In a little over ten years, Pure Storage has become one of the leading vendors in the enterprise storage industry. However, the IT world is changing as businesses adopt cloud-based solutions and hybrid architectures. Pure Storage has always had ambitions to become the next EMC. But does that make sense in a market where storage is increasingly becoming a commodity and just a part of the on-premises infrastructure? This article looks at the history of Pure Storage and what the future holds for a pure-play storage vendor in the 2020s.

The 2010s was an amazing decade for enterprise storage. Solid-state disks moved from an expensive add-on to the mainstream and arguably are now the primary storage media for the data centre[1]. The market was seeded by EMC in 2008 when SLC-based flash SSDs (known as Enterprise Flash Drives) were introduced into the DMX high-end storage platform. From that point on, incumbent storage vendors added flash support and eventually all-flash systems, while a new breed of all-flash start-ups began developing products and solutions. The race to compete in the all-flash array (AFA) market was on.

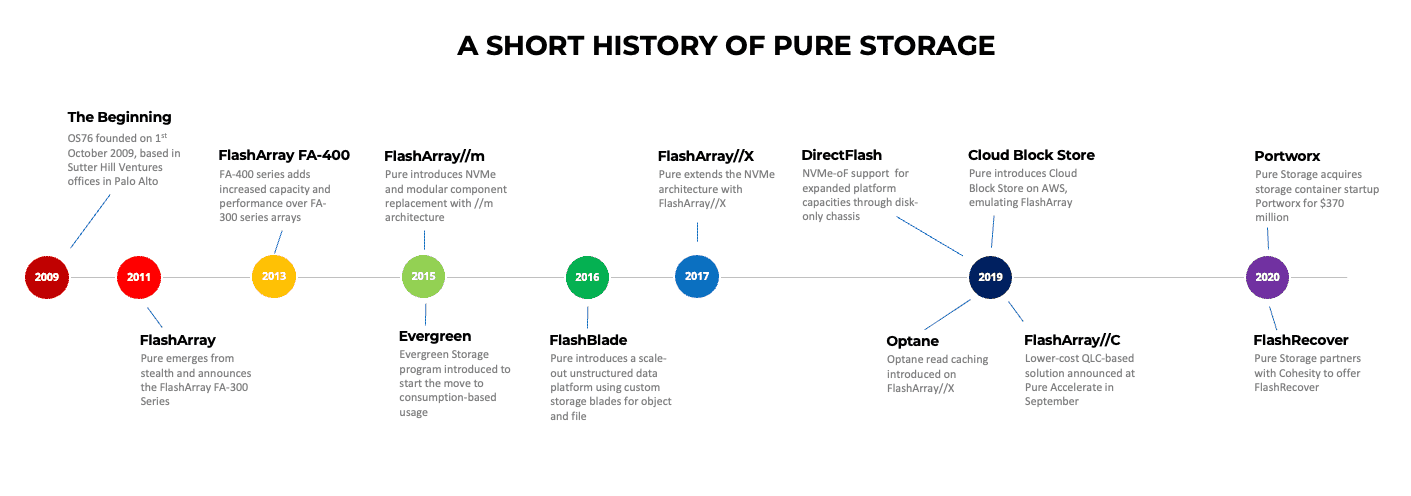

Pure Storage emerged from stealth in August 2011 following two years’ work developing the FlashArray FA-300 series. The original systems used commodity SSDs from Samsung rather than today’s custom flash modules. You can watch one of the earliest presentations on Pure Storage, recorded at Tech Field Day (embedded here).

Competing with the Incumbents

In the early days of FlashArray, Pure Storage competed directly against traditional hybrid and HDD-based EMC platforms. As the most prominent market player, EMC was the obvious company for Pure to challenge, and from a performance perspective, AFAs wipe the floor with traditional HDD-based systems. With the exception of mainframe support, FlashArray can deliver everything offered by Dell EMC high-end and mid-range products (PowerMax, VMAX, Unity and PowerStore) and makes an easy sell in the high-end premium array market.

