NetApp recently reported less than optimal Q3 FY2023 financial results, with a decline in revenue from all-flash and public cloud product lines. As businesses reign in spending and look to optimise the use of public cloud resources, could the Spot portfolio provide an opportunity for NetApp to make up for lost revenue?

Background

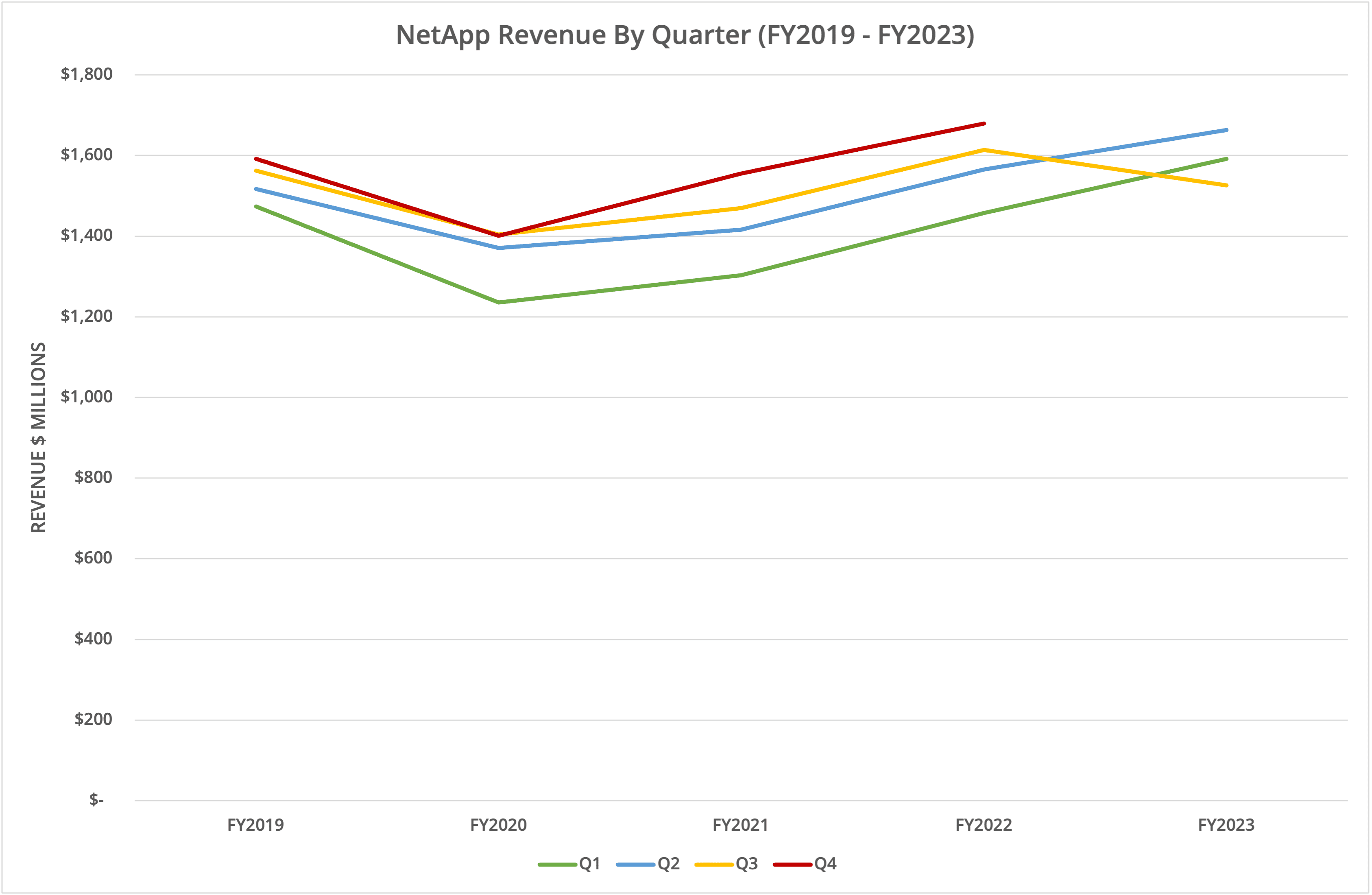

NetApp’s Q3 FY2023 figures were disappointing compared to the growth numbers reported since 2020. Figure 1 shows the year-on-year decline of 5.4%, compared to 9.2% and 6.2% growth in the previous two quarters, respectively.

All infrastructure businesses are experiencing some downturn, with the mini boom and bust created by the COVID pandemic finally showing through on revenue and the bottom line. The Ukraine war and global energy prices have focused companies on rightsizing their use of technology, putting off buying decisions and “sweating” assets. We discussed some of these issues in a recent blog post (here) that looks at workload repatriation on-premises.

