HPE has announced Q4 FY2023 and full-year results with annual revenue up 2% and increased gross margins. However, Compute (server) revenue is down 10% and Storage down 6% annually. Intelligent Edge and HPC/AI continue to prop up the business with 42% and 23% growth, respectively. Is HPE’s business pivoting away from its traditional core offerings?

Background

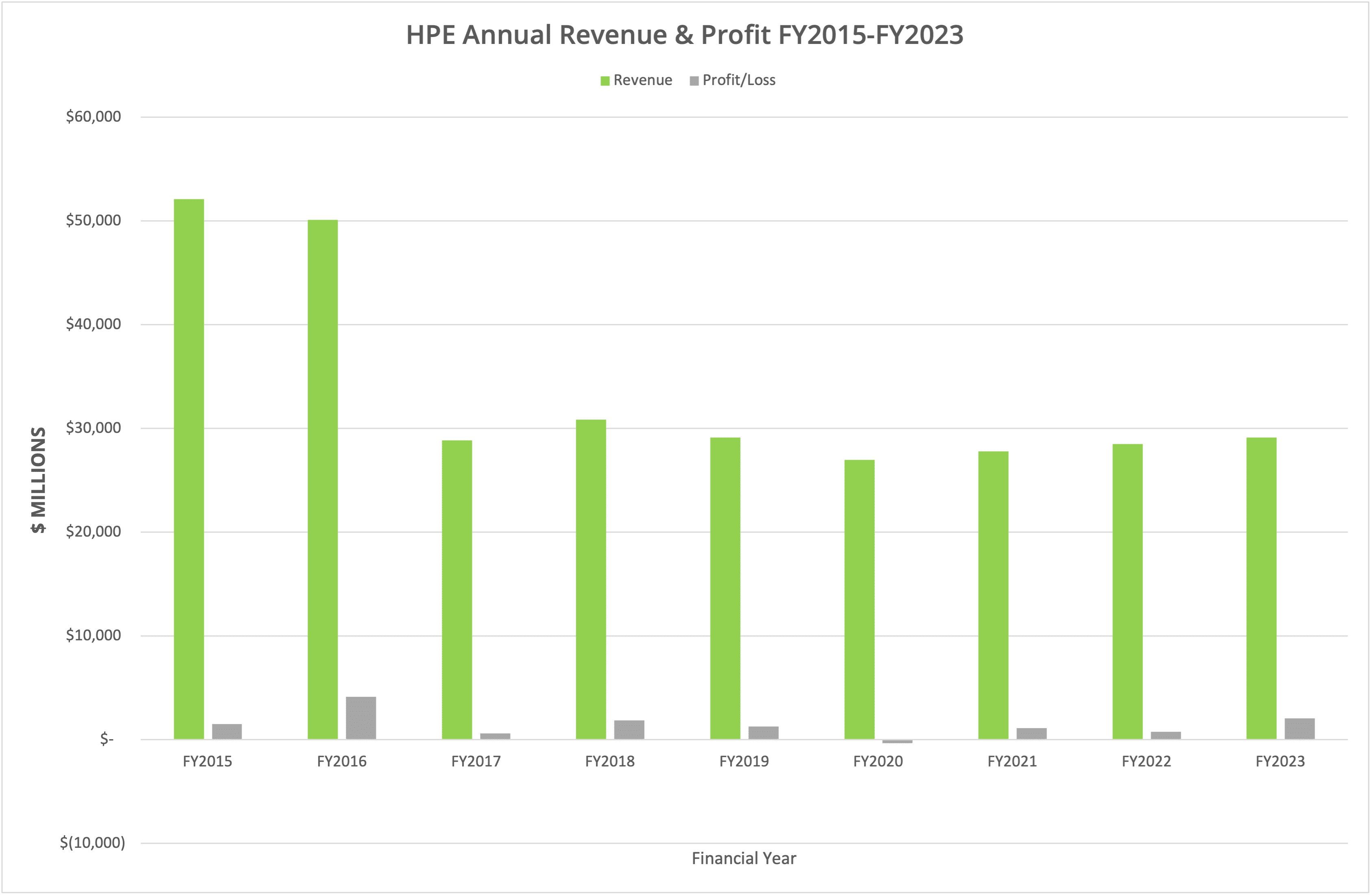

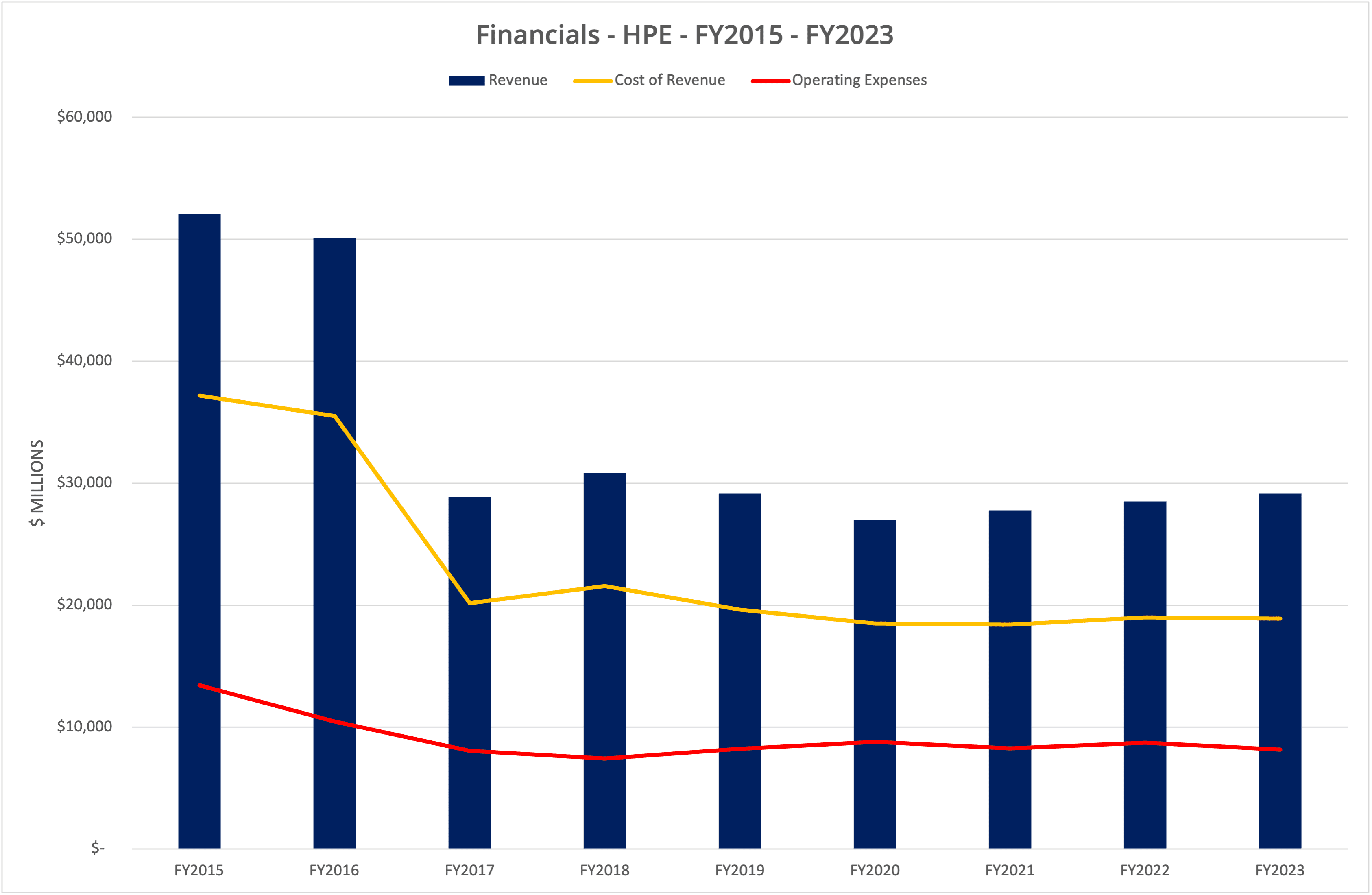

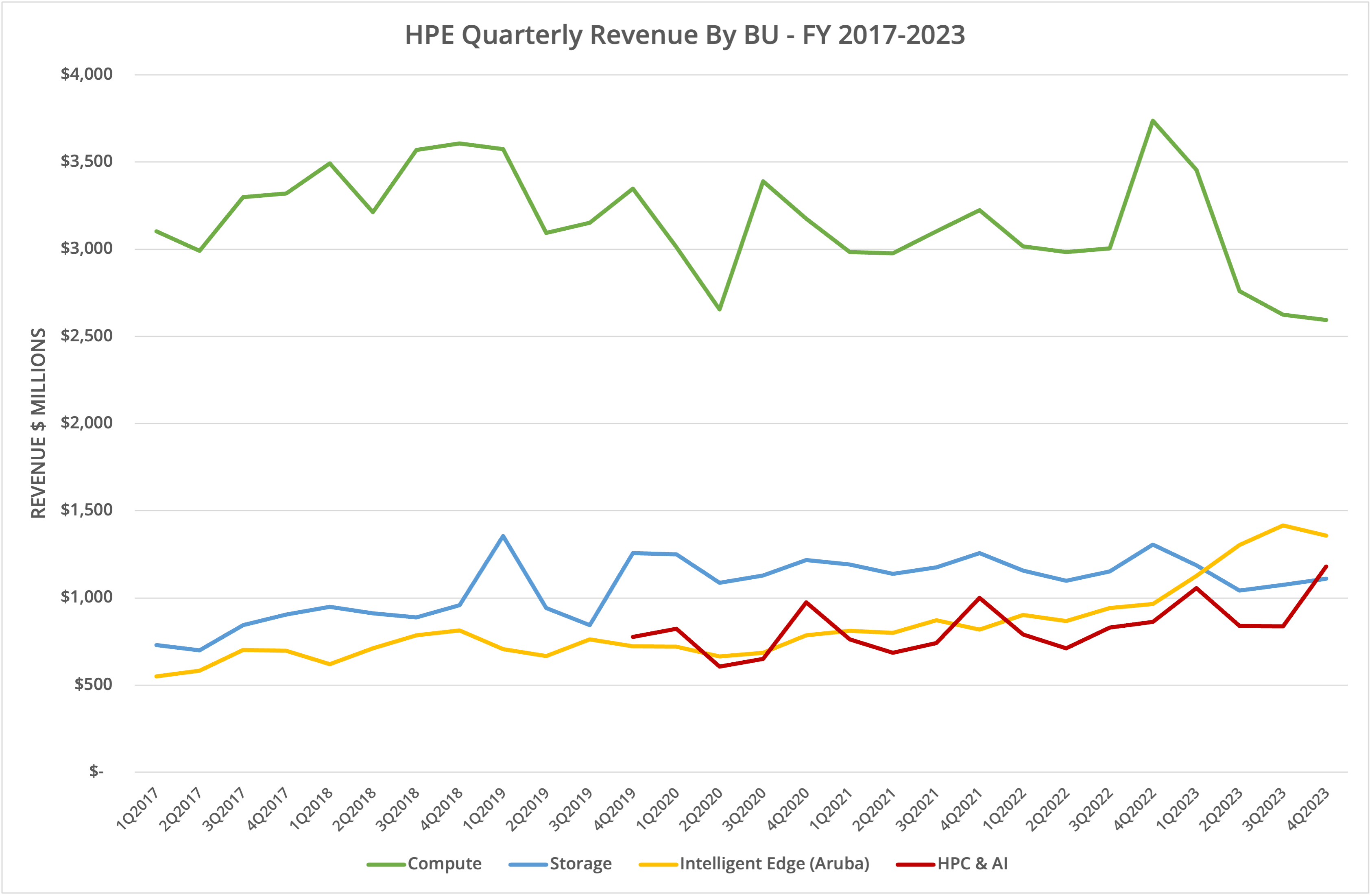

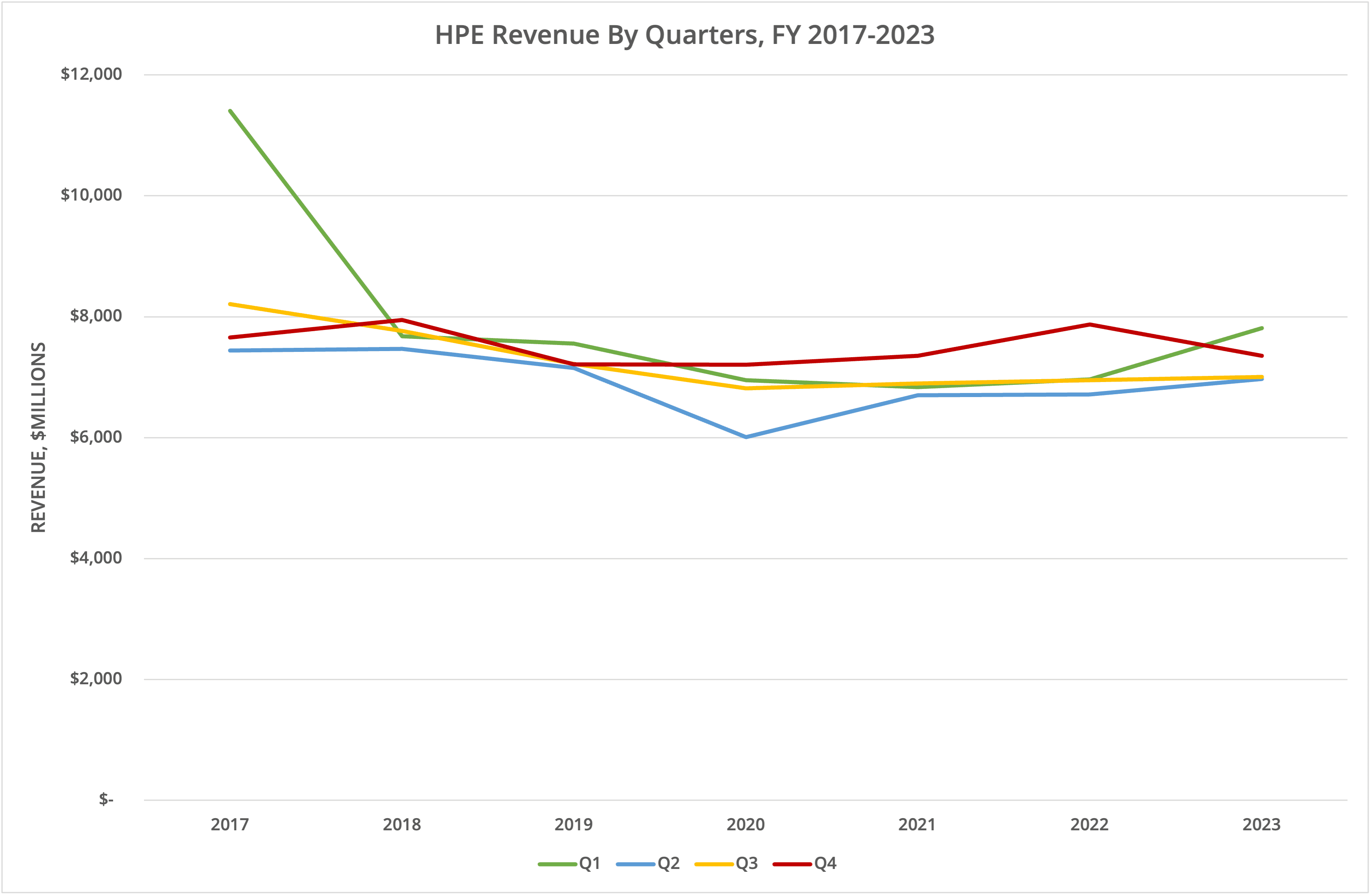

