Last week I watched with interest (from afar) at the announcements from Dell Technologies World. This event is the first in-person since the COVID pandemic but also the first after the spin-off of VMware. Watching the keynotes, it’s clear that Dell Technologies sorely needs a well-articulated hybrid/multi-cloud strategy from where the company is today.

VMware

Let’s start the discussion with VMware. I’ve always been a little confused by the spin-off of VMware from the parent, Dell Technologies. The most obvious explanation for the move was to gain capital to pay off more debt, which was achieved through the vehicle of a special dividend. The official line from VMware is:

The spin-off from Dell Technologies provides VMware increased freedom to execute its multi-cloud strategy, a simplified capital structure and governance model, and additional operational and financial flexibility.

(source)

However, once “sold off”, there will be no further dividends from which Dell Technologies can gain. In the future, the beneficiaries will be the Dell shareholders, mostly Mr Dell himself and his VC partners.

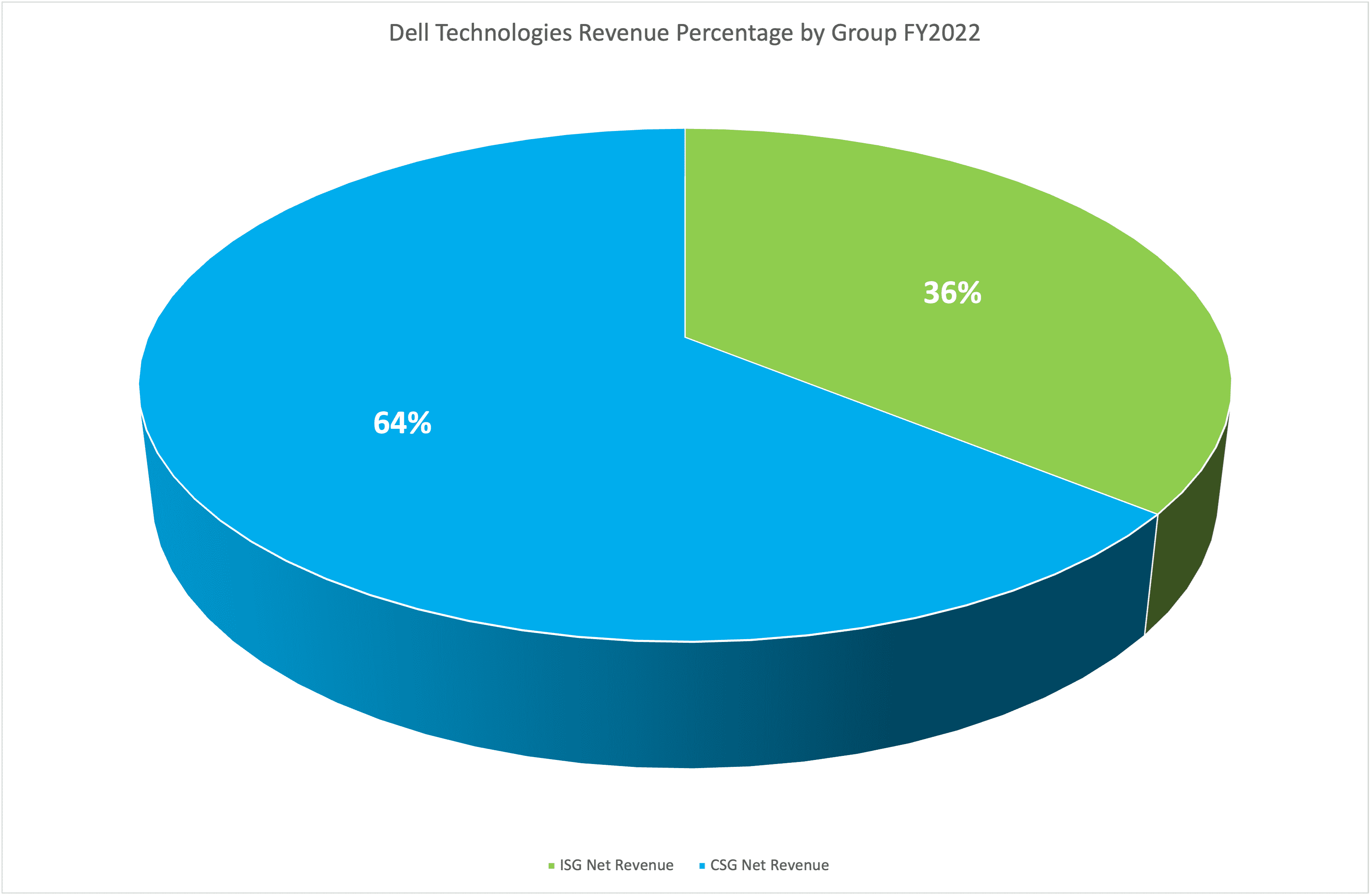

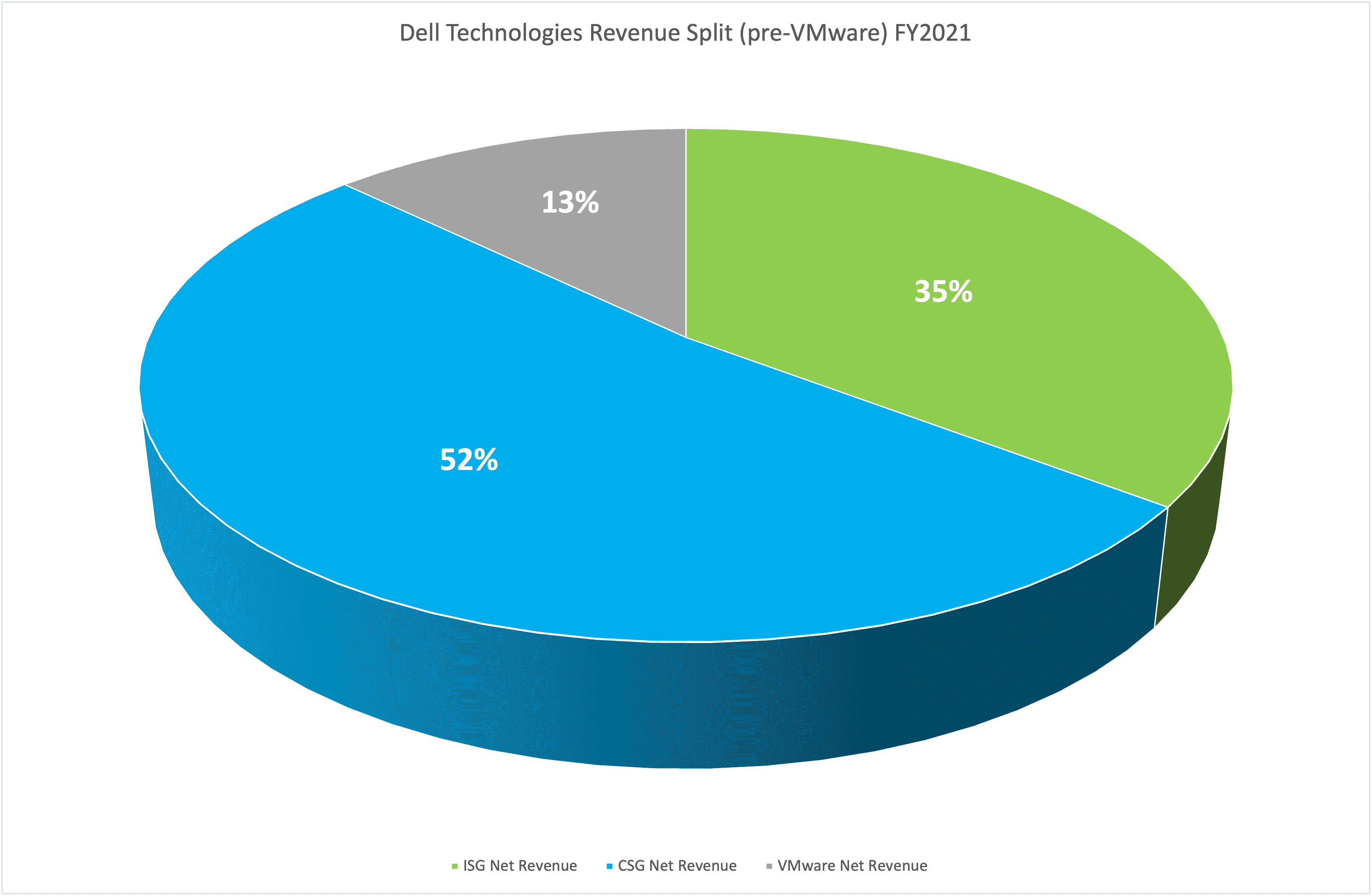

Dell Technologies is divided into two groups – ISG, the old EMC business, servers, and storage – and CSG, the Client Solutions Group, PCs, laptops, and mobile devices for corporate and consumers.

