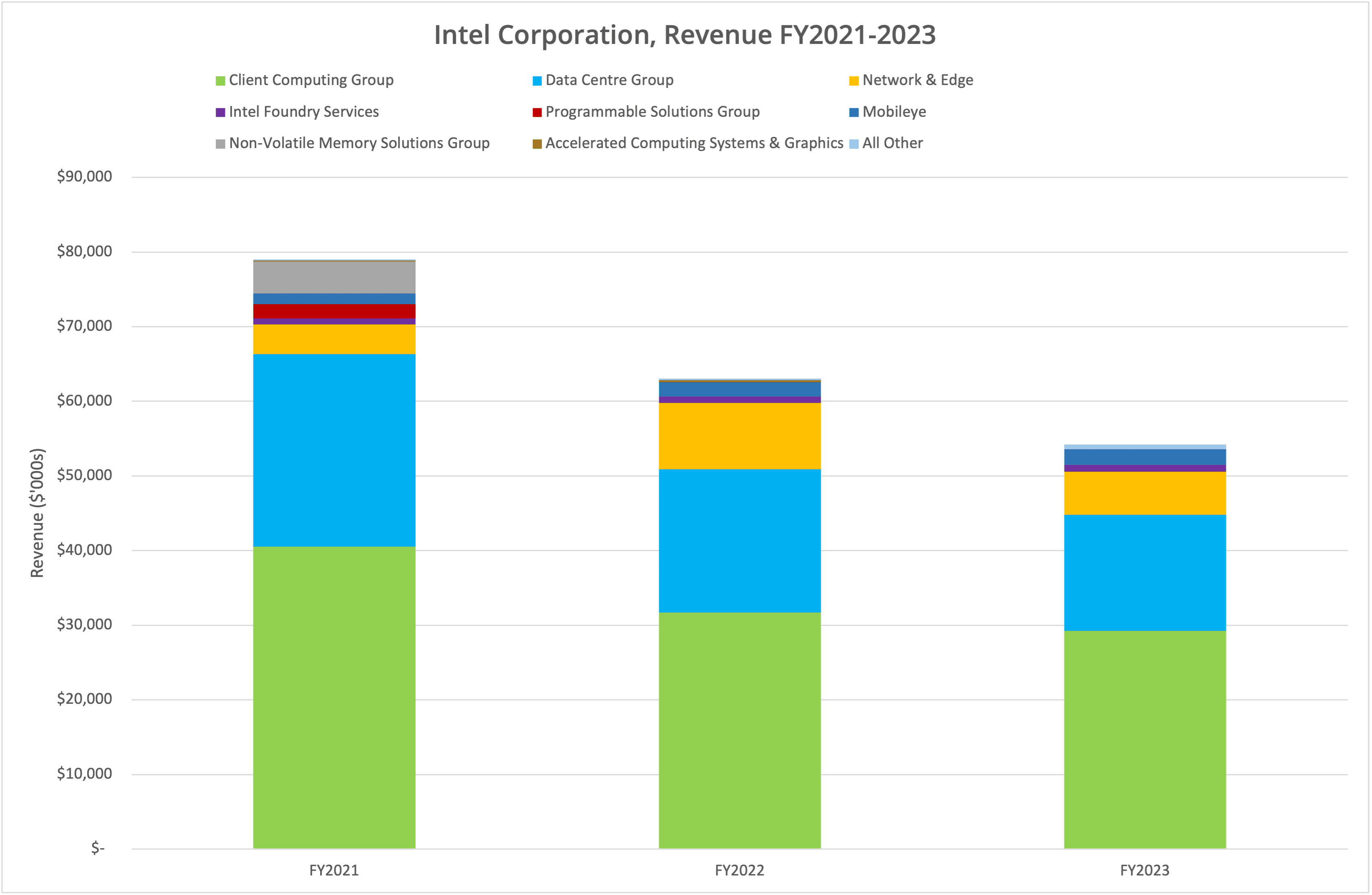

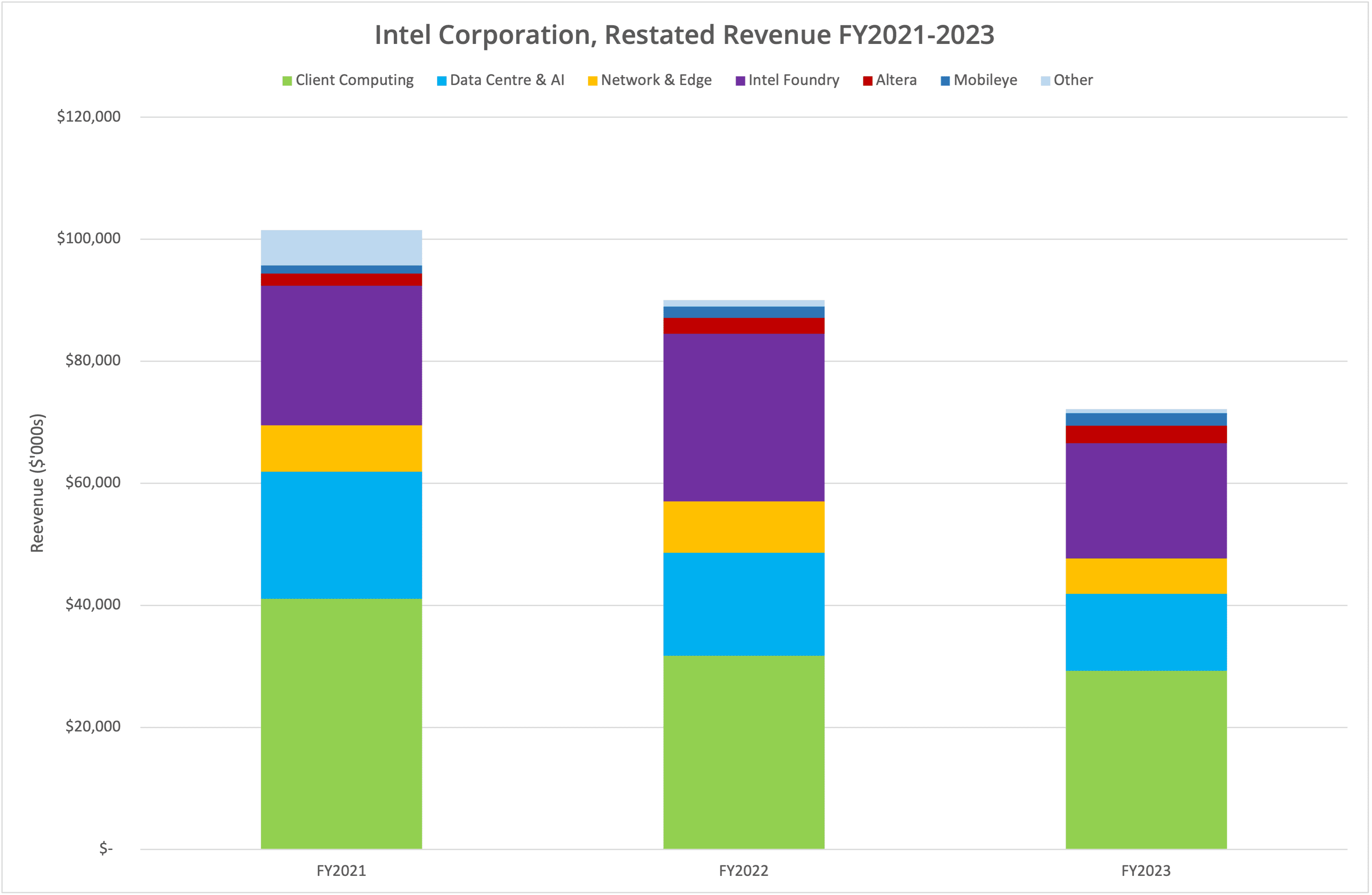

Let’s look at the restated financials compared to the data already published. Intel has reworked the last three financial years of data, providing revenue and income statements across the Products, Foundry and Other categorisations. Previously, Intel presented data across Client Computing, Data Centre, PSG, Network & Edge, Mobileye and Foundry Services. FY2021 also included the Non-Volatile Memory Solutions Group, which was sold to SK Hynix and became Solidigm.

