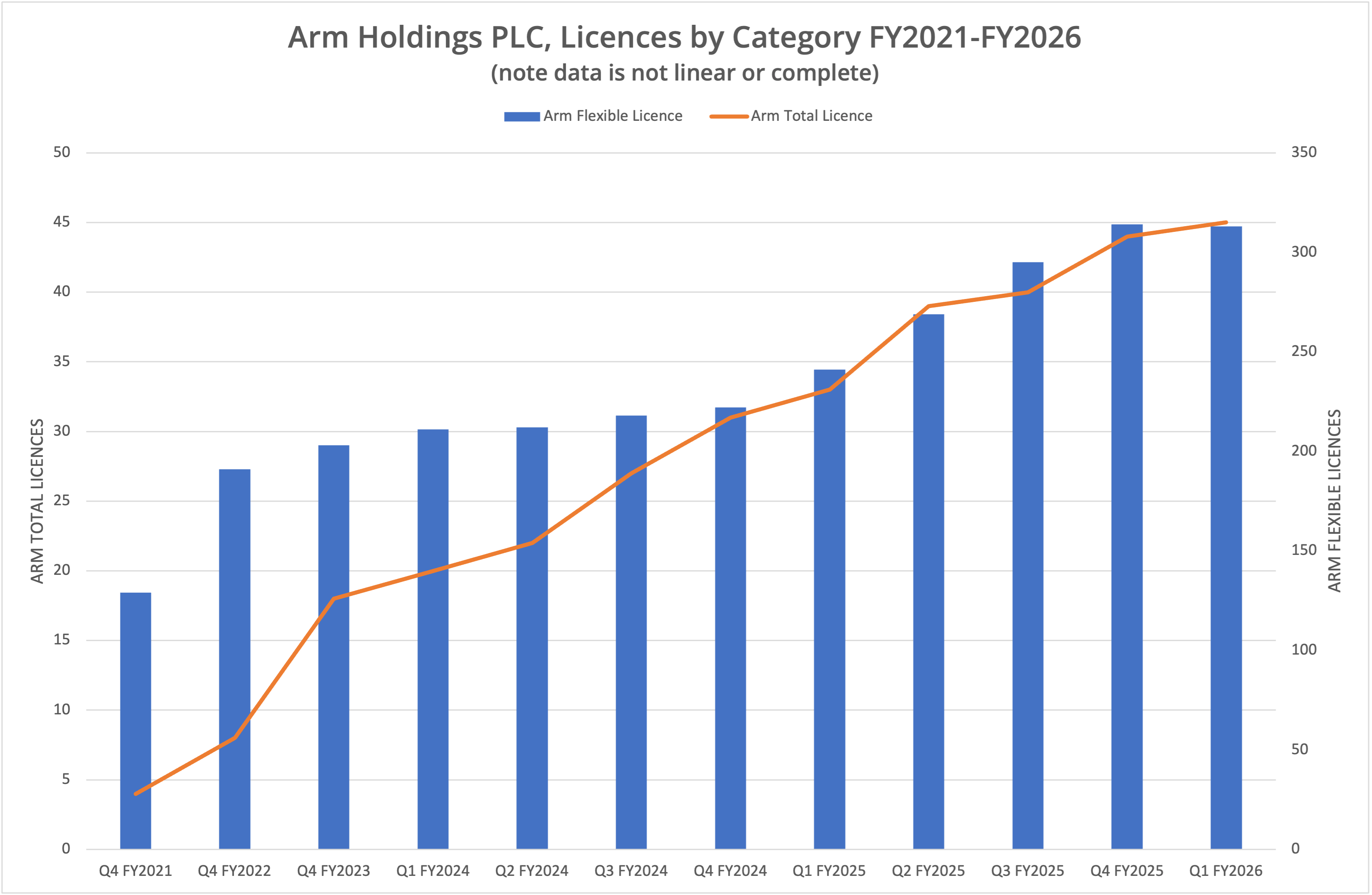

Arm Holdings PLC announced financial results for Q1 of FY2026 (ending on 30th June 2025) on 30th July 2025. For the quarter, revenue was up year-on-year compared to Q1 FY2025 by 12.1% at $1.053 billion, driven by a 25.3% increase in royalty revenue. However, sequentially, revenue was down 15.1%, a reflection of the quality of Q4 FY2025. For the first time since public data was available in Q4 FY2021, Arm Flexible Licences dropped slightly. Time for a change of direction?

