NetApp has announced first quarter FY2023 results. Revenue is up, ARR for public cloud is up. We take a quick look at the details to determine if the company has finally cracked the public cloud market.

We last looked at NetApp’s financial announcements in June 2022, with the FY2022 results. At the time, the data showed solid growth across the board. Since then, the main architect of the NetApp public cloud strategy, Anthony Lye, has left the company. Over the last few years, NetApp has made many acquisitions that form the basis of the company’s cloud products. There’s a dual approach with one strand focused on building out a hybrid cloud storage framework, while the other helps customers optimise cloud resource usage.

ARR

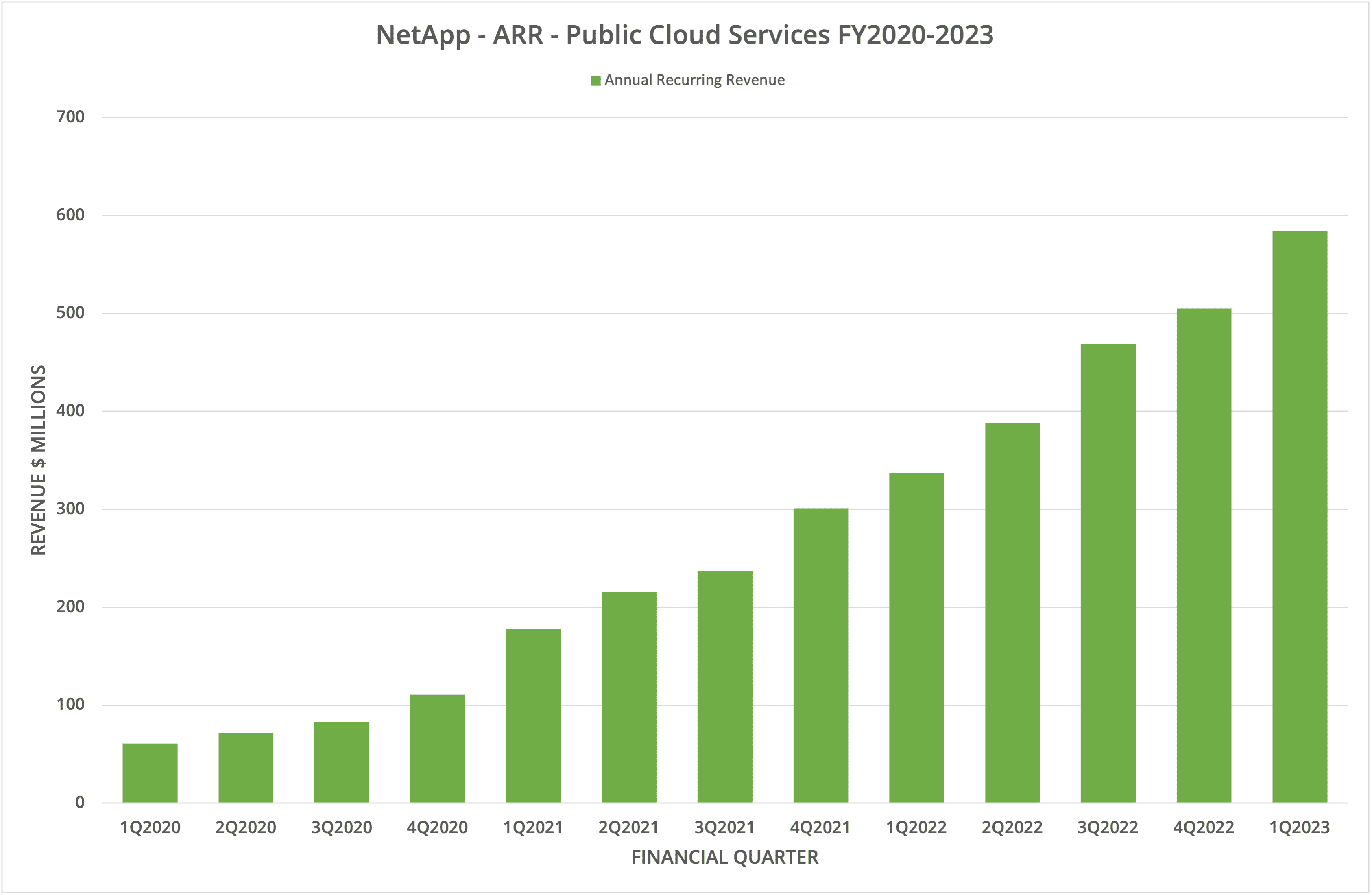

What does the data indicate? We’ve been able to put together a slide (figure 1) that details annual recurring revenue for public cloud services since NetApp started breaking the data out separately. The graph shows an accelerating growth from $61 million in Q1 FY2020 to $584 million in the current data (Q1 2023). Public cloud revenue now forms a significant part of NetApp’s income (currently 8% and growing) – although this percentage is revenue, not ARR.

Side Note: I tend to think of annual recurring revenue as an “aspiration” of future income, whereas revenue stated in official financials statements is a much more accurate view of the real state of play. We will continue to watch both sets of data over time.

Revenue Replacement

Of course, the first issue that springs to mind when a new line of revenue becomes established within an existing business is whether that source is now replacing previous streams of income. This scenario is definitely one that occurred with technology companies that replaced storage sales with HCI, for example.