However, enterprise customers like to minimise their supplier choices, so Pure Storage needed to bring new product lines to market that could widen their TAM (total addressable market) in the data centre.

In the unstructured storage market segment, FlashBlade (announced in 2016, available from January 2017) competes directly with Isilon all-flash solutions. The integration of CompuVerde into FlashArray also now provides Pure Storage with a two-pronged attack vector against the NetApp FAS and AFF platforms.

In the data protection space, Pure Storage acquired StorReduce in 2018 and used that technology to develop and release ObjectEngine the following year as a direct competitor to Data Domain. This product was subsequently shelved in place of a partnership with Cohesity (more on this later).

Outside of the core products, Pure Storage developed FlashStack, a Converged Infrastructure solution competing against the equivalent Dell EMC and NetApp products (vBlock and VxBlock from Dell, FlexPod from NetApp). The portfolio also offers a packaged AI CI solution called AIRI, released in 2018. Dell, HPE, NetApp and others have similarly constructed solutions of AI compute and fast storage.

Although Pure Storage doesn’t break out the individual product lines in their reporting, we know that in 1Q2021, FlashBlade accounted for approximately 15% of revenue with a $250 million run rate. In total, FlashBlade has generated around $1 billion of revenues since general availability. It’s likely that FlashArray continues to be the most significant contributor to the top line.

Cloud

All the products discussed so far are classic data centre solutions. Pure Storage has two cloud-native storage solutions – Cloud Block Store and Portworx.

Cloud Block Store (CBS) is a cloud-native storage solution based on FlashArray. The offering uses multiple virtual instances in AWS or Azure to build a virtual storage array. In the initial deployment, CBS emulated a FlashArray using two instances to represent two controllers and further instances each representing a DirectFlash module. This design was required to meet the restrictions imposed by AWS instances with NVMe drives that didn’t offer persistence or the ability to share volumes between instances. The Azure design is greatly simplified, using only two controllers and Azure Shared Disks. This feature removes the need to use a dedicated instance for storage and should be much cheaper for the customer to run.

The benefits of CBS are multi-fold.

- Homogeneous storage. Both on-premises and cloud storage use the same management tools and data replication process, making it easy to replicate block-based data into or out of the public cloud. The block-based storage offerings from AWS, Azure and GCP typically don’t provide direct exposure to applications and virtual instances outside of their cloud environment.

- Enterprise Features. Pure Storage can offer enterprise-class features such as de-duplication, compression and encryption that are directly compatible with on-premises hardware.

- Storage Savings. De-duplication offers customers potentially significant savings on storage, which at the right scale could cover the cost of the Cloud Block Store licence and virtual infrastructure. Customers using CBS have to pay for the cloud infrastructure and a capacity-based licence from Pure Storage.

CBS isn’t for every business as the cost can be high and only mitigated with many terabytes of deployed capacity. However, the design does represent a growing trend where we see storage solutions inserted between the public cloud infrastructure and the application.

The second cloud-native solution is Portworx. The Portworx Enterprise and px-backup products come from the acquisition of Portworx Inc in September 2020. At $370 million, the Portworx container-attached storage platform is expected to generate significant future revenue (the purchase price includes an assumed $320 million of goodwill). So, big things are expected in the container-attached storage market of the future.

Portworx Enterprise is a distributed persistent storage data plane for Kubernetes environments, implemented within the Kubernetes cluster. It consumes local block storage resources and exports them to applications as Kubernetes Persistent Volumes.

At acquisition, Portworx was arguably the leader in container-attached storage solutions. You can read more about this market and the challengers to Portworx in our analyst eBook (charges apply).

Challenges

While the storage market was evolving into flash systems during the 2010s, the rest of the enterprise market was changing too. The public cloud has seen tremendous adoption with steady double-digit revenue growth from all the major players. Many IT organisations now see Cloud as their primary and default choice for new application deployments. The result of this change has been multi-fold.

- Businesses have become comfortable with (and in many cases, expect) an operational expense model that uses service-based billing rather than outright purchase of hardware.