Background

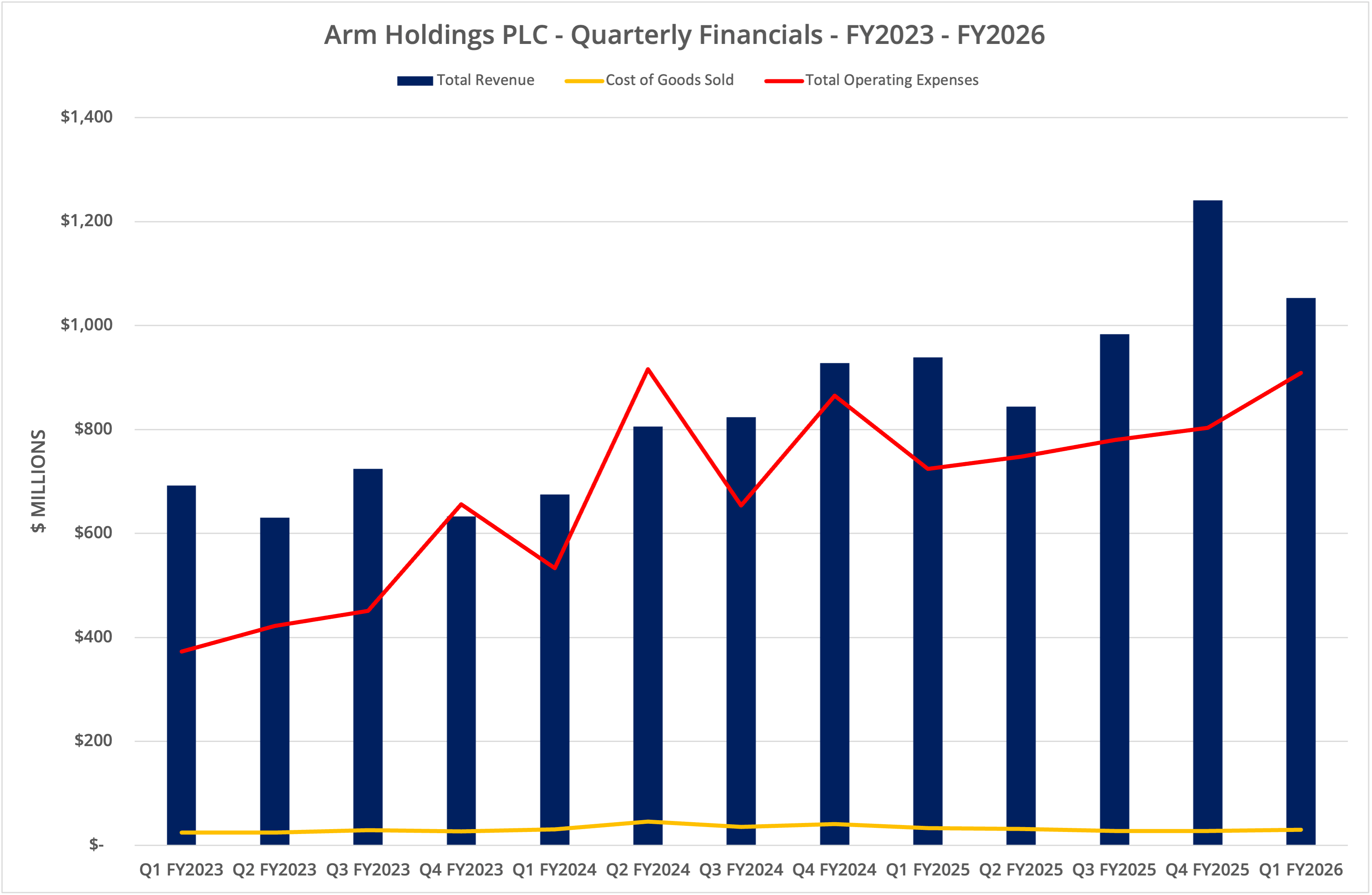

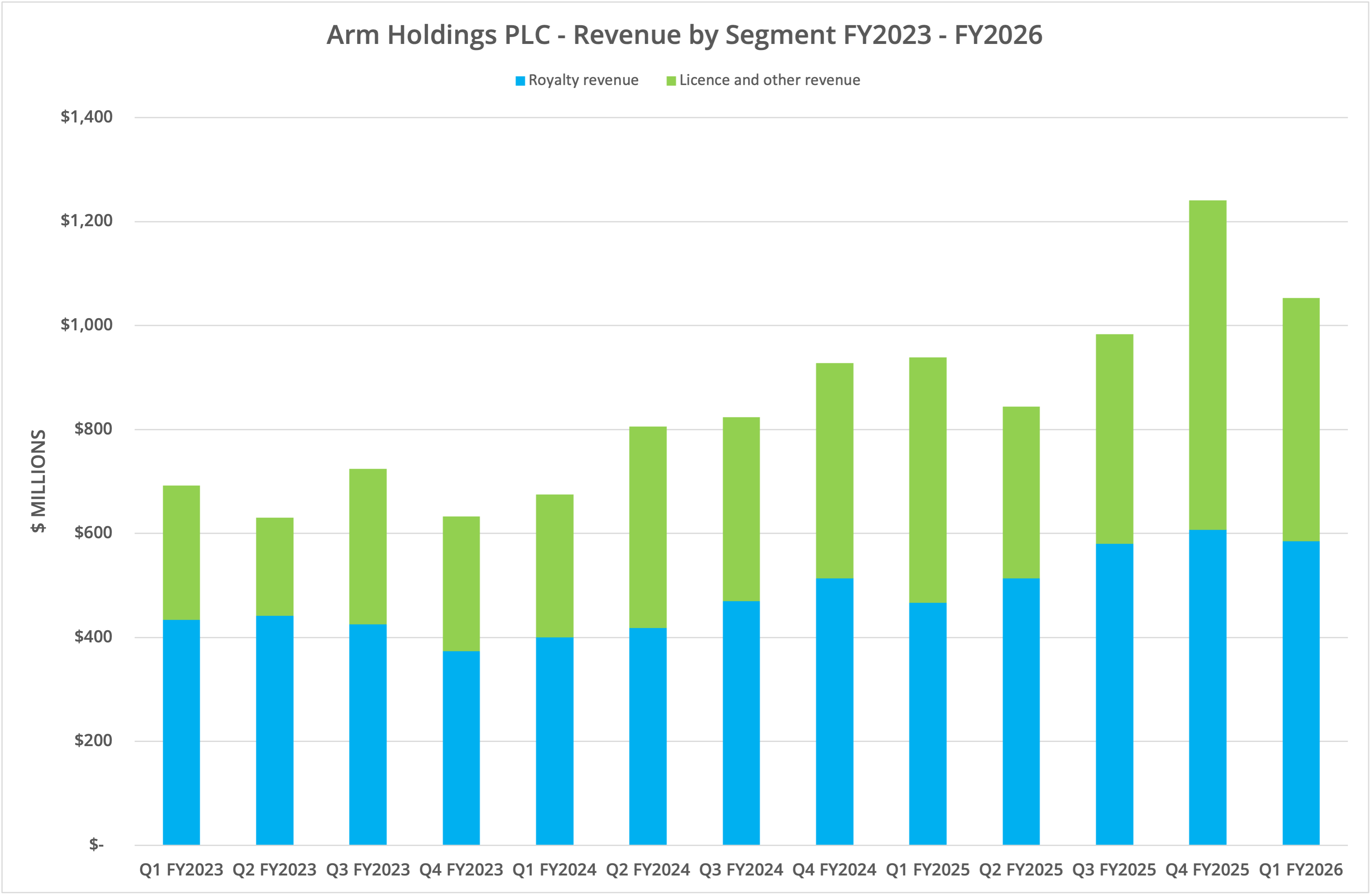

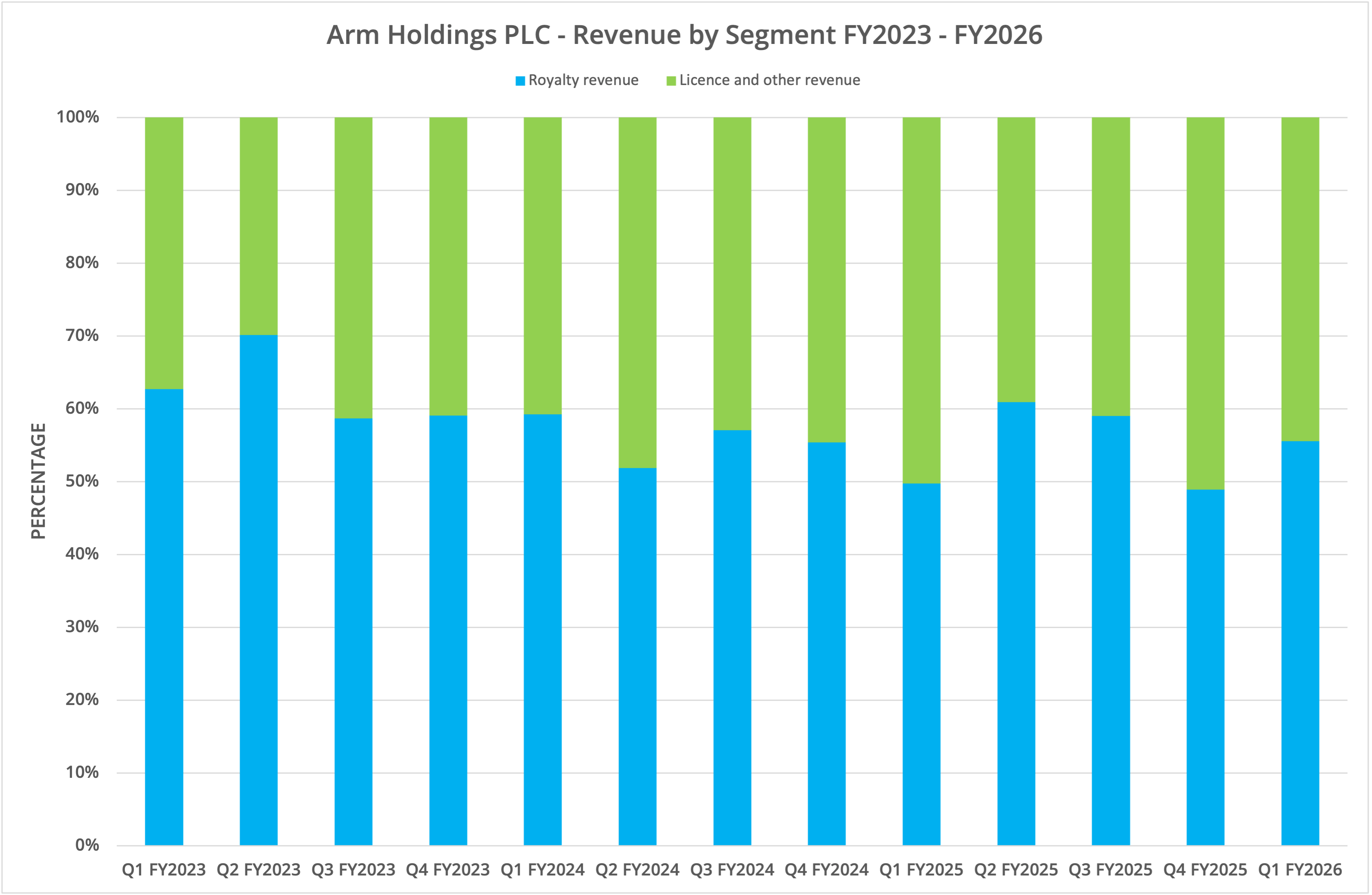

