Dell Technologies has announced financial data for the fourth quarter and the full financial year of 2024. Compared to FY2023, revenue is down 13.6%, net income is down 9.7%, while ISG declined 11.7% and CSG declined by 16%. Are there any positive messages to take from the data?

Background

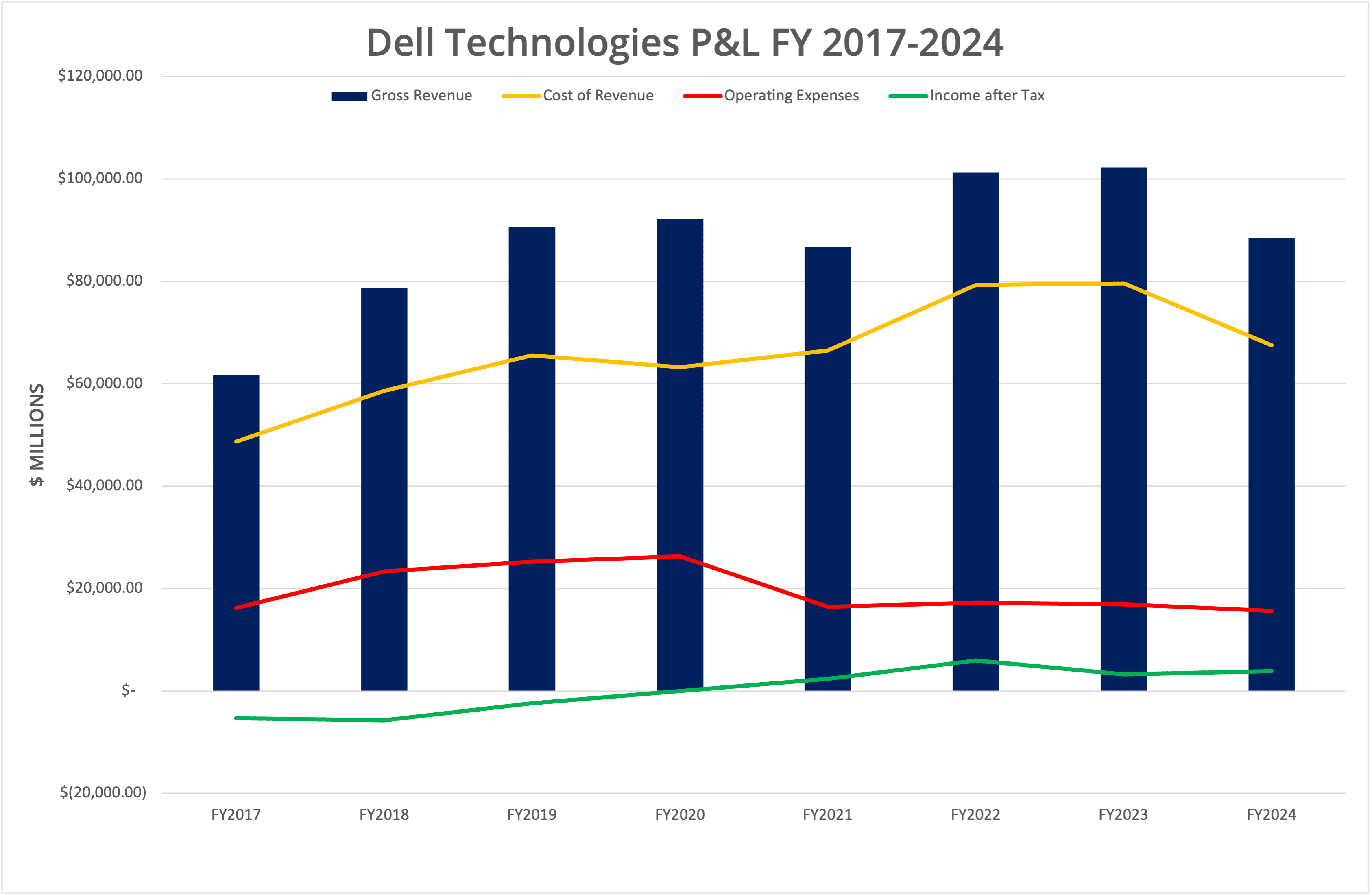

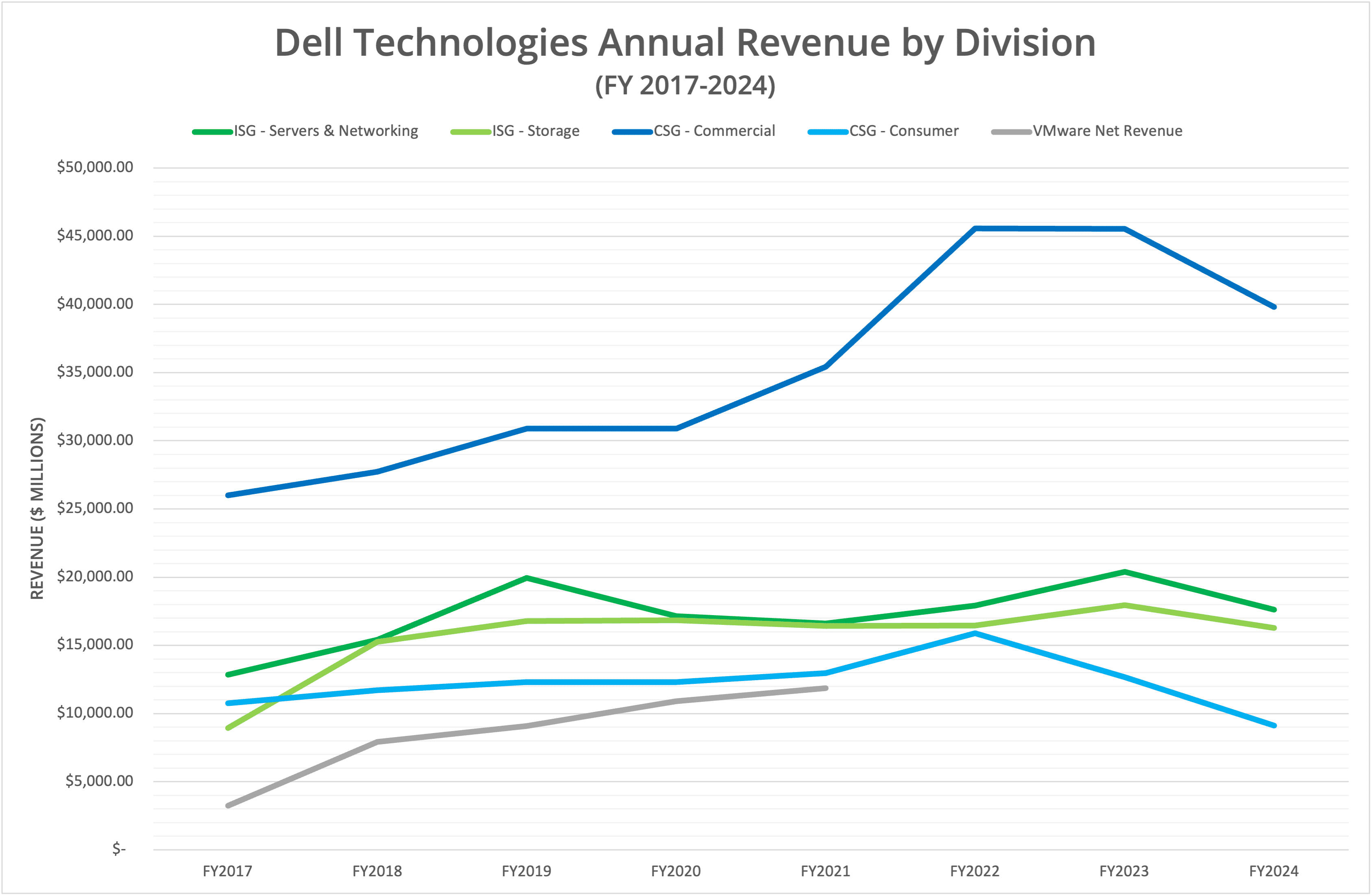

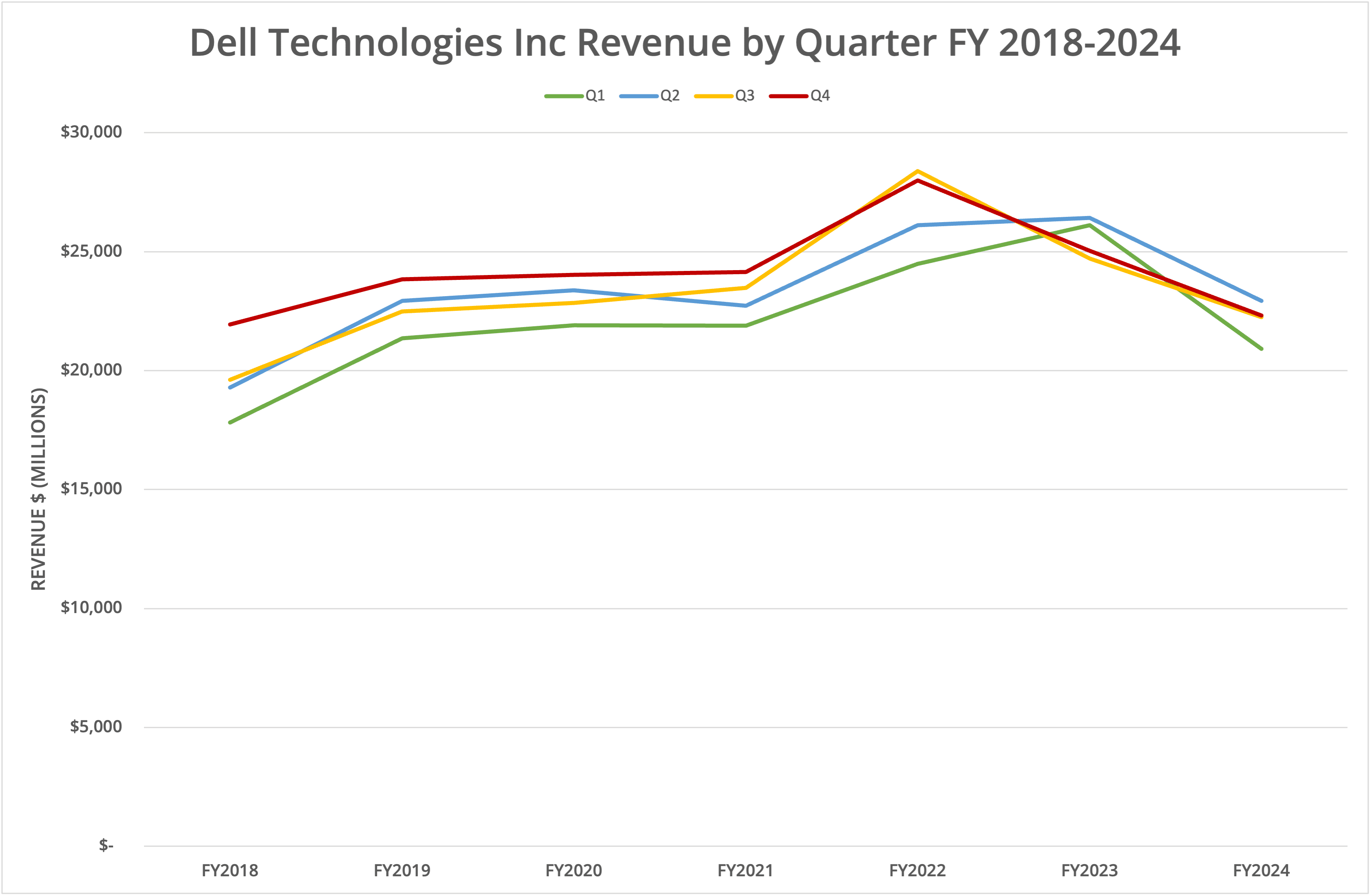

