HPE, Inc. has announced Q3 FY2024 financial results that show a year-on-year revenue increase of 10.1% but a second quarter of significant variance by business unit. The Server segment reported growth of 35%, while Intelligent Edge was down 23% and Hybrid Cloud revenue down 7%. HPE seems to be highly focused on selling servers, but other parts of the business show little good news.

Background

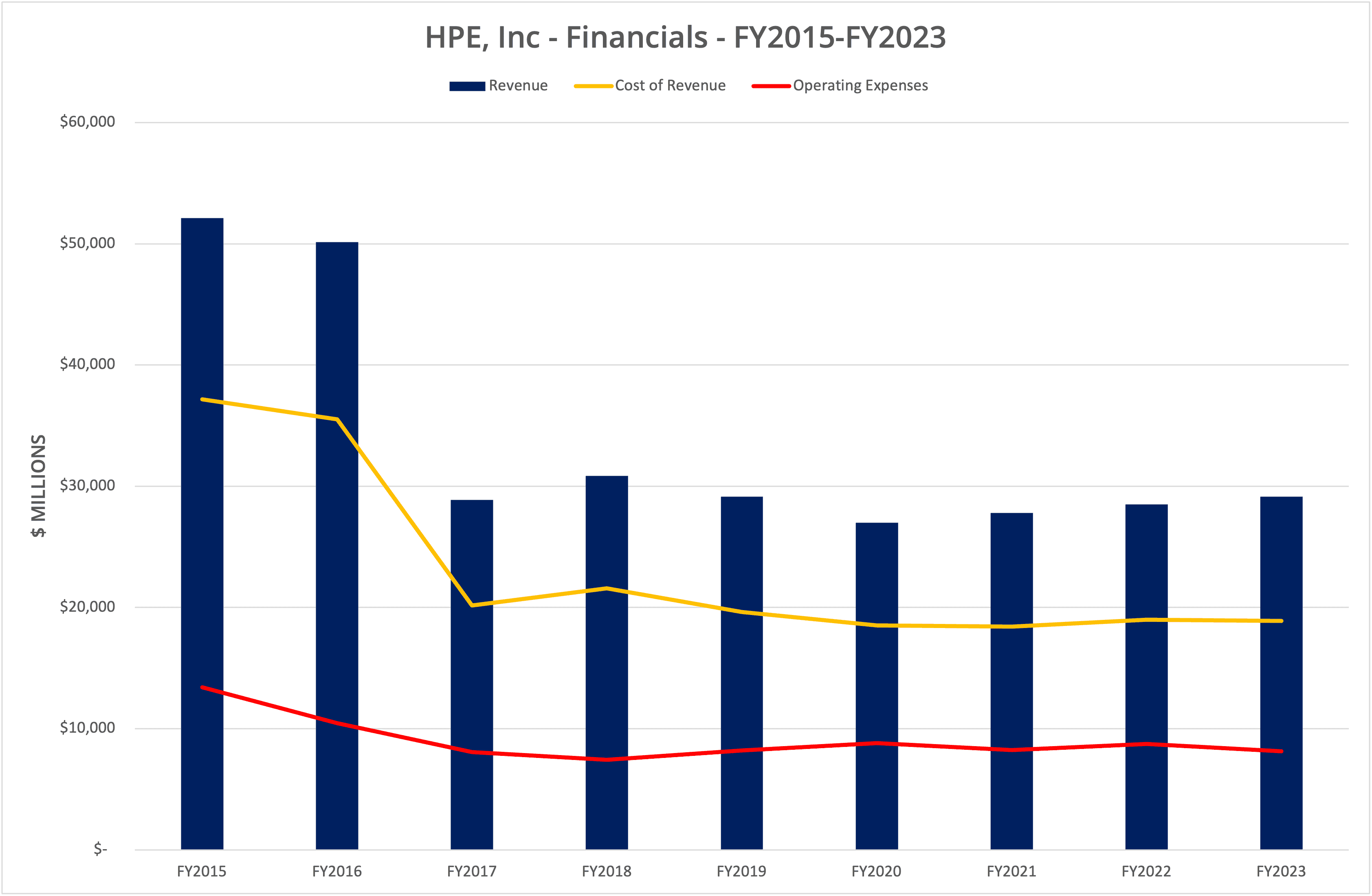

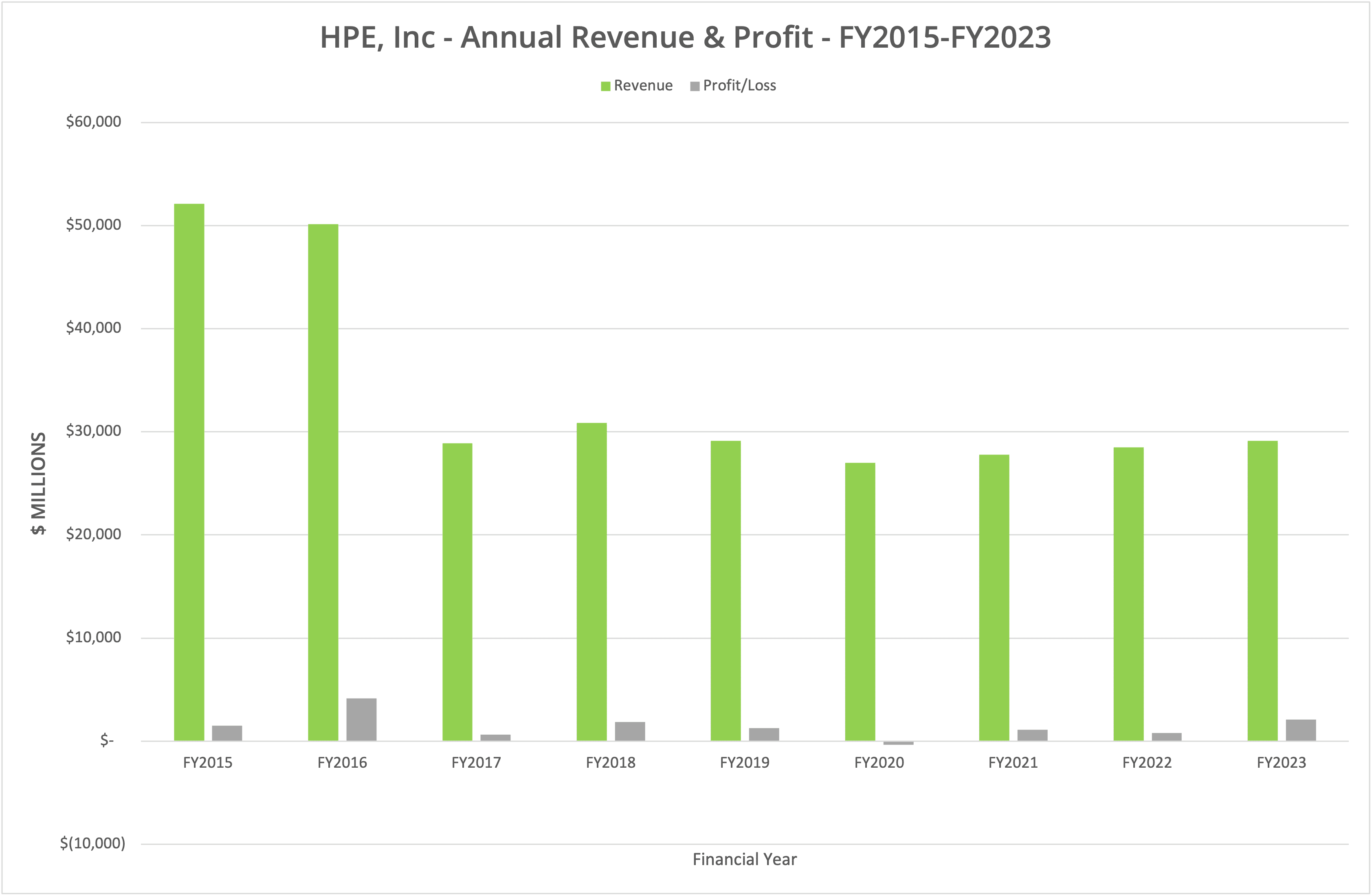

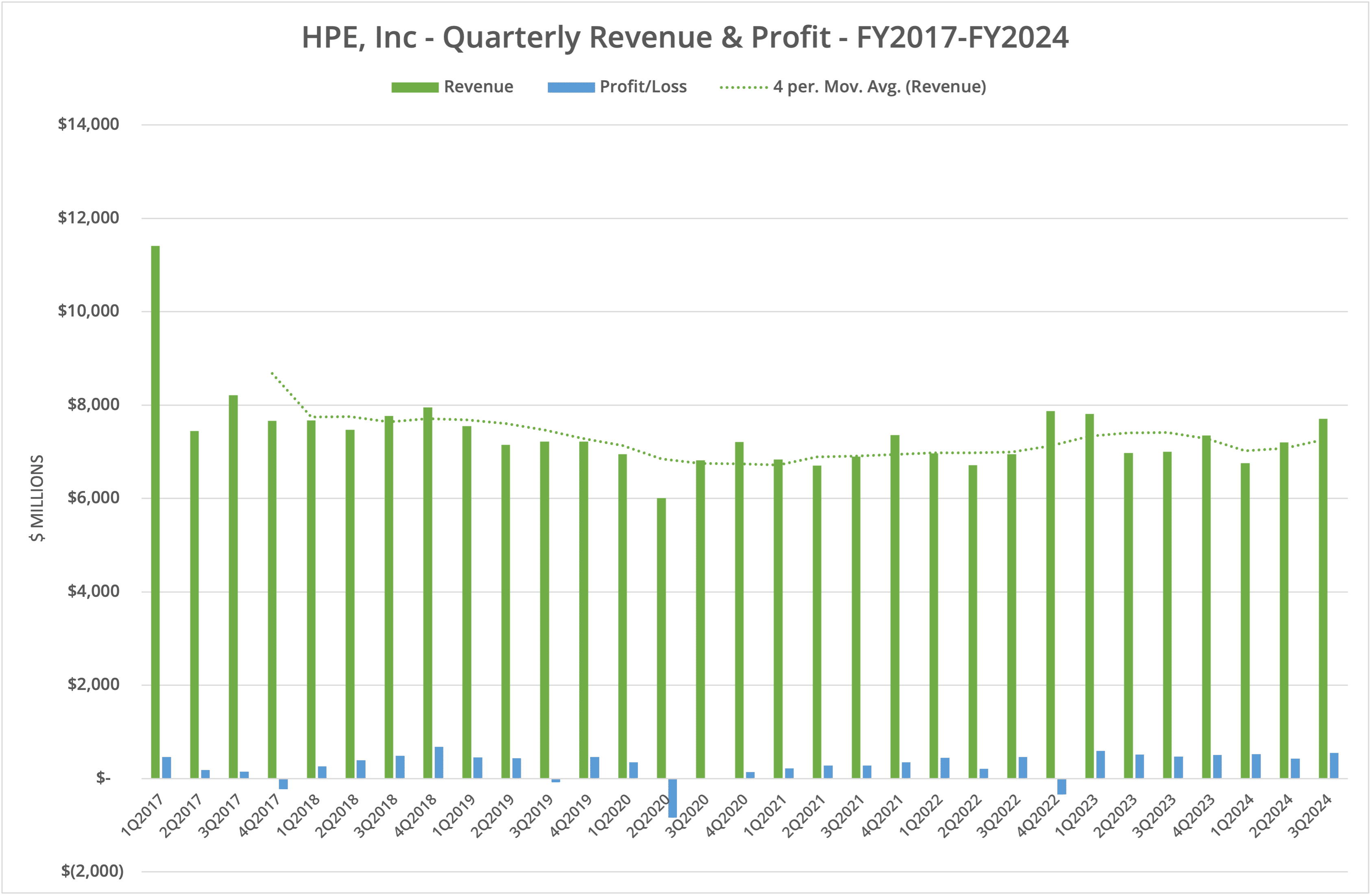

HPE, Inc. reported financial data for Q3 FY2024 on 4th September 2024. For the 3-month period ended 31st July 2024, overall revenue was $7.7 billion (up 10.1% year-on-year), with a gross margin of 31.6% (35.8% in Q3 FY2023) and profit of $547 million.

