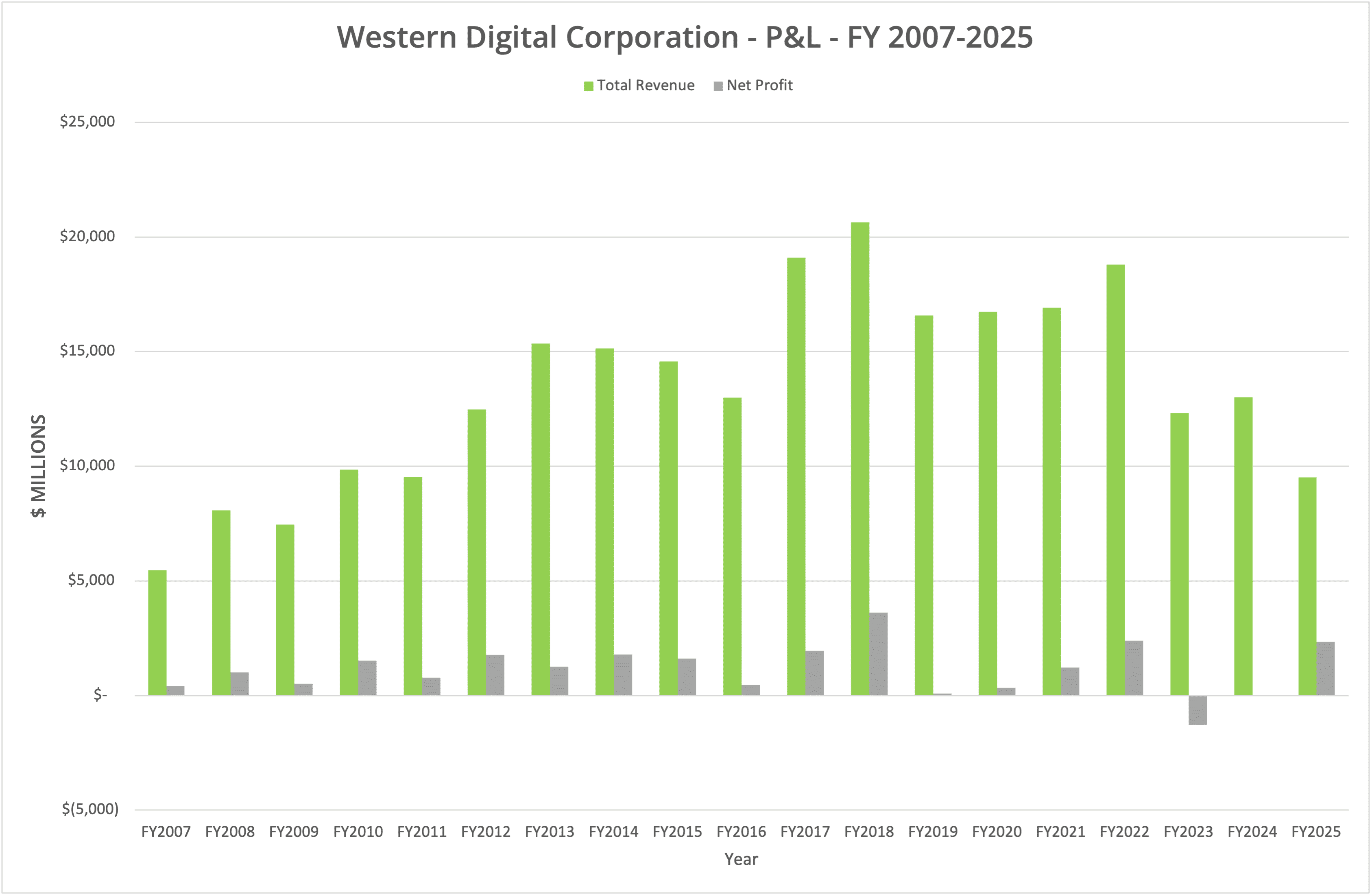

Western Digital Corporation has announced financial results for the fourth quarter FY2025 and the full year, the period ending 27th June 2025. In absolute terms, revenue in the quarter declined 30.8% year-on-year to $2.61 billion, but was up 30% when the contribution of SanDisk is removed from the data. For the full year, absolute revenue was down 26.8% at $9.52 billion, but up 51% when excluding SanDisk from FY2024.

