HPE has announced Q1 FY2024 financial results, which show revenue down 13.5% year-on-year and only an increase in gross margin as a news highlight. Is it time for HPE to admit that GreenLake hasn’t revived its fortunes and that a more radical pivot of the business is required?

Background

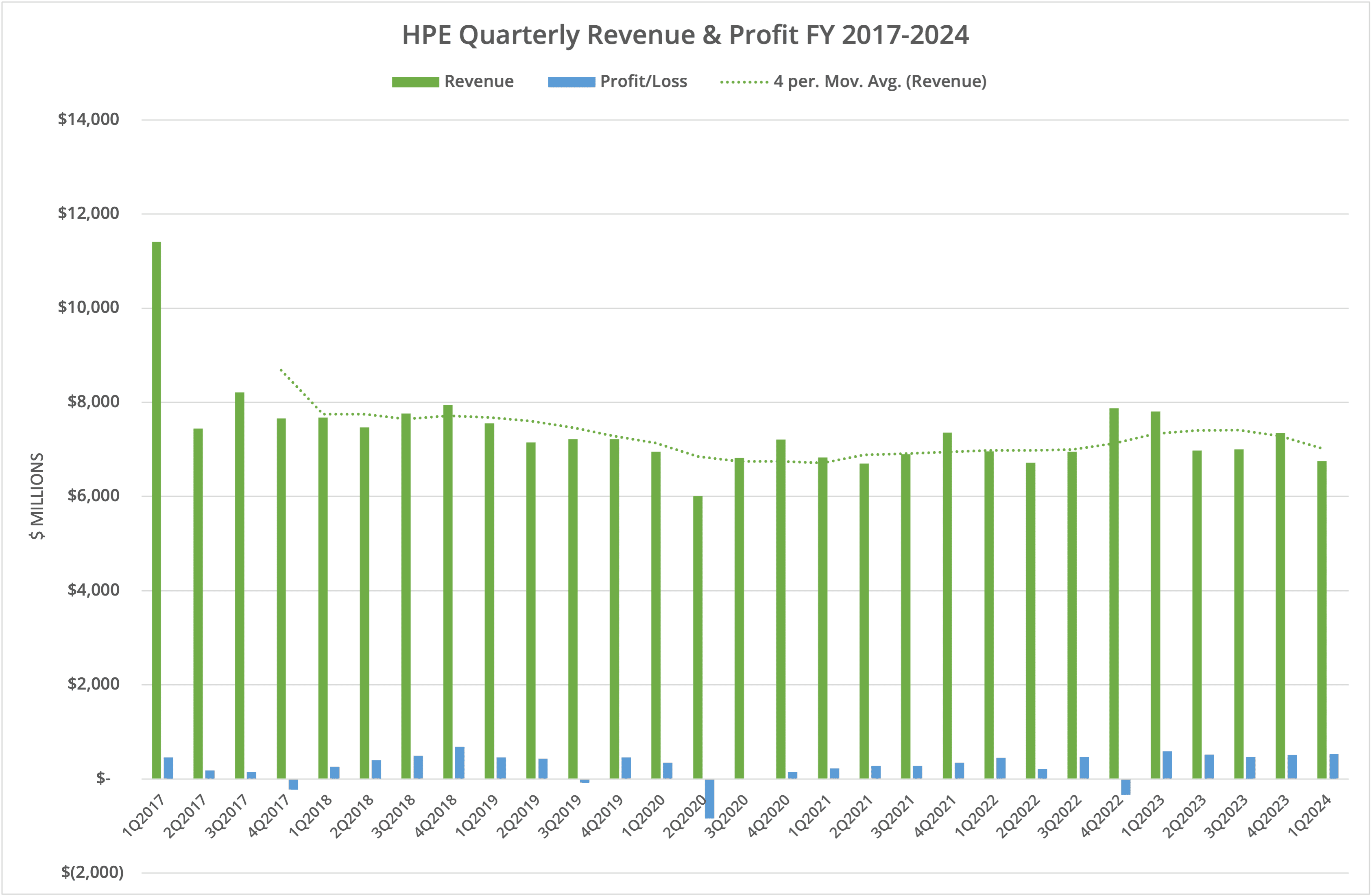