- Revenue growth in the hardware-based storage market is stagnant and has been for many years. The incumbent IT vendors are effectively fighting with each other for market share while the growth in cloud-based storage continues.

To a certain degree, Pure Storage has addressed the changing market in several ways.

Pure-as-a-Service. The first consumption-based models were introduced by Pure Storage under the Evergreen brand in 2015. Since then, the solution has matured, was expanded in 2018 as Storage-as-a-Service and evolved into Pure-as-a-Service. The current name reflects the evolution of the offering to include all products delivered as services, not just storage.

The Pure-as-a-Service model offers customers the ability to optimise their purchasing decisions while taking advantage of frequent hardware refresh cycles. In theory, Pure Storage is responsible for ensuring the ongoing availability of capacity and for maintenance of the infrastructure deployed in the customer’s data centre or in third-party co-location facilities such as Equinix.

FlashArray//C was introduced in 2019 as a new member of the FlashArray family, using cheaper TLC and QLC NAND flash media. FlashArray//X uses MLC flash. This new product provides Pure Storage access to a wider set of applications that don’t need the sub-millisecond latency of FlashArray//X but does provide the ongoing management flexibility of solid-state storage. However, there is a compromise in that //C systems have a much larger initial capacity footprint. As a result, the solution may not be suitable for smaller enterprise customers.

Principles

While we’re discussing FlashArray//C, it’s worthwhile touching on some of the principles of the Pure Storage business that could affect future growth. IT is in a constant state of flux as new concepts and technologies develop. What was achievable a decade ago is generally outpaced by modern architectures due to exponential growth in performance and capacity. This begs the question as to whether companies should stay with their original principles or look to evolve to meet market requirements. Pure Storage, as a company, holds specific (unwritten) principles that currently dictate the direction and evolution of the company and its products. Part of this approach exists because Pure built up a strong brand presence in its early days. Pure employees are “Puritans”, and the orange colour scheme even has a specific Pantone reference code.

There are also other principles to consider:

- Flash Only – Pure Storage products are all (currently) flash-only and based either on MLC or TLC/QLC designs. HDD or hybrid storage isn’t a consideration, despite the potential demand in the market.

- No Tiering – Pure Storage products do not implement in-product tiering. The concept has been highlighted many times as being excluded from the FlashArray and FlashBlade architecture. The FlashArray//X range currently supports an Intel Optane cache, but not as a tier.

- Storage Only – current products are focused on the storage market, with niche solutions in CI. Pure Storage doesn’t break down the numbers, so we can’t see the extent to which AIRI and FlashStack generate revenue. However, typically these products aren’t discussed often or frequently refreshed.

- Custom Hardware – this last point is perhaps both a blessing and a curse. Custom flash design has been a discussion point for many years, with few companies (Pure, IBM, Violin) taking the plunge to develop solutions around raw NAND chips. Custom designs represent significant R&D development but do offer much more control over the management of flash and the practical lifetime of products. However, the industry is addressing these issues with features like ZNS, which could significantly reduce the competitive advantage of bespoke NAND designs.

If Pure Storage is to continue to grow, some of these principles may have to be revisited and compromises made. This strategy isn’t such a bad thing and unlikely to affect Pure’s corporate image.