Background

Western Digital Corporation declared financial results for the period Q4 FY2025 and full year, ending 27th June 2025, on 30th July 2025. Excluding the impacts of SanDisk from historical data, quarterly revenue rose 30% to $2.61 billion, while the full year revenue was $9.52 billion, up 51%. In absolute terms, revenue declined 30.8% and 26.8% respectively.

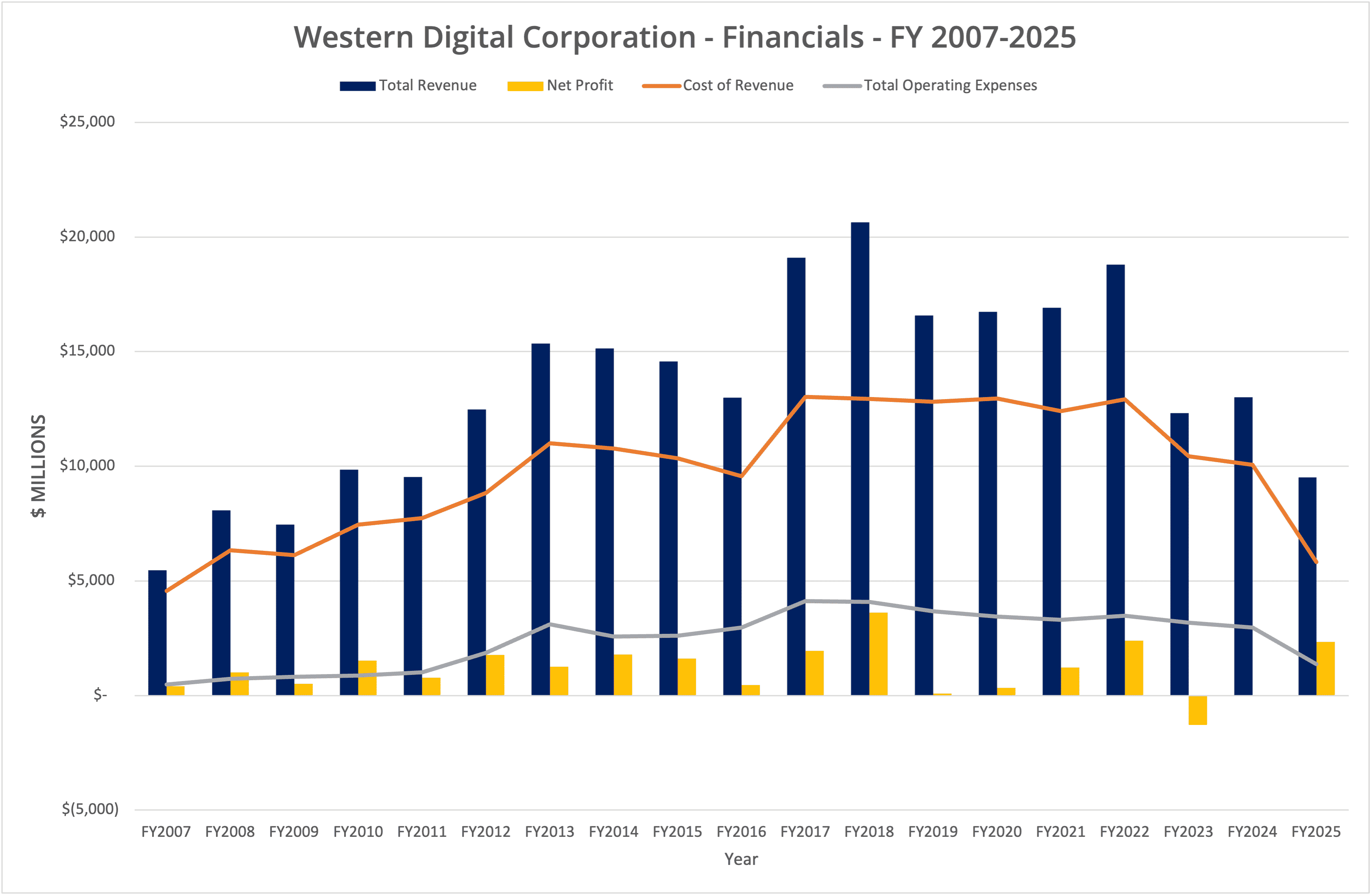

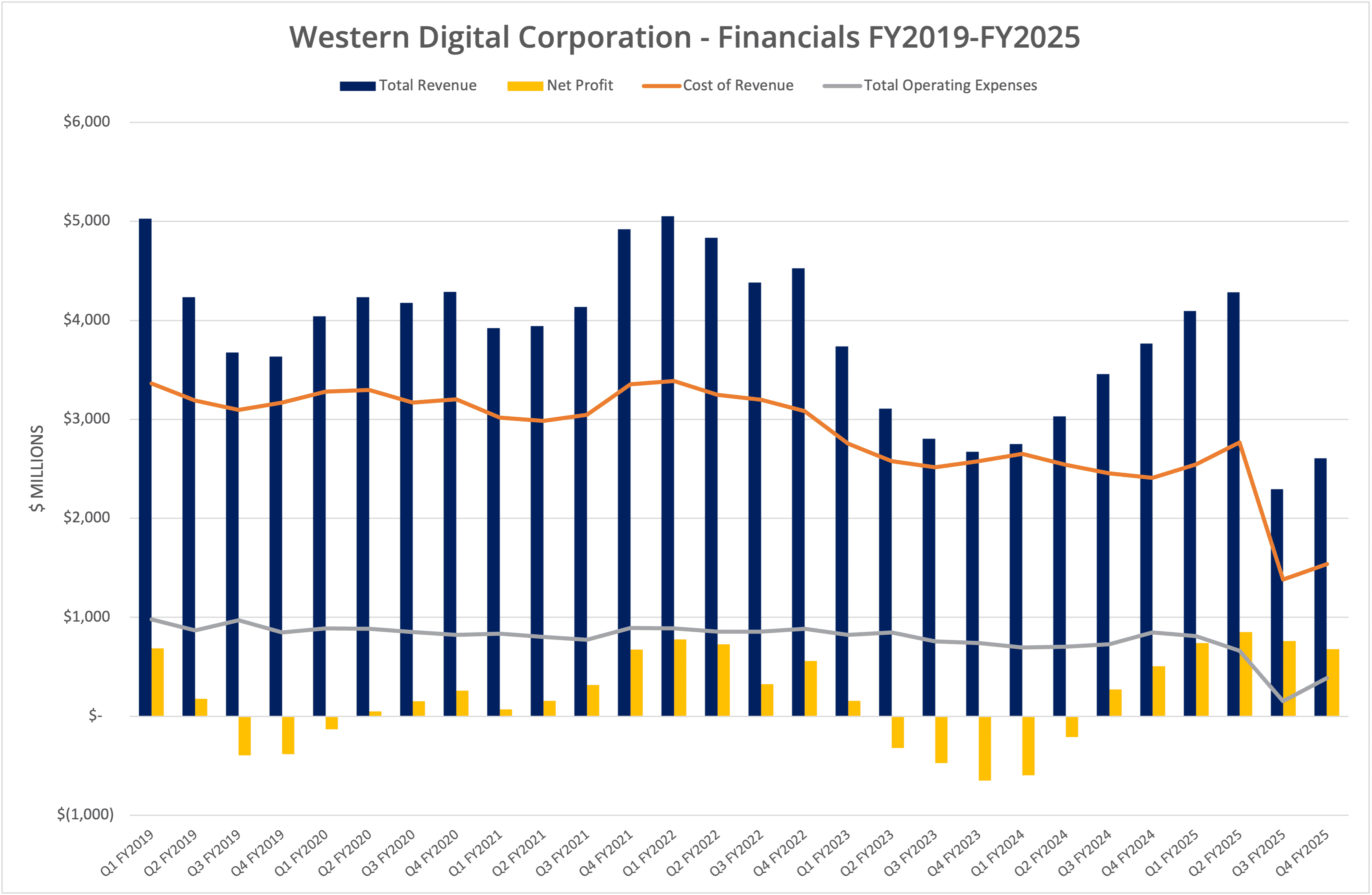

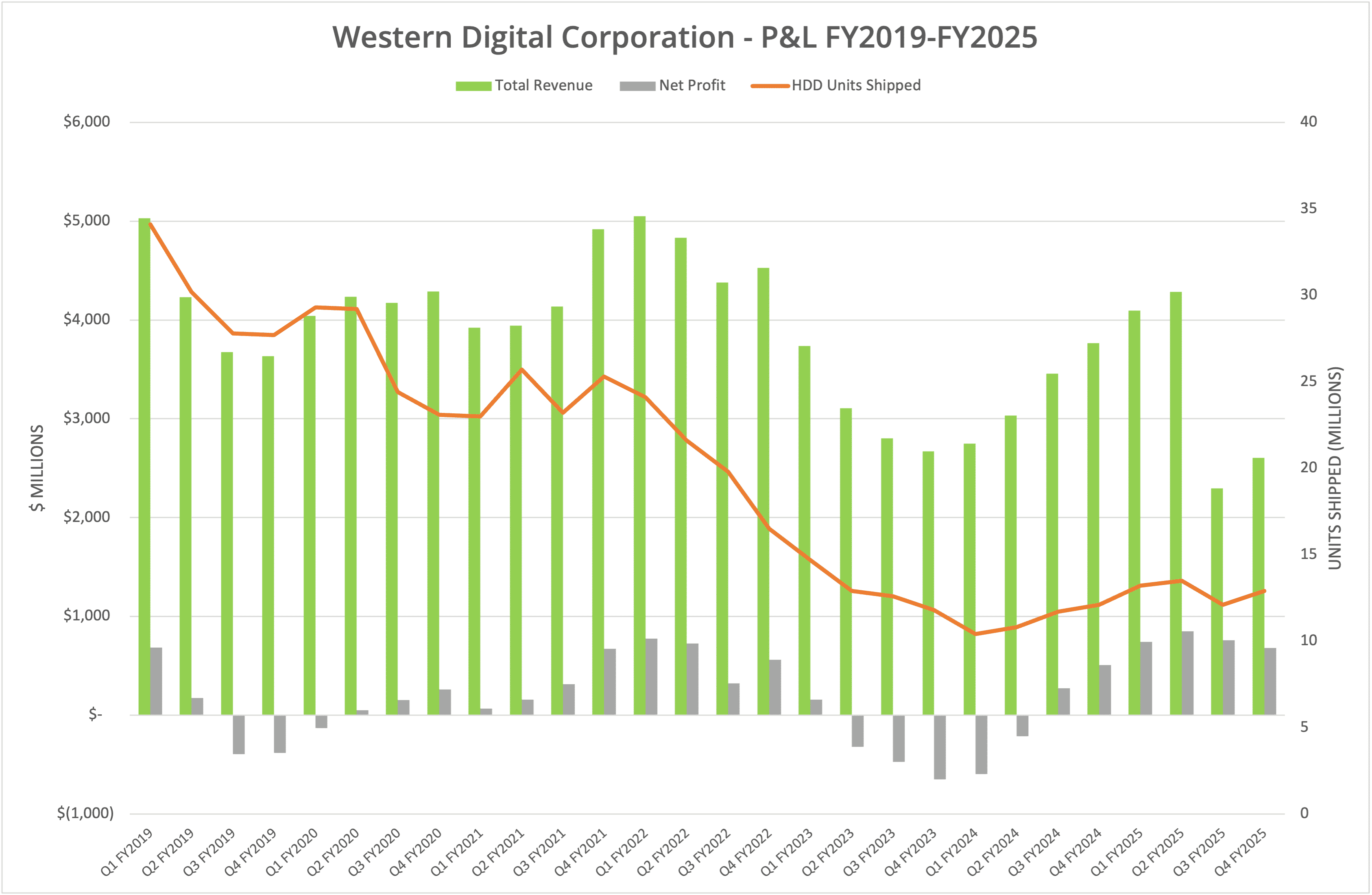

We present the data in six graphs labelled Figures 1 to 6.

