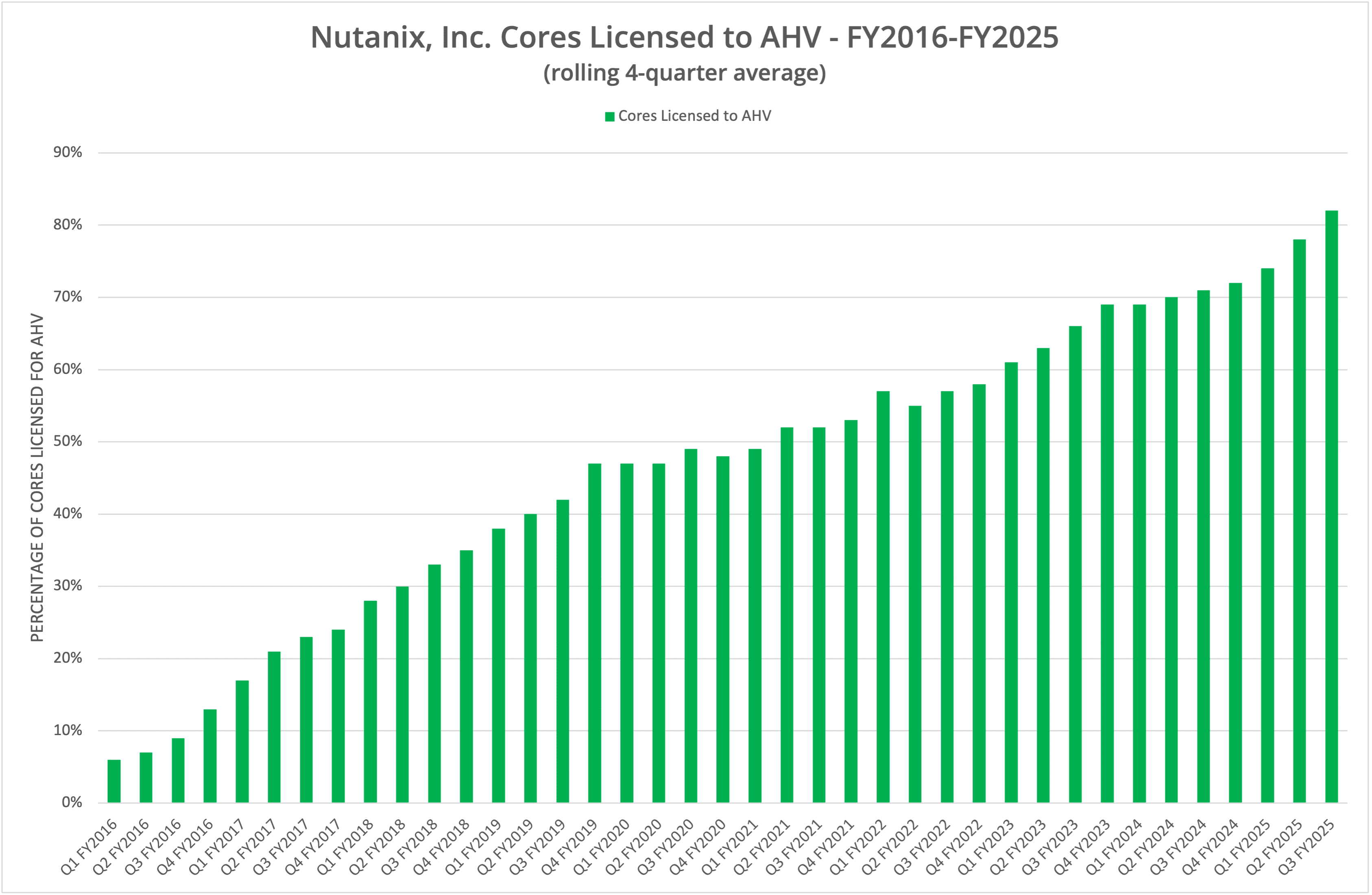

The early days of Nutanix were focused on using VMware vSphere to build an HCI architecture as an alternative to SAN storage. When the Acropolis Hypervisor (AHV) was announced at .Next in 2015, it signalled a pivot towards a platform strategy. AHV adoption by Nutanix customers has grown steadily, and ten years later it is at 82%, demonstrating a real alternative to VMware and vSphere.

Background

Nutanix was founded in 2009 and initially focused on eliminating shared SAN storage, using local media in clustered nodes of server hardware running VMware vSphere. Each node still runs a controller VM with custom software to aggregate local SSDs and HDDs into a resilient distributed storage layer spanning all the servers in a cluster.

Nutanix initially sold appliances, but it was evident that to pivot away from a hardware model (with thin margins and significant support overhead), the company would need to own more of the software stack. The obvious choice was to replace VMware vSphere with a homegrown hypervisor platform, and so AHV, the Acropolis Hypervisor, was born.

Catch-up

It is worth remembering that in 2015, VMware had almost 15 years of experience with ESX(i), first released in 2001. So, for Nutanix, there was a massive hill to climb if the company wanted to successfully transition customers to AHV and entirely eliminate the “vTax” of VMware.