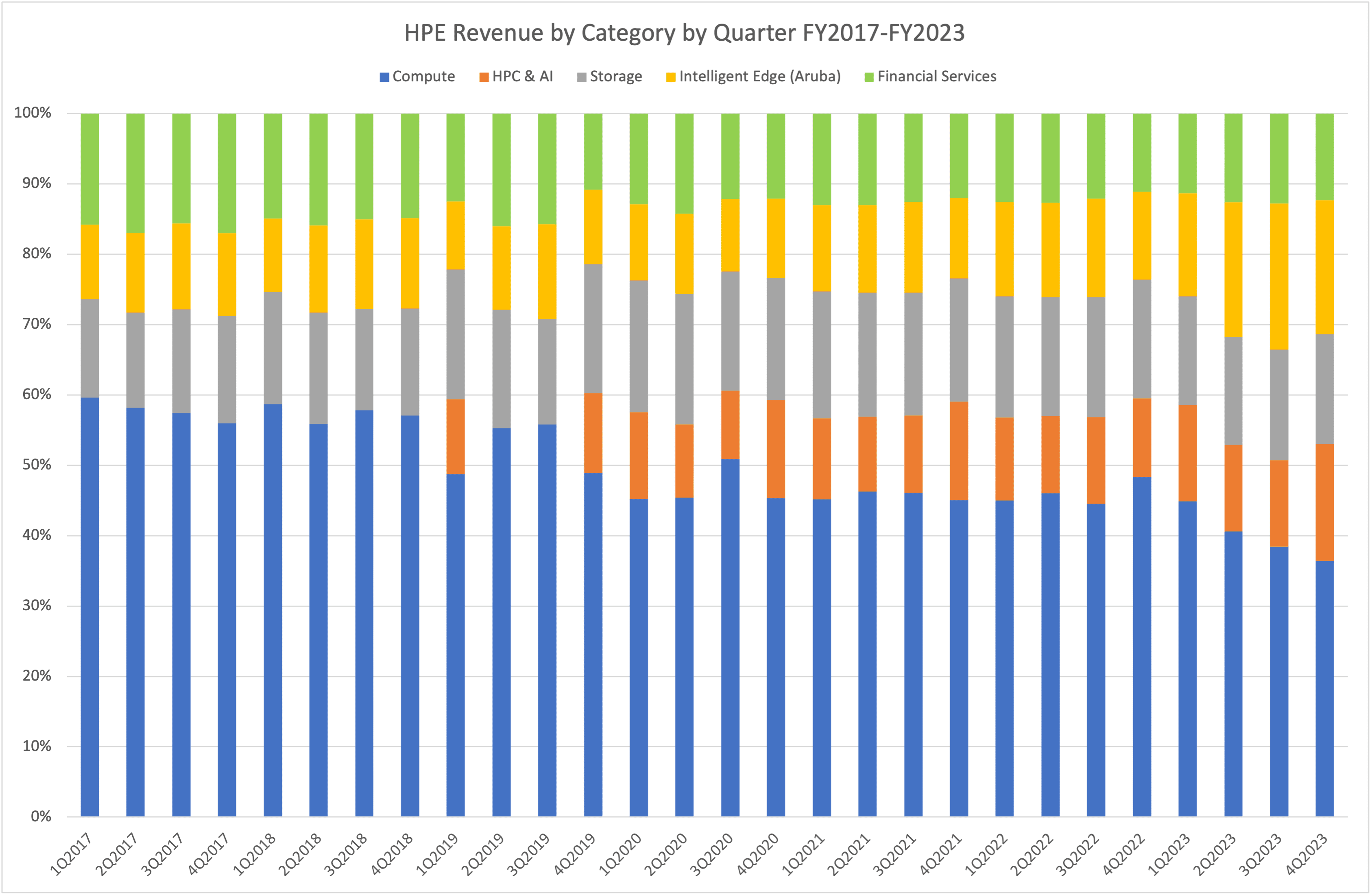

HPE reported revenue of $29.1 billion for FY2023, up 2.2% from the previous year. Across the five reported lines of business, Compute was down 10.3%, HPC & AI up 22.6%, Storage down 6.2%, Intelligent Edge up 41.6%, while Financial Services was up 4.2% relative to the previous year.

