To counter the challenge of the public cloud, many traditional on-premises infrastructure vendors introduced the concept of “as-a-service” models, including unit-based consumption. Data from financial accounts show that, in many cases, these services form only a fraction of overall revenue. Is the “as-a-service” market relevant or just a box tick for analyst reporting?

Background

Traditionally, computing hardware was sold to businesses as a single purchase with a fixed period of product maintenance attached. In the server and storage world, for example, that period was typically three years, with the option to extend maintenance after the initial warranty had elapsed. Generally, the post-warranty period attracted a higher cost for maintenance, because the equipment was older and so more likely to experience failures, but also because vendors wanted their customers to “upgrade” to the latest hardware.

This cycle, generally referred to as a “forklift upgrade”, is well-known in the industry and something we’ve commented on many times (see this post).

Projects

The three-year cycle is interesting as it probably evolved from the process of instantiating new application projects within a line of business. The business unit would fund the purchase and, once in production, hand over the equipment for IT to manage. After three years, the gnarly subject of whether to refresh or maintain arises, with IT generally footing the bill for either maintenance or replacement.

In smaller organisations, this piecemeal project-based process wasn’t a bad idea, although it was likely to be highly wasteful on resources, such as underutilised servers. Shared storage and server virtualisation created an ecosystem where resources could be shared, paving the way for internal service catalogues to be developed.

Service Catalogue

With an IT service catalogue, a business unit can buy resources from central IT and move away from fixed hardware architectures. Instead, storage, virtual servers and networking can be sold by the gigabyte, virtual machine and network port.

At the back end, infrastructure continued to be purchased on multi-year cycles, giving IT the headache of translating capital purchases into operational costs sold onto internal business units. In large organisations, economies of scale make this packaging task easier and, arguably, these companies tend to employ architects and invest in what is now called platform engineering to effectively create private clouds.

Public Cloud

In parallel with the on-premises cloud model, many businesses have moved partially or fully to the public cloud where the purchasing model is entirely opex-based. The public cloud platform vendors take on the responsibility of building service catalogues, that first started with basic components like networking, storage and virtual instances, but now includes complex applications and development platforms.

How are public and private clouds different? In reality, both solutions are almost identical. However, in the public cloud, vendors like AWS, Microsoft and Google have optimised their platforms to deliver a multi-tenant experience with consumption-based billing. Economies of scale mean that while growth in these platforms continues, hardware resources are rarely wasted.

Customisation

It’s important to note that public cloud platforms have built services on hardware that has (over time) been built specifically for operational efficiency. For example, AWS acquired Annapurna Labs to build Nitro, which provided server efficiency gains, increased security and added remote management for server hardware supporting virtual instances. Storage offerings have evolved slowly while an increased focus has been placed on application delivery. However, behind the scenes (as this AWS article attests), the infrastructure teams in AWS, Microsoft, Google and others are constantly striving to deliver more efficient solutions from an operational and cost perspective.

Side Note: It is interesting to note that the equivalent of Nitro, on-premises solutions like VMware’s Project Monterey and Nebulon’s Cloud-Defined Storage failed to make an impression on the on-premises infrastructure world. You can read more about these types of solutions in this post.

Private Cloud

Concerned with the impact of lost business to the public cloud, traditional infrastructure vendors have introduced consumption and “as-a-service” based models into their portfolios. Rather than following traditional purchase or lease agreements, businesses can buy by the terabyte or purchase infrastructure to support a fixed number of virtual servers.

In reality though, many of these offerings are still just lease purchases in a different financial wrapper and not true services. A service would let customers scale up and down (or gain discounts from longer-term commitments) and not be tied to the fixed architecture of the platform.

Storage-as-a-Service (StaaS) is one area where we’ve seen many vendor offerings that aim to deliver resources under a consumption-based model. NetApp has Keystone, Dell has APEX, Pure Storage has Evergreen, HPE has GreenLake, and Hitachi has EverFlex. How successful are each of these vendor solutions?

