Intel Corporation has announced financial data for the second quarter of FY2025, ending on 28th June 2025. Revenue was flat for another quarter, when compared year-on-year to FY2024, at $12.9 billion. Gross margin declined, while expenses pushed the business into a $3.2 billion loss for the period. Intel is working hard to stabilise the financials of the company, but more work is needed on a direction for the future.

Background

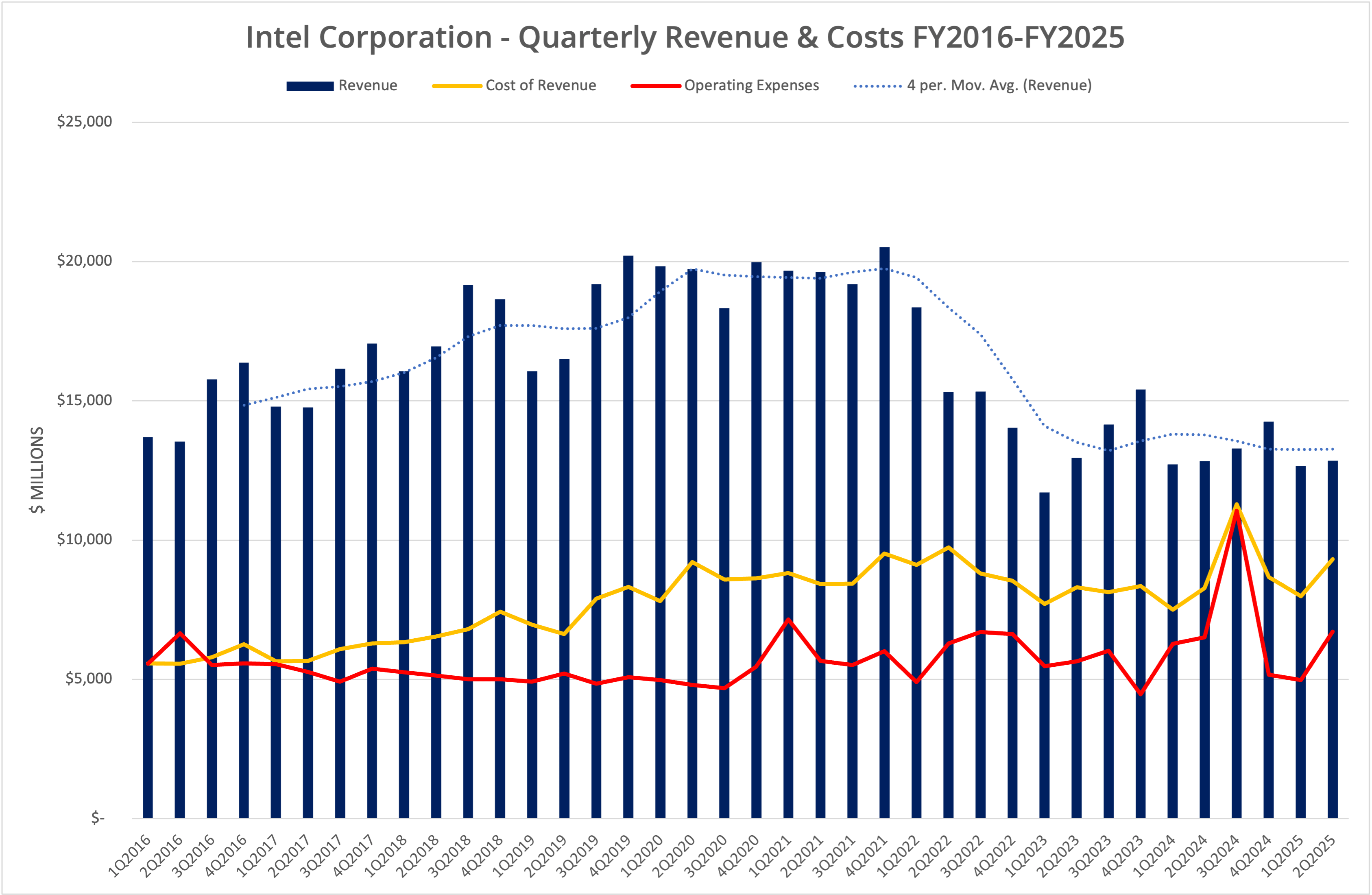

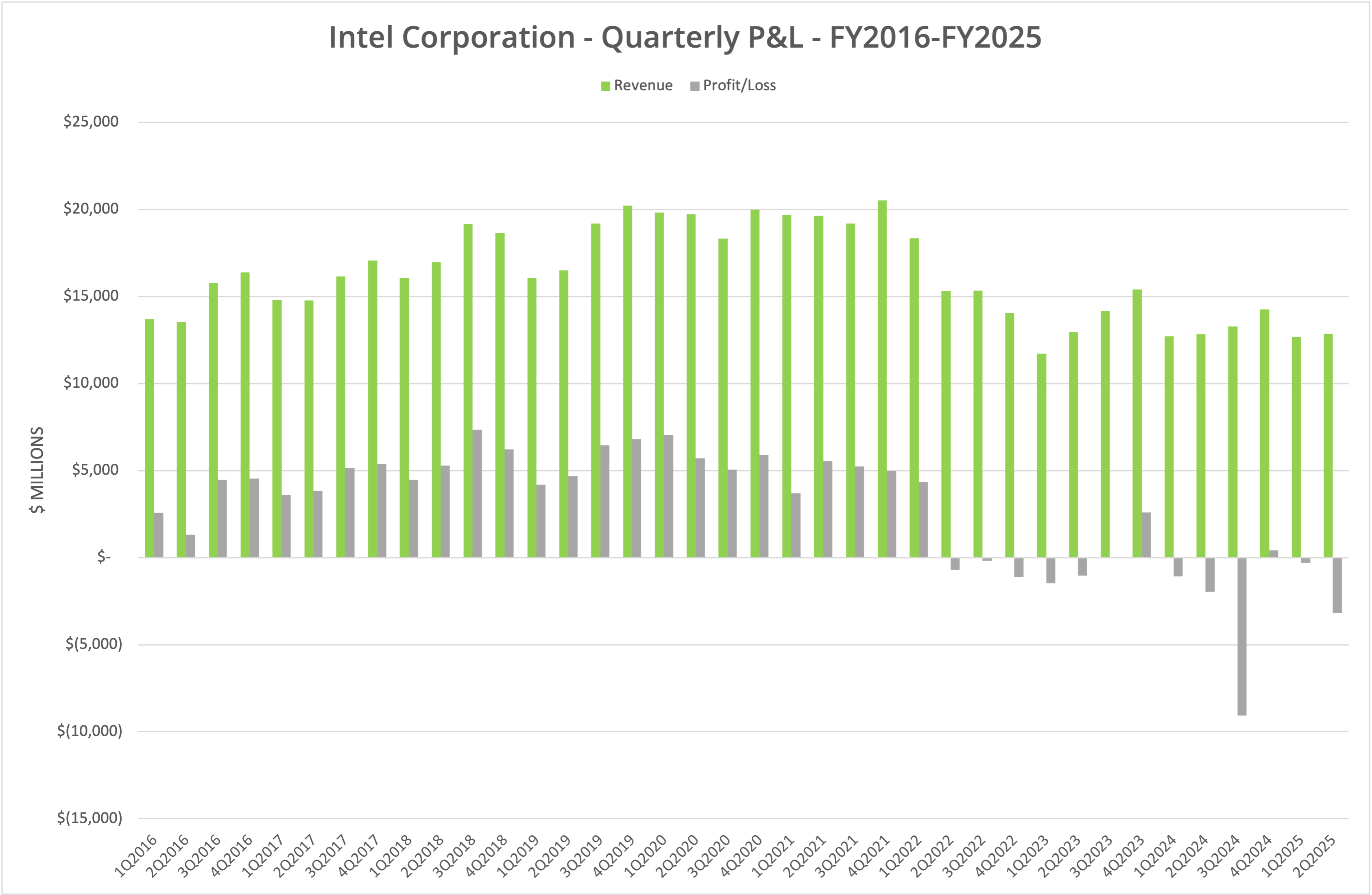

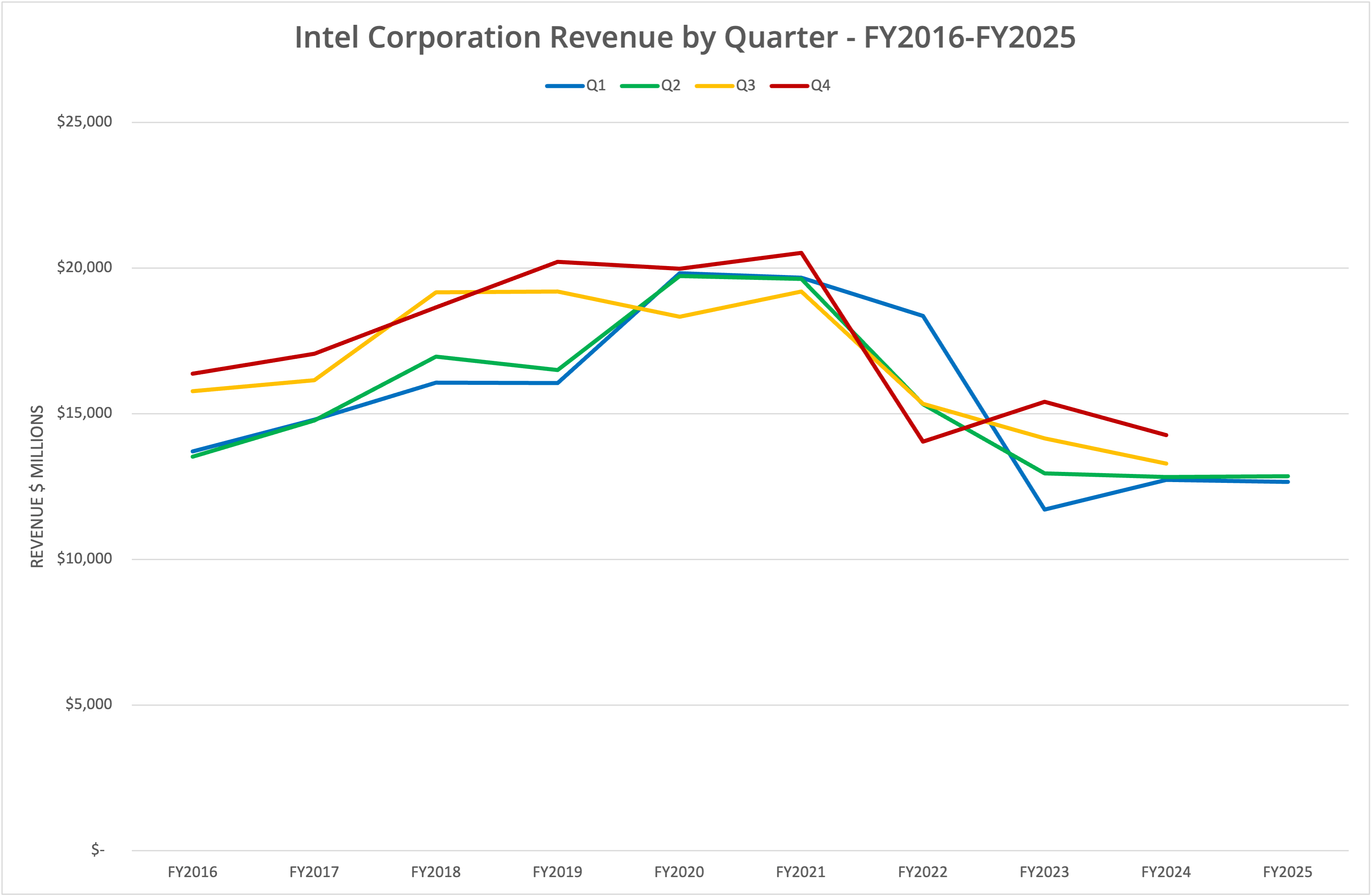

Intel Corporation declared financial results for Q2 FY2025 (the period ending 28th June 2025) on 24th July 2025. Revenue for the period was flat at $12.9 billion, while expenses (including impairment charges) increased, pushing the company into a $3.2 billion loss.

We present the data in four graphs, labelled Figures 1 to 4.

Stabilisation

It’s difficult to know where to start when discussing the turmoil occurring at Intel. In the last few weeks, the US government (specifically Donald Trump) has called for the resignation of newly appointed CEO Lip-Bu Tan, due to his involvement in a raft of Chinese companies. This was followed up with a face-to-face meeting at the Whitehouse and the announcement of potential plans for the government to invest in Intel further than has been implemented through the CHIPS Act.

Meanwhile, as part of the financials announcement, Intel indicated that fab projects in Germany and Poland have been cancelled. Some consolidation of overseas sites will occur, with assembly and test operations moving from Costa Rica to Vietnam and Malaysia (presumably, those locations are cheaper to operate). Staff cuts continue, with a target of 75,000 total employees by year end.