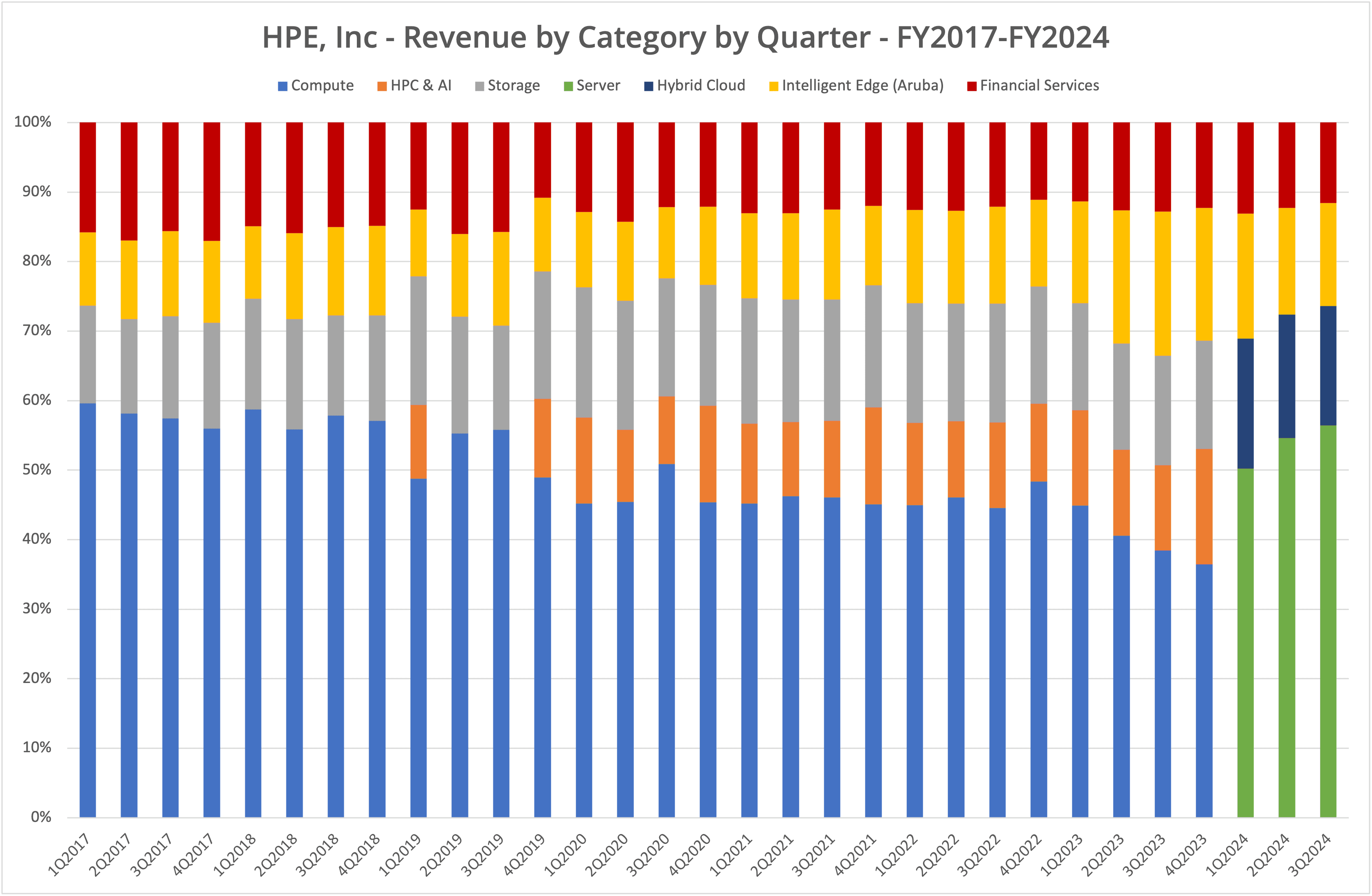

The Server business unit achieved $4.3 billion in revenue, up 35% year-on-year and representing 56% of the quarterly total. Intelligent Edge (networking) brought in $1.1 billion, down 20.8% (HPE figures show 23%, as we think some numbers are restated), representing 15% of the total. The Hybrid Cloud business delivered $1.3 billion in revenue, down 7% year-on-year, representing 17% of the total. The remaining revenue came from Financial Services, which was relatively flat at $879 million (11%).

We represent the data in seven graphs labelled Figures 1 to 7.

