AMD, Inc. has announced financial results for the first quarter of FY2025, the period ending 29 March 2025. Revenue rose 35.9% year-on-year to $7.44 billion. However, sequentially, that represented a 2.9% decline over Q4 FY2025. The latest results were driven by gains in Data Centre and Client business units.

Background

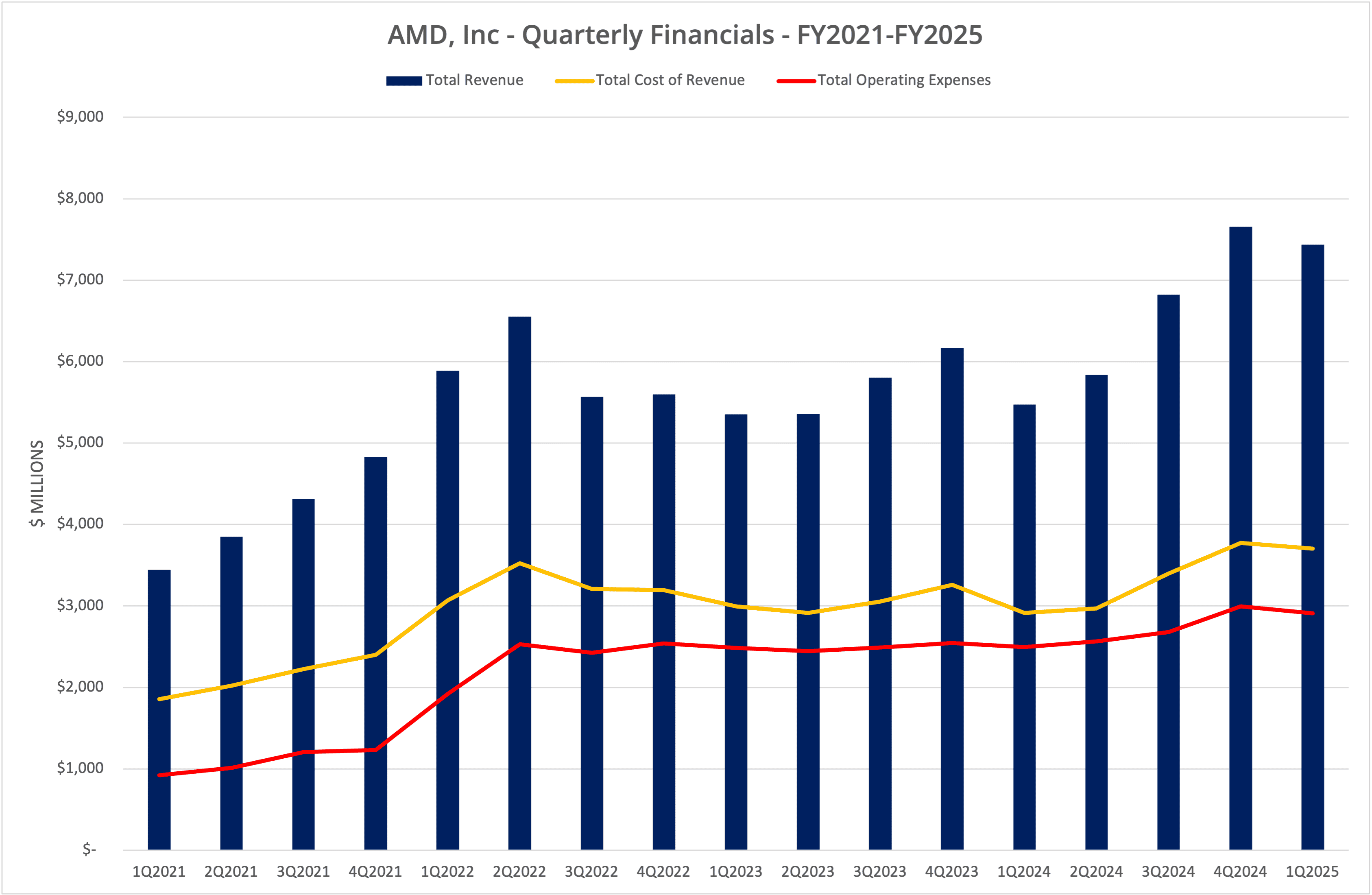

AMD, Inc. announced financial data for Q1 FY2025 (the period ending 29 March 2025) on 6 May 2025. Year-on-year, revenue grew 35.9% to $7.44 billion, although this was down 2.9% from the period Q4 FY2024.

