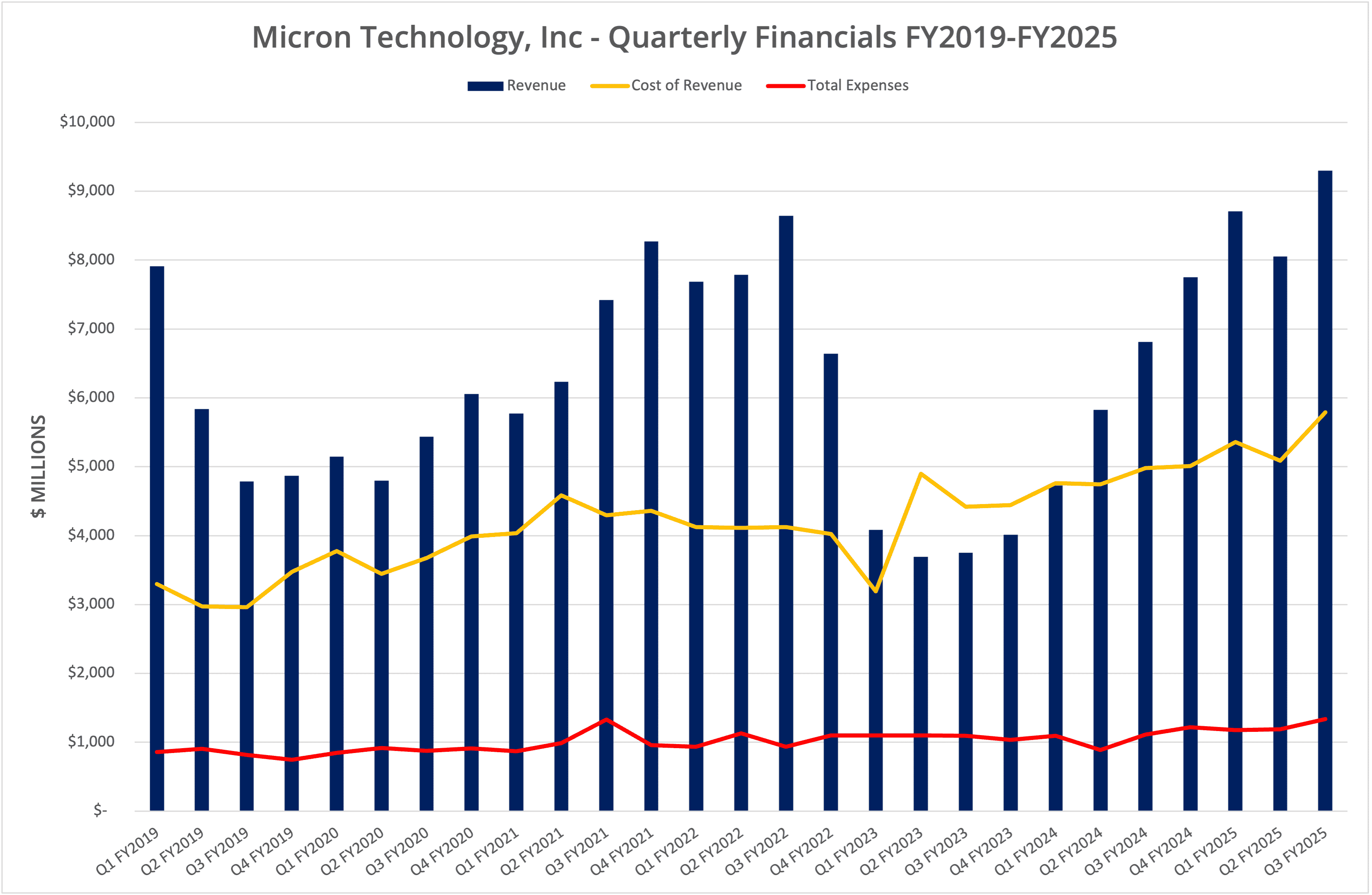

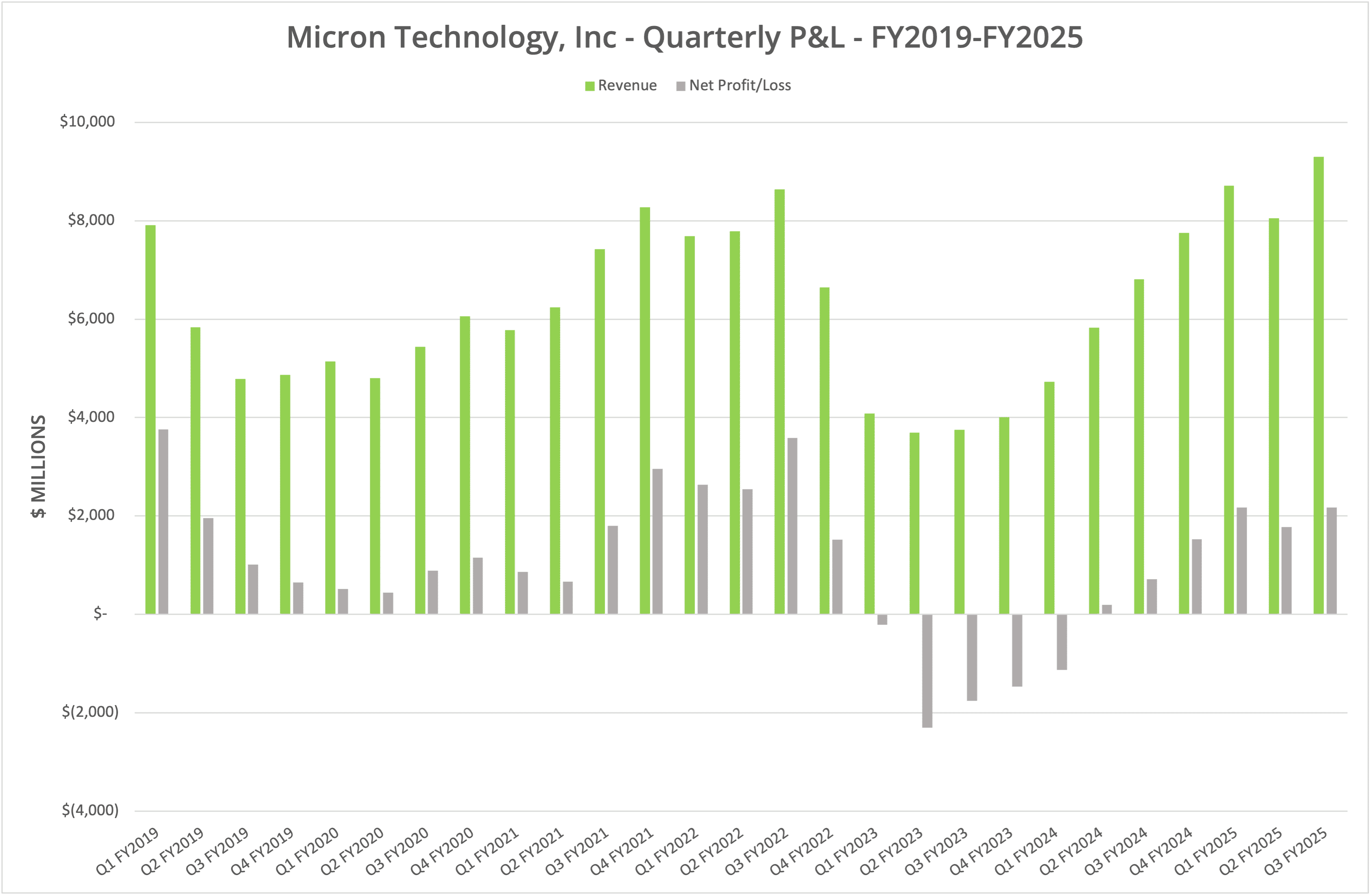

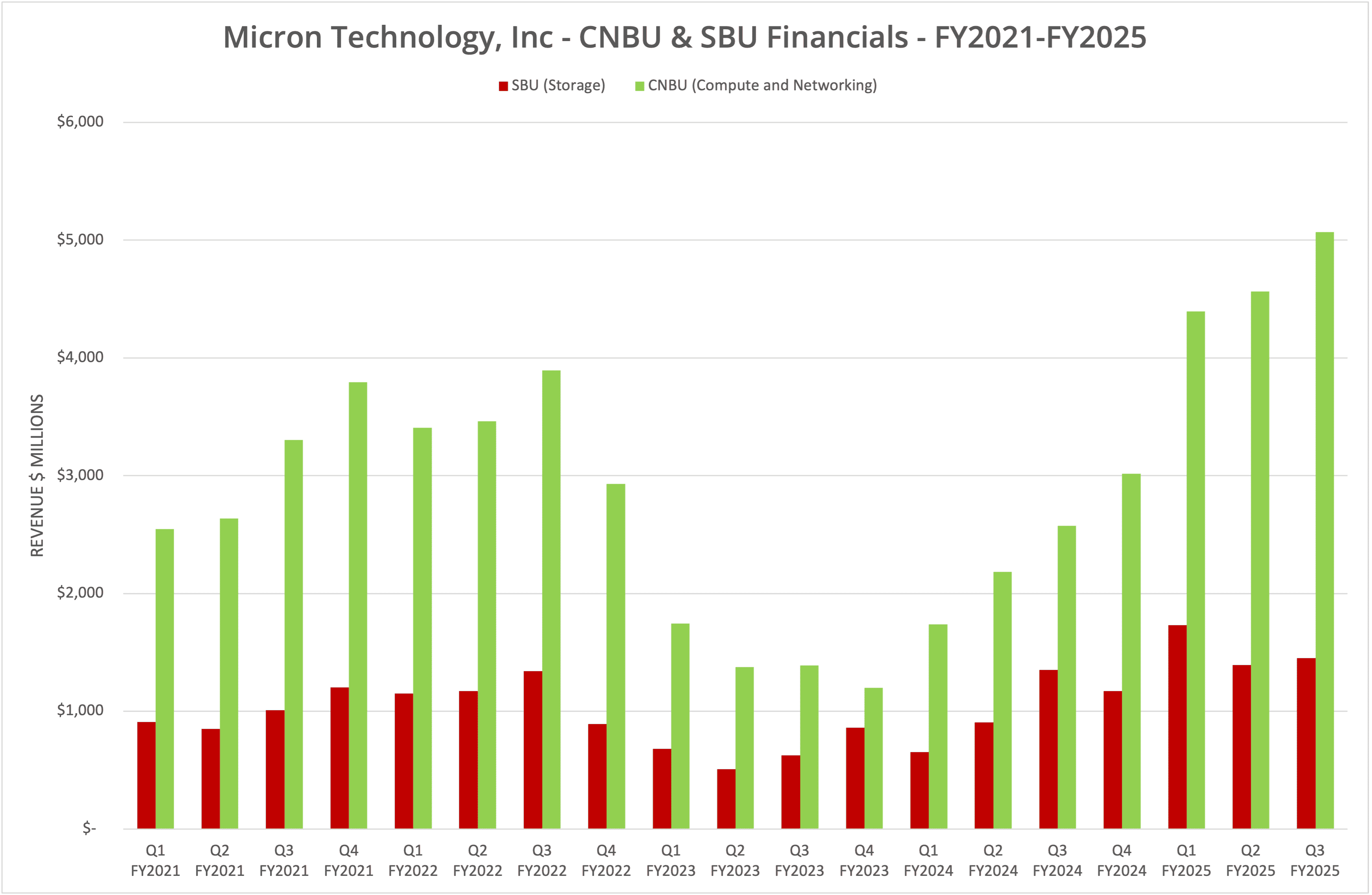

