NetApp has announced financial results for the fourth quarter and full year of FY2024, ending 26th April 2024. For the quarter, revenue was up 5.5% year-on-year. However, for the full year, revenue was down 1%, while ARR for the Public Cloud remained relatively flat. All-flash array systems remain the highlight of the results as NetApp continues to focus on core competencies.

Background

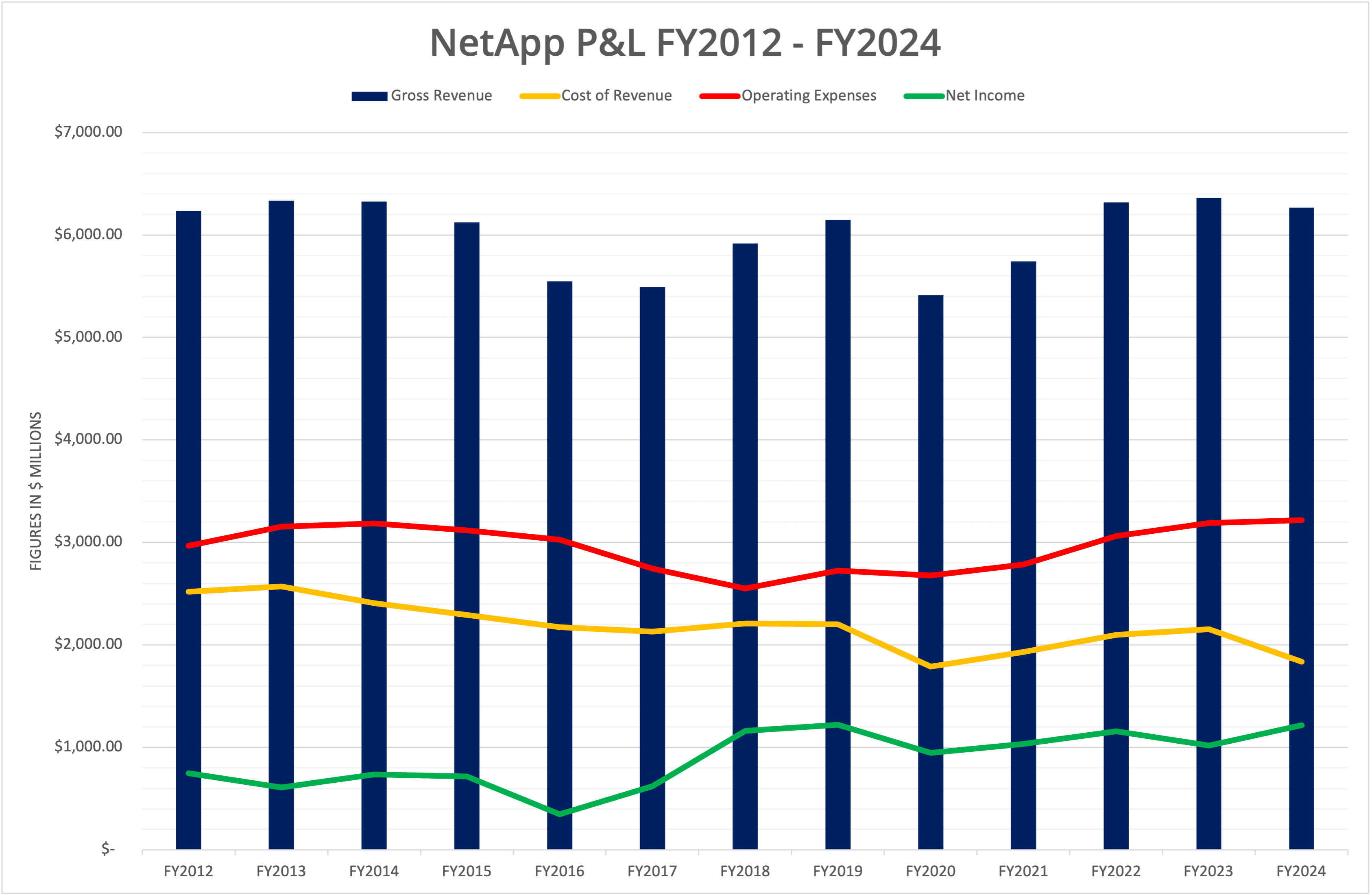

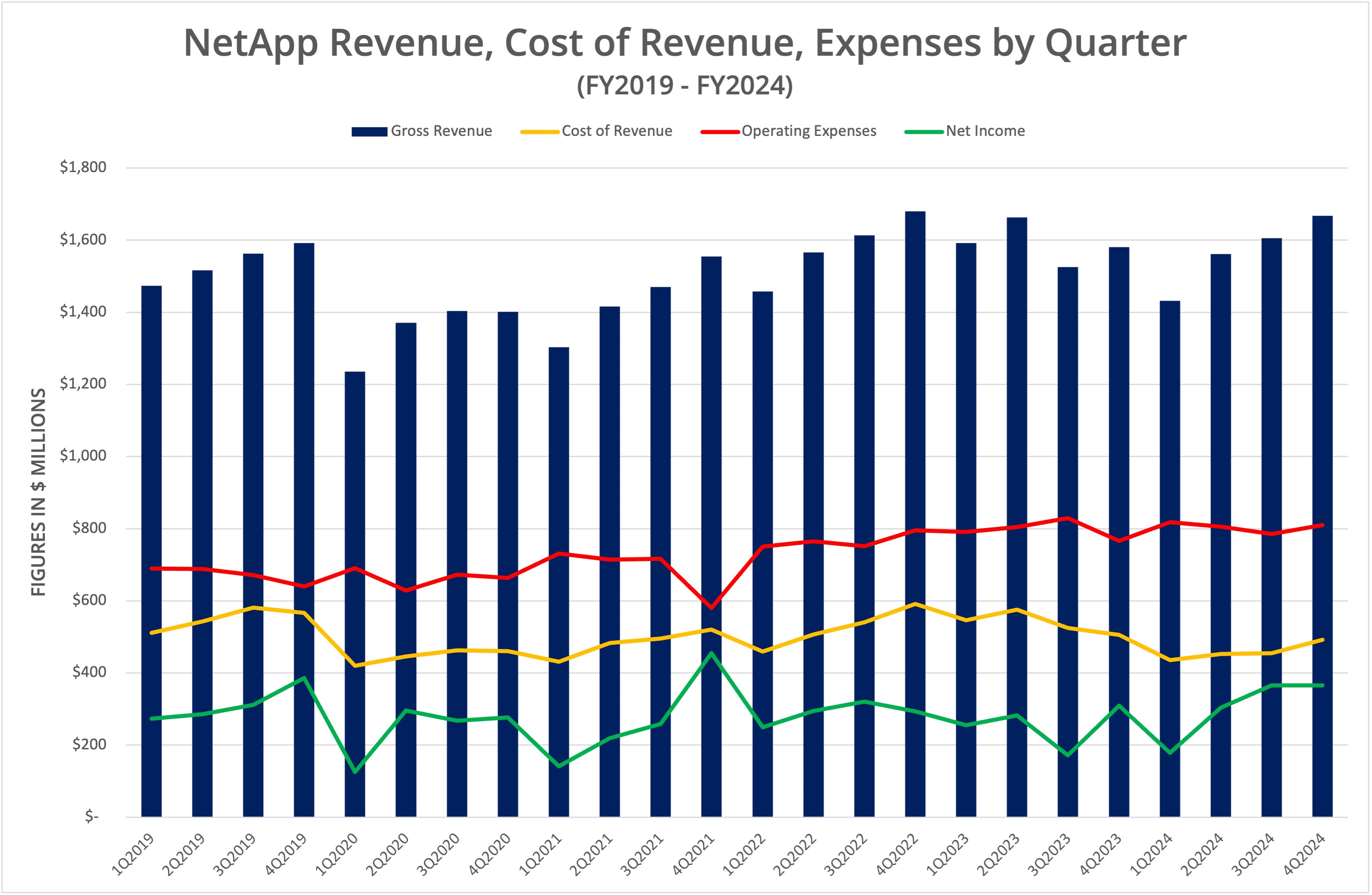

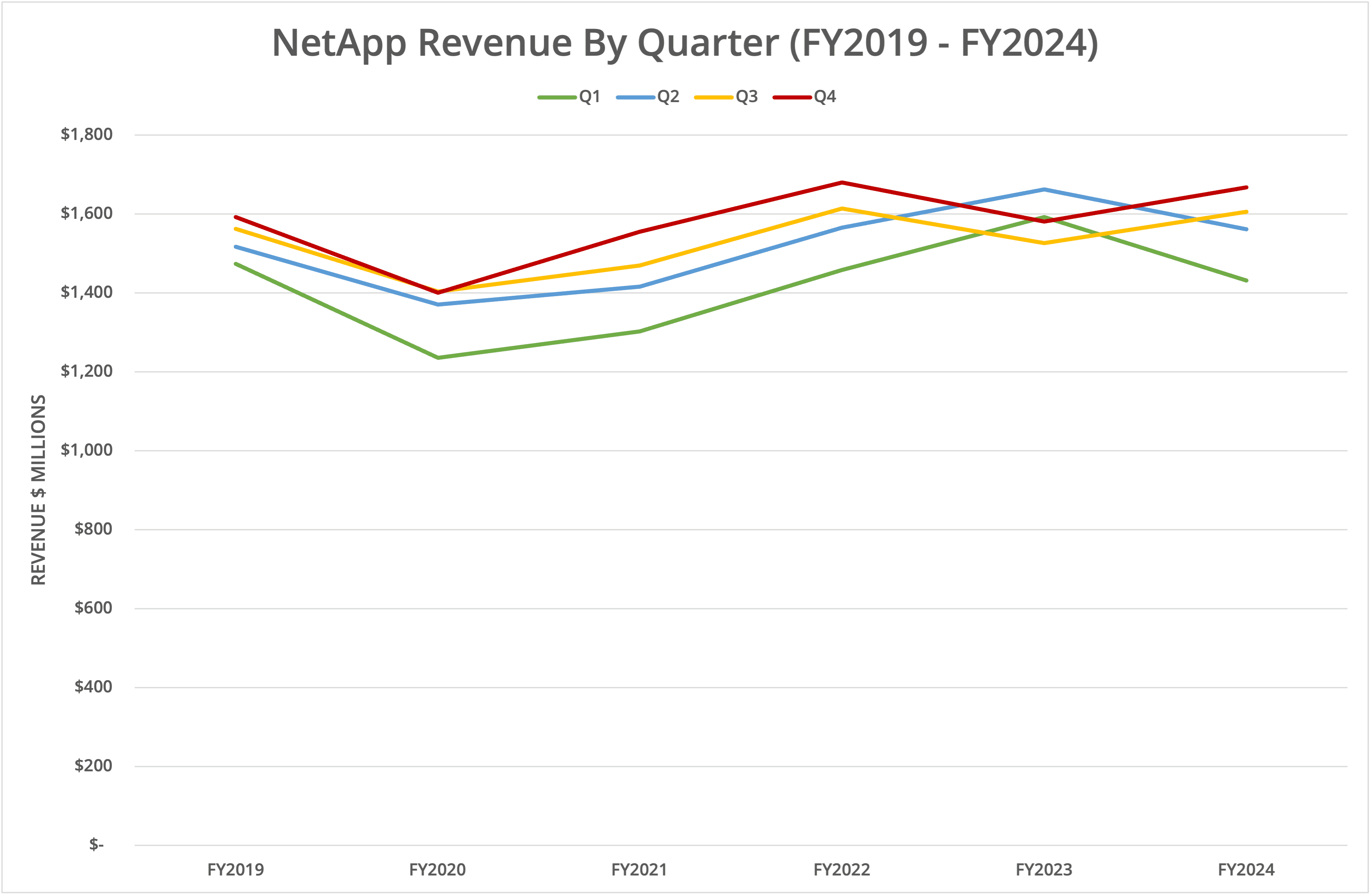

NetApp reported financial data for Q4 FY2024, including full-year results. We’ve shown this information in the embedded graphics, labelled Figures 1 through 5. For the financial year FY2024, revenue was down 1.5%, but net income (profit) increased by 19%, primarily due to reduced product costs.

