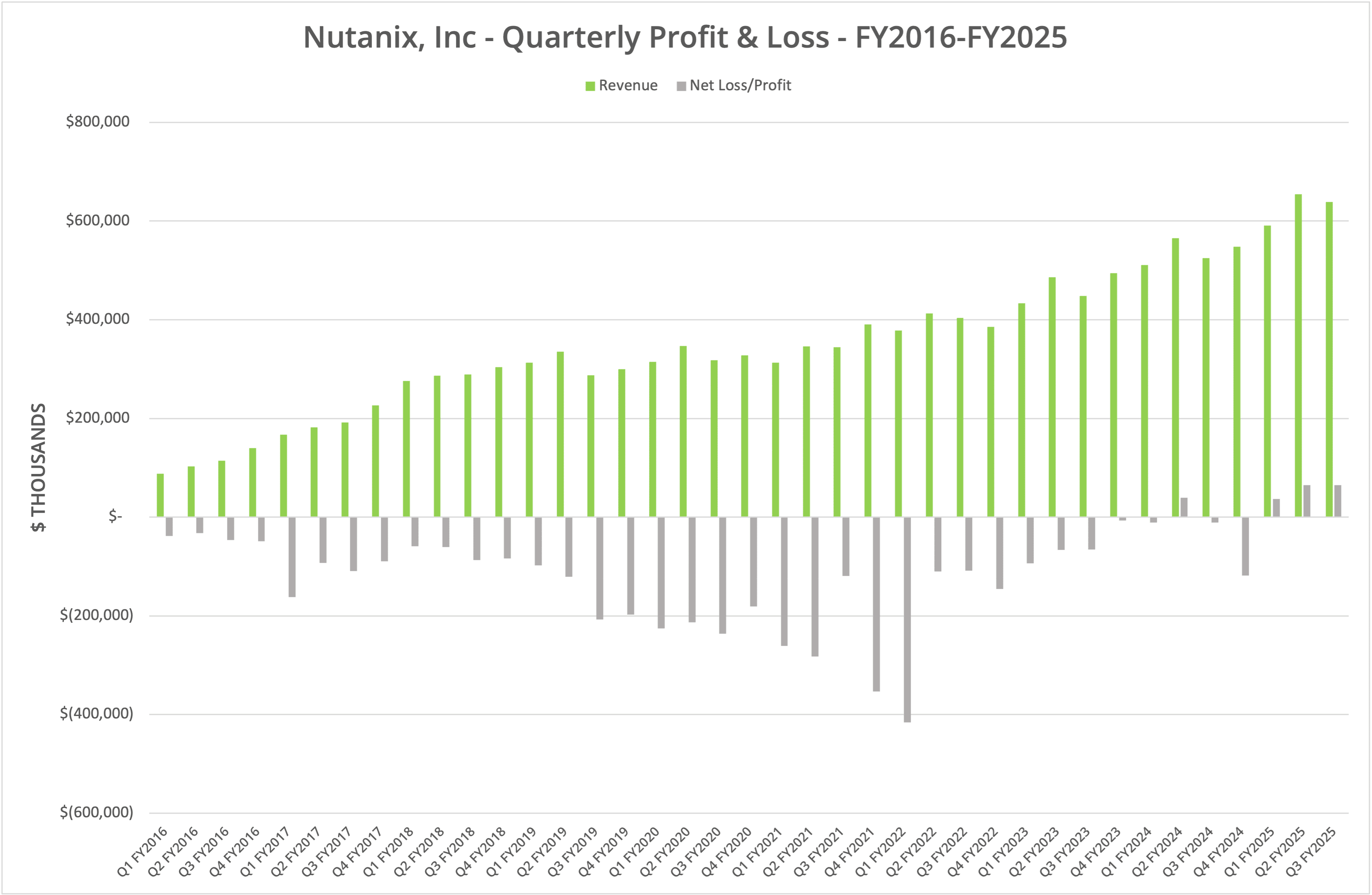

Nutanix, Inc. has announced financial results for the third quarter of FY2025, showing a revenue increase of 21.8% year-on-year to $639 million but down 2.4% sequentially. The company declared a profit of $64.5 million, compared to a loss in Q3 FY2024 of $11 million. With steady growth and improving AHV adoption, the future of the business continues to look strong.