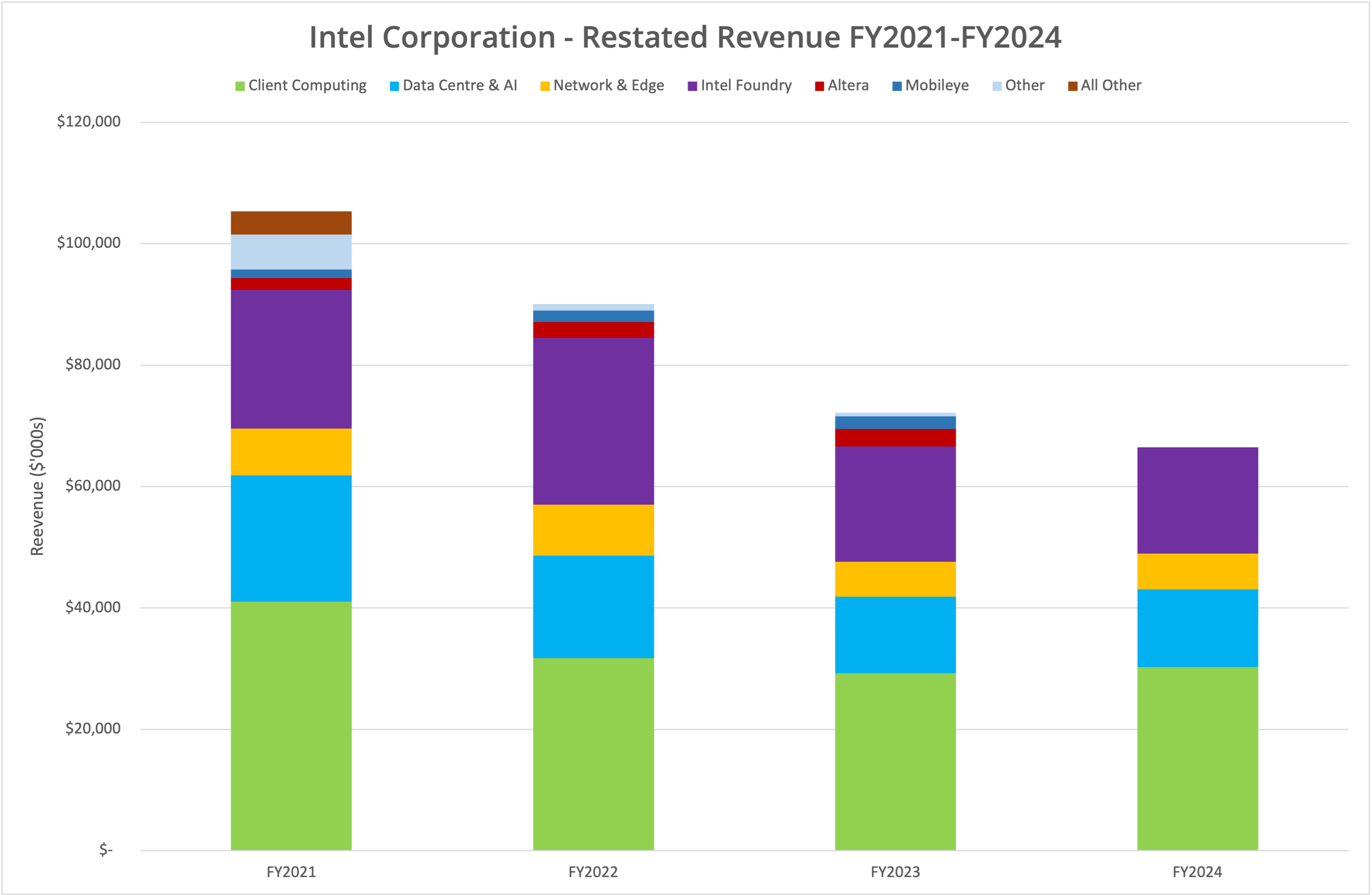

Foundry

While Lip-Bu Tan focuses on bringing costs and spending under control, questions arise for the future of the foundry business. The current 18A process will form the foundation of at least the next three generations of processor products (as highlighted in the earnings call), but the future of the next process size reduction, 14A, is in doubt. Tan indicated that investment in 14A will only occur if there is customer demand to justify the capital spending.

The increase in capital costs at Intel 14A makes it clear that we need both Intel Products and a meaningful external customer to drive acceptable returns on our deployed capital, and I will only invest when I am confident those returns exist.

Lip-Bu Tan, Intel CEO

However, this statement feels like a step backwards. Surely customers need to have confidence in the development of 14A before they commit? Unfortunately, write-downs like the $800 million impairment that pushed the quarter into a loss won’t inspire the market with confidence.

The Architect’s View®

Intel Corporation continues in a holding pattern while the dire financial position is corrected. However, that position risks turning into a death spiral (as I commented on LinkedIn recently) if the company can’t solve some fundamental issues.