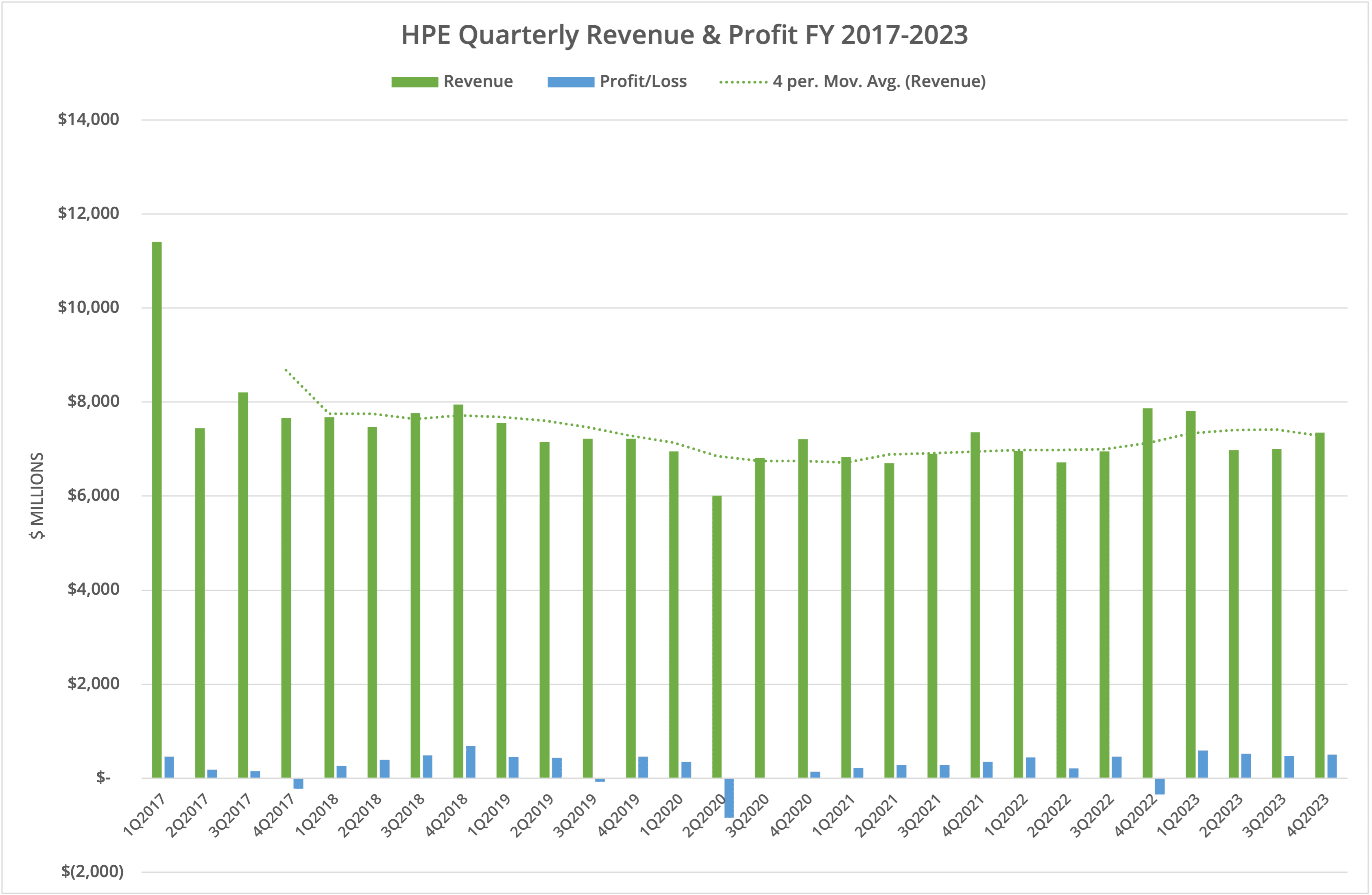

If we look at the quarterly data, compared to Q4 FY2022, revenue was down 6.6%, with Compute down 30.6%, HPC/AI up 37%, Storage down 14.9%, Intelligent Edge up 40.7% and Financial Services up 2.2%. The current quarter is the first to see a drop in consecutive quarter revenue for Intelligent Edge since 2Q2022 (5 quarters of growth).

Business Change

As we’ve highlighted previously, the Compute (server) business continues to decline, although Figure 4 shows that the rate of decline may have bottomed out. Instead, much better growth figures continue to be seen in the HPC/AI and Intelligent Edge business lines. AI is the most hyped industry sector at the moment, so we should expect to see growth here, especially following on from HPE’s LLMs as a Service announcement earlier in the year.

Does the data show a bigger picture with the long-term decline of servers and storage? The server segment is, relatively speaking, a commodity business where we think there will be a long-term decrease in spending as customers refocus on the public cloud and HPC/AI projects. This aligns with the revenue shift HPE is seeing.

GreenLake

How does this data reflect on the relative success or failure of GreenLake? Look at the quarterly data, and we see a repeated cycle of Q4 revenue being higher than that in Q2 and Q3. This is either cyclical buying or selling. Theoretically, if more income is being generated as ARR (annual recurring revenue), then we’d expect the quarterly peaks and troughs to be flattened, but this is not the case.

We still believe there is no evidence to show that GreenLake is turning HPE around. As we’ve highlighted in previous quarters, GreenLake is a marketing strategy that appears to have failed to catch the attention of customers, mainly because it is a financial model, not a true as-a-service consumption option.

