Subject to regulatory approval, HPE intends to acquire Juniper Networks for $14 billion. How will the company be assimilated into the HPE family and what does this acquisition say for the future direction of HPE?

Background

HPE announced the intended purchase of Juniper Networks on 9th January 2024, at $40 per share, as an all-cash transaction. HPE doesn’t have $14 billion of cash to hand, so the acquisition will be funded by a mix of some cash and new debt. HPE expects to make savings on overheads (described as synergies) of $450 million within three years of closing the deal. This (naturally) means rationalisation of administration, marketing, and sales staff.

Networking

We don’t cover networking as a technology topic, however, we can see that Juniper Networks focused on technology used within internet service providers, specifically routers, as direct competition to Cisco Systems.

Juniper Networks’ last full-year accounts (FY2022) show revenues of $5.3 billion, a gross margin of 55.8% and net profit of approximately 8.9%. Quarterly revenue for the first three quarters of FY2023 was around $1.4 billion.

HPE

While we can’t comment on the benefits of the combined entity from the technical angle, we can see from the press release that HPE intends to merge Juniper Networks with the existing networking business (called Intelligent Edge), at least from an accounting perspective.

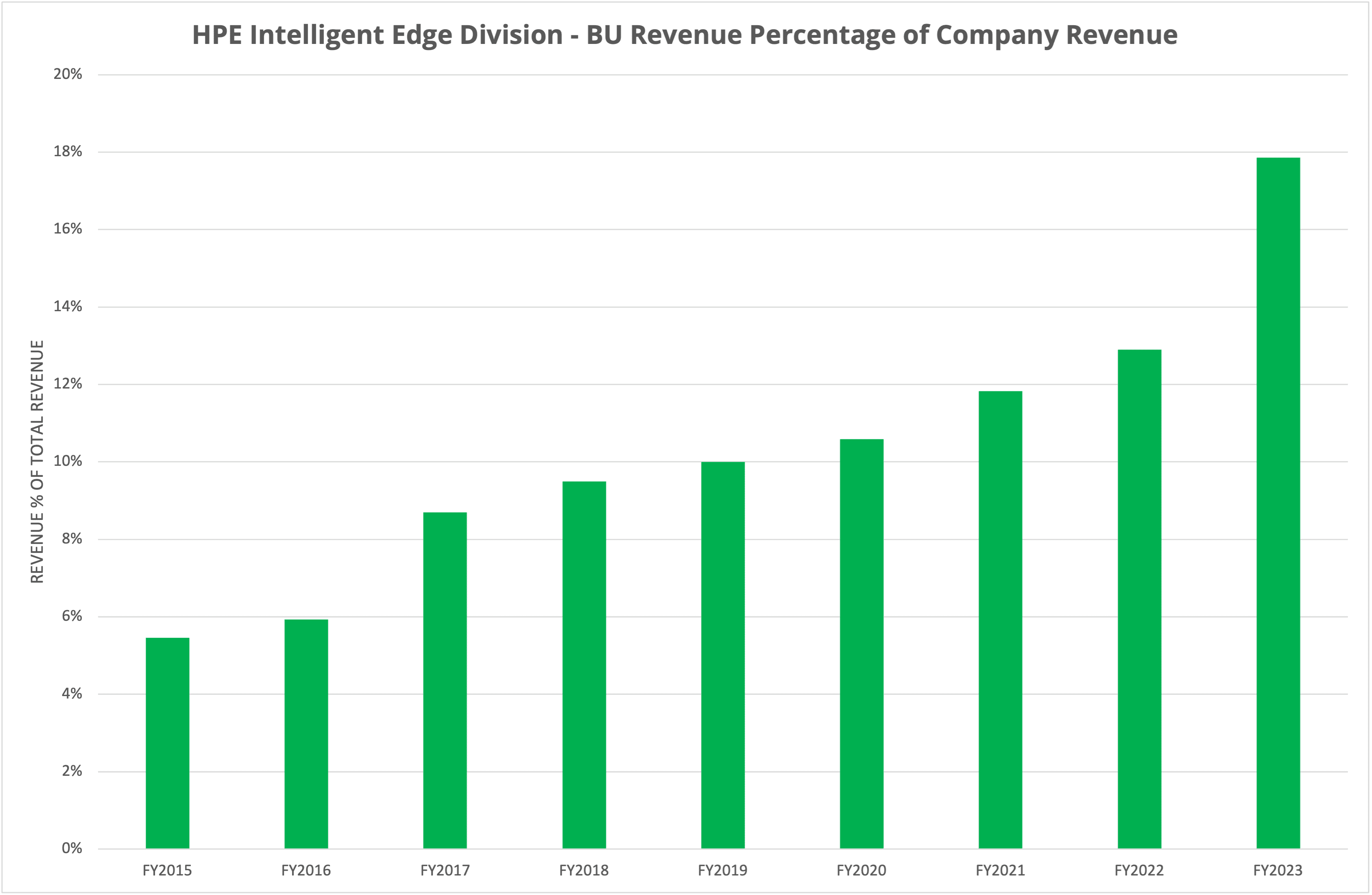

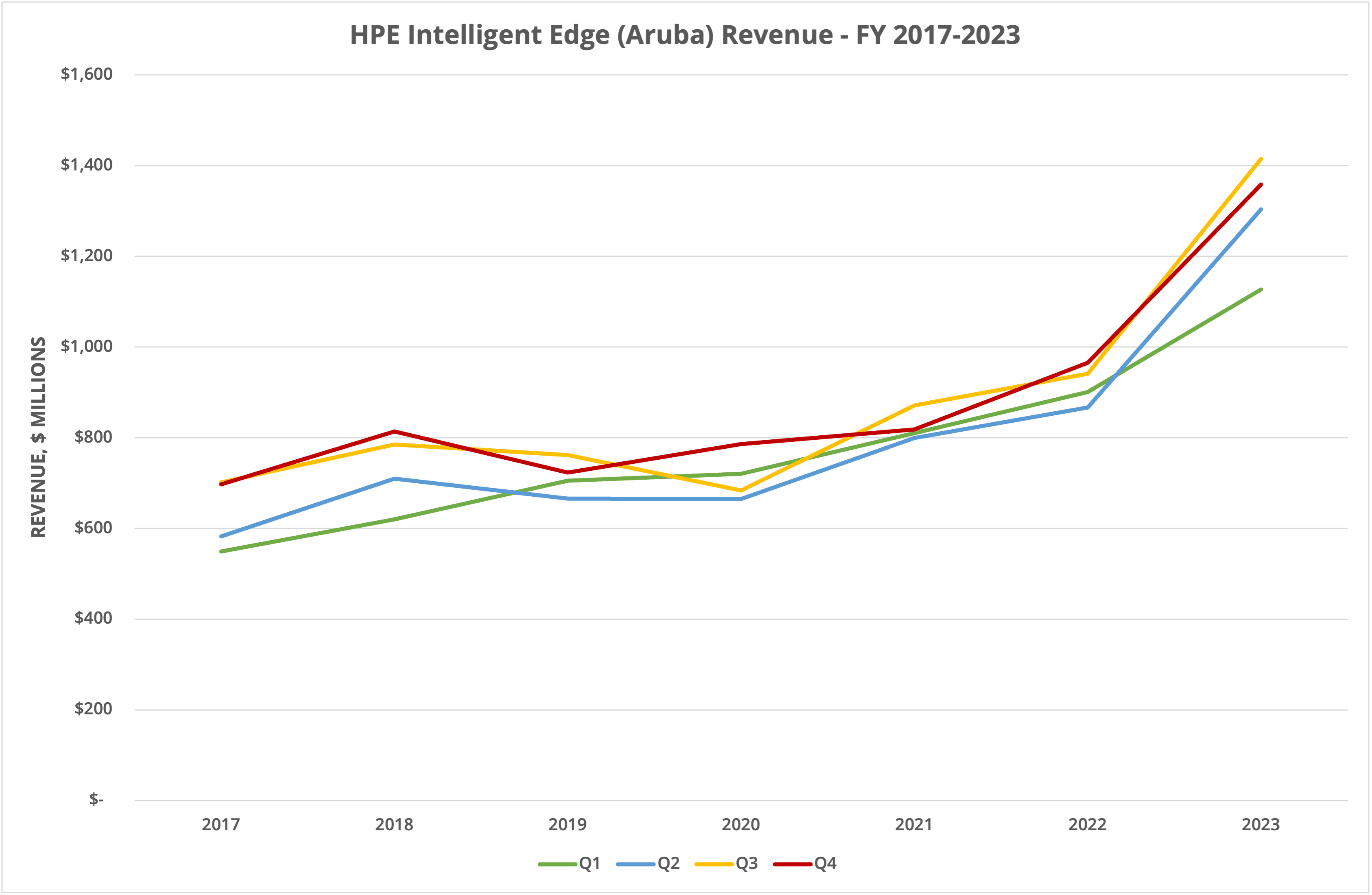

We’ve been tracking HPE financials for some time (see our X-Ray and latest post covering the Q4 FY2023 announcement) and have highlighted the relative and absolute growth of the Intelligent Edge business (Aruba) within HPE. Figure 1 shows this data graphed from FY2015 to FY2023.

Intelligent Edge currently represents 18% of HPE’s revenue. Adding in the latest annual revenue from Juniper Networks and that percentage jumps to around 1/3 of the revenue total, similar to that of Compute (the server business). For the last quarter of FY2023, the combined business would probably have been the highest grossing business unit.