Remember also that VMware introduced vSAN in 2014, stepping on Nutanix’s toes by attempting to replace the core value of the Nutanix platform. vSAN is effectively a virtual RAID storage array running in the hypervisor operating system across a cluster of vSphere nodes, but was poorly implemented in the early versions (there was no bit rot/corruption checking, for example, after write I/O). VMware expended considerable resources to make vSAN a success, probably more than the product justified.

Ecosystem

The greatest challenge for Nutanix in its desire to increase AHV adoption is, of course, the ecosystem that surrounds the core hypervisor. As we pointed out in this post from 2016, ESXi is not the most valuable part of the VMware platform, but rather, it is the suite of software that surrounds it. We map out the concentric layers of virtual server infrastructure in this post from 2023, which starts the discussion on VMware alternatives.

From 2016 onwards, Nutanix expanded its platform ecosystem. The company announced database platform-as-a-service (Era) in 2018, Acropolis File Services (2015), Acropolis Block Services (2016), object storage support in 2019 (Nutanix Buckets) and support for desktop-as-a-service through the acquisition of Frame in 2018. Software-defined Networking (Flow) was announced in 2018 as a direct competitor to VMware NSX.

Most recently, Nutanix announced external storage support in NCI (the evolution of VCP and XCP) for Pure Storage FlashArray. This brings the company full circle, adding external SAN support to a product that started out aiming to eliminate the need for SAN storage in the enterprise.

This final transition is quite an irony, bearing in mind the origins of Nutanix. However, it does reflect the ability of the company to evolve and adapt to what customers need rather than being obsessed with a specific product or function.

Platform

Nutanix has enhanced and extended AHV over the last decade, transforming it into a platform. In parallel, as our graphic labelled Figure 1 shows, AHV adoption has grown from mid-single digits to approximately 82% today. Nutanix uses a calculation based on licenced cores over a four-quarter average. This means the platform is licenced but doesn’t guarantee customers are using AHV over VMware. Of course, why licence a solution if you don’t intend to use it?

Conclusions

The core aspects of this discussion are clear. Nutanix needed to compete with VMware in software if the pivot away from a hardware model was to be successful. Looking at gross margin, which was 60% in Q1 FY2016 and 87% in Q3 FY2025, we can be sure the transition away from selling boxes has been a success (financially).

Nutanix has been successful in building an ecosystem around a core hypervisor, in this case, AHV, which itself is based on KVM. Any vendor can create a solution based on KVM, which is open source and part of the Linux operating system. So, the value of the Nutanix platform is not the virtualisation component per se, but the ecosystem that surrounds it. (Side Note: Broadcom knows this, which is why customers are being guided to buy the full stack of VMware software, not just the base hypervisor component).

We anticipate that Nutanix will push to eliminate the remaining 18% of customers not currently using AHV. With an upwards cadence in customer numbers, Nutanix can be more aggressive in pushing the homegrown hypervisor and ecosystem, even if a few customers drop off along the way.

AHV and the NCI platform provide Nutanix with its own lock-in opportunities, especially with platform services such as the Kubernetes capability and the multiple flavours of integrated storage. In this respect, we can say that Nutanix has taken the fight to VMware and delivered a competitive solution, just at the time Broadcom has increased licensing costs and begun sweating its VMware assets. The opportunity for Nutanix couldn’t be greater than it is today.

The Architect’s View®

What does the success of AHV say for the rest of the server virtualisation industry? The message looks straightforward. The hypervisor is not the most crucial aspect of your platform. Although hypervisor efficiency is essential, there are only four solutions on the market today – proprietary VMware, KVM/QEMU derivatives, Xen, and Microsoft Hyper-V (also proprietary). KVM and Xen are mature open-source features used by many virtualisation solutions, including SoftIron, Scale Computing, Proxmox, Verge.io and oVirt. The difference between hypervisor efficiency is marginal (although operationally, they differ significantly).

For each of the competing server virtualisation solutions, the ecosystem is the differentiator. A decade or more ago, we might have called this a private cloud or a software-defined data centre. The nomenclature doesn’t matter. Instead, we need to focus on the maturity of the features, including everything from software-defined networking and storage to multi-tenancy and automation.

There has never been a better time for server virtualisation vendors to target VMware. In addition, data sovereignty is questioning the use of US public cloud platforms, particularly in EMEA. The balance of private vs public could change, and server virtualisation platforms need to be ready.

Who would have thought that private cloud could see a renaissance at a time when the public cloud looks to dominate?

Related Content

- Nutanix Goes After Private Cloud with XCP (June 2015)

- VSAN 6.2 – Is it RAID or Erasure Coding (February 2016)

- Alternatives to VMware: Introduction (November 2023)

- Research Note: Nutanix expands support for external storage on NCI with Pure Storage FlashArray (May 2025)

X-Ray: Nutanix, Inc (Second Edition).

This Architecting IT report takes a deep dive into Nutanix’s history, products, services, and future outlook. This report is only available for download via paid subscription.

Copyright (c) 2007-2025 – Post #ccce – Brookend Limited, first published on https://www.architecting.it/blog, do not reproduce without permission.