Split

Since Western Digital split the HDD business from the SSD division (which became SanDIsk), the current financial details are more difficult to compare with historical data. WD has restated some earnings to show significant year-on-year growth for the current quarter and for the financial year as a whole.

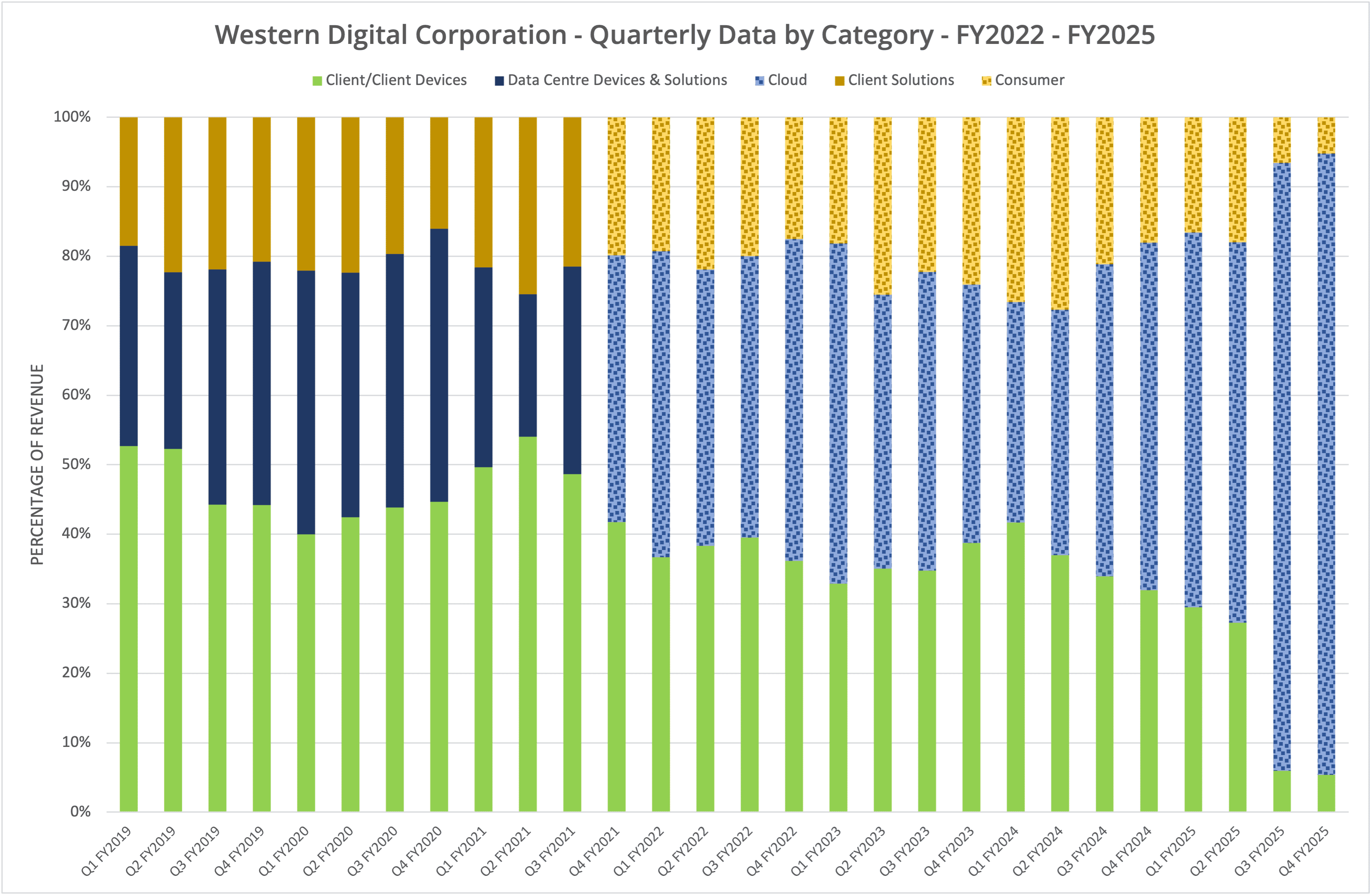

The results are good news for the company and derive from “Cloud” revenue, which accounts for 90% of all sales (Client and Consumer are 5% each, respectively).