Background

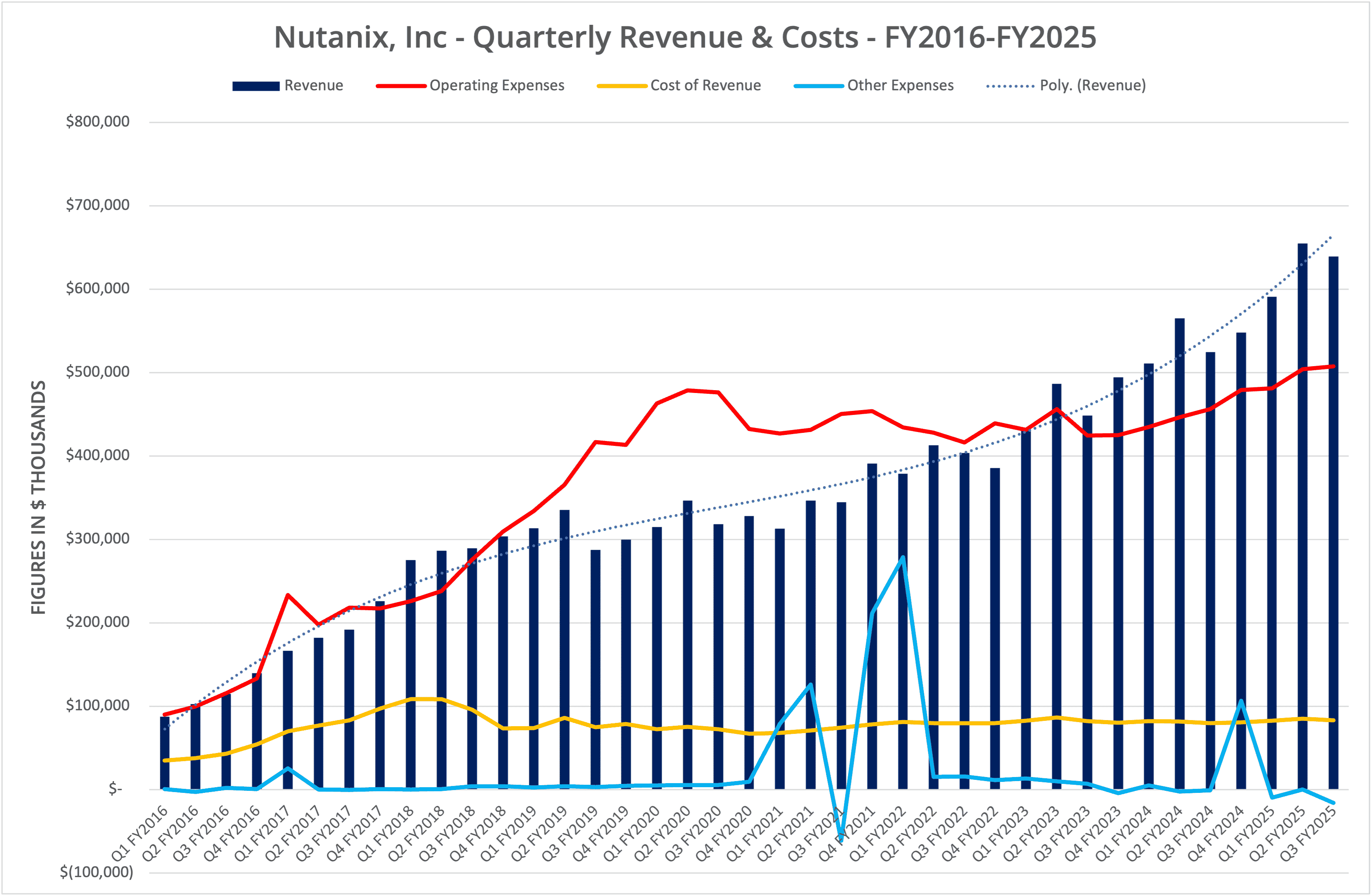

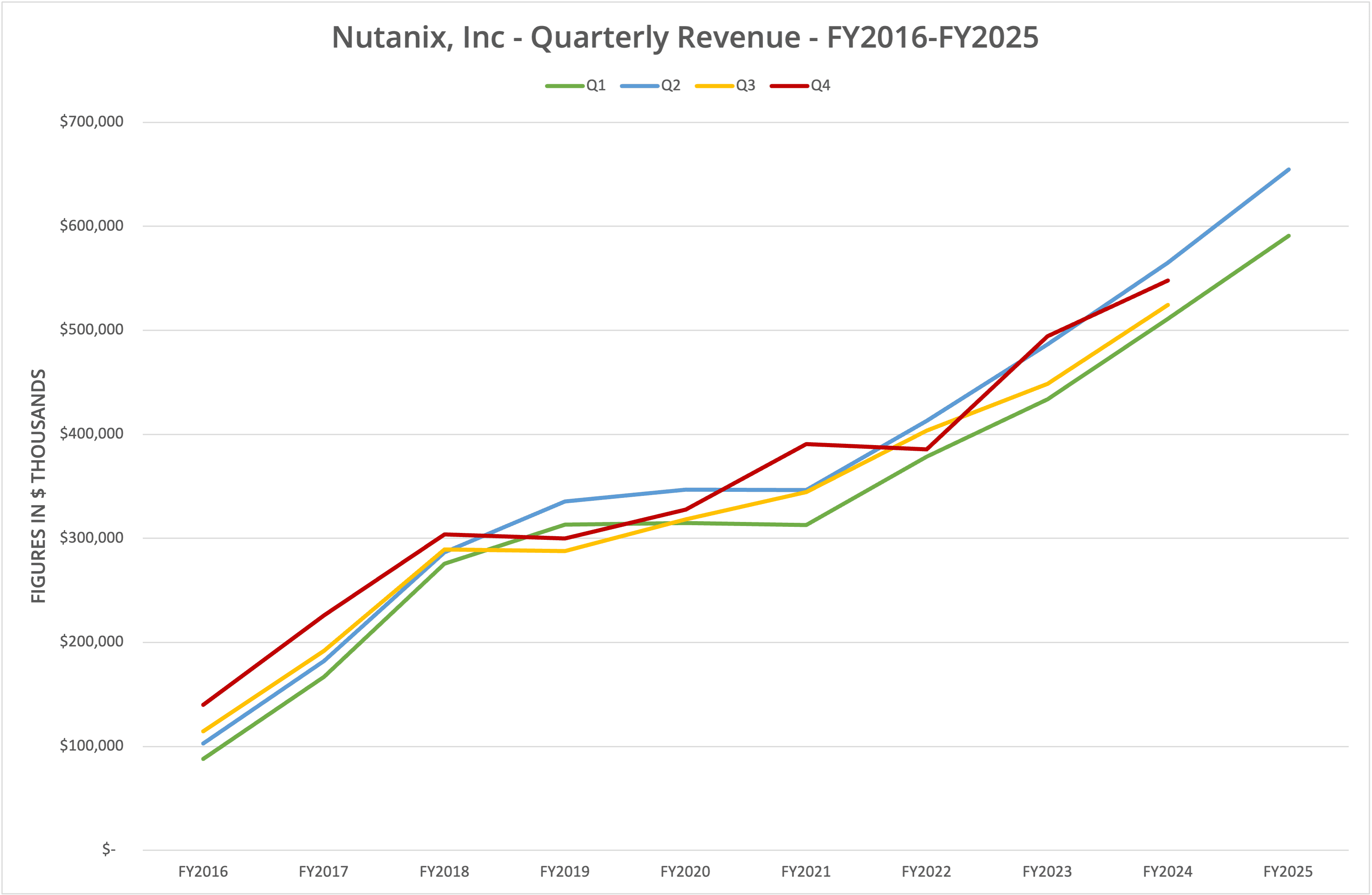

Nutanix, Inc. published financial results for Q3 FY2025 (the period ending 30th April 2025) on 28th May 2025. Revenue for the period was $639 million, up 21.8% year-on-year but down slightly sequentially at 2.4%. Net profit for the period was $64.6 million, compared to a loss of $10.9 million in the equivalent quarter of FY2024. Gross margin remains high at 87%.

We present the data in seven graphs labelled Figures 1 to 7.