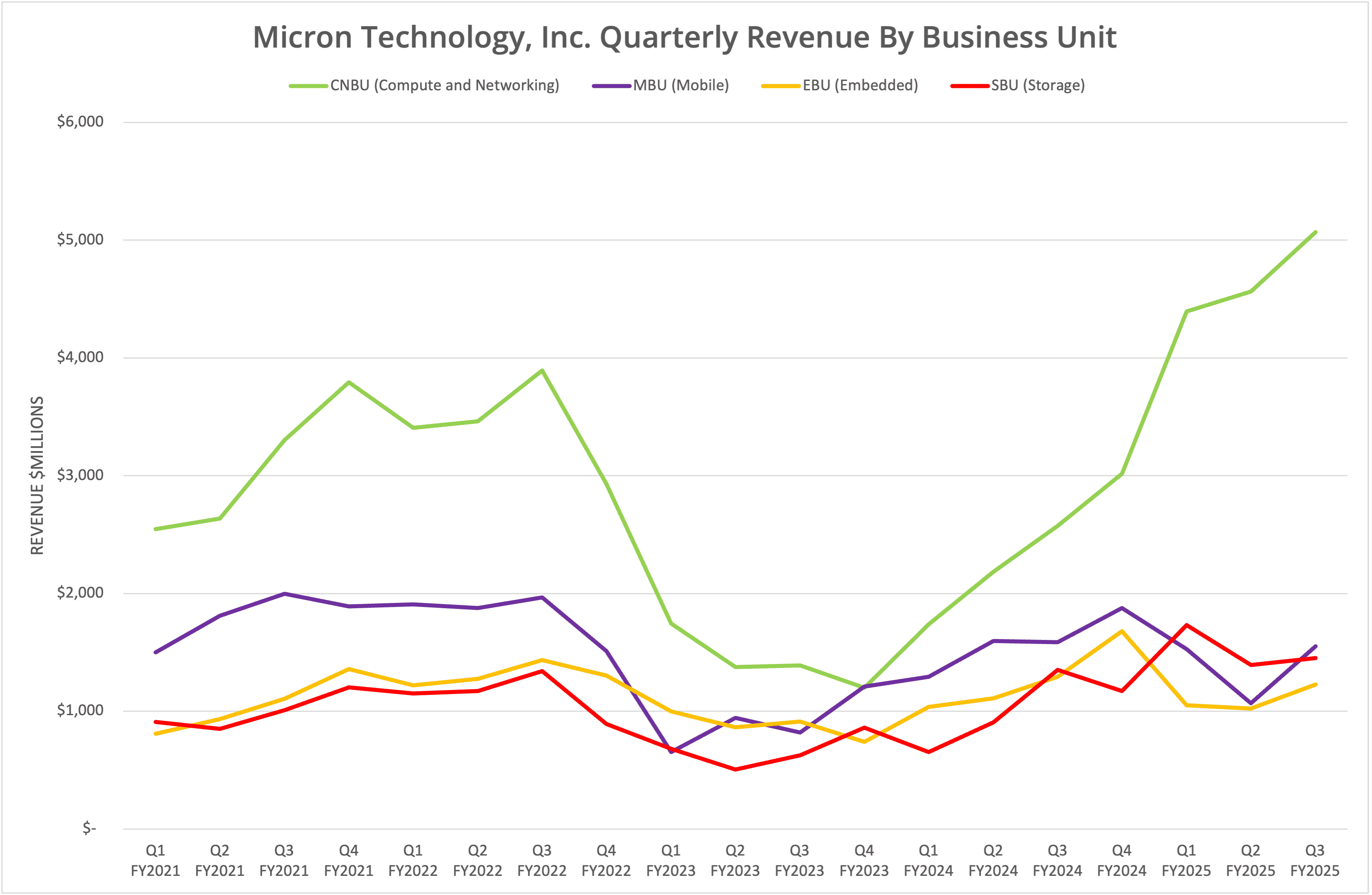

Micron Technology, Inc. has announced financial results for the third quarter of FY2025, ending 29th May 2025. Revenue for the period was up 36.6% compared to Q3 FY2025, at $9.3 billion. Sequentially, revenue increased 15.5%. The most significant gains were seen in the CNBU (Compute and Networking) business unit, driven by demand for high-bandwidth memory. The Storage BU improved sales by 7.2%.

