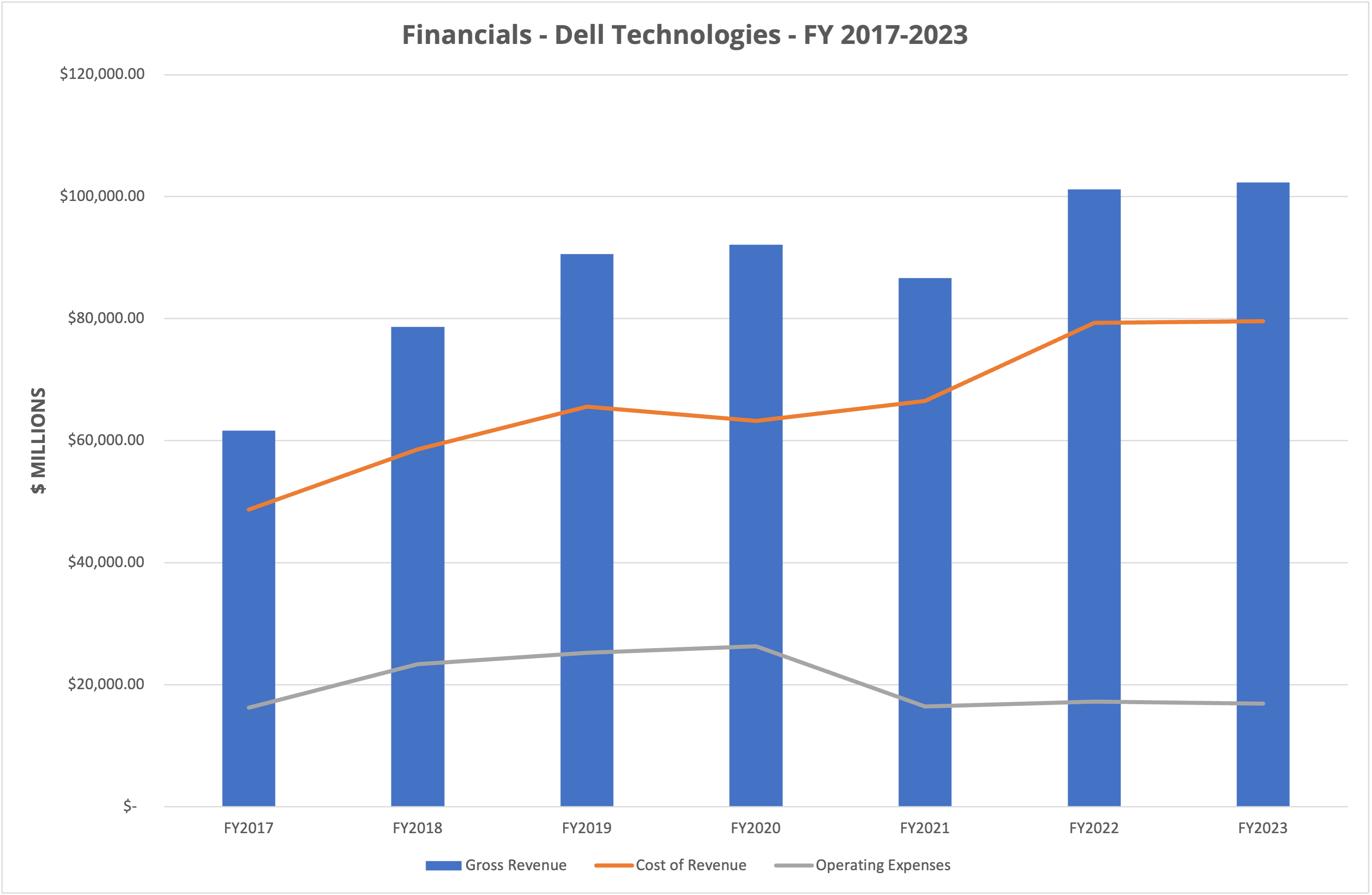

Dell Technologies has announced Q4 revenue figures for the financial year 2023 of $25 billion (down 11%), while revenue for the year is a record $102.3 billion (up 1%). These results seem to point to a tale of two different stories, so what can we learn from the data and where the business is headed?