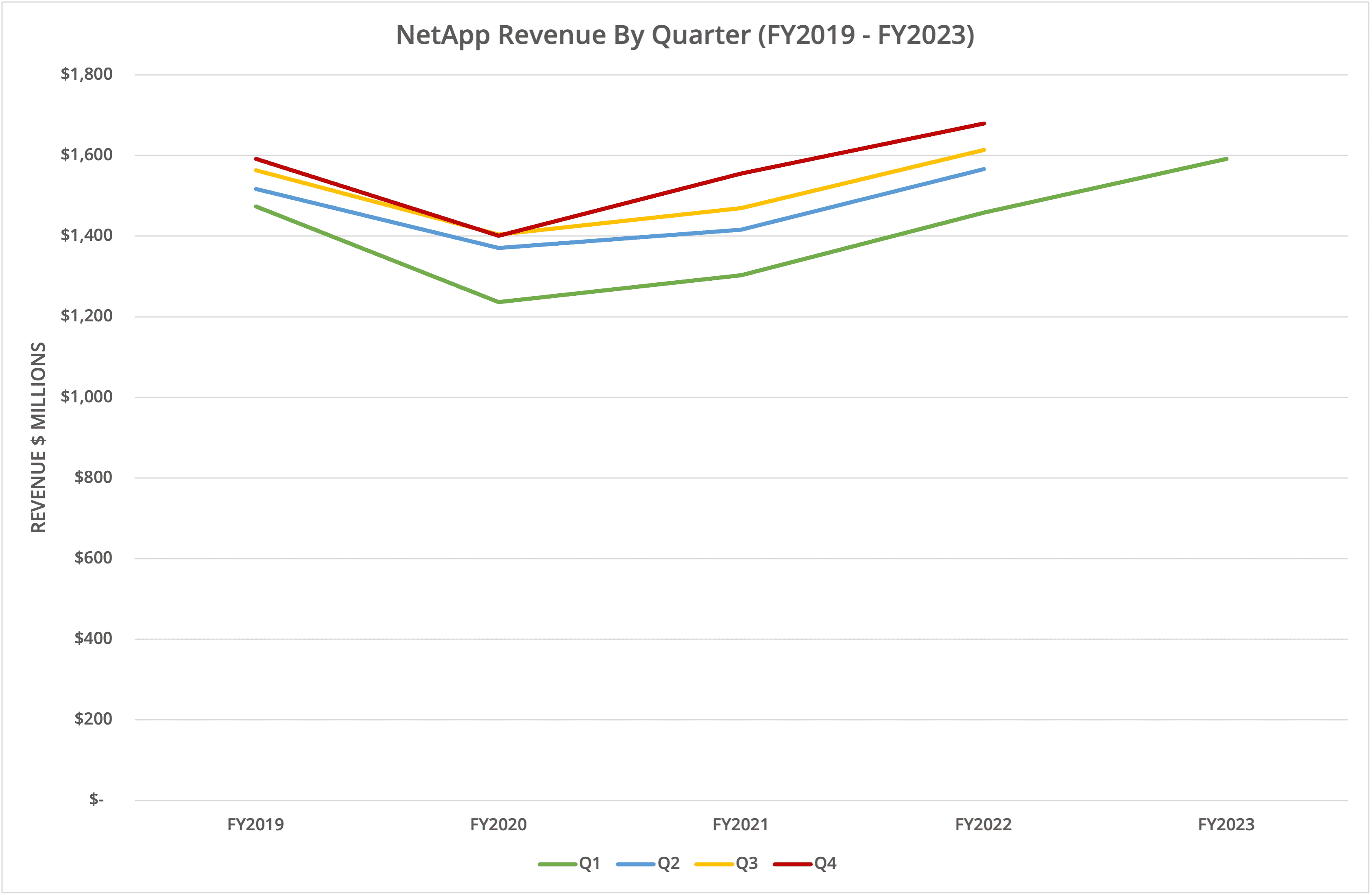

Figure 2 shows NetApp revenue by quarter from FY 2019 to FY2023. After the COVID-19 dip of FY2020, revenues seem to be back on track and growing. Q1 is always a “down” quarter compared to the others, so we should be looking for equivalent growth in the remainder of the year. From what we can see, the data doesn’t show any revenue replacement taking place, but the growth in product hardware year-on-year is slightly down and appears over time to be relatively flat.

The Architect’s View®

We’ve said before that infrastructure vendors can’t fight the rising tide that is the adoption of the public cloud. Working with hyper-scalers is the only route forward, as businesses settle into an equilibrium that uses resources in the cloud (SaaS and IaaS) and on-premises. For each business, the percentage of applications in each location will range from 0-100%. Some businesses will be 100% cloud, some won’t use cloud at all.

NetApp continues to make progress in delivering services to the hybrid market. However, we’d like to understand how much of this growth is attributed to the existing storage business ported to the cloud and how much to new features like Spot and workload optimisation. If each cloud service offering can be grown, the future looks bright.

The $64,000 question though, is who replaces Anthony Lye, and what will their strategy be for extending NetApp’s future public cloud service offerings?

For more information on our coverage of NetApp, visit our dedicated NetApp Microsite. NetApp is a tracked vendor for Data Storage, Data Protection, and Cloud Storage.

Copyright (c) 2007-2022 – Post #d8de – Brookend Ltd, first published on https://www.architecting.it/blog, do not reproduce without permission. NetApp is a client of Brookend Ltd.