Background

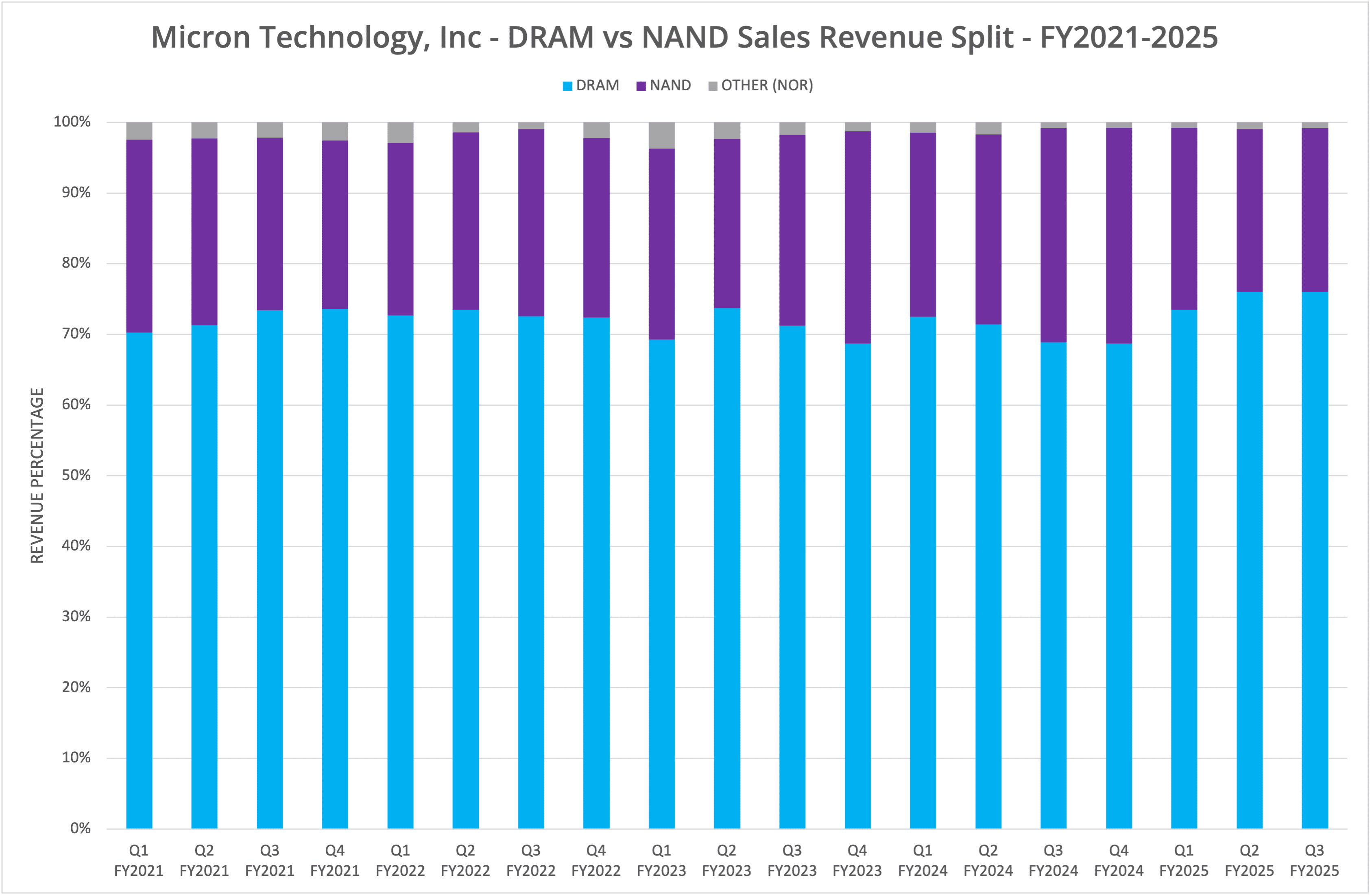

Micron Technology, Inc. declared financial results for Q3 FY2025, the period ending 29th May 2025, on 25th June 2025. Revenue grew by 36.6% compared to Q2 FY2025 and 15.5% sequentially, to $9.3 billion. The Compute and Networking business unit (CNBU) saw the greatest improvement, with another almost doubling of revenue (97%), while the storage business grew 7.2%. DRAM continues to be 76% of revenue generated in the quarter, a figure that has remained steady for many years.