Competing as an Incumbent

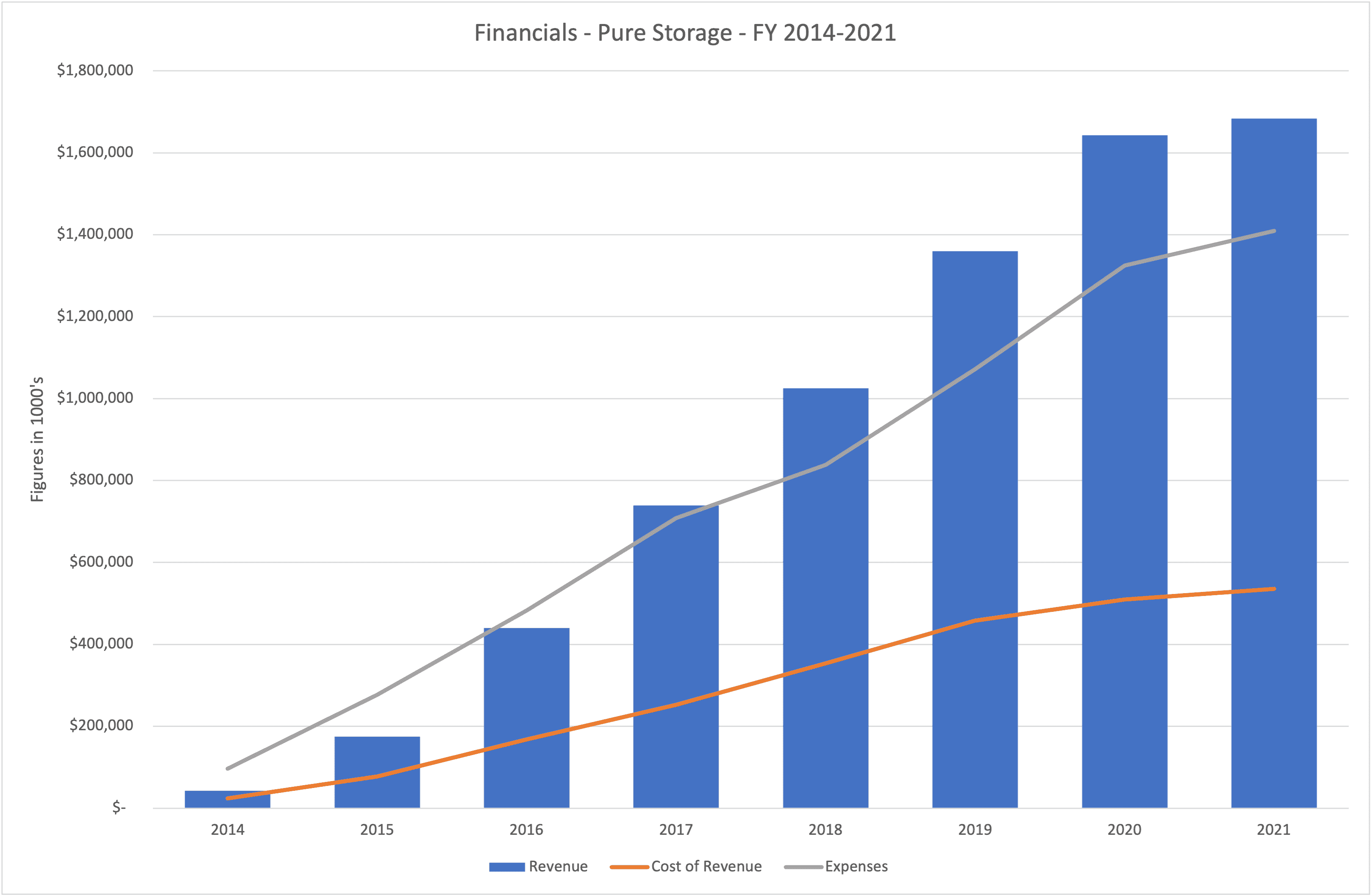

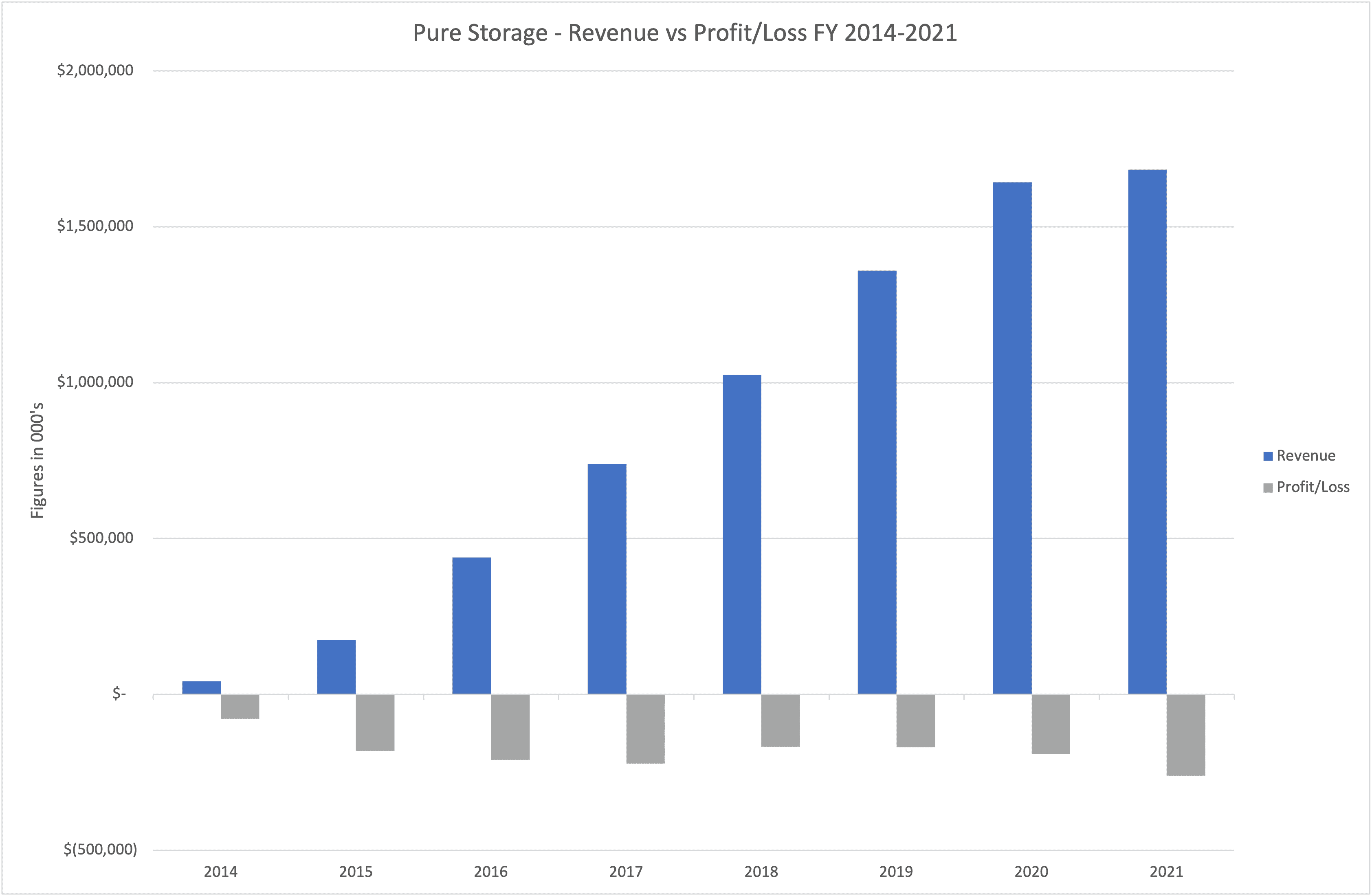

As we highlighted earlier, the enterprise storage market is essentially stagnant, which means the incumbent market vendors are competing with each other for a relatively fixed market share in terms of revenue. Having said that, Pure Storage has been successful at increasing revenue consistently on an annual basis (see figure 2).

The coronavirus pandemic flattened growth in FY2021; however, in 1Q of FY2022, growth has returned. But Pure Storage is yet to make a profit. Losses are increasing, albeit only slightly, despite a reduction in the cost of revenue and expenses (more details in figure 3).

In the on-premises market, Dell EMC has revised its portfolio with the all-flash PowerStore. This offering seems to be a reworked product based on the Clariion/VNX/ Unity family and lacks many of the flexibility features offered by FlashArray. This aspect is important because the “as-a-Service” model needs highly granular products that can be easily deployed and extended in customer data centres.

HPE has moved to brand the Primera and Nimble lines under the Alletra name in an attempt to move its portfolio of own-brand storage to as-a-service offerings. This transformation represents further obfuscation of the hardware detailed behind the HPE storage platforms and is a change we’ve seen play out for several years.