Background

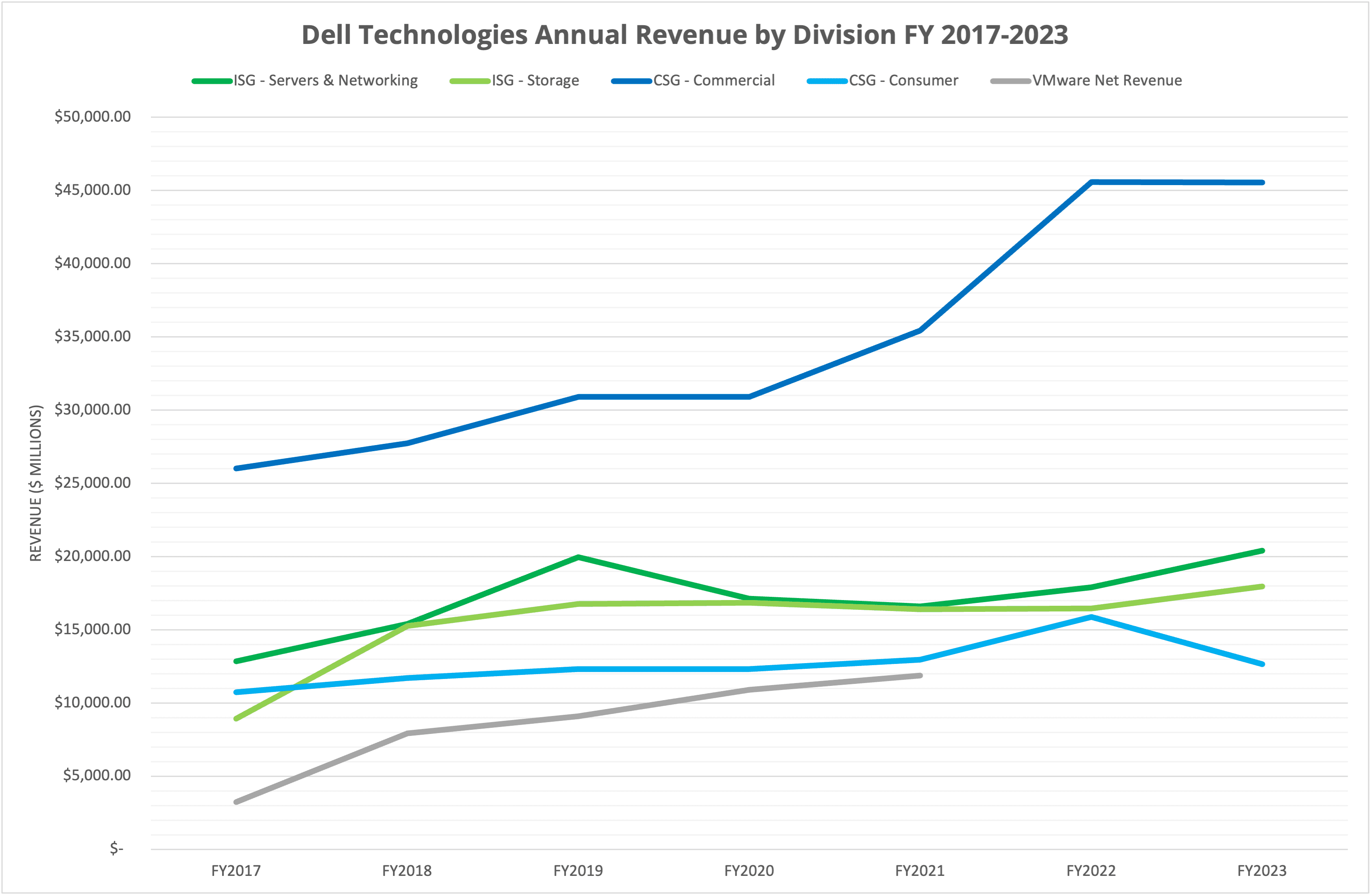

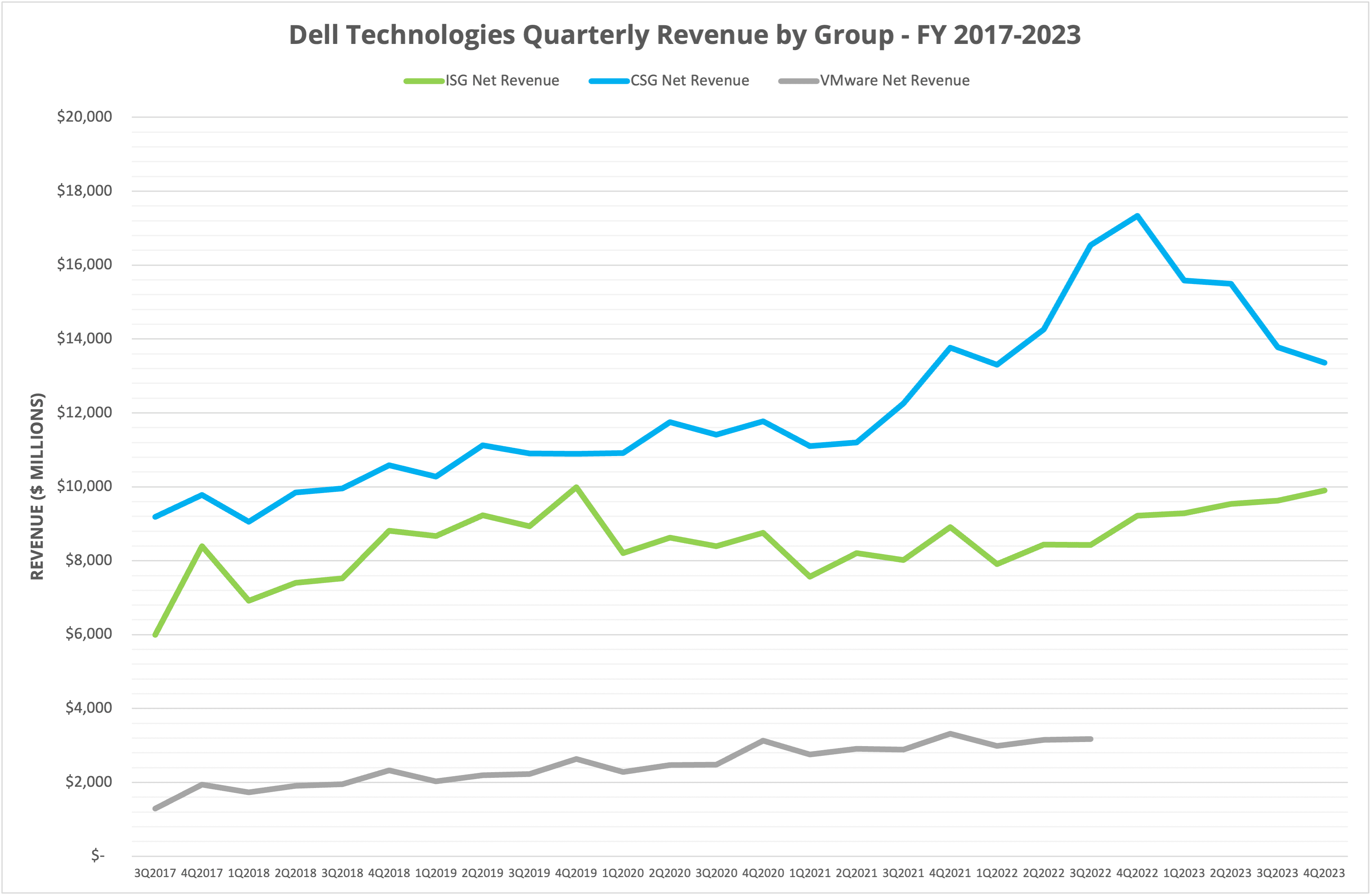

We last looked at Dell Technologies financial data back in August 2022 and prior to that May 2022 when we discussed the company’s hybrid cloud strategy. Figures 1 and 2 show annual data (overall revenue and revenue by division, respectively). It’s clear from the numbers that CSG Commercial contributed massively to the bottom line through the COVID pandemic as businesses sought to manage remote working.