Growth (Again)

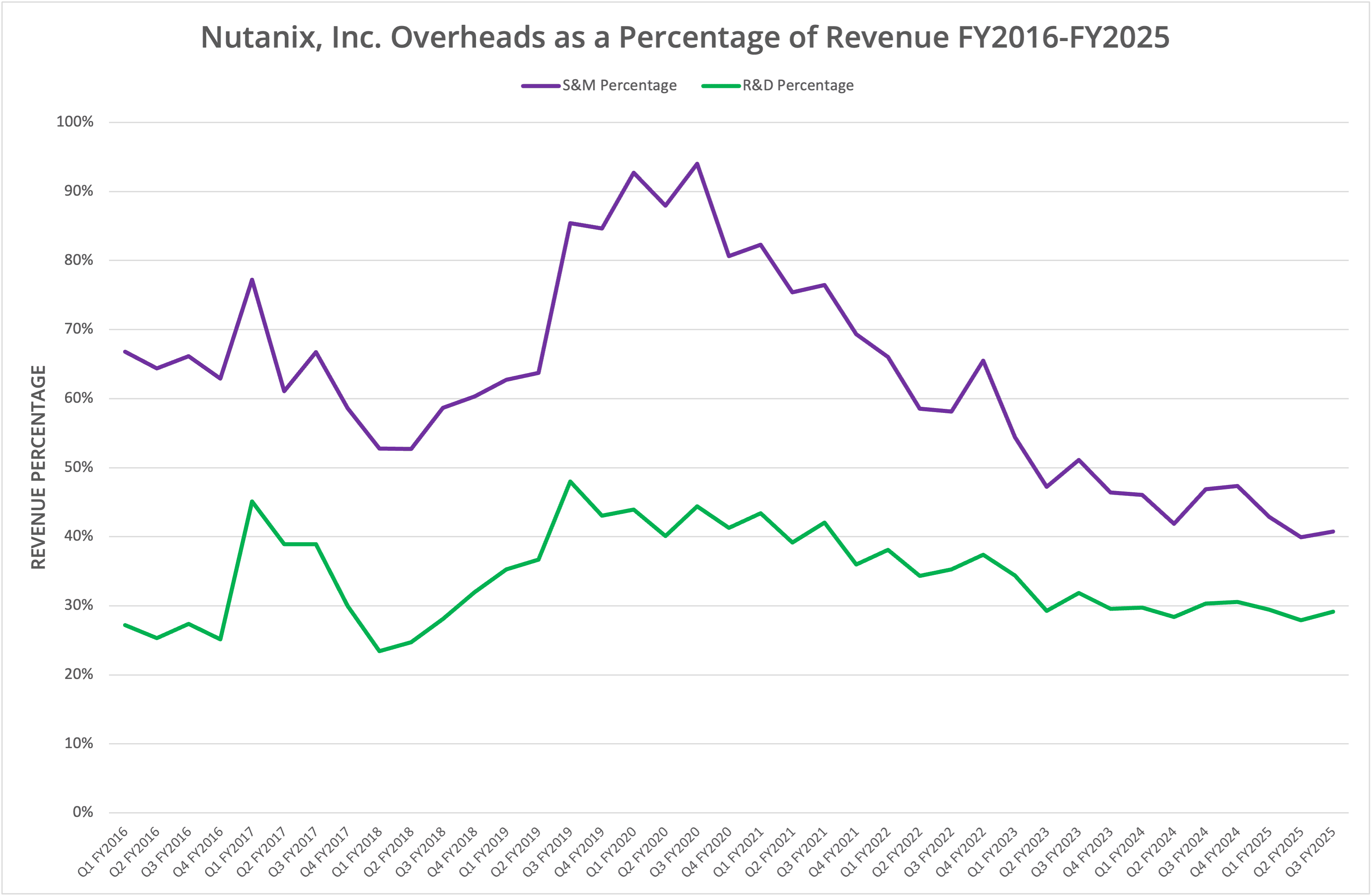

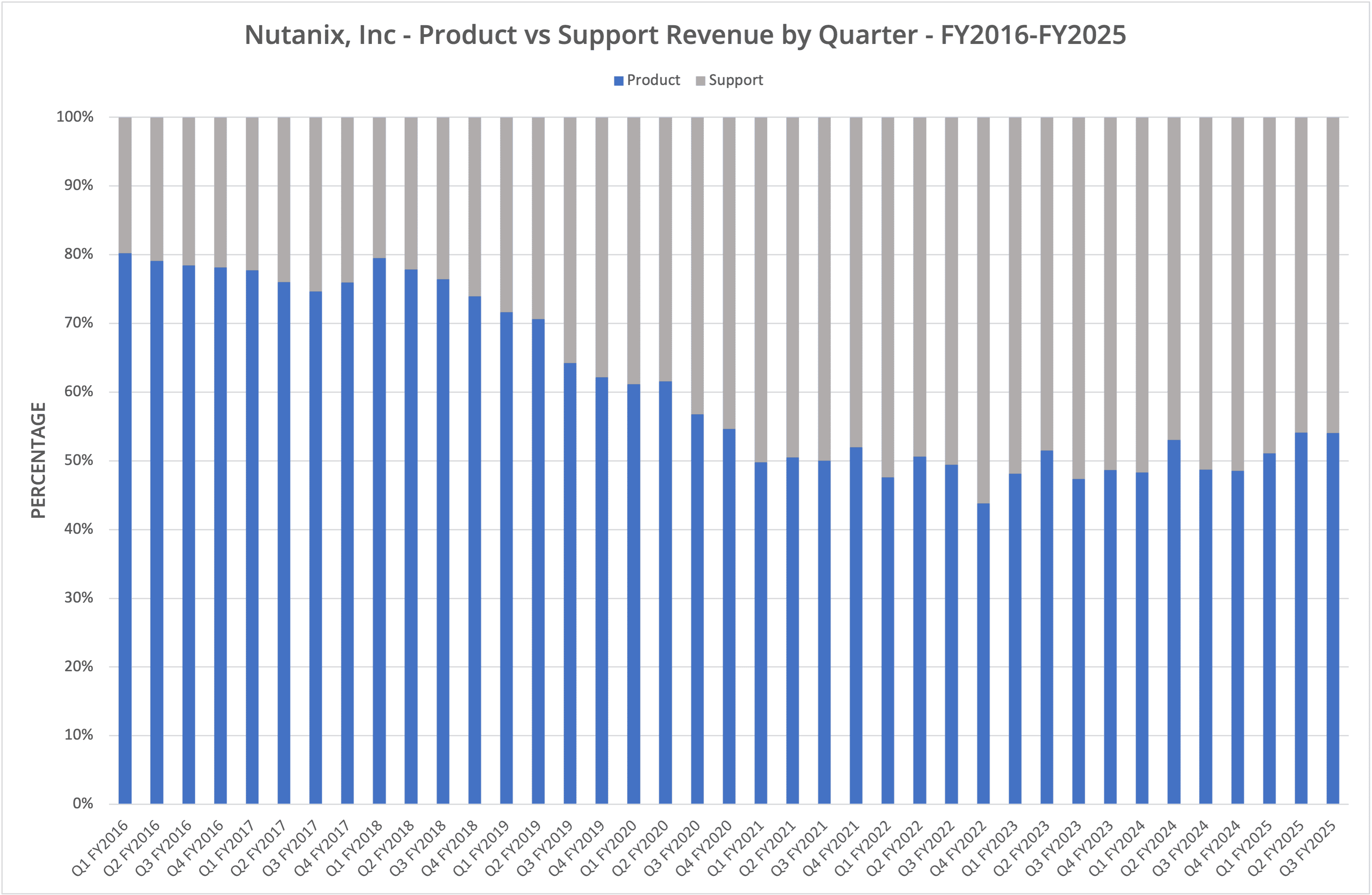

Once again, Nutanix puts in another quarter of consistent growth, both in revenue and customer numbers. Q3 FY2025 represents the third quarter of net profit, which started just over one year ago and looks now to be sustainable. Figure 4 provides a view of overheads as a percentage of revenue, which have continued to decline since the end of FY2020.