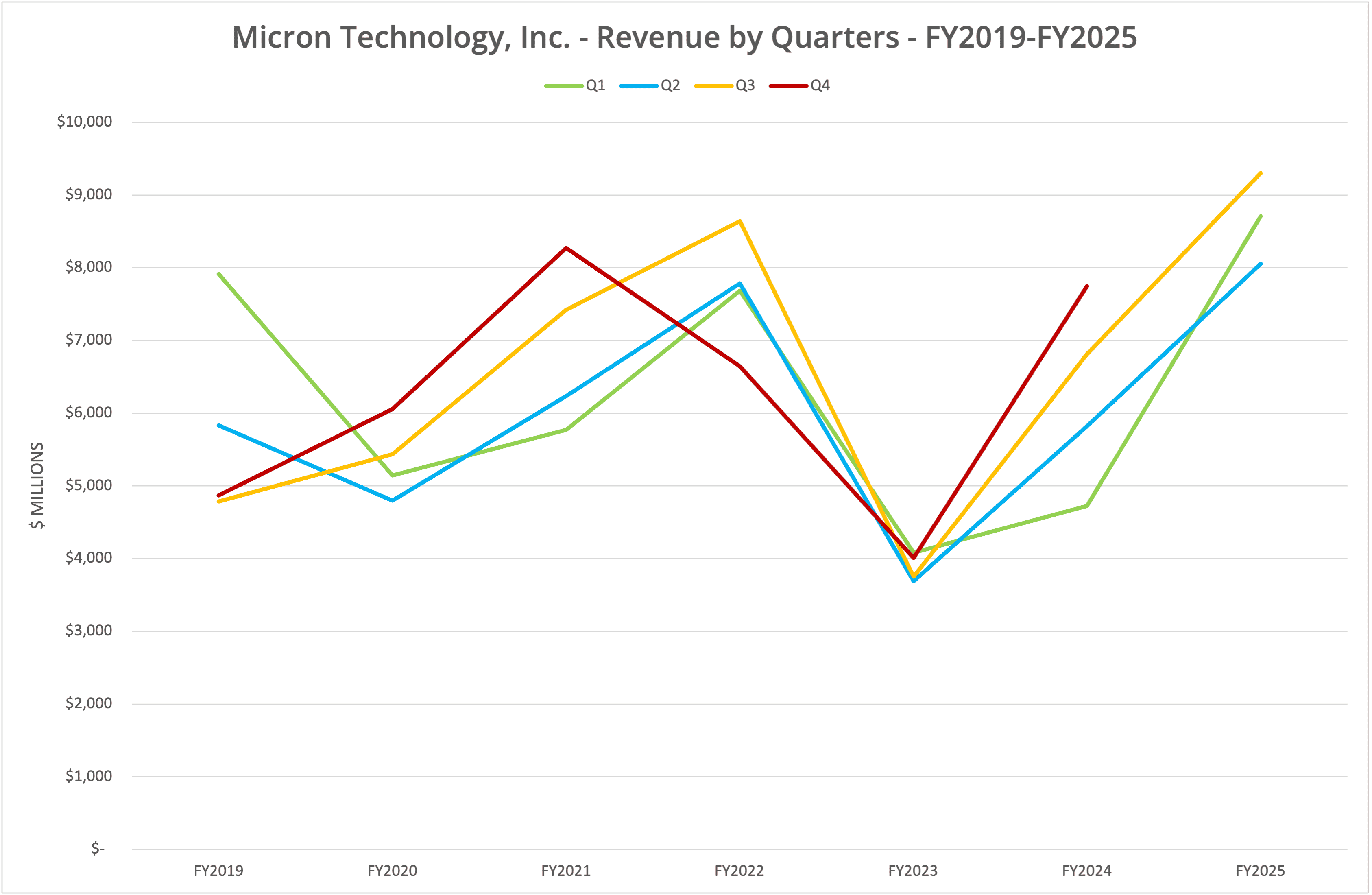

We present the data in six graphs, labelled Figures 1 to 6.