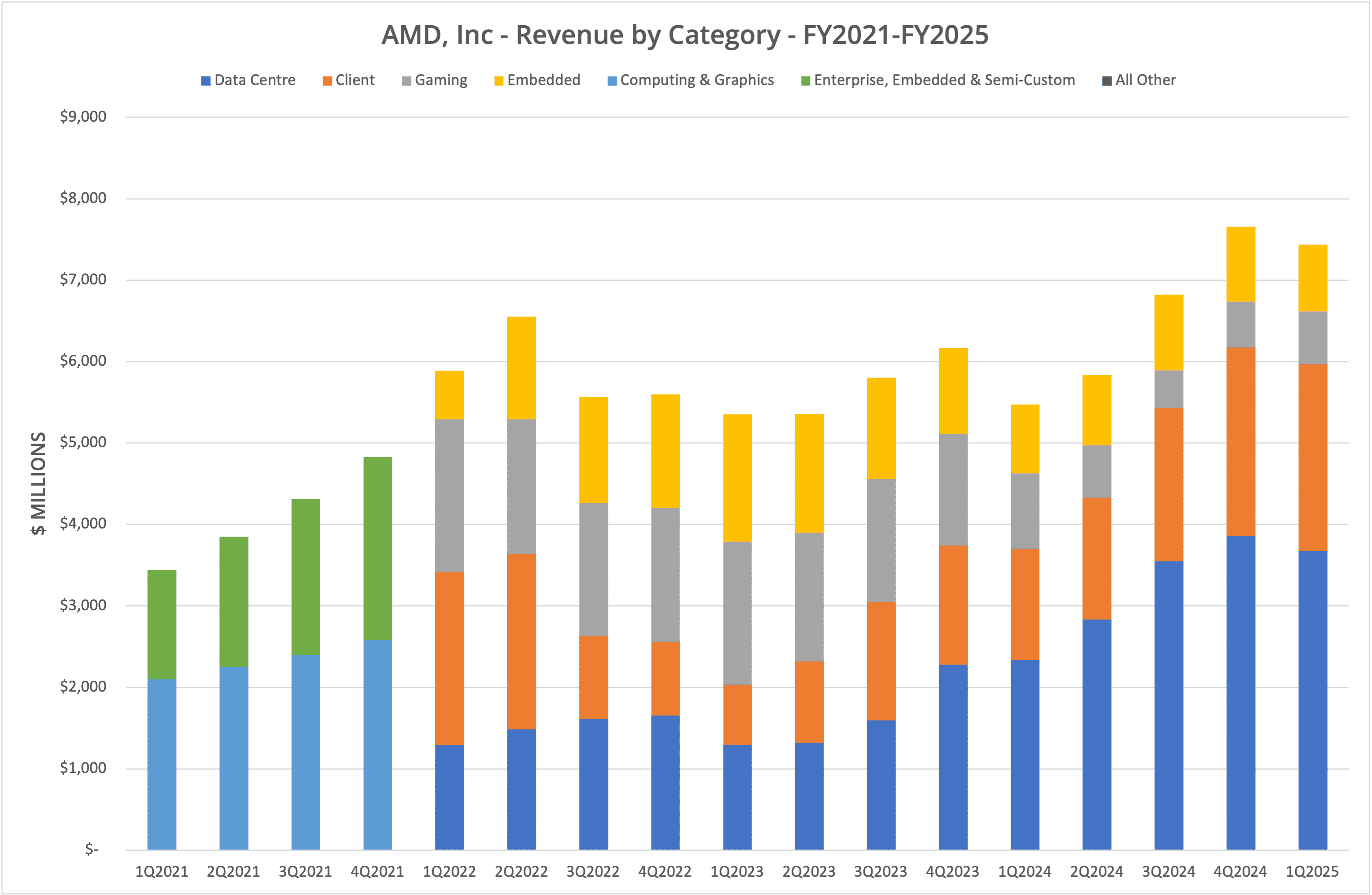

Looking at the individual lines of business, Data Centre and Client saw the greatest improvement, rising 57.2% ($3.7 billion) and 67.7% ($2.3 billion) year-on-year respectively. The Gaming division declined significantly, down 29.8% to $647 million. However, sequentially, that represented a 14.9% improvement. The Embedded business unit fell 2.7% to $823. AMD declared a profit of $825 million for the quarter, with a 50% gross margin.