Servers

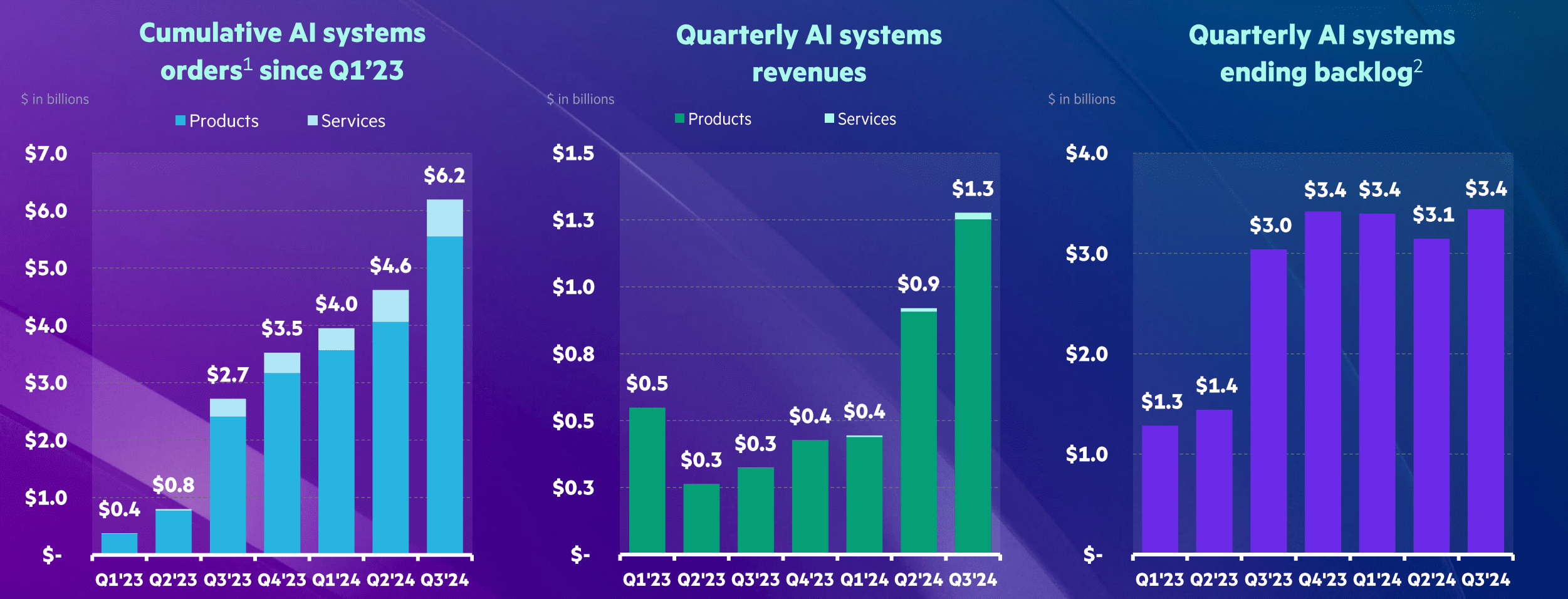

Undoubtedly, the big news is (once again) revenue from server sales, specifically those focused on AI. Within the Server segment, AI systems sales rose 39% compared to the previous quarter, to $1.3 billion. HPE reported that demand for AI systems rose $1.6 billion compared to the previous quarter and has totalled $6.2 billion since Q1 FY2023.

HPE is keen to show the growth in demand for AI systems (as shown in Figure 8), which also indicates the backlog in orders that currently looks relatively stable.