Cloud Business

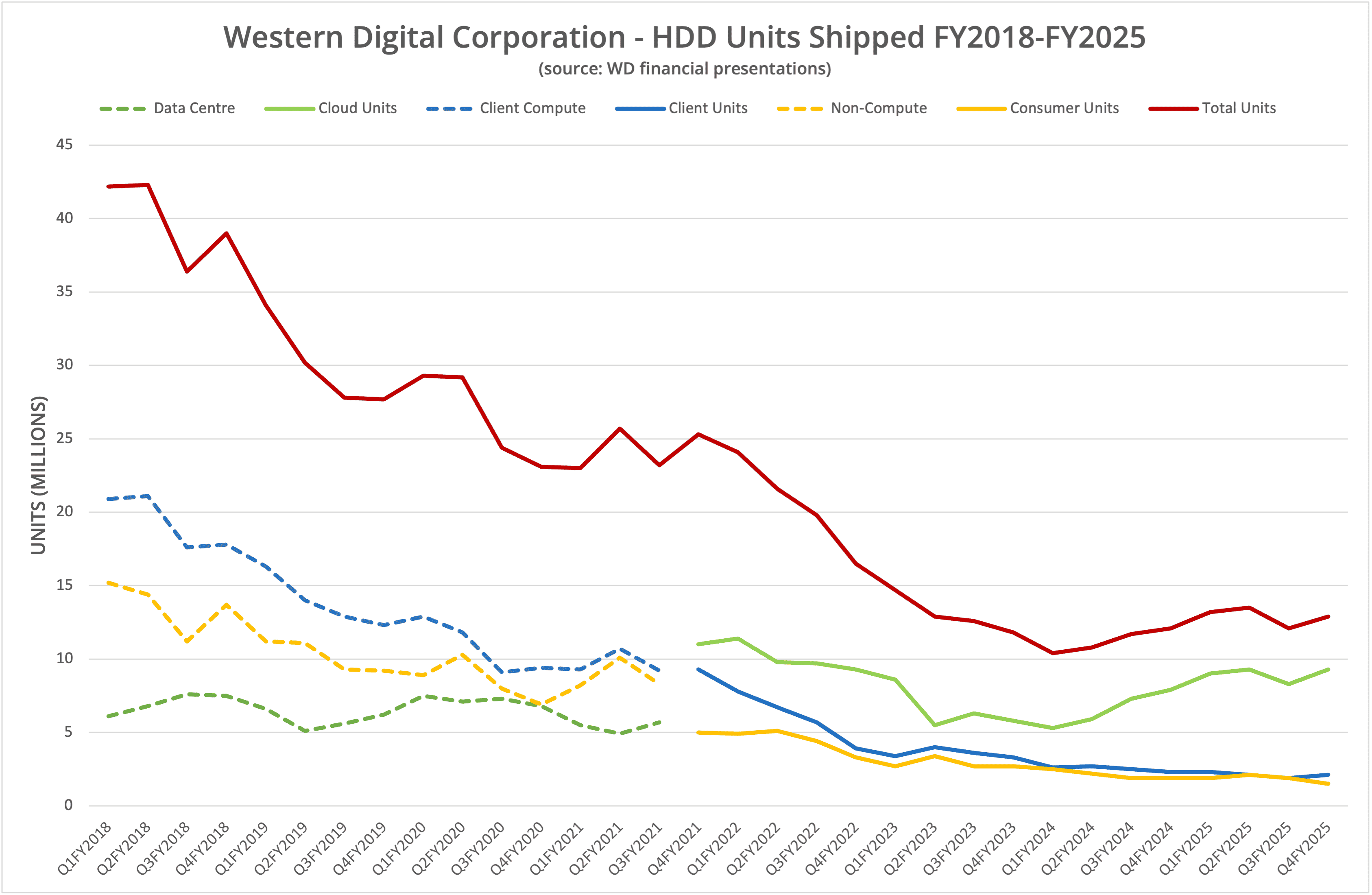

Western Digital, which effectively now only sells hard disk drives, is a commodity seller of storage media to the public cloud. As we’ve highlighted in the past and show in Figure 6, the volume of drives shipped has declined over time (from around 42 million per quarter in 2018) to approximately 12-13 million per quarter.