HPE

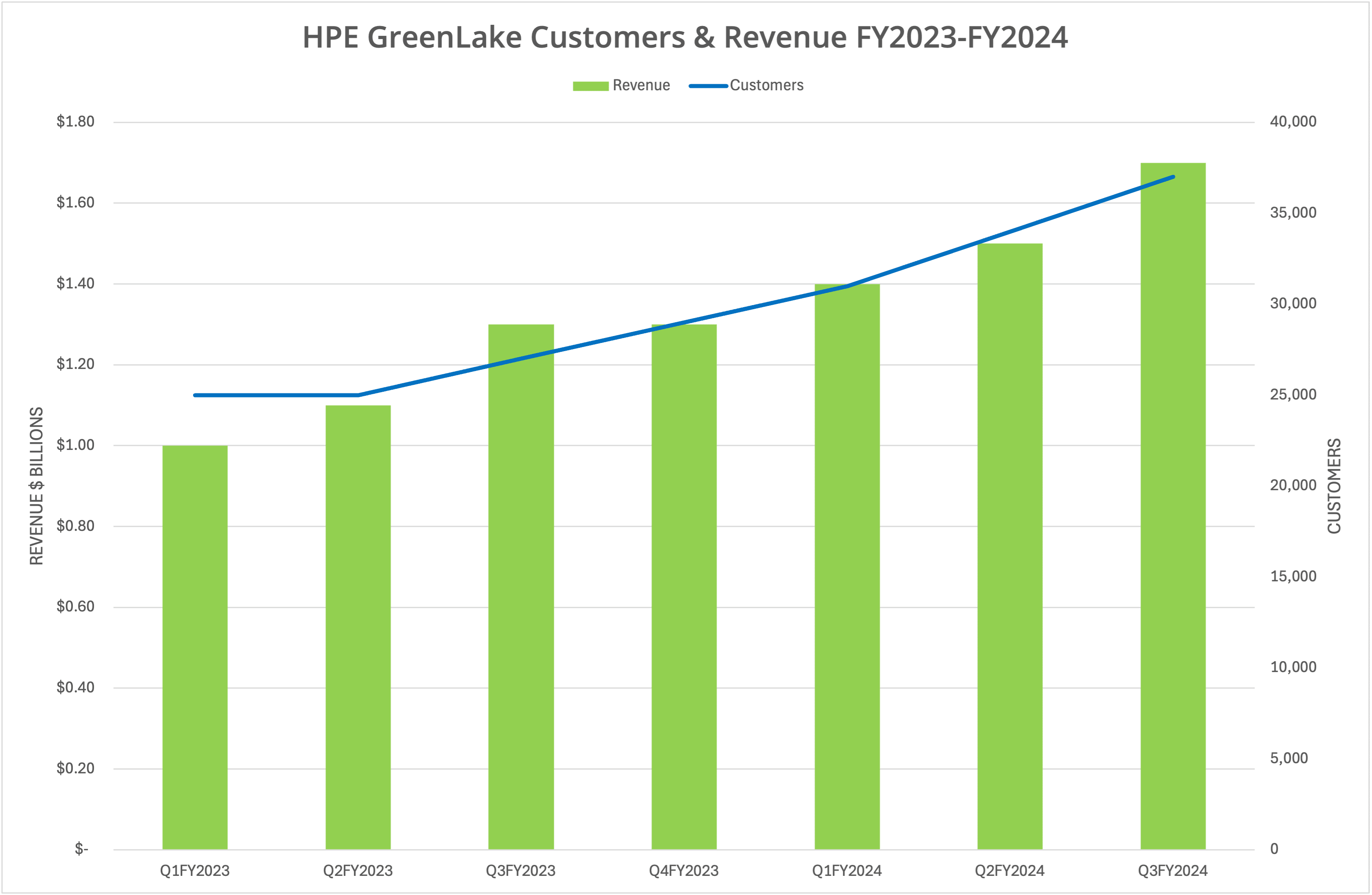

HPE CEO Antonio Neri announced GreenLake at HPE Discover in 2019. His promise was to enable all HPE hardware solutions to be sold under the GreenLake banner within three years. Looking at the latest financial results from HPE, we see that GreenLake has 37,000 customers and an ARR (annual run rate) of $1.7 billion. That sounds impressive, but bear in mind that represents only $45,000 per customer per year and is just 5.8% of HPE’s revenue for FY2023. You can see the HPE-published data in Figure 1.