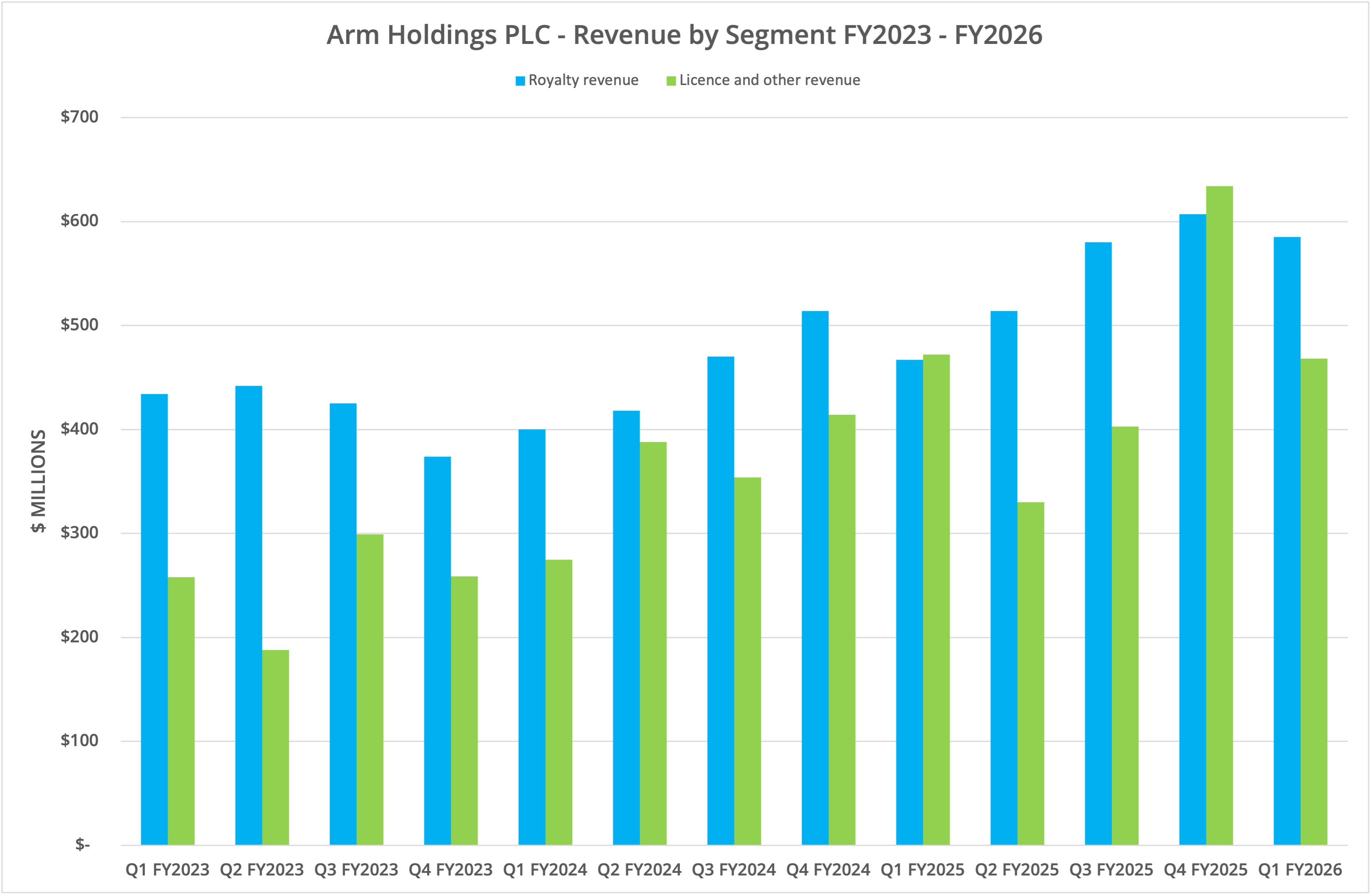

Arm Holdings PLC published financial results for the first quarter of FY2026 (ending 30th June 2025) on 30th July 2025. For the quarter, revenue was up year on year by 12.1% at $1.053 billion. This increase was driven by a 25.3% increase in Royalty Revenue. Licence and Other Revenue was flat, down slightly at 0.8%.