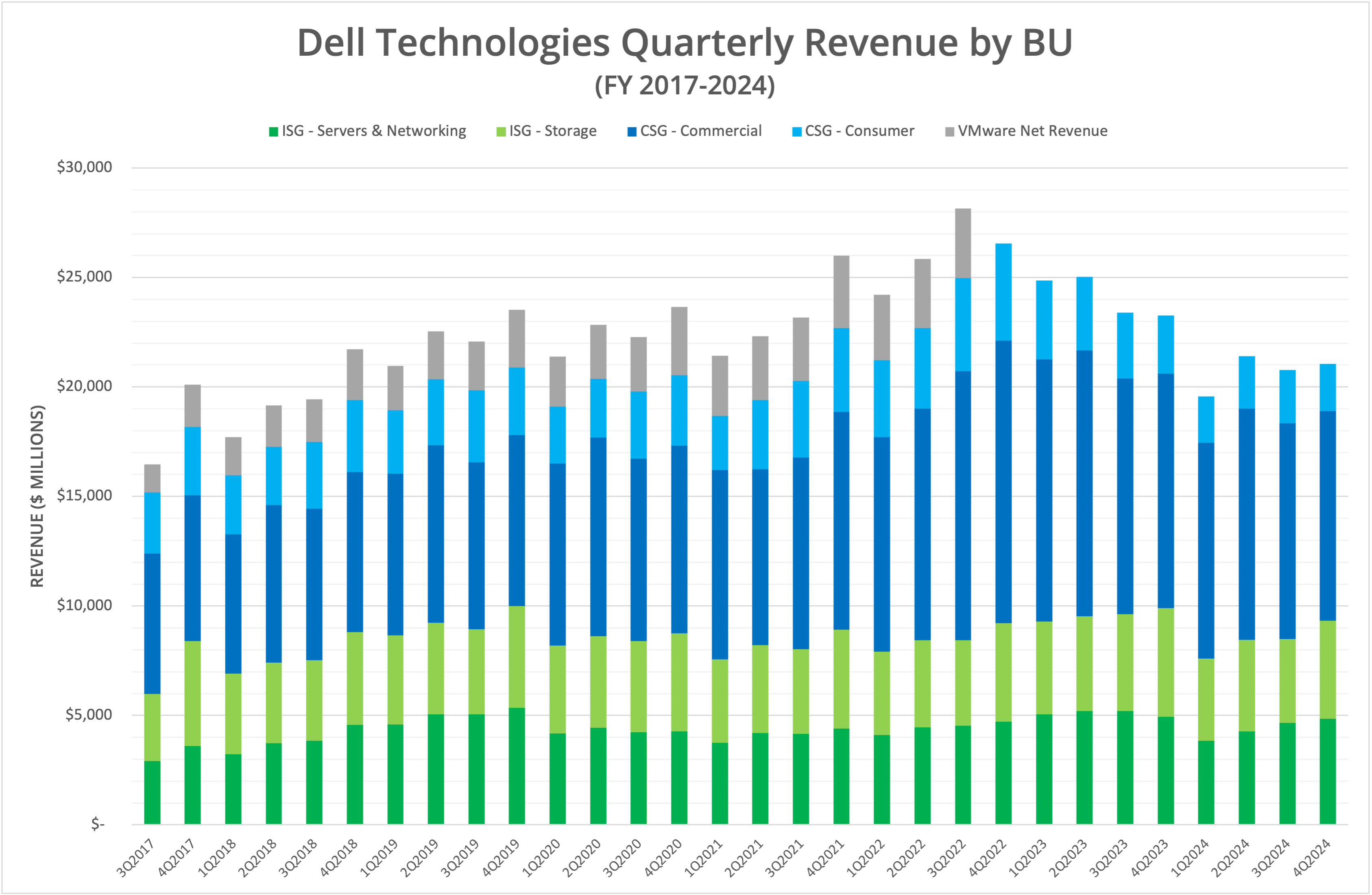

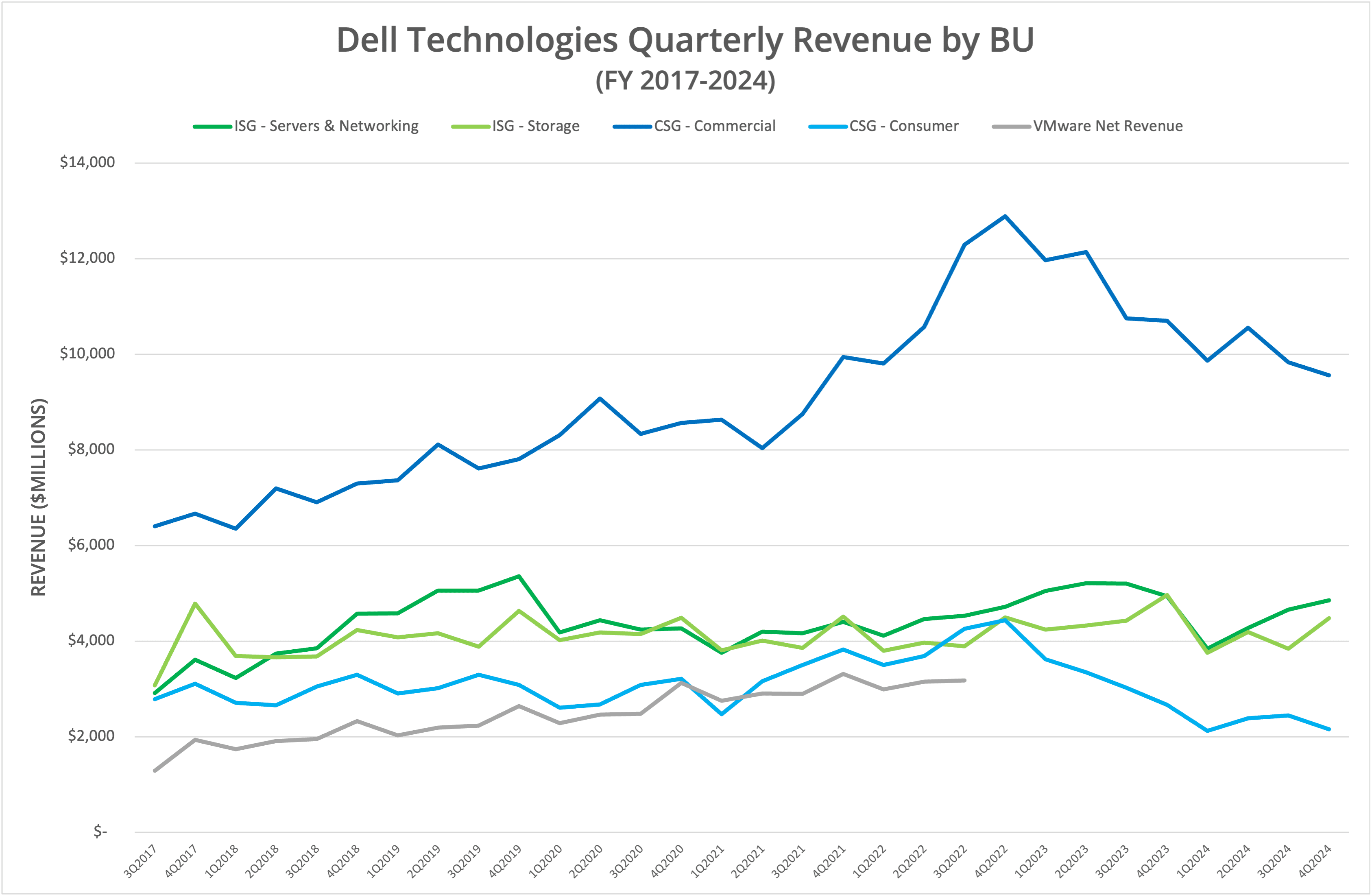

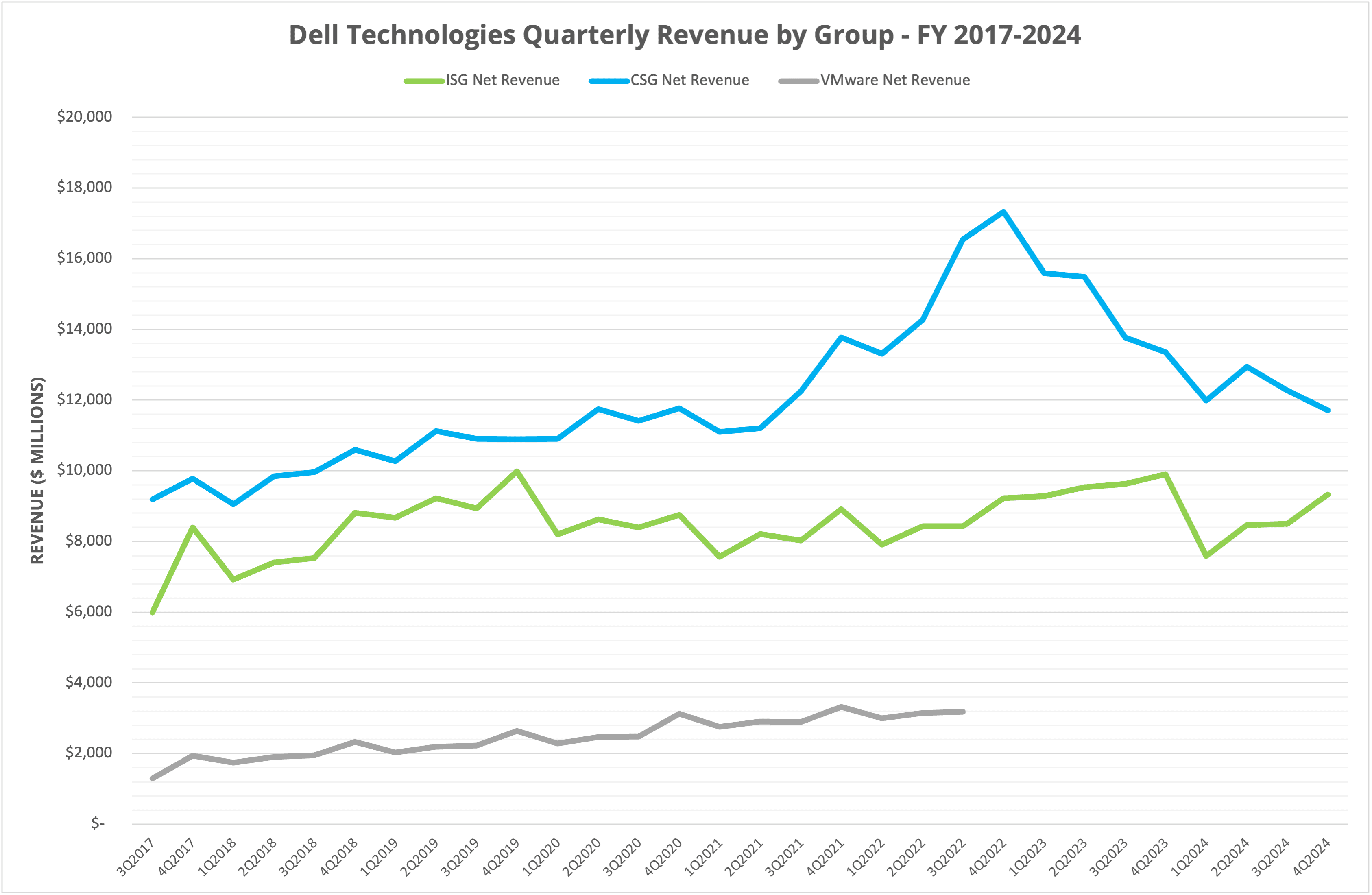

The data presented in the fourth quarter results highlights a picture of two distinct stories (or maybe more). Compared to FY2023, revenue was down 13.6% (the company forecasted a 12%-18% decline), while net income declined 9.7%. Both ISG (infrastructure group) and CSG (client group) declined by 11.7% and 16.0%, respectively. Figure 6 (the last image) demonstrates the change in fortune for CSG, continuing to see declines following the peak around Q3 FY2022, representing significant demand during the COVID-19 period.

Sequentially, ISG revenue has continued to recover, with a 9.8% improvement since Q3 FY2024. However, CSG doesn’t reflect a similar trend, with an ongoing sequential decline.