Dell

Dell Technologies introduced APEX in May 2021, following on from the announcement of “Project APEX” 12 months earlier. Very quickly Dell claimed $1 billion in revenue from the APEX model, as highlighted in the FY2023 outlook report and this interview with CRN. HPE didn’t believe the numbers (see this article).

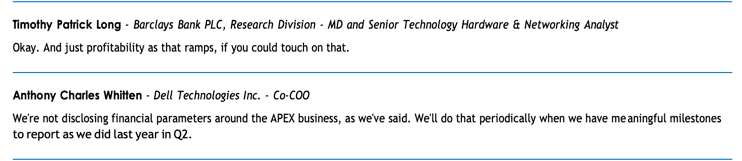

Since the FY2023 report, Dell continues to highlight APEX “momentum” but hasn’t published any specific financial data. In the transcript of the Q1 FY2024 financials call, co-COO Chuck Whitten (no longer with the company) indicated that Dell would not disclose APEX numbers and would only announce them in the future if the results were meaningful (see figure 2, page 13 on the transcript). As APEX no longer gets mentioned in Dell financial publications, we can assume that the APEX business has not grown in any meaningful way and still sits at around only 1% of Dell’s annual revenue.

NetApp

NetApp recently disclosed that Keystone had reached $155 million in TCV (total contract value) in FY2024 (page 14 in the linked document). This doesn’t mean all the revenue will be received in that period (the company hasn’t disclosed ARR data), so even if those sales were achieved in a single year, it still only represents 2.4% of revenue for FY2024. It is more likely that the TCV represents a three-year cycle, so annual revenue might only be just under 1%.

Pure Storage

Pure Storage has pioneered the subscription model from very early in the company’s history, reporting subscription income at around 50% of total revenue, with a constant trend upwards. Subscription doesn’t necessarily mean purchasing per GB and scaling up and down. Customers need to commit to minimum terms and capacities. However, Pure Storage is flexible in how customers can deploy purchased capacity between data centre locations. The company has also introduced innovations like energy credits.

Hitachi Vantara

Although Hitachi Vantara doesn’t publish any financial data, we know the company has a long history of delivering services to customers and has recently revamped its messaging for the EverFlex Infrastructure-as-a-Service offerings. Customers can choose to purchase/lease hardware or deploy infrastructure using a Consumption, Foundation or Managed service offering, which includes Hitachi taking responsibility for every part of the infrastructure deployment and support.

Success or Failure?

Does the lack of revenue (for some vendors) represent a failure in the move towards a subscription-based model? In our opinion, Pure Storage and Hitachi have the best approach to providing storage as a service to their customers. NetApp Keystone rarely gets mentioned in dispatches, and we have struggled to understand the Keystone offerings as they stand today. Dell APEX advancement seems to have stalled, while GreenLake hasn’t gained the customer traction we might have expected, especially when considering all the focus and marketing time the platform receives.

Why are some vendors doing better than others?

Design

Getting back to the earlier discussion on the public cloud, we highlighted how public cloud infrastructure vendors have specifically designed and built solutions that optimise the delivery of computing resources in multi-tenant environments. The transparency around pricing makes it easy to compare solutions offerings across each of the infrastructure components.

Although the “front-end” delivery of products and services to the customer has remained consistent, each vendor platform has optimised the hardware in use, specifically to address the operational and cost overheads incurred in delivering these solutions. This process also includes bringing new solutions to market, such as Arm-based servers with a better TCO compared to typical x86 instances.

If we look at storage and infrastructure design, Pure Storage has been at the forefront of engineering its products specifically for service-based consumption. This process includes standardisation of hardware, financial flexibility in hardware exchange and sharing, plus rapid increases in product density (150TB and 300TB SSDs coming soon).

HPE has also made some advances in hardware optimisation with the introduction of Alletra MP (although the marketing announcements on it have been poor). Customers can acquire and manage some aspects of the hardware through the GreenLake console, but mostly the offerings still appear to be repackaged leases.