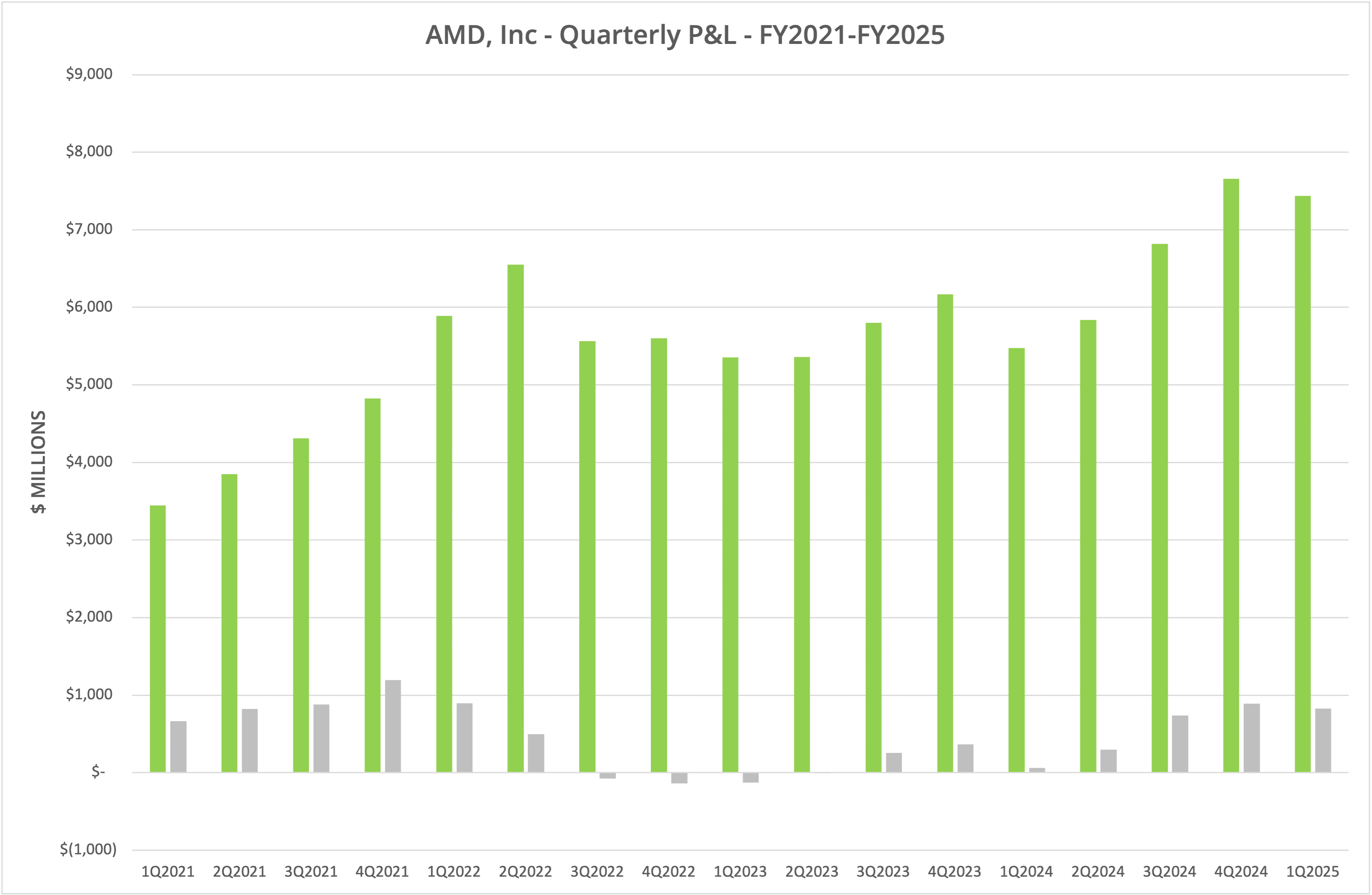

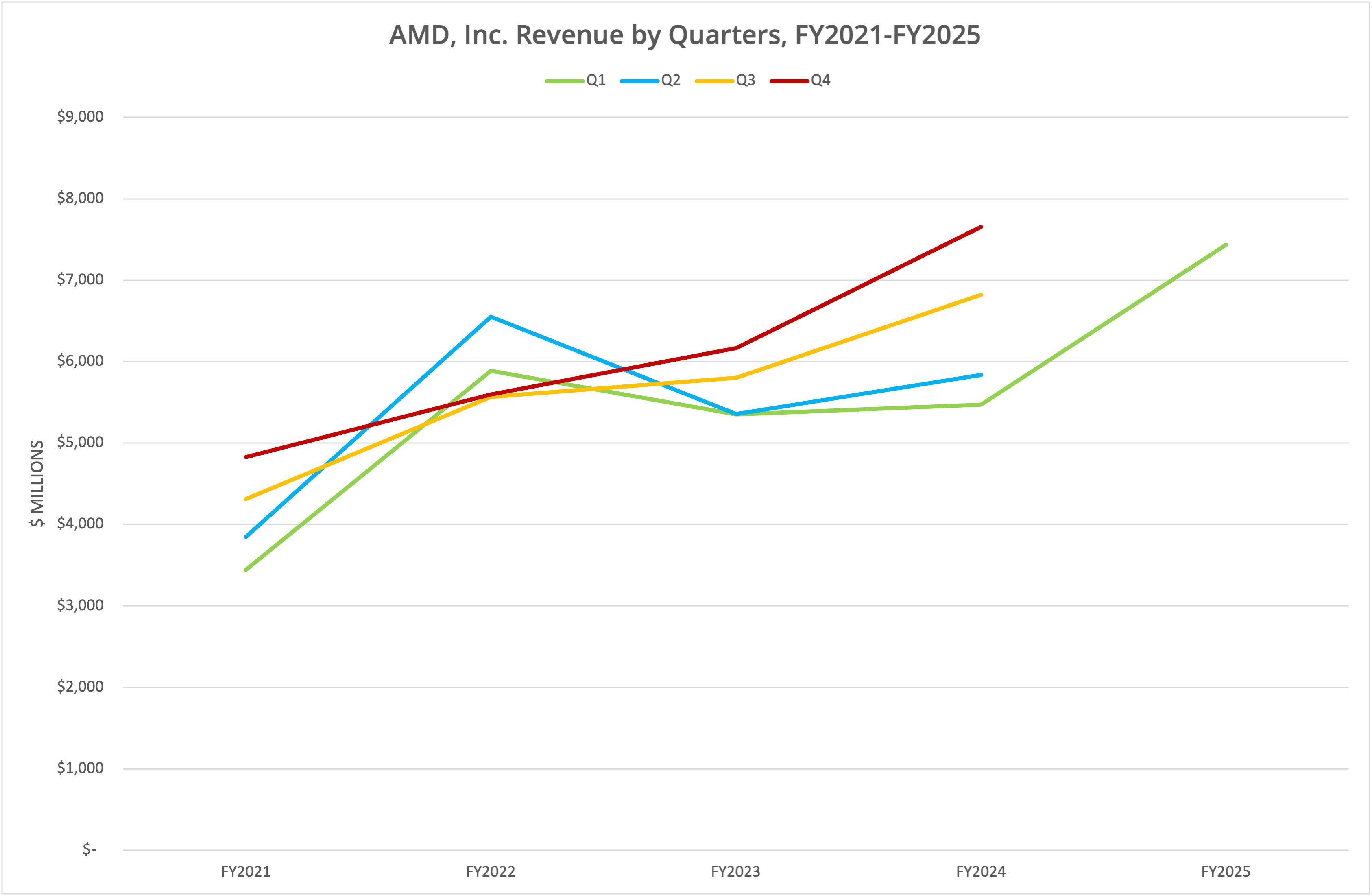

We present the data in four graphs, labelled Figures 1 to 4.

Transformation

Collectively, Data Centre and Client business units represented 58% of revenue in Q1 FY2022, the first period of the current reporting structure. That figure dipped to 38% the following year but has steadily increased to 80% today.

AMD attributes the growth in Data Centre and Client to the demand for EPYC processors in enterprise data centres and the public cloud, Instinct GPUs and Zen 5-based Ryzen processors on the desktop. This is an identical mix of products reported in the previous quarter as AMD solidifies its position in the processor market.