The AI Effect

Micron’s business continues to be driven by the requirement for HBM, primarily on GPUs for AI. In the latest financials presentation, CEO Sanjay Mehrotra indicated that HBM sales grew 50% sequentially and were the driving force behind DRAM revenue. While DRAM growth continues, and the manufacturing process shrinks, we will look in more detail at the NAND business and how that is evolving.

NAND

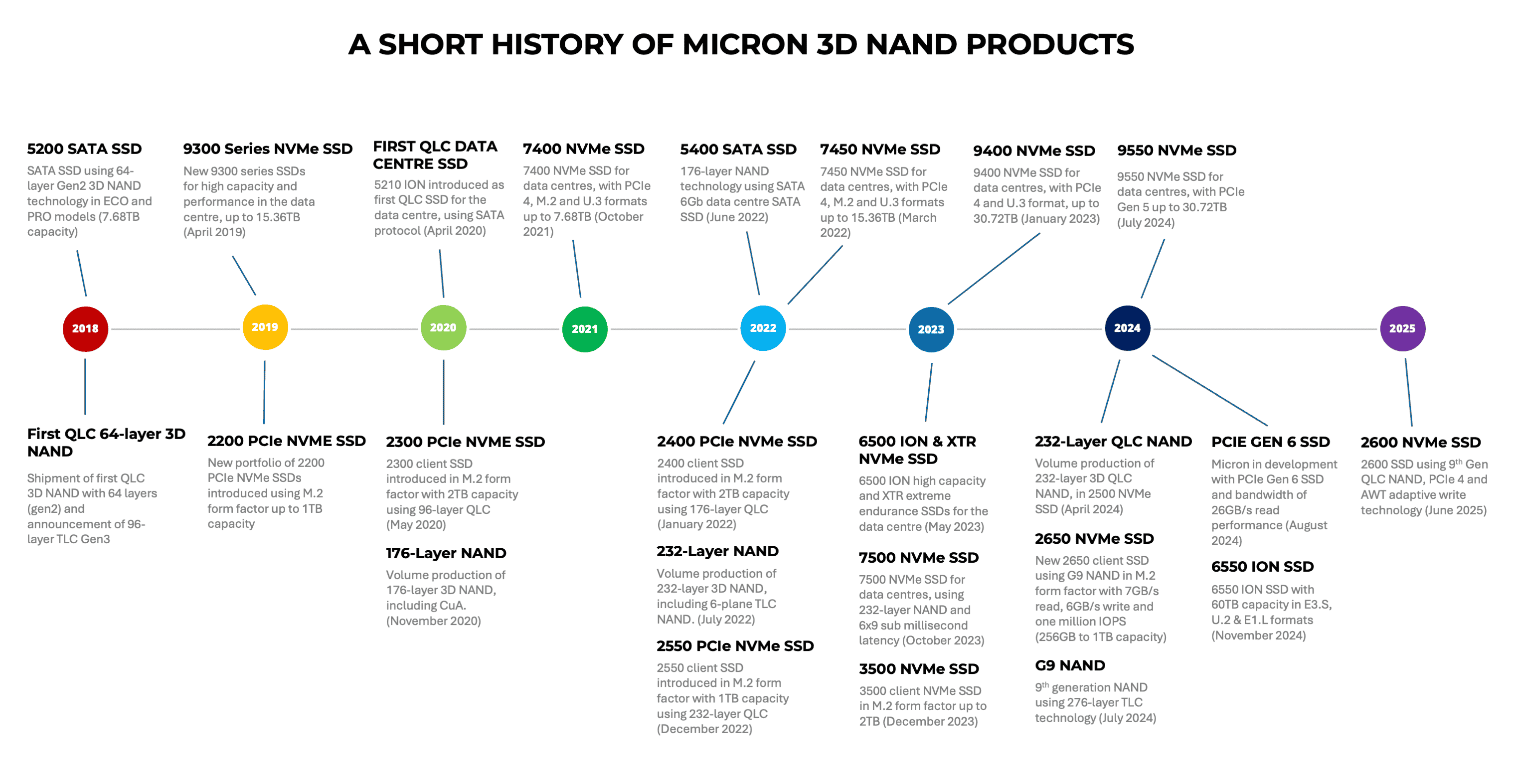

Micron both develops NAND chips and sells packaged components as SSDs. 3D-NAND development has reached the ninth generation, with 276-layer products now in production. Figure 7 shows a brief summary of 3D-NAND developments since 2018.

The product range is divided into client SSDs (2000, 3000 and 4000 series) and data centre SSDs (5000, 6000, 7000 and 9000 series). In addition, XTR NVMe SSDs fill the gap left by Intel and Micron’s 3D-XPoint products, using SLC for extreme endurance.

We can identify clear trends from Micron’s product history that also resonate with other vendors and manufacturers in this market. Firstly, we should remember that Micron both develops NAND technology and packages it into SSDs. NAND products are also sold to storage vendors such as Pure Storage for incorporation into appliances and systems.

Micron is currently at the ninth generation of 3D-NAND, scaling from 32 layers in the Gen1 solutions to today’s 276-layer Gen9. Not all generations deliver a layer improvement, but instead focus on performance and optimisation. However, the evolution of layer counts also coincides with increased product capacity (a maximum of 60TB).

Digging deeper into the product set, Micron offers a range of solutions that provide write-intensive (XTR), standard and read-optimised performance. In some cases, this is achieved within the same product family, such as the 9550 PRO and MAX options (PRO offers larger capacities, MAX delivers higher endurance).

Portfolio

Micron is a leader in the SSD market with the capability to develop new NAND products targeting specific requirements of the flash market. Over the last five years, the company has maintained a steady and increasing cadence of product releases and incremental improvements to the core offerings, which follow the underlying gains in NAND capacity.

The Architect’s View®