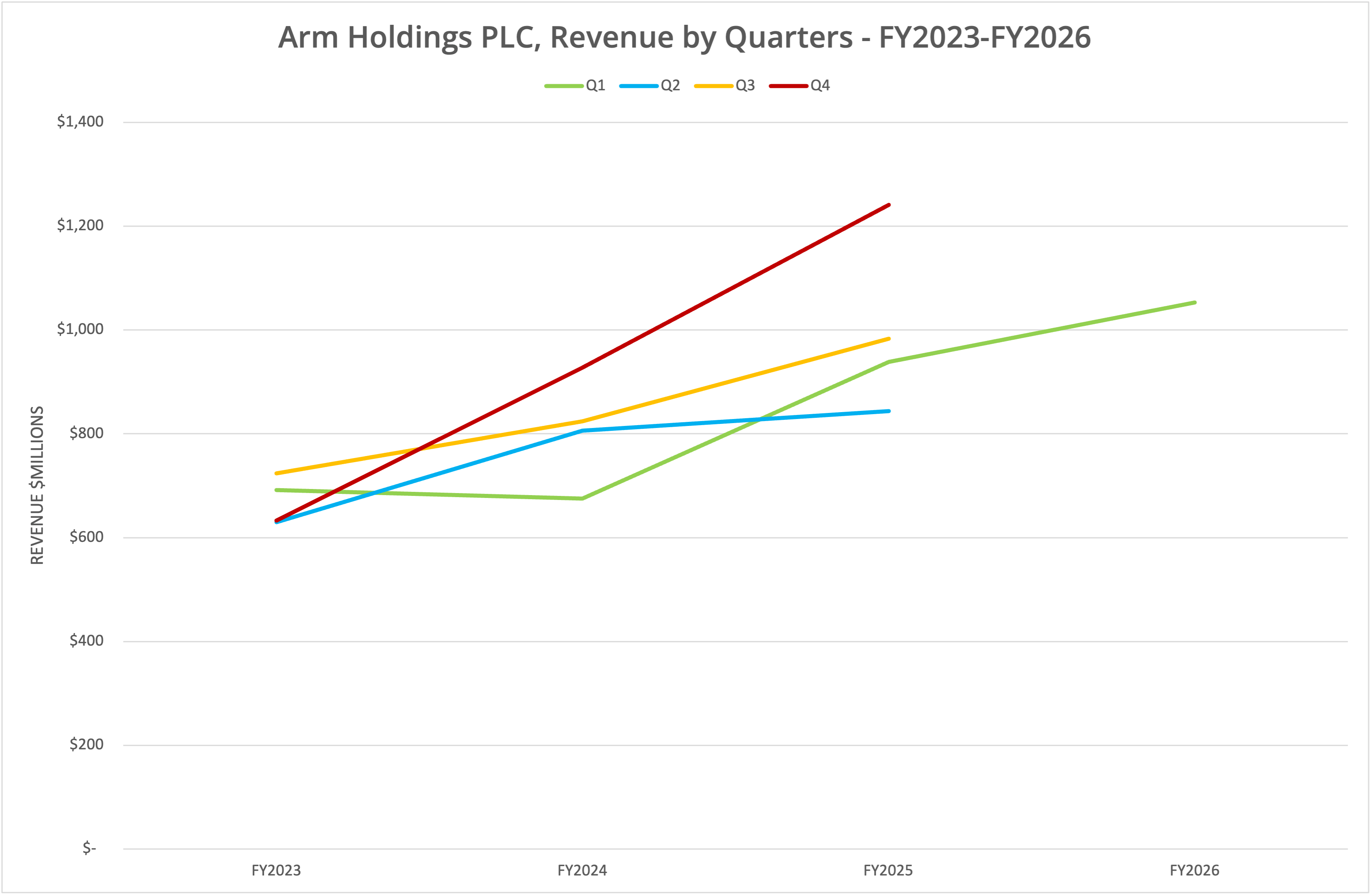

Compared to the previous quarter, revenue declined by 15.1% (Licence and Other Revenue was the big loser by 26.2%). We present the data in six graphs, labelled Figures 1 to 6.