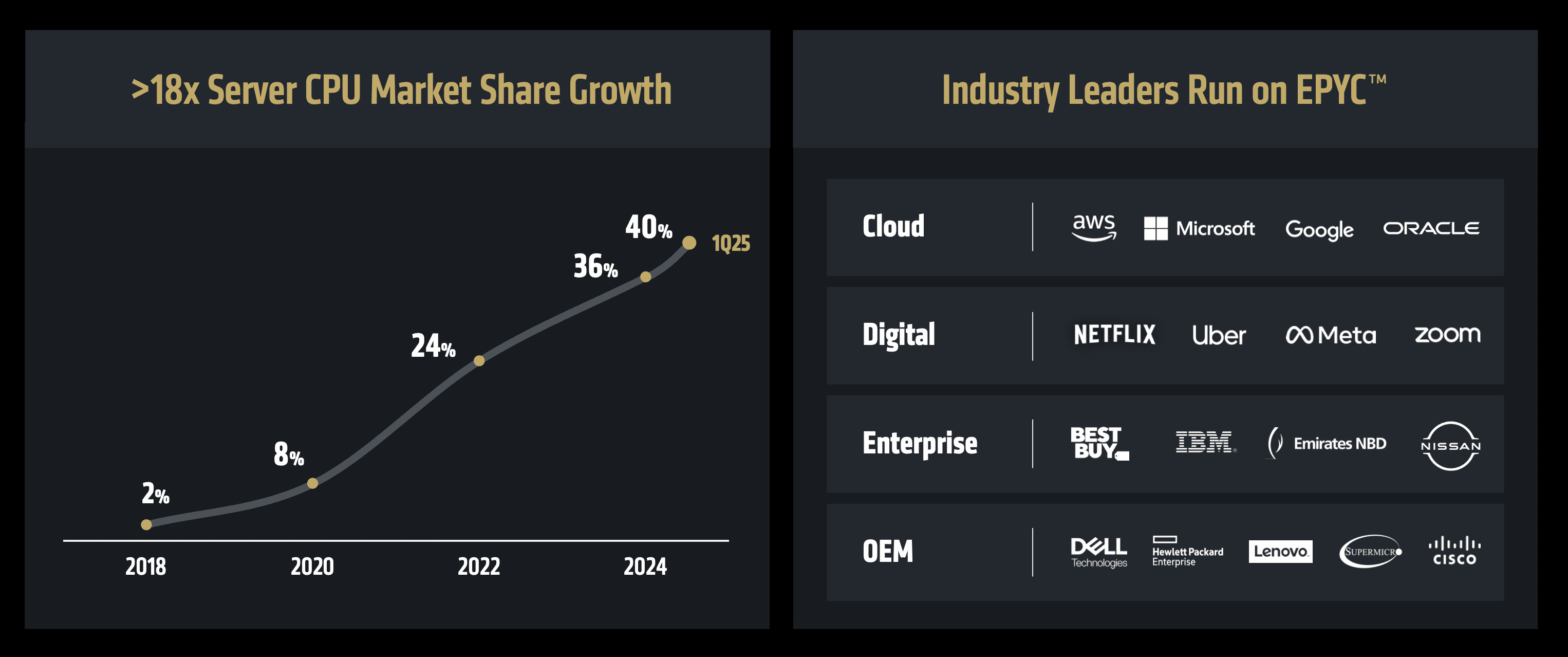

At its recent “Advancing AI” event, AMD highlighted continuing market share growth for the EPYC platform at 40% in the current period. Figure 5 shows this data, which has increased remarkably from just 2% in 2018 (EPYC was first introduced in June 2017). EPYC has held a strong leadership position compared to Intel Xeon, something we will cover in a separate research note.