Pivot

We’ve been asking for some time whether HPE is pivoting away from the traditional businesses of servers and storage, towards higher-margin networking and HPC. The HPE press release implies an AI angle to the Juniper acquisition (which we should expect from every company in 2024). However, putting the technical aspects aside for a moment, the Intelligent Edge BU within HPE has been growing steadily (while other BUs stagnate), so perhaps doubling down in the current market makes sense as a long-term strategy.

The Architect’s View®

As we’ve said already, Architecting IT doesn’t cover networking technology. For us, the more interesting aspect of this latest announcement is the future direction of HPE. With $14 billion to find, this acquisition will have debt to pay off for a few years. This could mean no further large, strategic acquisitions in other areas for a while. HPE desperately needs a reboot in the storage division, for example, having relied on partner solutions for many years. This move seems unlikely now. (Side note: imagine the risk using VAST Data currently represents, if a rival were to bid and acquire VAST in the next 6 months.)

The public cloud has taken a big chunk of market revenue from the legacy on-premises infrastructure vendors. We’ve suggested for some time that across the market we will see consolidation occurring. It’s a natural process when markets contract to merge businesses and protect margins.

HPE acquiring Juniper could be seen as either a pivot towards a market with greater prospects (and margins) or the start of further consolidation in the infrastructure market, driven by the increasing growth of the public cloud. We believe the consolidation playbook is the more likely route, as the on-premises market continues to research ways to beat the growth of the public cloud. Expect more acquisitions to come.

Copyright (c) 2007-2024 – Post #1b23 – Brookend Limited, first published on https://www.architecting.it/blog, do not reproduce without permission.