Comparing Q4 to the equivalent period in FY2023, revenue was up 5.5%, and net income increased by 18.4%. NetApp highlights the growth in all-flash systems, with an increased run rate (ARR) of 17%, at $3.6 billion, compared to $3.1 billion in the same period of FY2023.

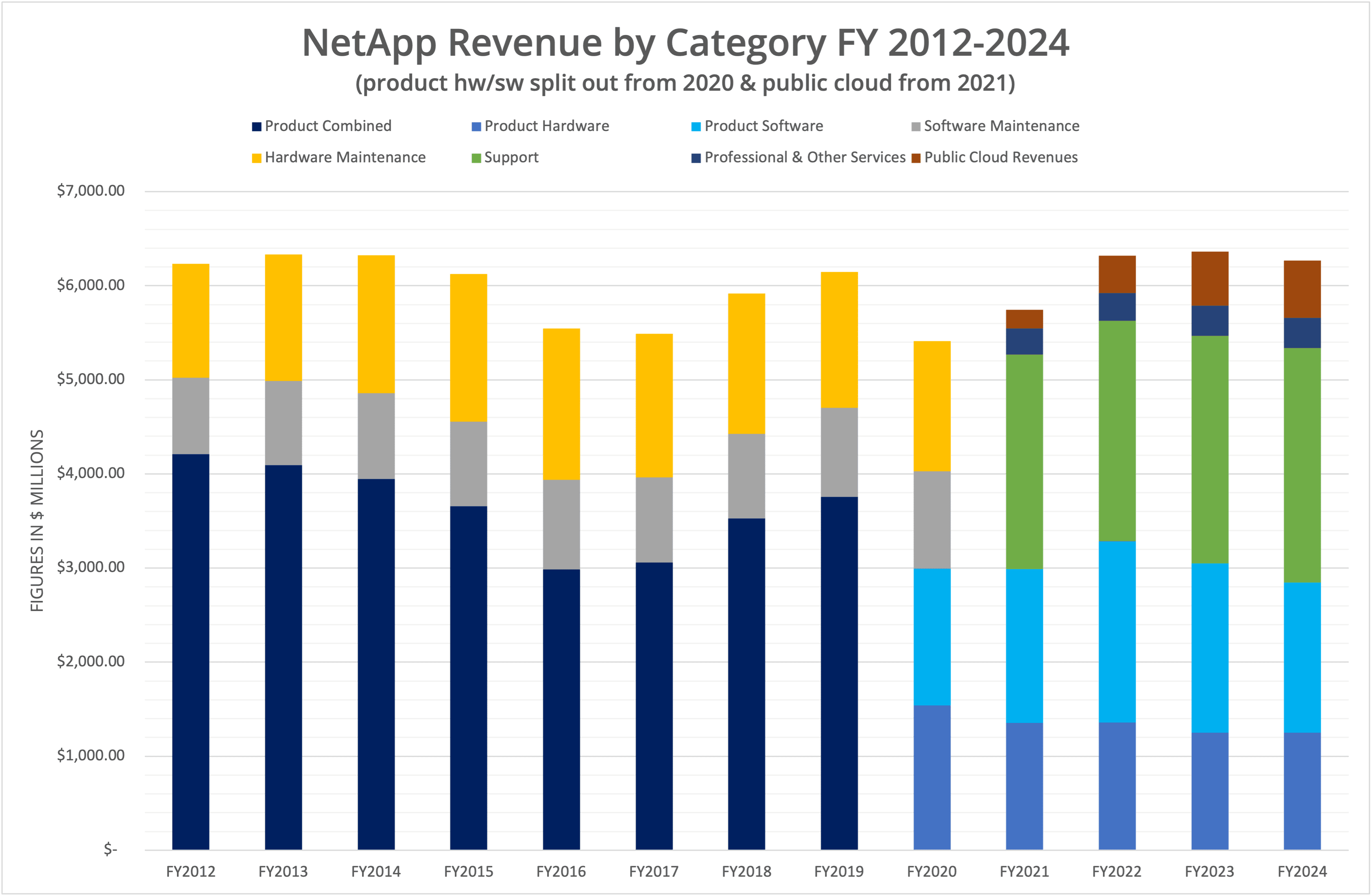

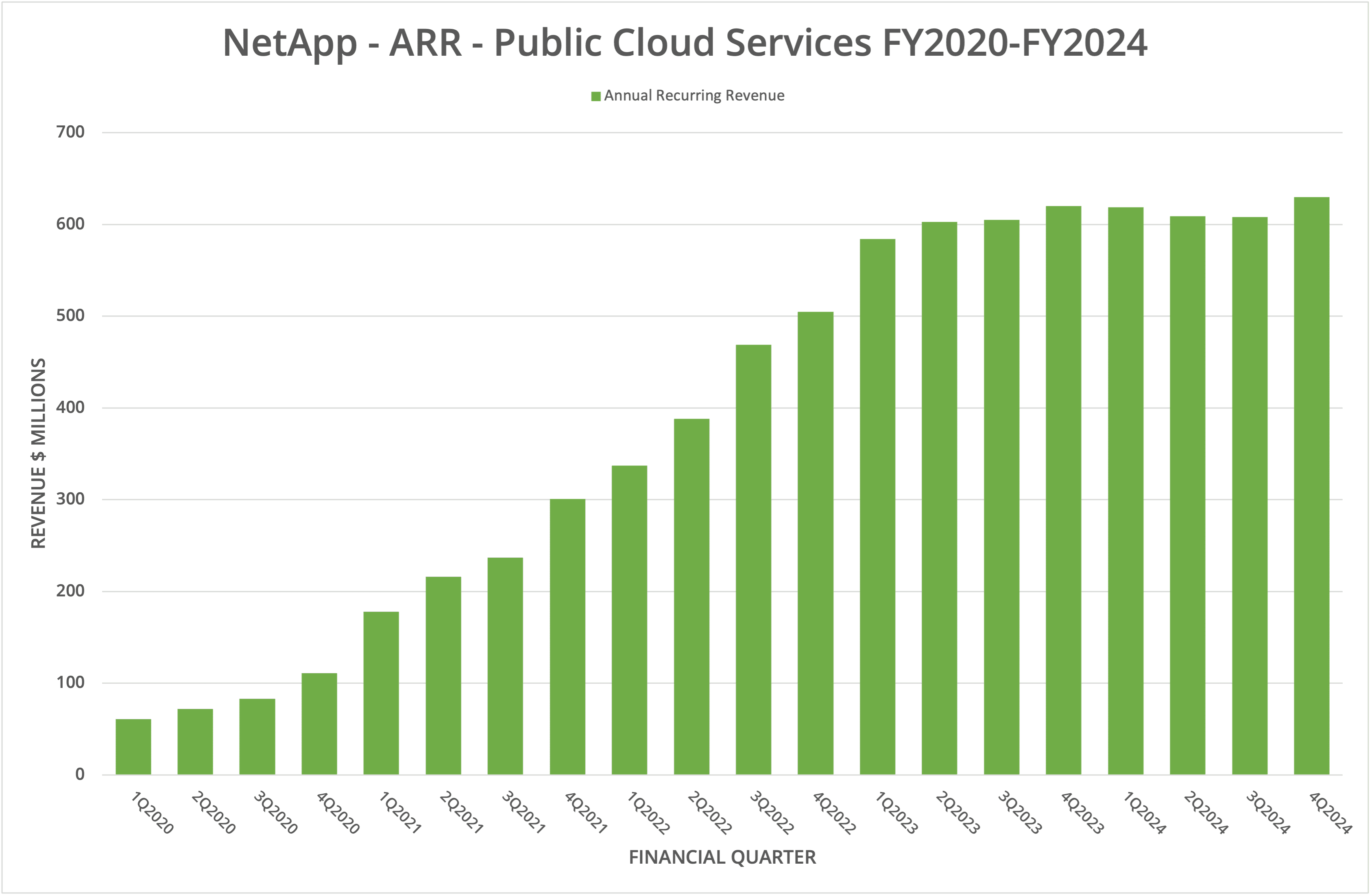

In the fourth quarter FY2024, ARR for public cloud services increased slightly, to $630 million, which is approximately 10% of all gross revenue. The Public Cloud segment of NetApp’s business has failed to grow significantly now for almost eight quarters.

Highlights

NetApp continues to gain momentum in its core business, namely all-flash storage systems. In May 2024, the company announced new AFF A-Series hardware based on an upgrade to Intel 4th Generation Xeon processors (Sapphire Rapids). These updated solutions offer greater capacity, efficiency, and higher performance than previous models.

The diversity of solutions had already been expanded during 2023, with C-Series based on QLC NAND and a relaunch of the ASA (All-SAN Array). Clearly, NetApp has identified product gaps in the market and is working hard to fill them, keeping competitive by using the latest server hardware.

Intelligence

In addition to hardware updates, NetApp has introduced the concept of Intelligent Data Infrastructure (IDI). An obvious question to ask is whether the “intelligence” applies to the management of data, or the infrastructure. In fact, it references both.