Hitachi Vantara has started a process of reimagining the VSP platform, with the launch of VSP One. The results of this transition will take some time to play out. Meanwhile, NetApp has restructured its products to meet customer demand for capacity and performance flash systems. We believe the upcoming disaggregated ONTAP solution could provide NetApp with more flexibility to meet scalable on-demand consumption models.

Only Dell doesn’t appear to have made any concessions in product design to meet a consumption-based service model. Perhaps this is why APEX does not seem to have seen any substantive growth in recent years.

The Architect’s View®

It would be incorrect to assume that “as-a-service” models have been a failure, as we have highlighted some vendors with successful implementations and others with work still to do. However, for many, the income from consumption-based models still sits in the single-digit percentage region despite massive focus and marketing dollars.

Does this matter? Firstly, customers want choice, which consumption models do offer. Based on the varying success of ‘as-a-service” models by vendors, we suggest that some implementations are better than others and so resonate more precisely with customer requirements. For businesses building internal service catalogues, it is definitely easier to align internal business customer spending with infrastructure purchases if your vendor lets you purchase by capacity.

Second, we should ask why on-premises infrastructure vendors introduced these services in the first place. We would argue that Pure Storage, for example, saw the opportunity to implement a new business model and designed its hardware accordingly. Hitachi has a history with large enterprise customers, where the service model works well. HPE was (arguably) looking to find some way to counter the attrition of the public cloud by promising a service-based option for everything. NetApp and Dell seem to have the least clear strategy and/or messaging.

Where do we go next? Some vendors (VAST Data, for example) have abandoned hardware sales and pivoted to software-only models, where subscriptions work well. Unfortunately, this approach won’t work for HPE, NetApp, Pure Storage or Dell, where hardware sales form a core part of the business. Instead, we see several options.

- Hardware optimisation. Vendors need to make their hardware both generic enough to support multi-protocol requirements and to be upgradeable in place with high granularity. Legacy architectures will just be a hinderance to service-based consumption because vendors need to seed each customer site with efficiently scalable technology that isn’t represented by legacy designs.

- Innovation. Vendors need to innovate with new features, improved efficiency and improved reliability, which reduces service calls and delivers enhancements in place. The “Tesla” model of over-the-air upgrades should apply to all on-premises infrastructure, making it easy for vendors to push out new capabilities without the customer needing to get involved.

- Flexible finance. Consumption models shouldn’t be restricted to repackaged leases. Pure Storage (for example) has demonstrated that energy credits and other incentives can be used as sales tools. There is clearly a challenge to deploy infrastructure to a customer that might not be fully utilised, which is where hardware design and innovation become important.

- Better marketing. Finding the details on some of the vendor offerings discussed in this article has been a challenge. Some vendors need to do a better job of explaining the benefits of their solution to customers, including how they function, both operationally and financially.

Finally, we would suggest that vendors need to find some “added value” in transitioning to a service-based model. In storage, for example, vendors can assume the role of the storage administrator by delivering updates and feature enhancements remotely, and by diagnosing and fixing performance problems. But there needs to be more.

Look at the public cloud again and we see features and functionality built onto the core components of storage, compute and networking. Public cloud vendors started with more complex solutions such as managed databases but have quickly expanded into offer managed Kubernetes, serverless functions, AI-based tools, data management tools, security tools and end-user computing.

We believe the traditional infrastructure vendors need to offer more than infrastructure and be moving up the stack to higher-level services. There is some evidence of this strategy in play; Pure Storage with Portworx Data Services and NetApp with BlueXP, for example. With workload repatriation definitely on the agenda (as highlighted by AWS), perhaps now is the time for infrastructure vendors to return to their roots and once again become solutions providers, by building and delivering true public clouds as a service.

Related Content

- On-premises infrastructure – as a service

- Finding the Value-Add of HPE GreenLake

- Dell Technologies Introduces APEX as the “New Dell”

- Delivering True Storage-as-a-Service

- Optimising Public Cloud Service Density

- Is NetApp Becoming a Service Provider?

Copyright (c) 2007-2024 – Post #c3b0 – Brookend Ltd, first published on https://www.architecting.it/blog, do not reproduce without permission.