NetApp, Inc. has announced financial results for the third quarter of FY2025, ending 24th January 2025. Revenue rose 2.2% to $1.64 billion compared to Q3 FY2024, although that figure was slightly down on the previous quarter. All-flash ARR increased by 10%, while the Public Cloud segment increased by 15.2%.

Background

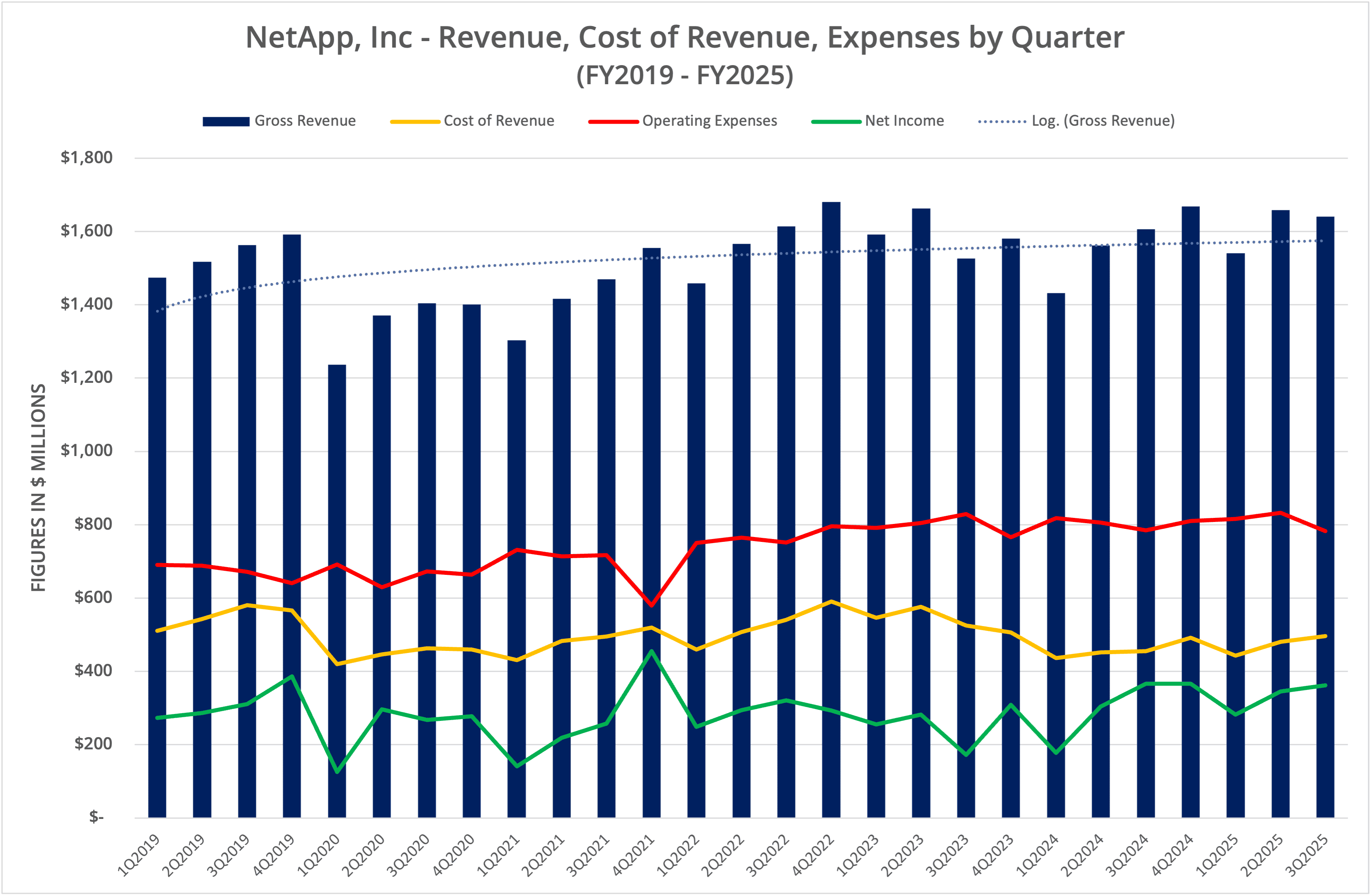

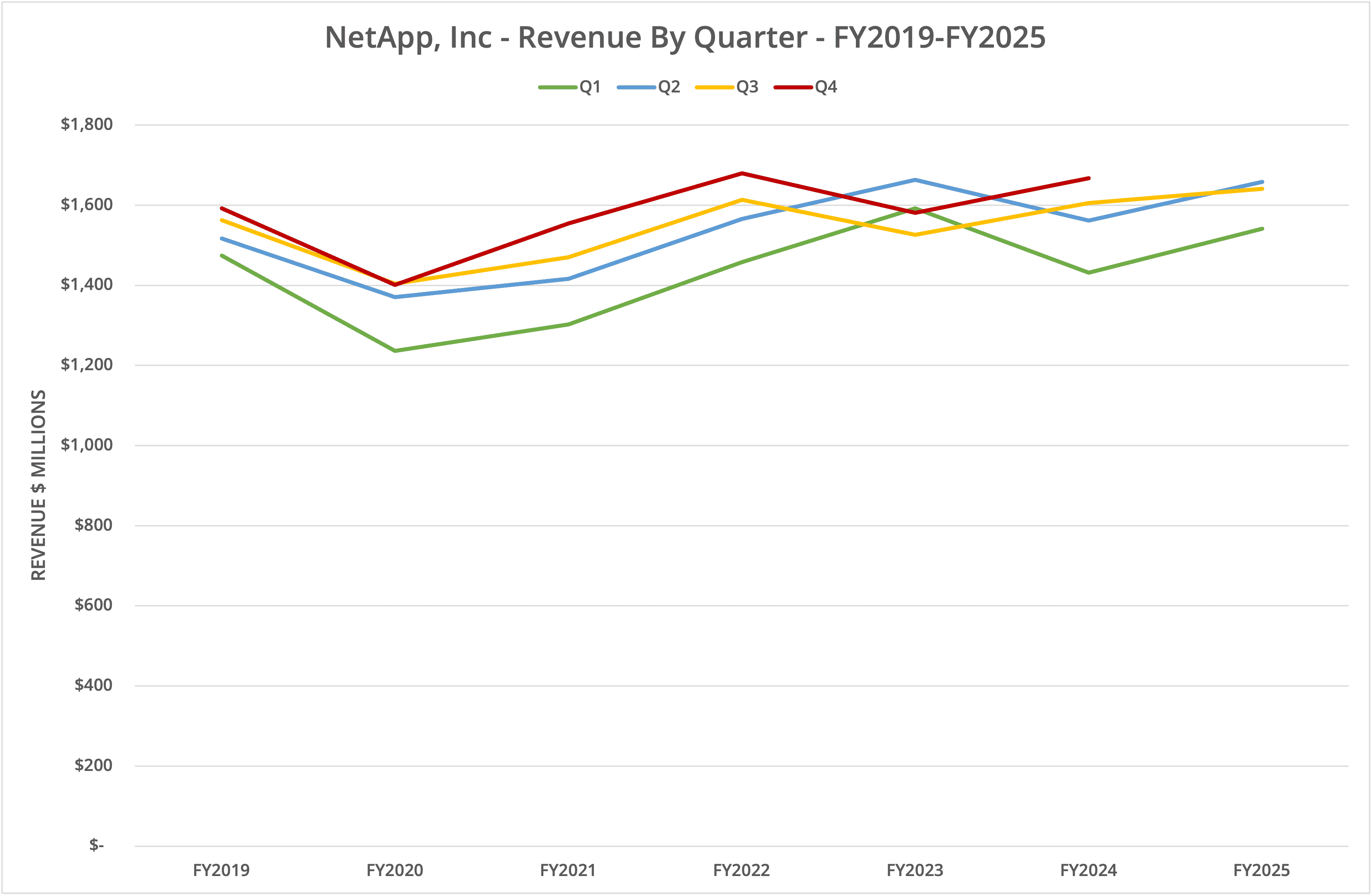

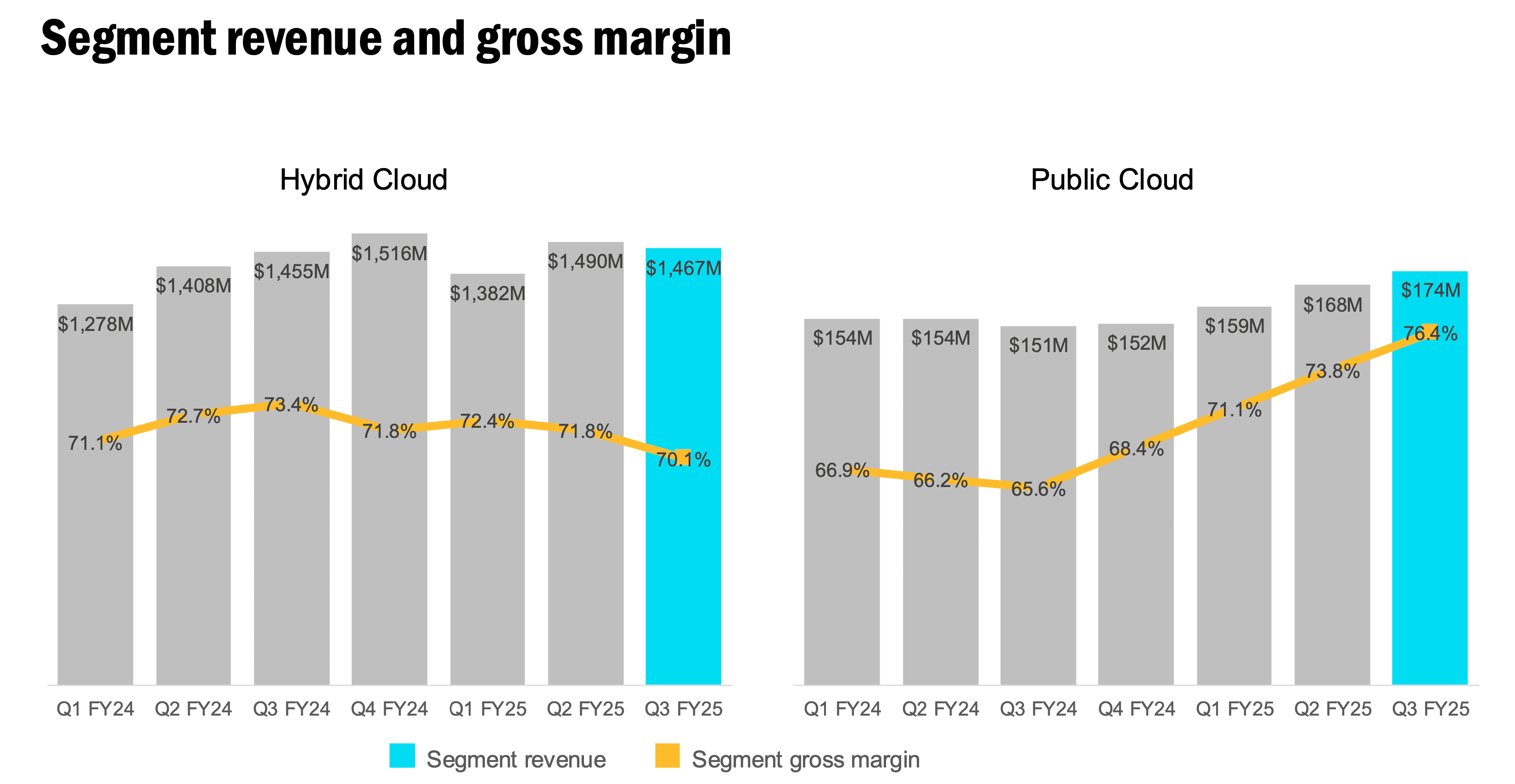

NetApp, Inc. has declared financial results for Q3 FY2025. Revenue for the period, which ended on 24th January 2025, was $1.64 billion, up 2.2% on Q3 FY2024. Sequentially, sales were down marginally by 1%. While product sales were down, all-flash ARR increased by 10% (representing an increasing change in the mix of products away from hybrid systems), and public cloud revenues increased year-on-year by 15.2%. We present the data in four graphs labelled Figures 1 to 4.