AI PC

From an industry perspective, the client market is expecting the “Next Big Thing” to be the emergence of the AI PC. Without a doubt, 2024 will be the year that AI stifles every other technology market, grabbing all the oxygen and news headlines. The AI PC, driven by Intel 14th Generation Core processors, include new processor extensions (such as Intel’s first integrated NPU) to make client-based AI inferencing a real possibility.

Of course, this leap in hardware also needs an accompanying step forward in software, and that, perhaps, is where the market is lacking. Microsoft has already introduced Copilot into Windows 11, with continuous improvements and extensions to the technology capabilities. However, this introduction is an iterative process, with an “advanced” version of Copilot expected in Windows 12 (or whatever it might be called). The timeline for this could be late 2024 or 2025.

Although the hardware will be ready, the software will take time to catch up. We’ve only highlighted the O/S capabilities, but businesses will be expecting more from applications. So far, though, there doesn’t appear to be any standards or O/S API frameworks in place that manage security and privacy requirements. This could result in piecemeal implementations that cause concern for enterprise customers.

One final point to consider. Every new PC will be an AI PC, if it has an Intel processor, as the technology is included by default. If the AI technology is ubiquitous, does that provide enough incentive to upgrade, or will enterprises and consumers simply replace ageing hardware on a previous cycle?

Enterprise AI

The other area that Dell Technologies is hoping will take off is the use of AI within the data centre. The company has partnerships with Microsoft (for Copilot 365), Meta (on-premises LLM such as Llama 2) and obviously NVIDIA (Project Helix hardware solutions), to name but a few. However, we see a few headwinds in adoption.

- AI hardware (specifically GPUs) has issues with lead time and availability. These hardware components are also expensive (to buy and run) relative to the cost of servers.

- The power draw for GPU hardware is much greater than traditional servers, which may impact the ability of businesses to deploy the hardware in existing data centre facilities.

- The use cases and ROI for AI capabilities don’t appear to have been formalised, which we believe will result in more initial proof-of-concept deployments than full-scale AI implementations.

- Spending on AI infrastructure may divert from refresh spending on existing servers and storage (or direct more spending into the public cloud.

The greatest challenge in the enterprise is to determine precisely what generative AI can be used to deliver. Many businesses will be keen to exploit the potential benefits of GenAI but may not have the funds, capabilities (people and infrastructure) or clear use case for the technology.

The Architect’s View®

Architecting IT doesn’t provide financial advice or comment on stock prices. However, it’s interesting to note that after the FY2024 results were published, Dell Technologies’ share price rose by almost one-third (but has fallen back slightly since). Clearly, the market sees potential in AI, both from the client and enterprise perspectives. This optimism is expressed elsewhere, with a significant rise in NVIDIA’s share price and that of Supermicro, as two examples.

In a gold rush, the shovel seller makes the most money, as the well-worn anecdote tells us. Dell Technologies could be well-positioned to increase revenue from AI in both client and enterprise markets. However, we think there’s a degree of over-optimism in the market, tied with adoption timescales that may elongate based on external factors (like software adoption of AI features).

Dell Technologies may be able to deliver the server hardware. However, across the board, we still see weaknesses in the storage portfolio (for example) that other vendors are able to exploit. Our long-term view is the AI bubble will be short-lived and deliver a short-term boost but not be a replacement for fundamentally better products in the current market. As such, we expect a constant long-term decline in Dell Technologies’ business unless something changes.

Related Content

- Dell Technologies Announces Q3 FY2024 Results

- Dell Technologies Announces Q2 FY2024 Results

- Dell Technologies Announces Q1 FY2024 Results

- Dell Technologies Announces Q4 FY2023 and Full Year Results

- Dell Technologies Microsite

X-Ray: Dell Technologies, Inc.

This Architecting IT report takes a deep dive into Dell’s history, products, services, and future outlook. This report is only available for download via paid subscription.

Copyright (c) 2007-2024 – Post #1d43 – Brookend Limited, first published on https://www.architecting.it/blog, do not reproduce without permission.