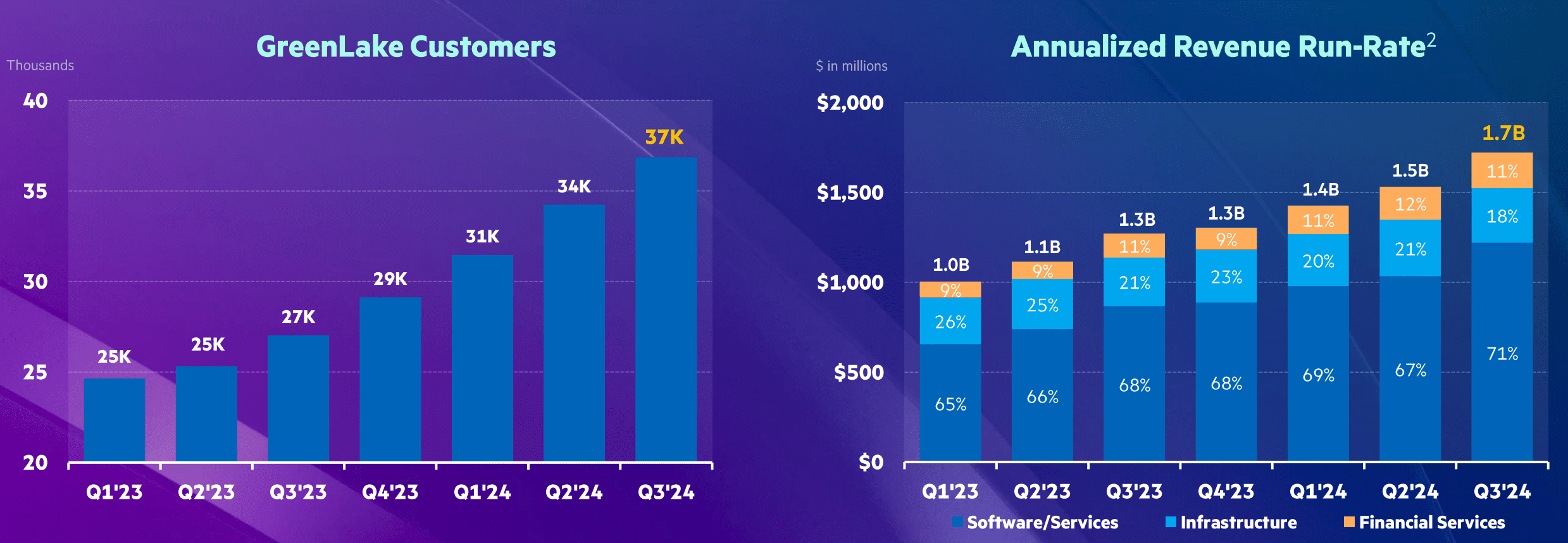

GreenLake

What about the rest of the business? Figure 9 shows GreenLake growth, which is healthy in terms of customer numbers, but at $1.7 billion of ARR, only represents 5.8% of HPE’s revenue for FY2023. Despite the hype and some six years in, GreenLake is still only a small part of the HPE business, which clearly continues to rely on traditional acquisition channels.