All-Flash

As we highlighted in our analysis last quarter, all-flash systems sales continue to be the star of the show, increasing ARR but not significantly increasing overall revenue (in fact for the quarter, product sales declined sequentially).

NetApp continues to evolve its hardware portfolio, recently introducing additional products in the ASA range for smaller entry-point requirements. The new ASA A20, for example, starts at 15TB raw, with the top-end systems delivering 2.67PB of all-flash capacity.

With the addition of the C-series and new AFF models announced last year (which align with the ASA products above), NetApp has worked hard to deliver a comprehensive and refreshed hardware portfolio.

Public Cloud

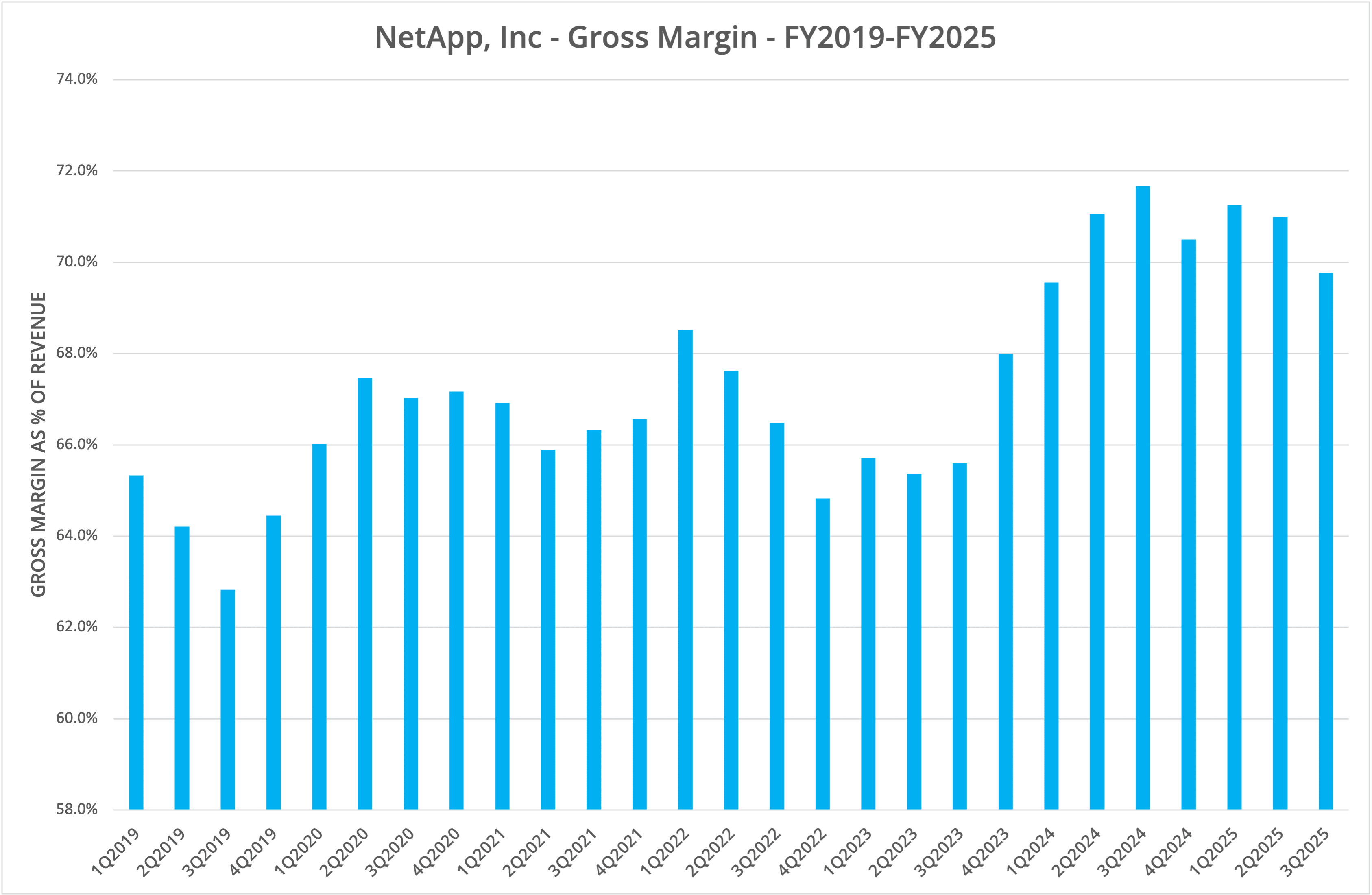

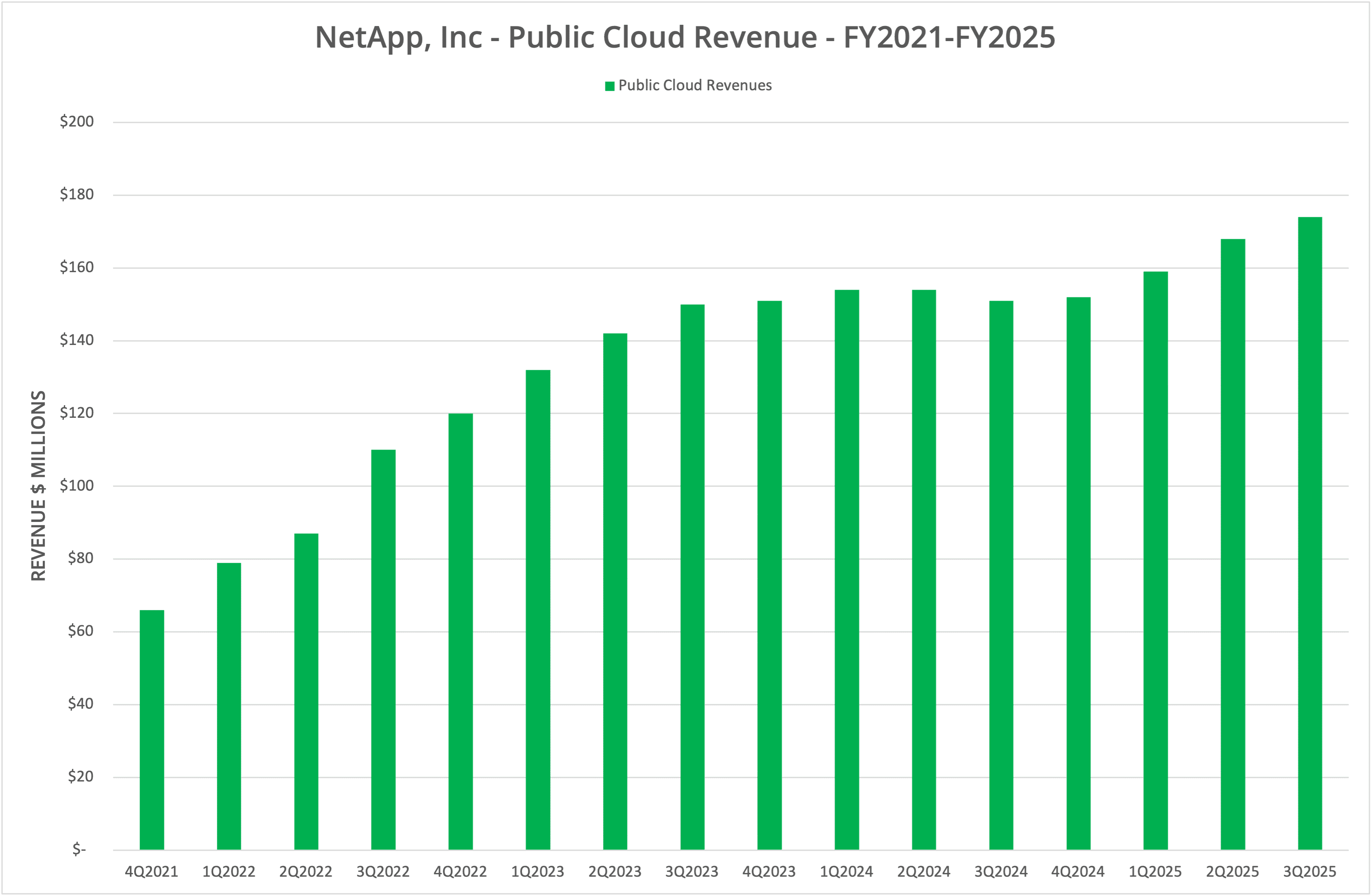

Elsewhere, public cloud revenue continues to increase, with a 15.2% year-on-year jump for the quarter to $174 million. It’s worth noting that public cloud revenues represent only 10.6% of NetApp’s revenue in the current quarter but have a much higher and increasing margin (see Figure 5). There’s some way to go before the public cloud segment can replace revenue that could be lost elsewhere.

Spot

One big piece of news during the quarter was the announcement on the offloading of most of the Spot business. As we’ve highlighted for some time, the Spot portfolio didn’t align well with the remainder of the NetApp storage business (see this post as an example).

Flexera will acquire the majority of the Spot portfolio for around $100 million (see our coverage here). During the post-results earnings call, NetApp indicated that the projected Q4 decline in Public Cloud segment revenue would be around $15 million, and the overall contribution annually from the Spot business was approximately $94 million. These numbers highlight a poor return on what was possibly $1.3 billion in acquisitions, of which around $600 million are being offloaded.

So, we expect the Public Cloud segment to be flat in Q4, aligning with the loss in revenue from the Spot portfolio.