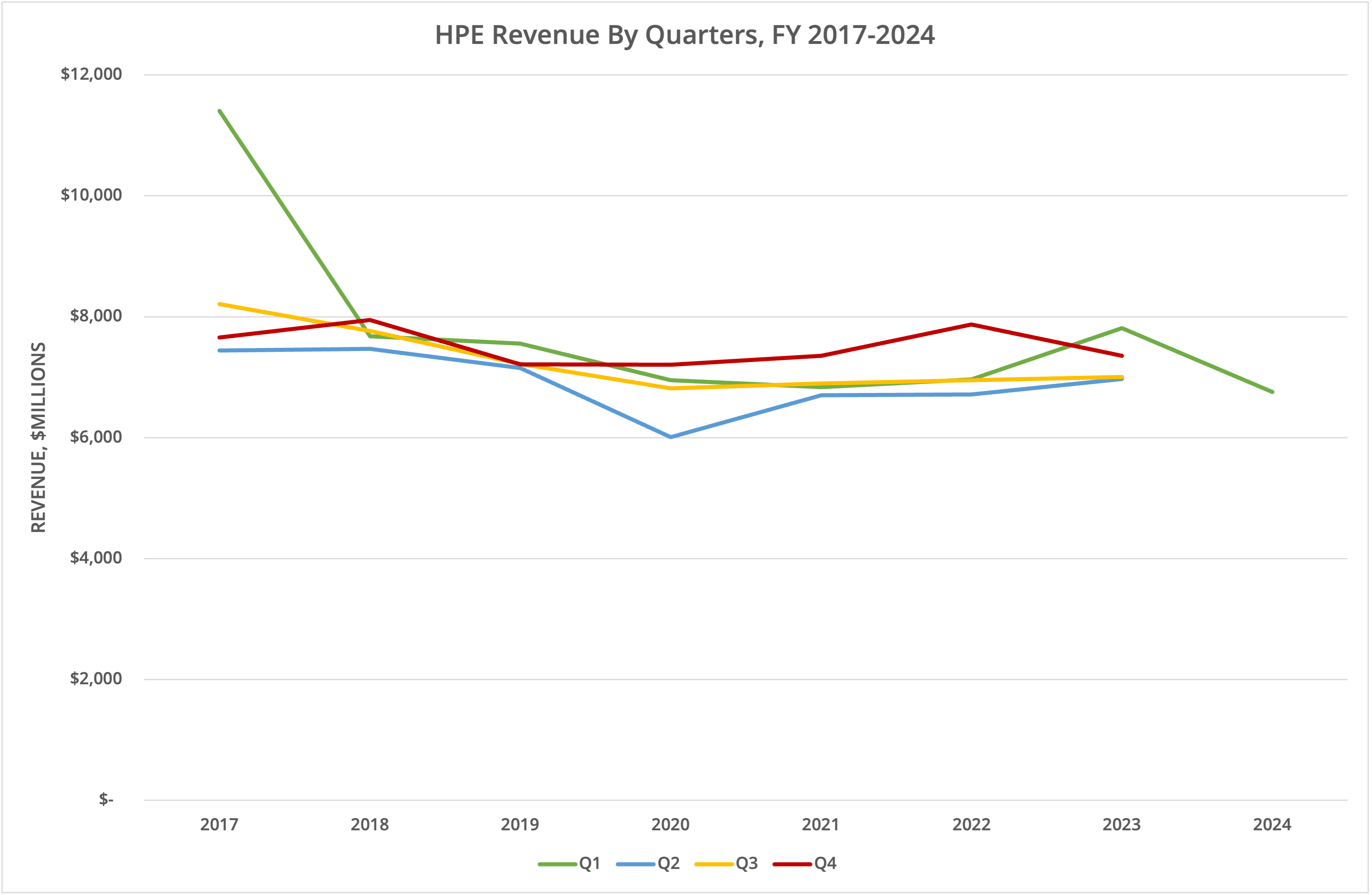

HPE reported Q1 FY2024 financial results, which showed a year-on-year decline in revenue of 13.5% ($6.8 billion and a guidance miss). The company highlighted an improved gross margin (36.4% compared to a previous 34.0%) and an increase in ARR of $1.4 billion (up 42% compared to the last period 12 months prior).