AI

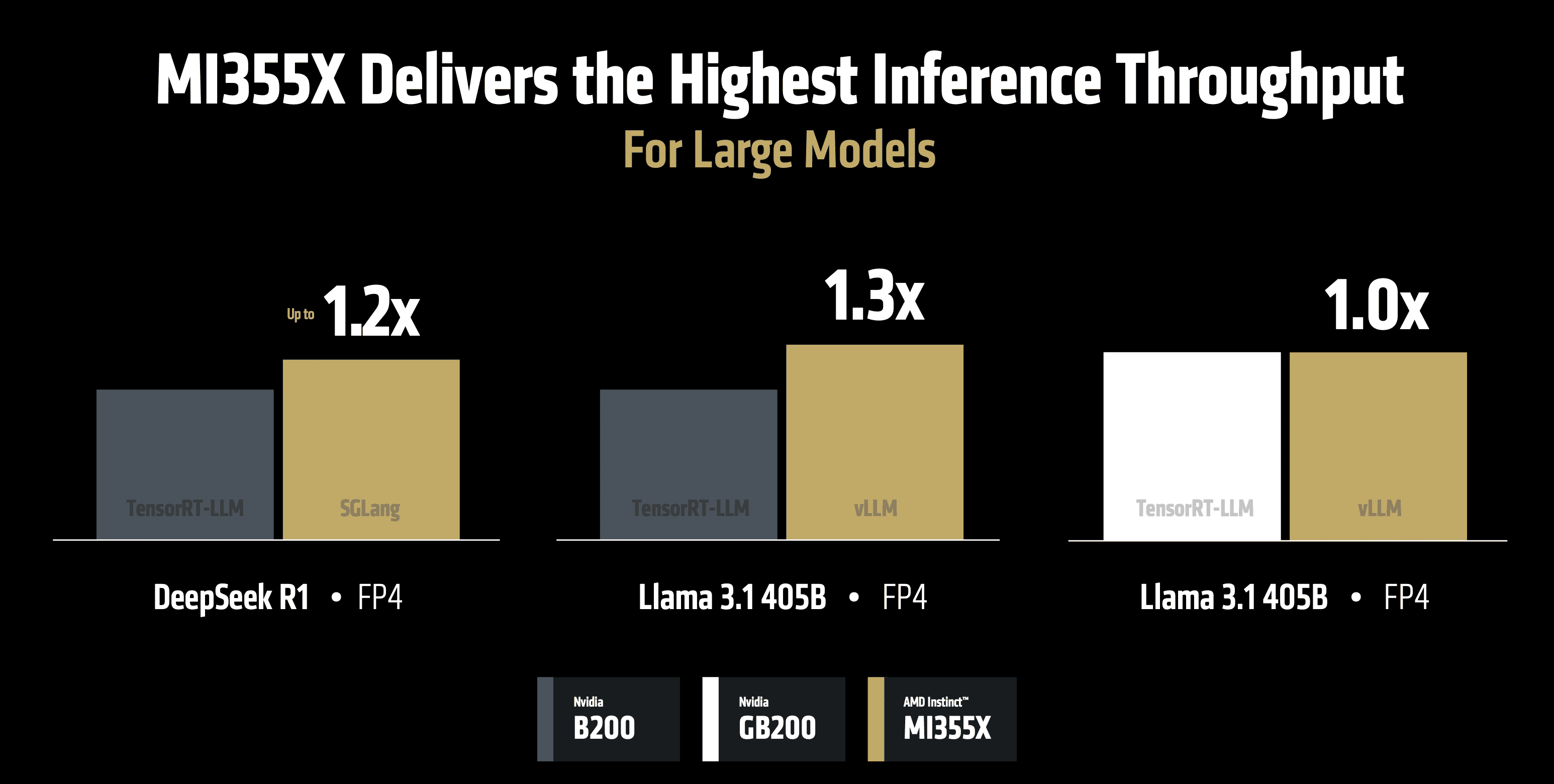

In the GPU market, AMD asserts strong leadership with the Instinct GPU family of products, claiming 40% more tokens/$ with the Instinct MI355X than NVIDIA B200. AMD claims slightly better or equivalent inferencing performance with NVIDIA B200 and GB200 platforms, although it is interesting to note that the differences are marginal (see Figure 7).

In software, AMD believes the open-source model of ROCm (its GPU programming framework) is a differentiator. The company announced ROCm 7 at the recent Advancing AI event, with an average of 3.5x performance improvement over ROCm 6.

As we’ve seen with the demand for GPU computing power, there will need to be some dramatic performance improvements over the next few years if the promise of AI is to be realised. Software and hardware stacks will need continued optimisation.