We’ve highlighted the efficiency improvements to infrastructure with C-Series and improved AFF A-Series. These capabilities are complemented with improved effective capacity efficiency (NetApp now claims 5:1 reduction) and “AI awareness” (if that’s a thing). In terms of “data intelligence”, improved capabilities for cyber-resilience and security, as well as (now free) solutions such as BlueXP Classification provide content-specific focus that was initially promised with the Data Fabric concept from way back in 2015.

Public Cloud

Probably the most challenging area for NetApp is how to increase revenue and engagement in the Public Cloud. As shown in Figure 5, Public Cloud ARR has essentially flat-lined (although there was growth in Q4). At a recent Analysts’ Day, I spoke with Ashish Dhawan, who leads the Cloud Business Unit at NetApp. He indicated that the various flavours of ONTAP in the public cloud (FSx for NetApp ONTAP, Azure NetApp Files and Google Cloud NetApp Volumes) are continuing to grow, and the impact on revenue comes from a re-focusing of the Spot and related solutions that we discussed as one side of the NetApp “Brain”.

Although we can’t directly comment (yet) on the strategy (as most of the analyst presentations were NDA), work is well underway on “re-imagining” the integration of the collection of assets acquired and aligned under the Spot brand. We expect to see more of the details on this at NetApp Insight in September 2024.

The Architect’s View®