Expectations

Financially, Q1 FY2026 initially looks disappointing when compared to the previous quarter, which did see a marked rise in revenue. However, the current quarter was only the second in Arm history to exceed $1 billion in revenue, with Royalty Revenue up 25% year-on-year, representing a record for the company. Arm CEO Rene Haas attributed some of the reduction in revenue to the regular licensing cycle.

Neoverse

Current growth is down to the increase in adoption of Neoverse in the data centre and public cloud. Arm claims that 70,000 businesses now run AI workloads on Arm chips, an increase of 40% year-on-year. In hyperscale platforms, Arm expects a 50% share of the market, which is remarkable, considering the relative youth of the platform across public clouds. Of course, Arm is also deployed as part of NVIDIA superchips such as Grace Blackwell.

New Markets

Arm licenses levelled out during the quarter (see Figure 6), with Total Access licences up by one and Flexible Access licences down by one. Licensing can’t grow indefinitely, as there is a natural limit of vendors looking to develop solutions based on Arm cores (although those vendors could drive more revenue for Arm by virtue of products sold).

As a result, we see Arm discussing GPU and NPU technology in the current CEO shareholder letter. There is an opportunity for Arm Ethos NPU and Immortalis GPU technology at the edge, in targeted use cases that aren’t purely related to large-language models. This is an area we will cover in more detail with specific research.

While the numbers might not look as good as expected, we see no change in the prospects for Arm’s business, which is gaining further market share in some parts of the enterprise data centre (specifically the public cloud).

New Business

What new business areas could Arm move into?

Earlier in the year, it was widely reported that Arm could move into chip manufacturing, starting with CPUs. Meta is one of the first customers identified in the press stories. The idea that Arm would compete against customers has taken the industry by surprise, but in reality, it is a logical move for the company.

To understand why, we need to look more closely what at Arm currently offers today. The central IP provided to customers is based on processor and GPU cores, from which the customer builds custom designs to meet their requirements. This is a process Apple, for example, has been doing for many years on the mobile and tablet products, more recently with MacBooks.

Building the hardware ecosystem around Arm cores requires engineering skills, which is why Arm also offers the Compute Subsystem (CSS) platform to aid the development of complete products. In general terms, think of this as being analogous to the chipset provided by Intel and AMD that builds on x86 processors.

We envisage that Arm’s plans are less about manufacturing hardware and selling discrete components, and more focused on creating SoC designs that could be built into server and consumer products with much less engineering and development time by the customer.

The one area this makes the most sense is the on-premises data centre, where Arm could develop solutions that make it easier for vendors, including Dell, HPE and Supermicro, to create Arm-based server solutions for enterprise customers.

Of course, this area may not be the target at all. The intention may be to bypass traditional vendors and develop solutions for larger customers using OCP designs, such as tier one and tier 2 public cloud and hyper-scale platforms (Meta is the obvious example).

The Architect’s View®

As Intel Corporation flounders, the winners are currently Arm and AMD. AMD is tied to the x86 architecture (for the moment), while Arm offers the most credible alternative across consumer and enterprise markets.

There is always a finite limit to the number of licenses Arm can sell (although those licences individually can become more valuable). As a result, new markets, such as more complete products, are a logical next step for the company.

News on Arm processor designs is expected in the summer (which is now), so an announcement could be imminent. Whatever is revealed, this moment could be pivotal in the next stage of Arm’s evolution and the direction of the processor market.

X-Ray: Arm Holdings PLC

This Architecting IT report takes a deep dive into Arm’s history, products, services, and future outlook. This report is only available for download via paid subscription.

Copyright (c) 2007-2025 – Post #3a22 – Brookend Limited, first published on https://www.architecting.it/blog, do not reproduce without permission.