In the financial year before spin-off, VMware represented about 13% of revenue, compared to 35% for ISG and 52% for CSG. With recent increases in CSG revenue, the current split is about 1/3 ISG and 2/3 CSG (see figures 1 & 2). However, VMware delivered the most margin (average of about 31%) compared to ISG at 11% and CSG at just 6%. VMware’s business was also growing, with a positive story on hybrid and multi-cloud.

Growth

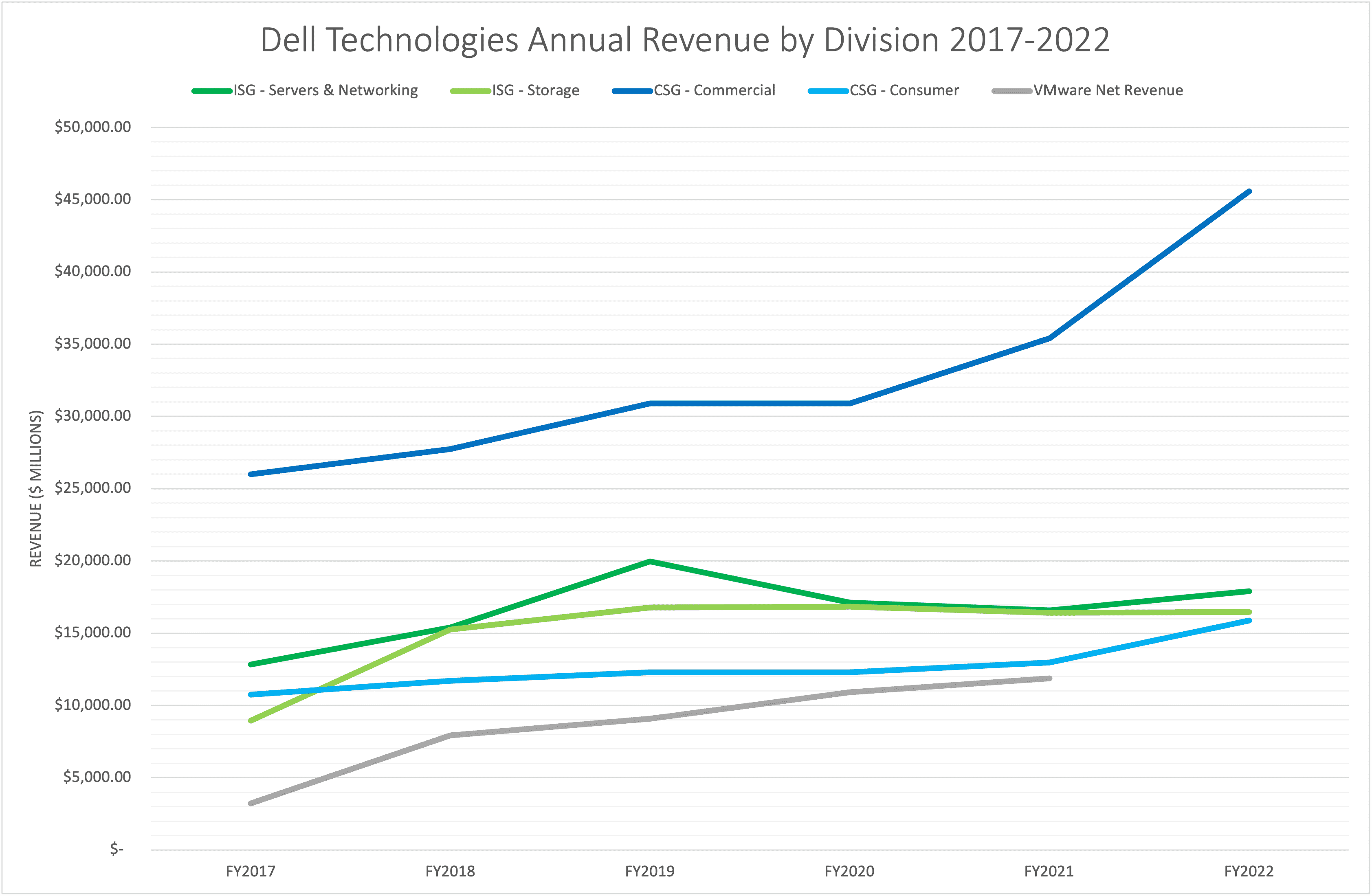

Dell Technologies’ business appears to be doing well, exceeding $100 billion in revenue for FY 2022. Chris Mellor highlights the success in a recent article. However, I disagree with the premise the analysis presents. Chris makes comparisons with HPE, NetApp and IBM, none of which now have (or in some cases, have ever had) a PC business. IBM divested its server business in 2014 and had already sold off the PC business a decade before that. Hewlett Packard split into HPE and HP Inc in 2015, bifurcating into enterprise and PC businesses. NetApp has never been in the server or PC business, selling only storage products and solutions (although partnering on FlexPod and a brief attempt at HCI).