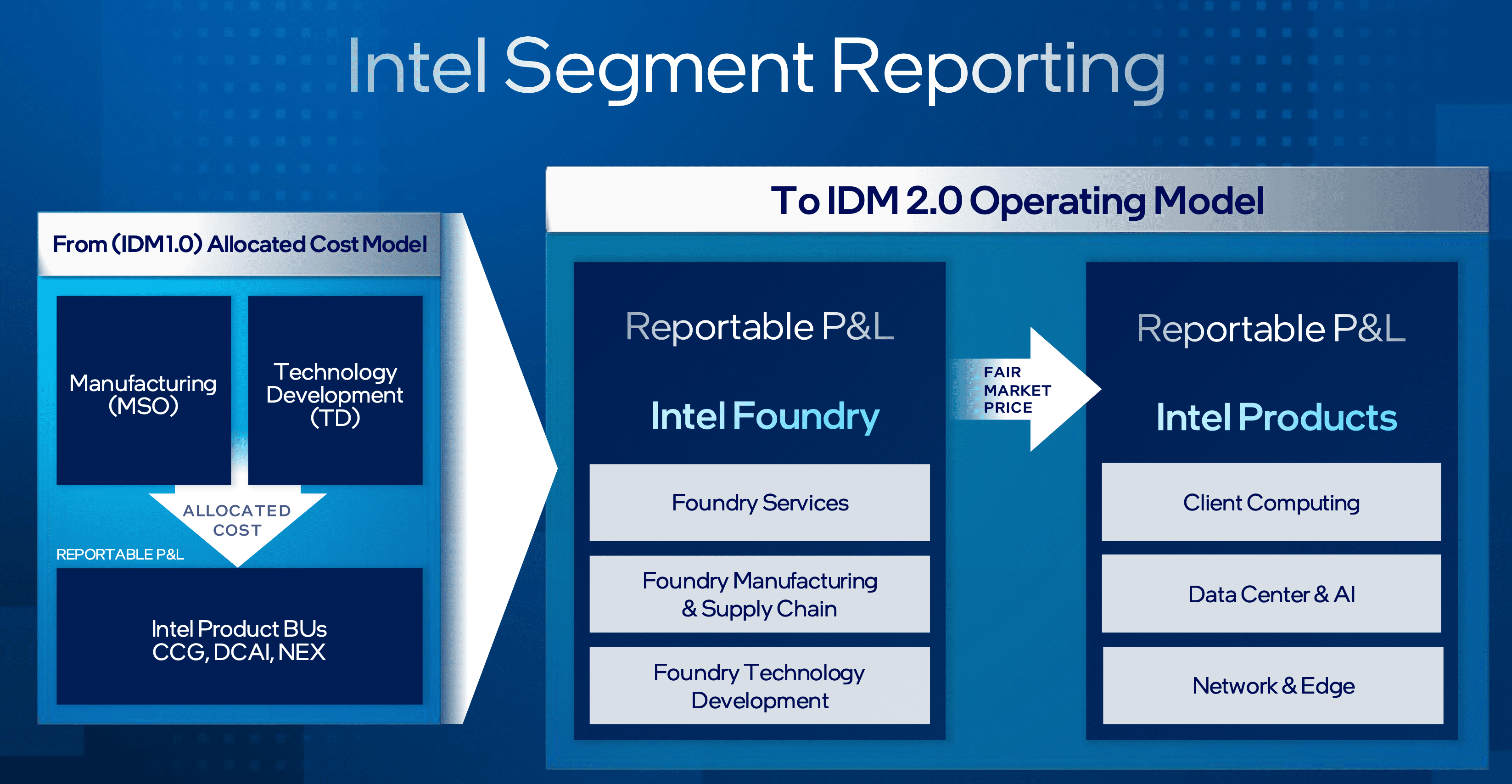

The revenue data is shown in two graphs, Figures 4 and 5. We’ve attempted to keep the colour schemes similar between the two categorisations, with the result that we see a significant attribution of revenue to the Foundry business. The rationale behind this restatement is to create a process that highlights fair market price for the foundry services that were previously embedded in the individual business units (Figure 6). Note that the revenue totals don’t align as we haven’t shown inter-segment eliminations in the graph data.

The restatement data shows that the Foundry business made an effective loss over the last three financial years of $5.1 billion, $5.2 billion, and $7.0 billion (FY2021-2023). Intel justifies these losses as part of the investment in Foundry, including new facilities being built in the US and EU. Losses are expected to peak in 2024 and lead to break-even at some time between now and 2030.

Intel expects that adoption of new foundry processes and scaling up of production will lead to improved gross and operating margins over time, for both the Products and Foundry businesses. The company has announced $15 billion in current future deals for the Foundry business (much of which we know will come from Microsoft), increasing to greater than $15 billion of annual external (non-Intel) revenue by 2030. Of course, Intel has also been the recipient of significant government investment and loans (around $50 billion to date).

The Architect’s View®

We’re starting to see more detail on the ambitions of Intel (and Pat Gelsinger) to reinvent the business. The Programmable Solutions Group has been floated off as Altera with an independent P&L (we reported this back in October 2023). Financial separation of the Foundry business provides the ability to transform this operating segment into a profitable company, with the future possibility of an IPO.

We don’t believe that the current long-term strategy is to turn the Foundry business into a separate public entity. The current plan is to create a sub-company that can operate with a degree of independence that attracts profitable business, which will include many new organisations, such as hyper-scale cloud vendors.

Gelsinger is reversing a tightly knit organisation into a loosely connected federation of companies with fewer direct dependencies and lock-ins. It creates a structure where each entity has an independent chance of winning in its respective market. We now need to follow these streams separately, as they align more equitably with the rest of the industry.

Has Intel pulled a masterstroke with this reorganisation? Don’t forget that even this week, TSMC announced grants and loans from the US government totalling $11.6 billion. Samsung is expected to announce subsidies worth $6.6 billion for chip manufacturing. Intel does not exist in a vacuum in this market, so investments by the company need to work.

There’s still a long way to go on this transformation journey. Whether it will be successful is still to be determined. However, Intel currently appears stronger in the manufacturing part of the business than the products segment. Can a single CEO balance the demands of two separate businesses? That’s the $64,000 question.

Copyright (c) 2007-2024 – Post #cc5d – Brookend Ltd, first published on https://www.architecting.it/blog, do not reproduce without permission. Images copyright (c) of Intel Corporation, except the financials graphs.