The Architect’s View®

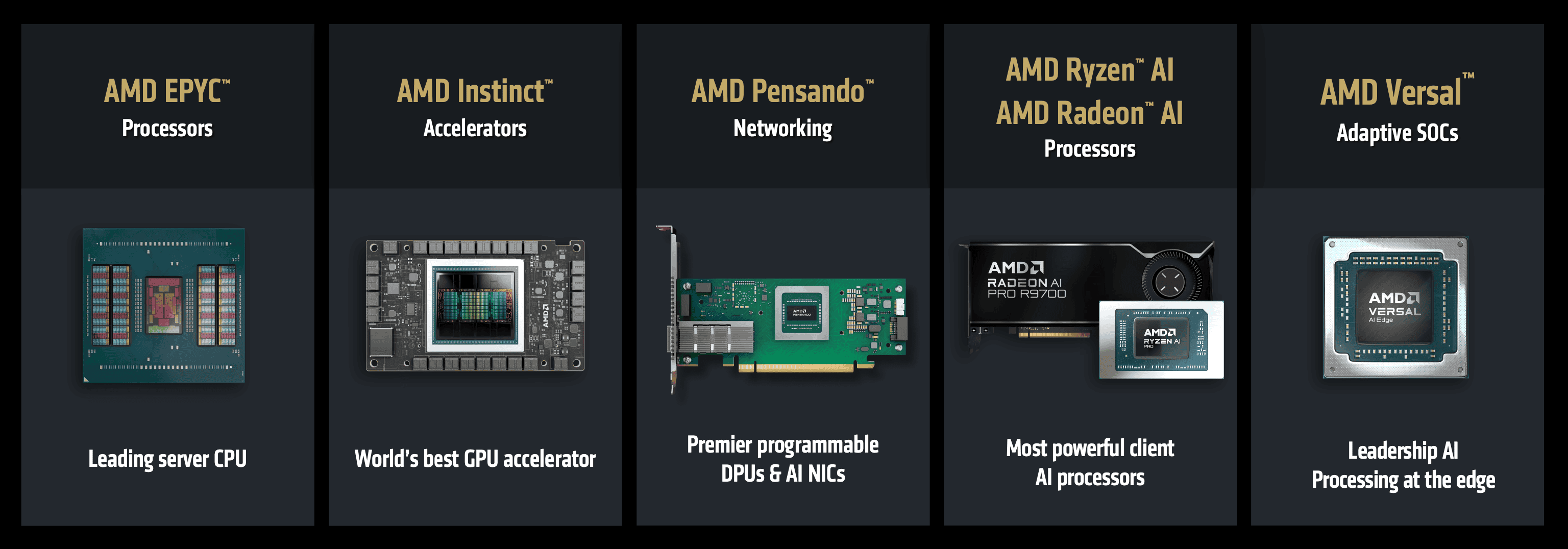

One of the most interesting slides presented by AMD at Advancing AI shows the portfolio of products offered across the broad spectrum of markets (Figure 6 above). For the enterprise data centre, this means EPYC processors, Instinct GPUs and Pensando Networking. The Client space is covered by Ryzen and Radeon product lines.

The acquisition of ATI in 2006, Xilinx in 2020 and Pensando in 2022 has placed AMD in a leadership position compared to Intel, certainly in the data centre market and increasingly on the desktop. Compare the current AMD growth success with Intel, where the company is shedding jobs and business divisions rather than bringing them together.

In this respect, AMD has several years of growth trajectory ahead, specifically with the demand for data centre GPUs and the ability to take share of the CPU market from Intel. What then?

In the CPU market, we see an increasing threat from Arm, a scenario we’ve highlighted for many years. The result could be a three-way competition, with Intel, Arm and AMD all looking to take market share. Currently, AMD has the advantage over Intel, but in the competition between x86 and the Arm (currently v9) architecture, Arm continues to take data centre share.

AMD is committed to promoting x86 (see this post on the x86 Ecosystem Advisory Group) but isn’t wedded to the technology in the same way Intel is. AMD could take a risk and invest in RISC-V as a parallel thread if x86 loses market share to Arm. At this point in time, these markets are all at a balancing point for which the future isn’t easy to predict.

However, in the meantime, we see AMD continuing to grow the business, particularly at the expense of Intel.

Copyright (c) 2007-2025 – Post #5ff4 – Brookend Limited, first published on https://www.architecting.it/blog, do not reproduce without permission.