This latest set of financial data highlights a business that is cyclical in nature. Revenue is highly dependent upon the demand for memory products, as indicated by Figure 3. In contrast, the storage business unit has only seen modest gains over the last 12 months.

While the improvements in Micron’s SSD technology are steady, the company doesn’t offer the highest capacity SSD, nor the highest layer count for 3D-NAND. In addition, we can see from the latest accounts that operating income from NAND products (mainly SBU) is much lower than DRAM (mainly CNBU).

Micron will restructure and present data across four new reportable segments from the annual 2025 reports. These will be:

- Cloud Memory Business Unit (“CMBU”): Focused on memory solutions for large hyperscale cloud customers, and HBM for all data centre customers.

- Core Data Centre Business Unit (“CDBU”): Focused on memory solutions for OEM data centre customers and storage solutions for all data centre customers.

- Mobile and Client Business Unit (“MCBU”): Focused on memory and storage solutions for mobile and client segments.

- Automotive and Embedded Business Unit (“AEBU”): Focused on memory and storage solutions for the automotive, industrial and consumer segments.

As a result, some of the exposure of the NAND business will be mitigated in the restructuring of operations.

For Micron (and the broader vendor market in general), restructuring products with a focus on business requirements makes complete sense. The features of storage and memory will become increasingly intertwined within application use cases such as AI. Meanwhile, vendors such as Pure Storage will take raw NAND and develop solutions to fit its market requirements.

There is an opportunity for Micron (and others) to develop NAND and products that meet the specific requirements of hyper-scalers, including cloud platforms and businesses such as Meta. We would like to see how Micron will evolve to meet the needs of these organisations as time progresses.

It is possible that building for the industry can provide one solution to the cyclical nature of the NAND (and memory) business. This is an area we will be watching keenly over the next few years.

Copyright (c) 2007-2025 – Post #4b3e – Brookend Limited, first published on https://www.architecting.it/blog, do not reproduce without permission.