If we dig deeper into Dell’s financials since going public again in 2016, we can see that the growth in revenue has been achieved by CSG and VMware. Specifically, CSG Commercial has achieved around 50% growth from FY2020 to FY2022, whereas ISG has seen only small changes both up and down. Of course, VMware is no longer contributing to the bottom line.

Pandemic

Without any specific insight, it’s hard to know what has driven the revenue increase at CSG Commercial. We could propose everything from greater working from home during the pandemic (and the need for more laptops/computers) to Dell managing the supply chain well, or even the return to work and companies refreshing technology.

Irrespective, CSG is driving Dell’s growth, not ISG. VMware added to that but is no longer in the mix. So, from an enterprise perspective, we should be comparing ISG with the other vendors on Chris’ graph, in which case the growth (or lack of) is relatively similar.

Hybrid Multi-Cloud

The Dell Technologies World 2022 presentations majored on the hybrid multi-cloud emphasis. If I had a dollar for each time I heard a presenter claim, “The on-prem, off-prem debate is over, the future is multi-cloud”, then I’d be a rich man. But what, in the Dell context, does this mean?

We recently blogged about definitions; you can read that discussion here. In a nutshell, hybrid extends a single cloud across others to enhance features and functionality. Multi-cloud enables the use of many deployment models and locations, for example, on-premises, SaaS, co-location or public cloud.

APEX

The Dell Technologies strategy for hybrid multi-cloud is centred around APEX. We covered the launch at DTW in 2021 (read about it here), following on from the first announcement at DTW 2020. The initial offerings covered storage and compute. Dell Technologies now presents three pillars – Compute, Data Storage and Data Protection.

- Compute – solutions based on on-premises server deployments and cloud services using VMware.

- Storage – data storage services on-premises, multi-cloud services (using Faction) and PowerScale (Isilon) for Google Cloud.

- Backup – APEX backup services (delivered by Druva) and PowerProtect DD Virtual Editon (Data Domain). The company also introduced CyberVault capabilities as a service in the public cloud, which appear to be an extension of the vaulting capabilities we saw at Storage Field Day 14 in 2017. At the time, this was known as Isolated Discovery.

Also in the mix is Project Alpine, the initiative to move Dell Technology storage solutions into the public cloud. From the brief demonstration on-stage during DTW, it appears that solutions such as PowerStore will run as virtual instances in the public cloud, for example, on EC2.

Alpine

How easy will it be to transition PowerStore, PowerScale, PowerFlex and ObjectScale into the public cloud? Firstly note there’s no mention in this article of PowerMax, which is generally deployed in high-end enterprise solutions and for mainframe. Some of the capabilities of the PowerMax platform (namely Fibre Channel and mainframe support) have no real public cloud support or requirement. Add in the issue of porting the InfiniBand DVMA (Dynamic Virtual Matrix Architecture), dual nodes per controller and standby power supplies, then we start to get an idea of the scale of the problem.

PowerStore also has similar challenges, as the architecture relies on dual enclosures, shared NVMe drives and mirrored NVRAM. To get an idea of the issues involved in porting a physical hardware appliance into the public cloud, this article we wrote in 2019 discusses how Pure Storage implemented Cloud Block Store by emulating components of FlashArray with virtual instances and local NVMe drives.

Of course, EMC has previously released the midrange Unity as a VSA, with limited support (and resiliency). Deploying a 100% available solution in the public cloud is a totally different challenge that needs to transcend the availability of a single virtual instance, so there’s work to do there. PowerScale is already in Google Cloud, so should be relatively easy to port elsewhere (subject to partnership agreements), while PowerFlex and ObjectScale seem much more logical and more straightforward to implement as they’re essentially software-based solutions. Unfortunately, these platforms are not the majority of ISG sales.

There lies the challenge for Project Alpine – the most successful ISG platforms are those which are intrinsically hardware-dependent and so challenging to port to a software-only model.