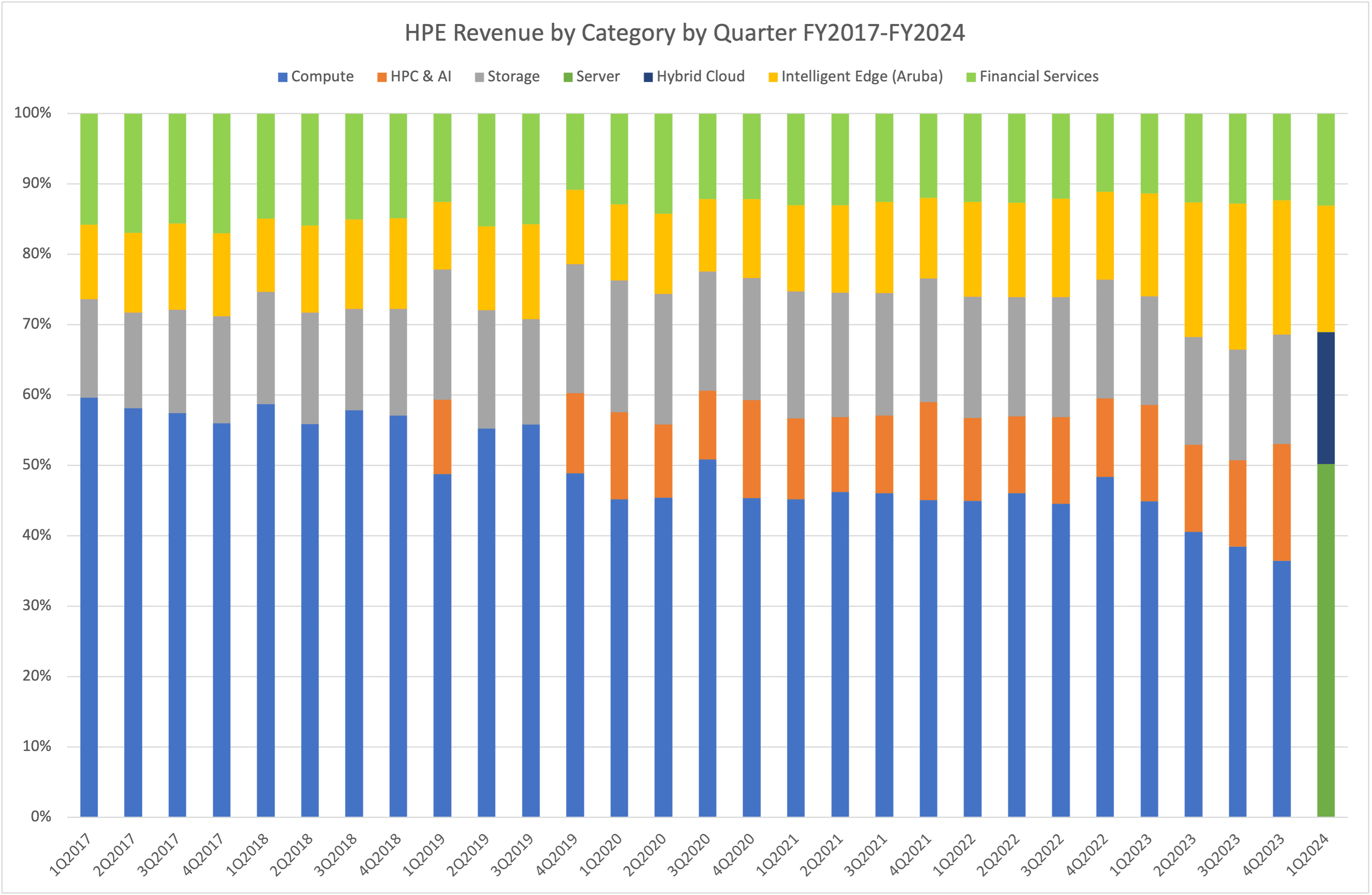

HPE also chose to re-organise reporting and consolidate the previous “Compute” and “HPC & AI” divisions as “Server”. Storage is no longer a separate reporting item and has been amalgamated into the broader “Hybrid Cloud” category.