Decline

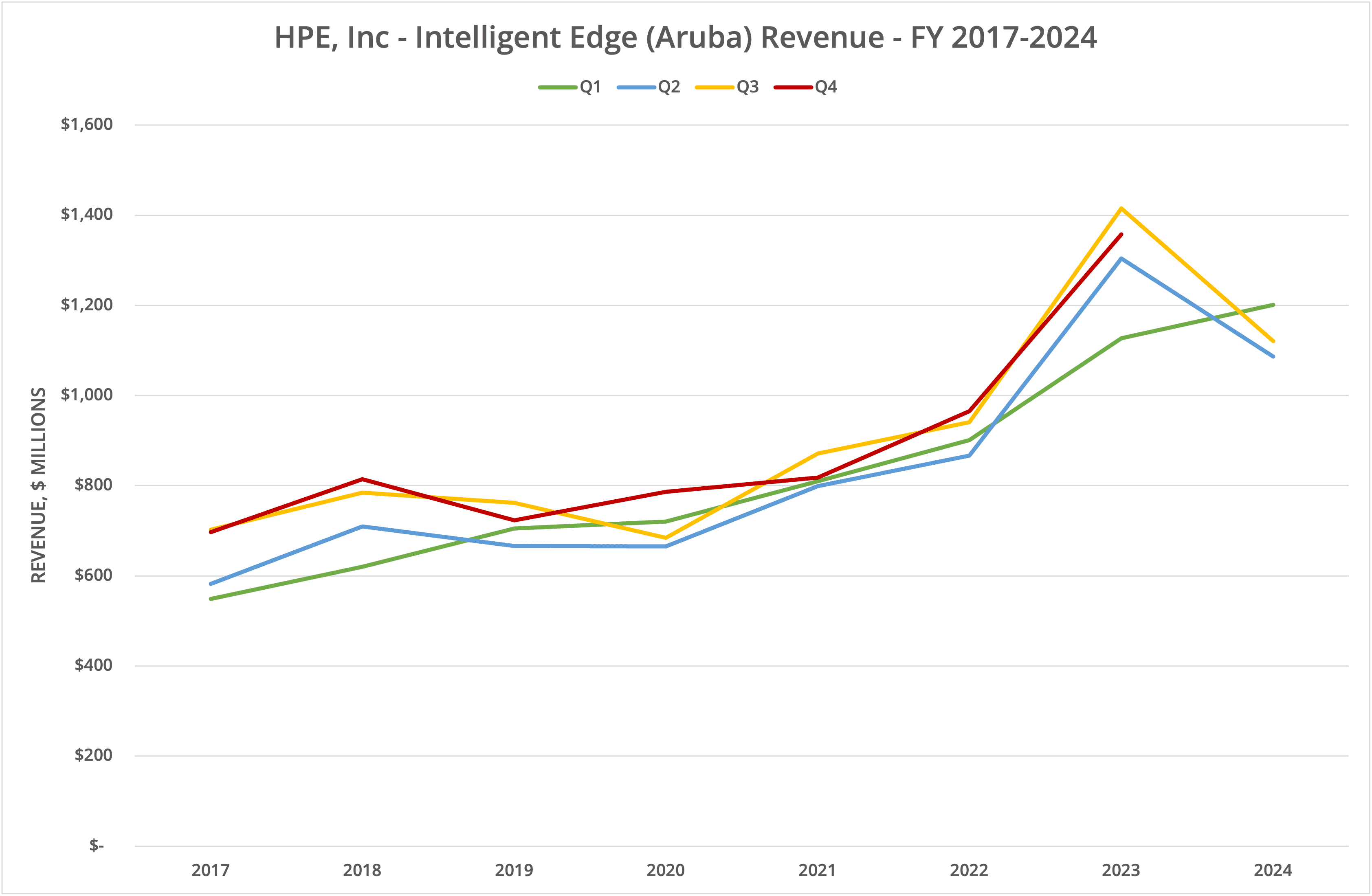

Elsewhere, the previous growth in Intelligent Edge (Aruba networking) has stalled and headed into decline. The post-earnings release call and transcript provide no real explanation other than a series of financial jargon. The expectation is that the addition of the Juniper business will bolster revenue for this segment.