Spot On

The interesting aspect of NetApp’s current strategy is the development of an almost parallel business that focuses on workload optimisation. The start-up Spot was acquired in 2020, followed by Fylamynt (February 2022), Cloudcheckr (October 2021), Instaclustr (April 2022), Data Mechanics (June 2021), Cloudhawk and CloudJumper (April 2020). In a February 2022 post, we suggested that all these acquisitions were creating an essentially separate business, built and run by Anthony Lye, who subsequently left the firm for Palantir in July 2022.

Portfolio

With so many acquisitions, how are these diverse solutions being brought together into a consistent portfolio? NetApp defines four categories:

- FinOps

- Spot Eco – reserved instance (RI) and savings plans virtual instance optimisation.

- Eco Reports – enhanced billing and reporting to manage RI and dynamic workloads.

- Cloud Analyser – finds anomalies and optimises public cloud usage, through rightsizing, committed usage and purchasing strategies.

- Cloudcheckr – appears to duplicate the optimisation features of Eco, but also adds security monitoring and compliance.

- Containers

- Ocean Suite – Ocean, Ocean for Spark and Ocean for Continuous Delivery, three Spot capabilities for orchestration of container-based workloads.

- Infrastructure

- Elastigroup – application scaling and rebalancing management.

- Spot Security – Security analysis and threat detection.

- Desktop

- Spot PC – Desktop management and optimisation.

Trying to rationalise the solutions and options available isn’t straightforward. The Spot portfolio is not directly listed through the NetApp website, but instead is at https://spot.io/ and in an interesting piece of inception, Instaclustr also operates as a separate website (at https://www.instaclustr.com/) with a tagline of “now part of Spot by NetApp”. The Instaclustr solutions are focused on managed database provisioning, which seems a little different from the optimisation capabilities of Spot.

Measure, Optimise, Implement

There’s no doubt that NetApp has acquired a plethora of tools from which to build out an optimisation portfolio. So far, though, there seems to be some overlap. The Cloudcheckr functionality appears to duplicate some of the original Spot capability, while there’s no obvious optimisation for container-based workloads and storage. None of the cloud offerings appears to encompass on-premises workloads, which would be relevant for the current trend of application rebalancing (including repatriation – see here and here).

- NetApp BlueXP – a new experience?

- NetApp Announces Q1 FY2023 Results

- NetApp delivers solid FY2022 growth, but there’s work to do in public cloud messaging

All these options appear to focus on the retroactive analysis of existing workloads. As we discussed in a podcast recorded in January 2022, optimisation includes making use of existing resources efficiently while considering restacking on alternative clouds. The third step in optimisation is to direct new workloads to the most appropriate platform before deployment. We believe this capability exists within Spot Eco but doesn’t include the ability to assess on-premises infrastructure.

The Bottom Line

The Spot portfolio does feel like a “work in progress” and, in many ways, feels similar to the early days of the NetApp Data Fabric discussions. From statements in the recent financial announcement, it’s unclear how much revenue Spot contributes to the bottom line. This excerpt from the Q&A session gives us no real clue (or maybe it actually does):

“Spot has done well, and Cloud Insights has stabilized and met our internal targets. So, the shortfall was mostly from the cloud storage business. I think that in Spot, it’s the opposite, right? When people are concerned about cost optimization, Spot is a perfect tool for that, and they had a good quarter.”

Q3 FY2023 Earnings Call

So, in a downturn situation, surely the Spot tools should be selling themselves? We just don’t know.

The Architect’s View®

The NetApp left brain that sells storage both on-premises and in the public cloud is a well-defined business. Despite best efforts, even the public cloud isn’t immune to a customer spending slowdown, as highlighted in the latest financial figures. The NetApp right brain, focusing on optimisation and efficiency, still seems to be in its infancy and could have lost its biggest advocate with the departure of Anthony Lye.

- NetApp – Transformation, Bifurcation or Re-invention?

- Can NetApp Reach Escape Velocity to the Public Cloud?

As yet, the right-brain business doesn’t seem to have a clear strategy or enough momentum to even be highlighted as a line item on the accounts. So, does the Spot portfolio have a long-term future within NetApp, or might we see the divestment of those investments?

We believe that the idea of customers having choices in data placement, with the ability to optimise workload deployment, addresses the two main aspects of how to consume public and private clouds in a hybrid way. At present, the hybrid storage capabilities are evolving successfully, but the Spot side needs more work to bring in on-premises capabilities, including orchestration.

We also think that the left-right brained NetApp needs greater development of the corpus callosum that links these two apparently independent business lines. There’s so much more that can be done when optimisation covers the choice to move data to compute or compute to data. Greater integration and synergy between both business lines would make the whole NetApp stronger. The vision isn’t clear yet, and we hope there’s an Anthony Lye 2.0 in place to carry it forward.

Copyright (c) 2007-2023 – Post #e344 – Brookend Ltd, first published on https://www.architecting.it/blog, do not reproduce without permission.