NetApp is holding ground in a competitive hardware market, where product efficiency and sustainability are becoming increasingly important. As we highlight in our Market Perspective report on primary storage systems (embedded here), these capabilities are increasingly seen as table stakes, while features such as cyber-resiliency are differentiators. As the story of Intelligent Data Infrastructure continues to unfold (again, we expect more details at Insight), we should see improved strength in the hardware portfolio.

Essential Features of Primary Storage Systems 2024 – Market Perspective

This Architecting IT report reviews the market for primary storage systems, typically those offering block-based storage for the enterprise. This report rates vendors using our Trimetric. Premium download – $495.00 (BRKWP0307-2024)

Spot and the Public Cloud continue to be a work in progress. Obviously, NetApp has a strong position as the only storage vendor with cloud-native storage in the three major public cloud platforms. We believe this is probably an unassailable lead that derives from the software-defined storage nature of ONTAP.

At Insight 2024, the key announcements to watch for will be how features of the Spot products become more tightly integrated into the BlueXP platform (which originally was divided into Spot and BlueXP, see this blog post). The concept of the “evolved cloud”, as discussed two years ago, appears to have been dropped in favour of IDI. We look forward to seeing how this strategy “evolves” in the coming months.

Post #aff3. Copyright (c) 2024 Brookend Ltd. No reproduction in whole or part without permission.