NetApp continues to sell on-premises ONTAP and all-flash FAS (AFF) solutions but is making a broader play for integration with the public cloud. The company already has partnerships with Azure and GCP, directly integrating into the public cloud APIs and offering a true storage service for the public cloud. In a recent earnings announcement, NetApp showed strong figures, with much of the growth coming from the public cloud.

IBM’s storage business appears to be quietly imploding, with quarterly revenue reductions. Hitachi Vantara still sells hardware products but has a much greater focus on solutions.

Outside of the big vendors, new players are already attracting attention. VAST Data Inc. is evolving quickly, with a transformed business model and over a $150 million run rate (February 2021). StorONE is a minnow looking to be the next big storage company, with an architecture that exploits Intel Optane, NAND Flash and HDDs. The founders have history, selling Storwize to IBM in 2010. Then there are a raft of software-defined storage companies and the risk from the public cloud.

Becoming EMC

At the top of this article, we discussed Pure Storage becoming the next EMC. Although this suggestion does have a degree of irony, looking back in time, we can see that EMC became a hugely successful company through disaggregation and the purchase of one key asset – VMware. The acquisition of VMware could be seen as inspired or lucky, depending on your point of view. Joe Tucci aimed to build a portfolio of companies – the EMC Federation – all of which would be loosely coupled and co-operative, adding to the overall revenue of the parent entity. In the end, this model didn’t work, and only core EMC storage and VMware provided the bulk of revenue. Dell eventually dissolved the Federation a few years after the EMC acquisition.

Pure Storage needs to find new market segments that will expand the business. Further expansion into infrastructure looks like a non-starter. The margins are small, and the competition is fierce. Instead, a more logical approach would be to move “up the stack” and focus on the value of data rather than storage.

The partnership with Cohesity represents an element of this strategy, bringing a data protection solution for customers that uses FlashBlade at the back end. However, the implementation is limited to using Pure Storage products as storage capacity and not exploiting the capabilities of FlashBlade.

Pure Storage needs to acquire a data protection company and integrate its hardware solutions more tightly with backup software. In addition, the company should consider moving into the data analytics space, with tightly coupled architectures that exploit the benefit of on-premises hardware but can also be deployed in the public cloud. As a third strand, the Portworx acquisition needs to demonstrate unique capabilities that come from integrating the PX-Enterprise products with on-premises hardware. Kubernetes-based storage still has gaps that need to be filled.

The Architect’s View™

The legacy of the EMC Federation model still pervades the IT industry. Acquisitions like Kasten (Veeam), Hedvig (Commvault) and new ventures like Metallic (also Commvault) are retained as independent brands. Pure Storage has already done the same with Portworx, as both a brand and product under the Pure Storage portfolio.

Ultimately this could be the future direction Pure Storage will need to take. This strategy is well documented and understood, from Andy Grove’s strategic inflection points in “Only the Paranoid Survive” to the zoned development of new businesses and product lines in Geoffrey A Moore’s “Zone to Win”. Pure Storage needs additional and more diverse product lines, preferably software-based and dealing with data rather than infrastructure.

Hardware has been a growth business since the turn of the 2000s but has a high COGS compared to software. Hybrid cloud has ushered in a model where infrastructure is cheap to use and readily available at a near-infinite scale. In the future, only the largest (or most paranoid) of enterprises will need dedicated on-premises infrastructure. While FlashBlade and FlashArray will play a part, the future for Pure Storage is definitely data and the value that can be derived from it.

You can find more Pure Storage content at our dedicated microsite. Pure Storage is a Tracked Vendor by Architecting IT in storage systems and software-defined storage. Pure Storage has been a customer of Brookend Limited prior to 2021.

[1] Dell PowerMax, PowerStore, HPE Primera are all flash-only products

Copyright (c) 2007-2021 – Post #6a46 – Brookend Ltd, first published on https://www.architecting.it/blog, do not reproduce without permission.