Over that time, Average Selling Price (ASP) across all media has increased from $60/unit to $179/unit in the last quarter, reflecting the transition to mostly high-capacity archive drives. Generally, the retail unit cost for the newest large-capacity hovers around $600, irrespective of the volume of data capable of being stored.

Unfortunately, Western Digital has chosen not to provide ASP details in the current quarter, a decision that has also been taken by Seagate. There is much discussion on ASP in the post-earnings call transcript. It is clear that financial analysts use this metric as a guide when interpreting the company’s earnings, while WD has decided that the ASP data provides too much information. With some pushing, WD confirmed in the call that the ASP had declined in the current quarter. We will come back to the implications later.

HAMR

Like Seagate, WD is betting on HAMR as the technology to increase drive density over the next decade. During the February 2025 analyst’s day, WD presented a chart showing 36-44TB CMR/UltraSMR drives based on HAMR on a 2026 timeline. 80-100TB drives are predicted for around the 2030 timeframe, with 100+TB drives in the future.

If the industry can meet the current projections, within five years we can expect HDDs that store 2-3 times current capacity but with the same performance as current devices.

TCO

WD believes there will still be a competitive market for hard disks, based on a graphic presented at the analyst’s day. The company expects (based on internal data) the $/TB trend for enterprise SSDs and HDDs to roughly move in the same direction, maintaining a 6x differential in cost.

This metric only holds true if WD can execute on the timeline for new capacity drives. Similarly, we would expect to see the SSD manufacturers keeping to their targets. However, we already have 122TB solid-state drives today, with the promise of 245TB within the next 12 months.

The increasing capacity of SSDs within a single device also affects total cost of ownership (TCO), which WD fails to recognise in the chart. The company does present a graphic showing a 3.6x difference in power, acquisition and other costs. However, we think this number needs more explanation and research, especially with respect to the inability for HDDs to act as a replacement for SSDs in all but the lightest of performance use cases.

The Architect’s View®

Western Digital has a roadmap to 100+TB drives within the next decade. In itself this is a remarkable achievement for the industry that only released the first 1TB drive in 2007.

However, the mechanical nature of HDDs is their Achillies heel. Rotational speed is stuck at 7,200RPM using a single read/write head per platter. Throughput is a function of speed and linear density at around 270MB/s. Random IOPS figures are typically less than 200. In comparison to SSDs, HDD technology performance looks positively stone age.

As we have highlighted many times, $/GB is not an adequate measure of comparison between SSDs and HDDs. TCO, which includes space, power, cooling and performance requirements, are all necessary when making comparisons. HDDs can barely offer anything more than archive performance unless built into very specialised architectures.

Over the next decade, the ability to justify SSDs in place of HDDs will increase. HDDs will be further consigned to the archive tier, especially if current workload limits cannot be increased (current drives offer 550TB/year, or around 20x of capacity, but this diminishes with each capacity gain).

While the constant growth in capacity of individual drives will continue, units shipped will remain flat unless overall storage capacity demands from hyperscale customers increases. The challenge for WD (and Seagate) is that both companies are now dependent on the whims one customer market.

We already know that one hyperscale company, Meta, has started to use QLC in place of some HDD use cases. How long will it be before Amazon, Azure or Google start building custom SSDs with “merchant silicon NAND”, including 5-bit per cell, when (and if) it becomes widely available? Very quickly the demand for HDDs could plummet, in a market with just a single big group of customers.

OK, so that’s the future. Today we can see Western Digital has successfully achieved the spin-off of the SSD business into SanDisk and continues to experience growth in revenue and HDD demand. This is good for the company and investors, but surely the spectre of further SSD transition is just around the corner.

Copyright (c) 2007-2025 – Post #33fc – Brookend Limited, first published on https://www.architecting.it/blog, do not reproduce without permission.