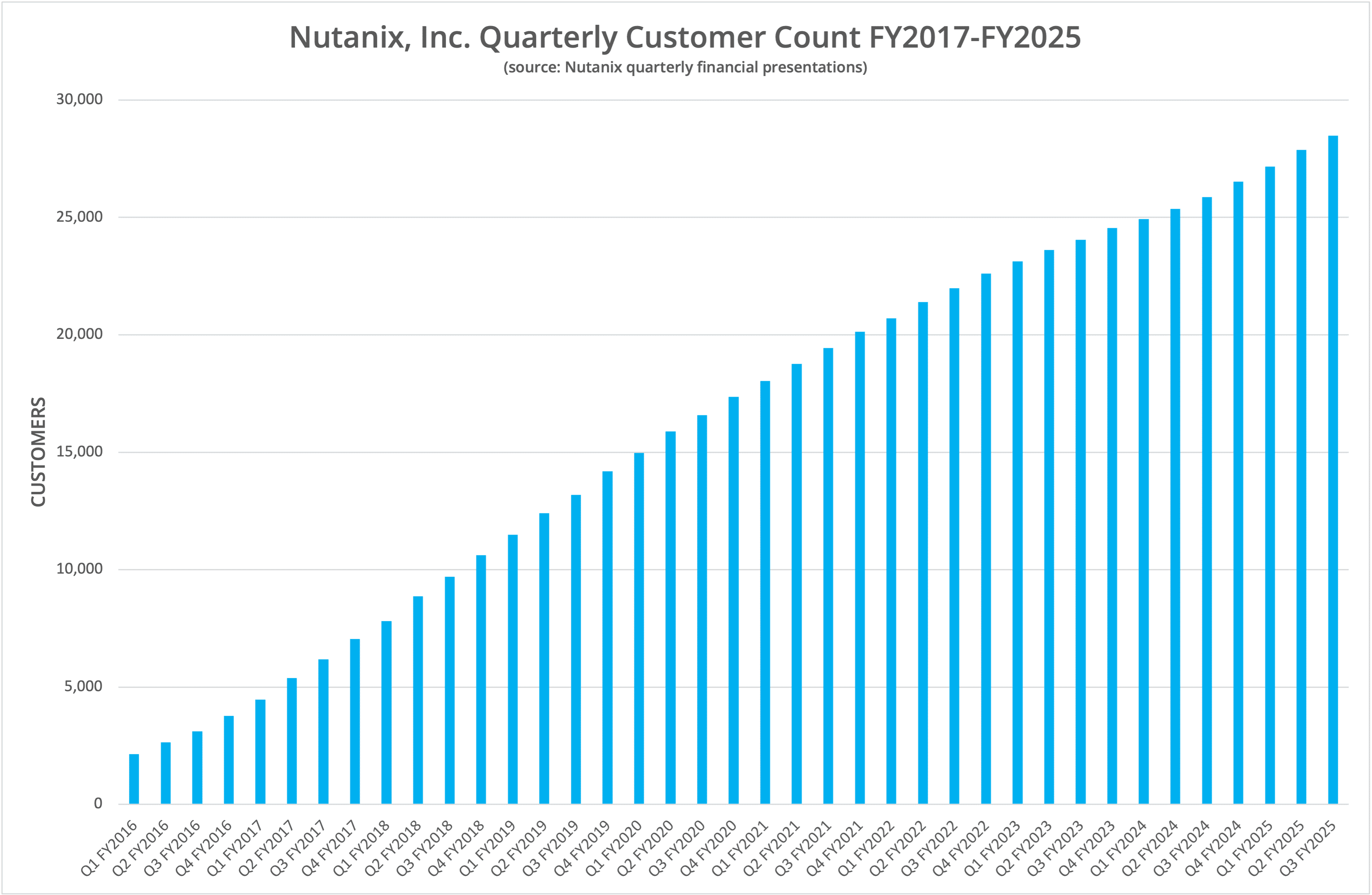

Nutanix is quickly approaching 30,000 customers (see Figure 7 for the data), with a steadily rising trend over the last two years. As we reported for Q2 FY2025, the average customer spends around $71,000 per year (ARR divided by customer count), which has increased again to approximately $75,000 annually.