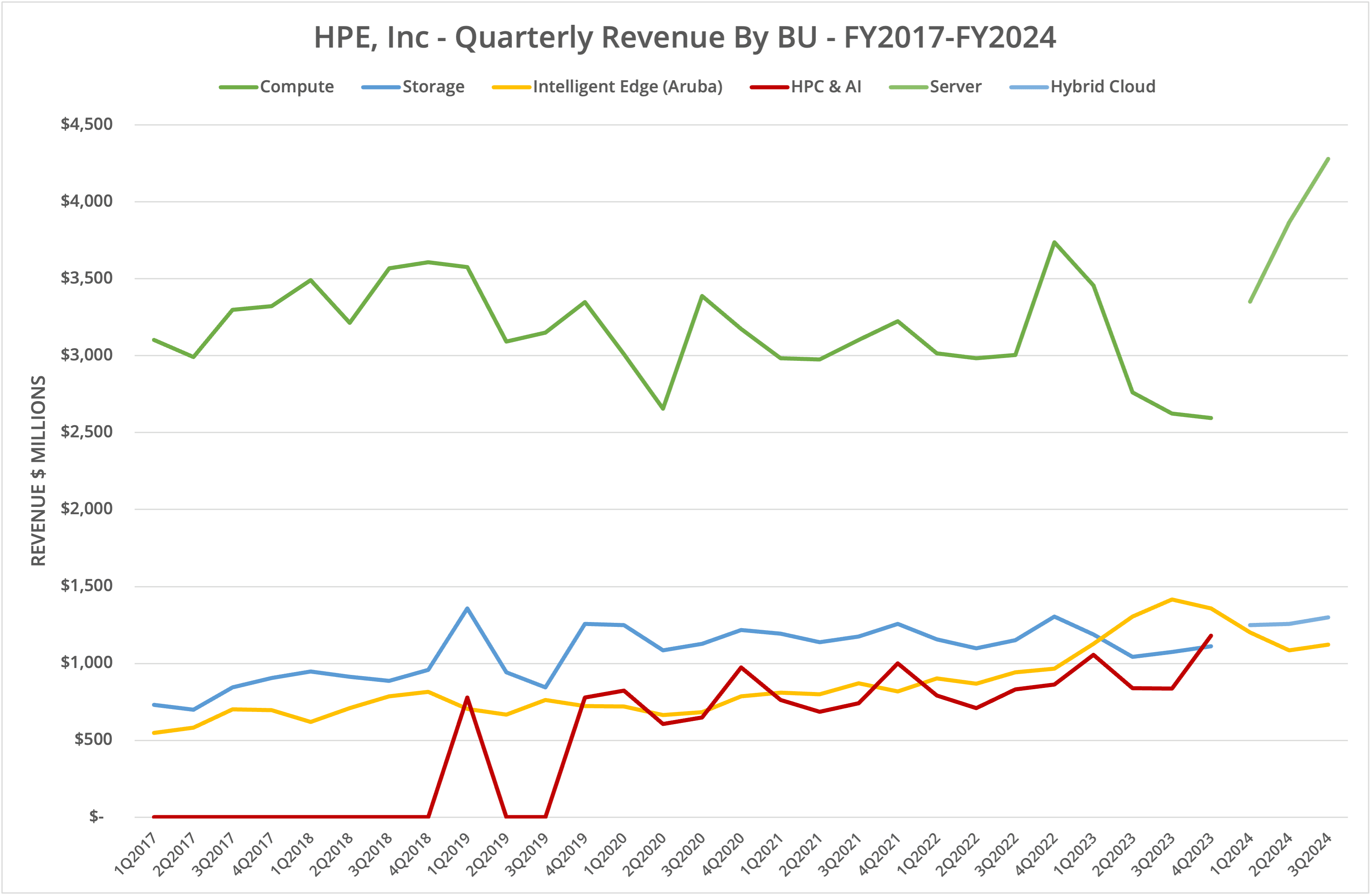

Also, somewhat strangely, HPE reported another decline year-on-year in the Hybrid Cloud business, which now contains and obfuscates the previously reported Storage business. Justification for the decline is blamed on a transition to a cloud-native and software-defined platform, the Alletra MP. While this is partially true (Alletra MP now offers a public cloud offering), in reality, the heritage 3PAR and Nimble platforms have been realigned on standardised hardware. File services are now partially delivered by the partnership with Vast Data, which is also running on the Alletra MP platform.

AI Drag

In a parallel to the recent financial announcement from Dell, the significant uptake in AI server hardware sales doesn’t appear to have improved other areas, such as storage. One apparent excuse offered by HPE is the transition to “new protocols” required by AI systems. This seems odd, as HPE has offered file and object solutions for many years, including partnerships with vendors such as Scality. So meeting customer requirements shouldn’t be a problem.

We also can’t equate the lack of revenue growth with the apparent increase in Alletra Storage and HPE GreenLake Hybrid Cloud SaaS demand, which is quoted as “double-digits” (meaning at least 10%). Either the new growth is replacing legacy storage solutions (with no net increase), or new sales are at a much lower per-transaction value.

The Architect’s View®

Looking back at our analysis from Q4 FY2023, we highlighted a business being propped up by HPC/AI and Intelligent Edge sales. HPC/AI is now the Server segment, while Hybrid Cloud encompasses Storage and Compute (the non-AI part). Almost a year later, the networking business has faltered, while AI server sales are keeping the business in the black in terms of revenue growth.

Despite all the claims of growth, we see no measurable improvement in the Storage business (our main focus in tracking HPE), which we believe is due to the engineering of storage solutions onto the HPE Alletra MP hardware platform. In June 2024, we released a Research Note that detailed the evolution of the block storage solutions for Alletra MP. Unfortunately, HPE’s poor marketing means this information isn’t easy to locate online, which may be confusing for customers looking to understand HPE storage offerings.

It is also challenging to rationalise what revenue has been derived from the Vast Data partnership; Vast’s Data Platform is used with Alletra MP to deliver file storage services. Contrast the reported Hybrid Cloud revenue with the recent financials of Pure Storage and NetApp, and it’s clear to see who the winners and losers are in the storage market.

HPE is profiting from the current wave in AI as businesses look for ways to acquire new customers or add value for those they already have. We have no idea how long the AI gold rush will last, by which time the market will be flooded with hardware. Looking purely at the Storage business within HPE, the evolution of solutions continues to be relatively opaque and based on legacy solutions from 3PAR/Nimble or partnerships such as Vast Data.

Whilst we recognise HPE has made initial efforts to address the public cloud storage market, the current offerings fall way behind the competition. We believe it is unlikely the HPE Storage (and, by definition, Hybrid Cloud) business will grow much in the coming years, as customers eventually transition to more attractive competitor solutions.

We see this scenario as a worry for the long-term value of HPE, which is increasingly dependent on short-term trends for business growth.

Related Posts

- Analysis: HPE Announces Q2 FY2024 Results

- Analysis: HPE Announces Q1 FY2024 Results

- Research Note: HPE updates GreenLake for Block Storage with Alletra MP and introduces AWS Cloud Edition

- HPE to Acquire Juniper Networks for $14 billion

Copyright (c) 2007-2024 – Post #1ddd – Brookend Ltd, first published on https://www.architecting.it/blog, do not reproduce without permission.