The Architect’s View®

HPE continues to be a business in a holding pattern. Customer revenue is being shifted from traditional computing to HPC and AI. While this appears to be a good short-term gain for HPE, we see several headwinds. The first is the supply chain for GPUs, where every business is competing for products to sell to customers. The second is the depth of offerings now available in the public cloud.

This week at AWS Reinvent, Amazon announced updated AI training hardware and further integration of AI tools to aid the development and production of AI models. The public cloud vendors are outpacing the on-premises vendors with new hardware and software solutions optimised to their requirements. By comparison, on-premises vendors will continue to purchase off-the-shelf components that will gradually lose efficiency compared to the public cloud.

HPE could stem the tide by further extending its cloud HPC and AI offerings, building out those service offerings in a similar way to AWS, Azure, and Google. That means investing in software and workflow tools. Does HPE have the will to go down that route? We’ll be watching to find out.

X-Ray: Hewlett Packard Enterprise Corporation

This Architecting IT report takes a deep dive into HPE’s history, products, services, and future outlook. This report is only available for download via paid subscription.

Copyright (c) 2007-2023 – Post #3f22 – Brookend Ltd, first published on https://www.architecting.it/blog, do not reproduce without permission.

This post is only available to Individual, Vendor or Enterprise subscribers. Restrictions on distribution are based on those licensing terms. Check our Terms of Service for details.