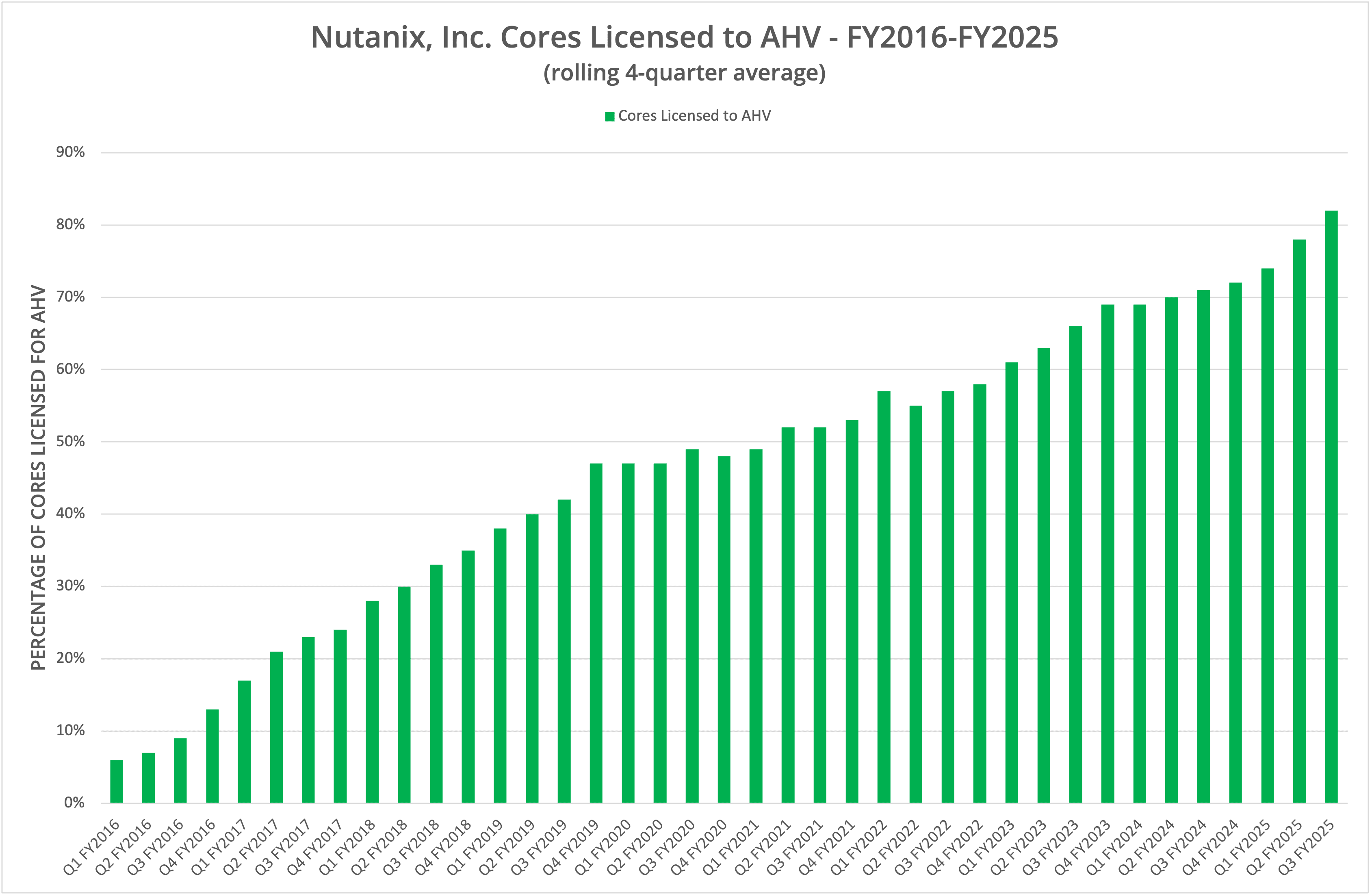

As we covered in a recent Commentary article, AHV adoption has reached 82%, highlighting the almost total migration of customers away from VMware and vSphere. The announcement of VCF9 will likely see that number increase close to 100% as customers are transitioned away from legacy VMware licensing to the new regime under Broadcom.

The Architect’s View®

The Nutanix train rolls on, delivering solid numbers each quarter, which, except for a blip in FY2019/2020, have been remarkably consistent. In recent announcements, the company unveiled a partnership with Pure Storage that will integrate FlashArray with NCI (our coverage here).

With a fully mature ecosystem to challenge VMware, Nutanix looks like it will grow revenue for perhaps the next 18-24 months without too much difficulty. By then, VCF9 and new licensing terms will be well-embedded at Broadcom, providing a better view of the private cloud market and potential competition.

What happens after that? We believe this is the point where Nutanix needs to out-innovate VMware rather than match it feature-for-feature. Both companies have tried VDI and container support, but those areas aren’t where new growth will be found in the enterprise. AI might offer an opportunity for growth, but this doesn’t provide new revenue streams, only additional licences.

Instead, we think Nutanix should focus on ecosystem functionality, taking a lead from the products and solutions offered in the public cloud. Finding a partner and providing support for Arm could be one differentiator. As we highlighted in 2021 (here), improving cloud “density” means offering add-on capabilities similar to Nutanix’s existing database-as-a-service feature.

Making this move will undoubtedly mean more acquisitions, perhaps a small data protection vendor, security platform (for zero trust) or something similar.

With everything in place to take on VMware, the future of Nutanix will be interesting to watch.

Copyright (c) 2007-2025 – Post #5554 – Brookend Limited, first published on https://www.architecting.it/blog, do not reproduce without permission.