- Better products. The x86 architecture is being displaced by Arm in the public cloud and risks being sidelined in hyperscale environments. Similar challenges are emerging on the desktop, with little appetite for the “AI PC”. While raw power has always been the strength of x86, the future is predicated on performance with efficiency, simply due to the massive scale of computing demand being driven by technologies like AI. Intel also has challenges with the GPU market segment, where its products are non-existent.

- Making the Foundry business a success. TSMC has both the capital and momentum, being the first choice for the majority of processor manufacturers. While the risks of the supply chain exist, we don’t believe they are enough to justify customers moving away from TSMC in any meaningful way. In the current cost-cutting vein, we also don’t think Intel has sufficient capital to compete against TSMC.

We don’t for a moment believe Intel is about to go out of business anytime soon. There is a huge and continuing demand for x86 products that will last for at least the next decade. But the signs of competition are easy to see.

Rather than expand at length on the issues in this quick financial review, we will provide a more detailed analysis in a separate commentary post. In the meantime, Intel will continue to garner headlines for all the wrong reasons. Finding a path to re-invention needs some radical ideas and changes in direction, we hope the company is prepared to make.

Copyright (c) 2007-2025 – Post #bb44 – Brookend Ltd, first published on https://www.architecting.it/blog, do not reproduce without permission.