Integration

Looking at the broader market and what’s been achieved already, Dell Technologies is in serious catch-up mode. NetApp first released NPS (NetApp Private Storage) in 2014. This is the co-lo solution, which Dell only offered from 2021. In the same year, NetApp also introduced ONTAP running on the public cloud (Cloud ONTAP). This link shows one of the earliest discussions of the Data Fabric. Cloud ONTAP was revamped in 2018, with a fully managed service integrated directly into AWS introduced in September 2021.

Pure Storage introduced Cloud Block Store into AWS in 2019, quickly followed by an implementation in Microsoft Azure. HPE (through the Nimble acquisition) has offered Cloud Volumes (co-located) since 2017.

However, lift and shift of existing products into the public cloud is of no actual use except for two integration points. The first is to enable on-premises and cloud data to co-mingle efficiently. The second is the ability to integrate 3rd party vendor storage with cloud-native APIs, a capability only NetApp offers at present.

It’s fair to say that Dell Technologies is perhaps 3-5 years behind the competition, even if GA products were announced today.

The benchmark for the future has been set by Amazon FSx for NetApp ONTAP and anything less will not provide the level of integration customers will quickly come to expect.

Strategy

So, what is the long-term cloud strategy for Dell Technologies? Back at the beginning of 2019, I suggested that VMware at the head of a newly floated Dell might be the right choice to lead the company into the next decade. After all, VMware has much greater margins than CSG or ISG and should be a growth market for at least the next ten years (if the Tanzu strategy works). That direction now isn’t going to happen.

Having just completed Michael Dell’s latest autobiography (Play Nice But Win), I’m drawn to the conclusion that Mr Dell is 100% focused on delivering the lowest cost computing technology, firstly to the consumer and second to the enterprise. Over the last 38 years, he has been very successful in that approach. However, despite ingesting EMC, Dell Technologies is still two-thirds a PC business, and there is little need for PC technology in the public cloud.

Where, then, does the Dell hybrid multi-cloud strategy go? Another area of current hype is 5G and edge. We’re told that 5G adoption is set to grow massively in the coming decade, but thanks to Gartner, we’ve learned to wait and see how hype cycles play out. We don’t cover telecoms, but I don’t see 5G/edge as a game-changer that will introduce an entirely new market. There are, for example, huge issues around privacy and security of data that need to be resolved first. However, I could be wrong, and there could be a considerable business opportunity putting servers in remote locations.

ISG

Outside of 5G/edge, what hybrid strategy can the ISG division hope to follow? Storage revenue is basically flat, while the market competition is fierce from the likes of VAST, Infinidat & Pure Storage. The multi-cloud strategy is way behind the competition and will take several years to catch up. Competing vendors are starting to build stories around data and adapting to new technologies such as containerisation. Typically, EMC would acquire, but that’s not been a strategy for some time. Instead, Dell Technologies continues to sweat legacy assets.

Software

As hardware margins shrink and the public cloud continues to grow, the logical direction is to develop more software assets. Pure Storage, for example, acquired Portworx in 2020 and has continued to build its fleet management and data platform capabilities in-house. Unfortunately, as we learned at a Tech Field Day event in January 2020, Dell Technologies is following a flawed approach to storage and platform automation. Greater investment in software and data solutions should be the way forward, however Dell Technologies’ strategy appears to be partnering with software companies rather than owning the technology.

The Architect’s View®

The big question for Dell Technologies is whether there is a long-term growth market for infrastructure sold directly to end-user businesses. In the EUC (End-User Computing) market, the answer is, undoubtedly, yes, because everyone needs a device of some sort to access technology. It’s likely (for some time at least) that businesses will provide that technology to their employees to ensure secure access to data.

In the remainder of the market, businesses have three choices – use the public cloud, use co-located services (like Equinix) or use infrastructure on-premises. Increasingly, the squeeze appears to be with on-premises solutions as growth moves to the cloud. This change is not an overnight phenomenon – after all, the modern public cloud era (as defined by AWS) is already 15 years old – but it is happening.

Dell Technologies must take a leap of faith and choose to find alternative revenue streams other than on-premises infrastructure. The change isn’t for today but for ten years’ time when the public cloud and competing vendors will have whittled the business down through a process of attrition.

VMware seemed to be that route forward, but with that option denied, the future appears to be one of merger and consolidation in a long-term shrinking market.

Post #ddde. Copyright (c) 2007-2022 Brookend Ltd. No reproduction in whole or part without permission. The Architect’s View is a registered trademark of Brookend Ltd.