IDI

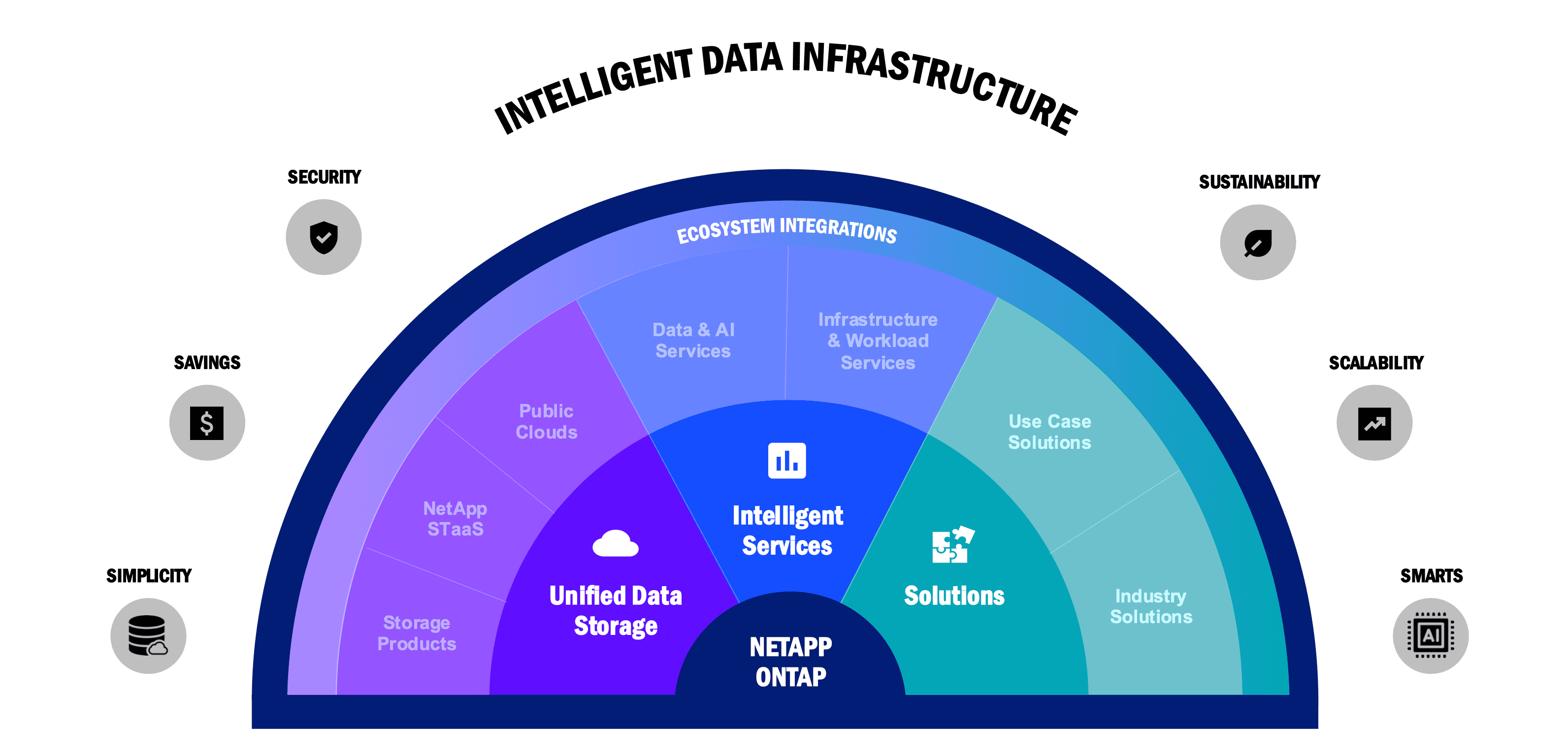

Now that a clear decision has been made on the future of the non-hardware side of the business, we can revisit the image shown as Figure 6, which visualises the “Intelligent Data Infrastructure” approach NetApp will pursue during 2025. The three pillars (Unified Storage, Intelligent Services & Solutions) are much clearer to rationalise, although arguably, the graphic should either show each segment in equal size or provide greater emphasis on Intelligent Services, which is likely to generate the most margin in the future.

Services

We highlight the “services” aspect because this is an area the entire IT market is embracing. Consumer businesses such as Apple, Inc. have huge services revenue, despite traditionally operating in a product market. Similarly, SaaS has expanded significantly in the enterprise market, as has storage-as-a-service and data protection-as-a-service.

NetApp reported a 60% rise in revenue from its service platform, Keystone, although no specific revenue number was reported. In October 2024 we analysed the storage-as-a-service market and calculated that Keystone could conceivably represent only 1% of NetApp’s annual revenue.

The Architect’s View®

2025 might be a pivotal year for NetApp. The hardware platforms have been revamped, but there is significant competition for both traditional storage products and newer architectures, such as that offered by VAST Data or Weka. We expect that NetApp will provide details of a new scale-out architecture later in the year, which could represent an opportunity to support a range of new protocols, such as structured data tables and a fully integrated object solution.

Will 2025 be the year in which NetApp moves away from ONTAP? Probably not. It is more likely that ONTAP evolves to support true scale-out storage, rather than the node-pair clustering in the current platform.

Elsewhere, the Intelligent Services segment needs to evolve solutions that drive additional revenue, preferably with a service model that increases recurring sales.

If we have one negative comment on the sale of the Spot portfolio, it’s the expected IT recession that will accompany the end of the AI boom. Eventually, the current frenzy for AI will abate, leaving IT spending budgets in disarray, as excessive funds were diverted to the development of GenAI solutions and AI agents. At this point, optimisation and efficiency will once again be on the agenda. However, for NetApp, the Spot portfolio will be a distant memory.

As we’ve said, 2025 could be an important year for NetApp, one that redefines the long-term future of the business.

Related Posts

- X-Ray: NetApp, Inc.

- Analysis: NetApp offloads FinOps assets to Flexera

- Analysis: NetApp announces Q2 FY2025 financial results

- Research Note: NetApp teases new disaggregated storage architecture for ONTAP at Insight 2024

Copyright (c) 2007-2024 – Post #2b2b – Brookend Limited, first published on https://www.architecting.it/blog, do not reproduce without permission. NetApp is a Tracked Vendor for data storage solutions.