Taking the reorganisation into consideration, the Server segment was down 23% year-on-year at $3.4 billion for the quarter, while Hybrid Cloud declined 10% (at $1.2 billion) and Intelligent Edge continued an uptrend with 3% year-on-year ($1.2 billion).

Supply Chain

HPE blamed the accessibility of GPU technology on the revenue miss, with an additional decline in networking demand. This isn’t the first time HPE has struggled with the supply chain; it previously reported issues during the COVID-19 pandemic. However, as a leading infrastructure vendor, we believe that HPE should have learned from past experience and have been ready for the anticipated GPU demand.

Reorganisation

Reporting granularity has been modified from Q1 FY2024, with the Server business unit encompassing Server and HPC & AI. Previously reported data for Storage now disappears into Hybrid Cloud and isn’t itemised separately.

Reporting consolidation is a good way to hide the revenue decline in individual business units. However, it could also be argued that if HPE is moving to a genuinely service-based model, then individual hardware tracking is no longer relevant. That would be true if solutions such as “software-as-a-service” were really that.

GreenLake

This raises the question of whether GreenLake genuinely provides value as an “as-a-service” model. HPE highlights the increase in ARR, up 42% compared to 12 months previously. The reporting behind ARR means sales can’t be recognised immediately and are amortised over the contract period. That could explain some of the HPE drop in revenue if it wasn’t for the fact that GreenLake has been in place for almost five years.

We see ARR as a red herring when it comes to predicting future business revenue. ARR simply smooths out the revenue peaks and troughs, reducing some of the unpredictability of end-of-quarter and end-of-year deals. However, with thousands of potential customers, there will still be, on average, new customers and departing customers in each quarter.

We also see gross profit as another red herring. HPE’s profit margin has averaged 32.7% over the last 29 quarters, with a standard deviation of 2%. There’s barely any upward trend or improvement occurring. Gross profit only matters if overheads are well managed. There’s no long-term evidence of an improvement in HPE profit figures.

The Architect’s View®

It is difficult to predict where HPE’s business is headed. In our analysis of the Q4 and full-year FY2023 results, we highlighted the GPU supply chain as a headwind issue. It appears that prediction has been proved right. All infrastructure companies are hoping for a boost from Generative AI. If HPE can’t source the hardware, it will fall behind the market even further.

The networking growth area (Intelligent Edge) has faltered, which is possibly why HPE announced the Juniper acquisition. Bolstering the networking offerings reduces the risk of a demand downturn in one specific product segment.

What is the core ethos of the HPE business? The fundamental building blocks of IT are still compute, networking, and storage. However, none of these pieces are complete without software to drive it.

Back in December 2022, we discussed rumours that HPE might be interested in acquiring Nutanix, which at the time was trading at around $30/share. Today, Nutanix is worth twice as much ($65 at the time of writing) following the fallout from Broadcom’s VMware restructuring. An acquisition looks out of the question (especially after buying Juniper Networks).

Without a complete hybrid cloud offering that Nutanix could have provided, is it enough to offer customers cloud-based management with BYOD licensing for the software components? We don’t think so. If the public cloud has taught us anything, it’s the benefit of tightly integrated hardware and software all the way up the stack.

This quarter has been challenging for HPE. There doesn’t appear to be any light at the end of the tunnel for future growth. We believe HPE needs a radical overhaul to stay relevant otherwise the business will continue to operate in a zombie holding pattern for years to come.

Copyright (c) 2007-2024 – Post #223f – Brookend Limited, first published on https://www.architecting.it/blog, do not reproduce without permission.