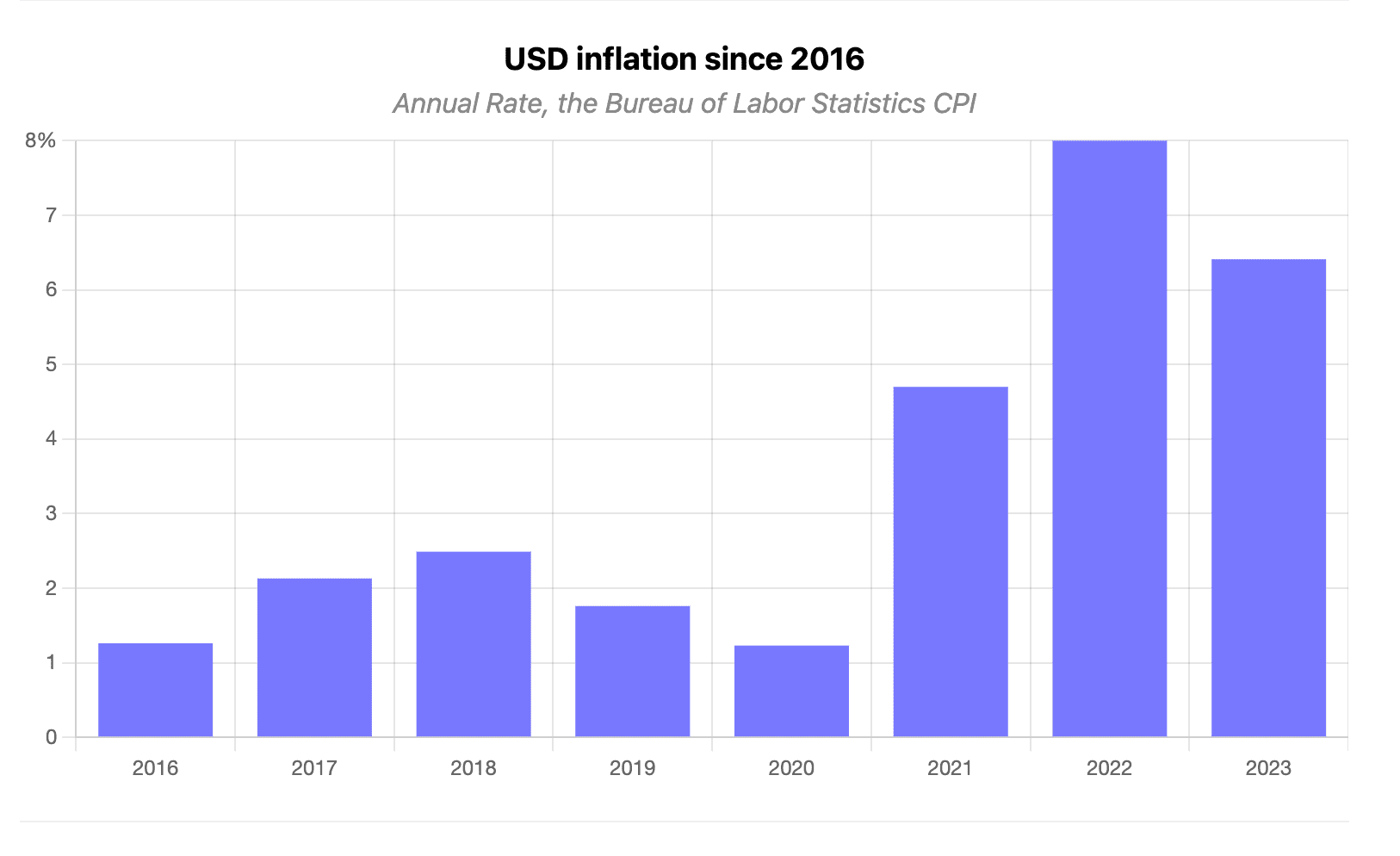

In the last 12 months, CSG Consumer revenue has declined, while CSG Commercial has flatlined. Both ISG Servers/Networking and ISG Storage have seen increases of 14% and 9% respectively. Taking inflation into account (figure 3), these numbers are probably more depressed than this.

CSG

The Client Services Group (CSG), effectively the laptop and PC business, did well in the pandemic, but that benefit is over. Back in May 2022, we highlighted how CSG was driving Dell Technologies’ growth. Now it’s impacting the meagre 1% improvement seen in FY2023.

Should we have expected any other outcome as we entered and exited a global pandemic? Probably not. In one respect, the pandemic impact on CSG and ISG were inverse to each other. There’s a degree of yin and yang involved, where improvements in ISG have countered the decline in CSG.

ISG

What about servers, networking and storage? It’s fair to say that ISG did well, probably off the back of latent server demand, but also the ability for businesses to refresh “big iron” storage, now that the travel restrictions of the pandemic are over. ISG income is up 35%, with operating margin increasing from 10.9% in FY2022 to 13.2% in FY2023 (in contrast, CSG declined to 6.6% from 7.1%).

The Architect’s View®

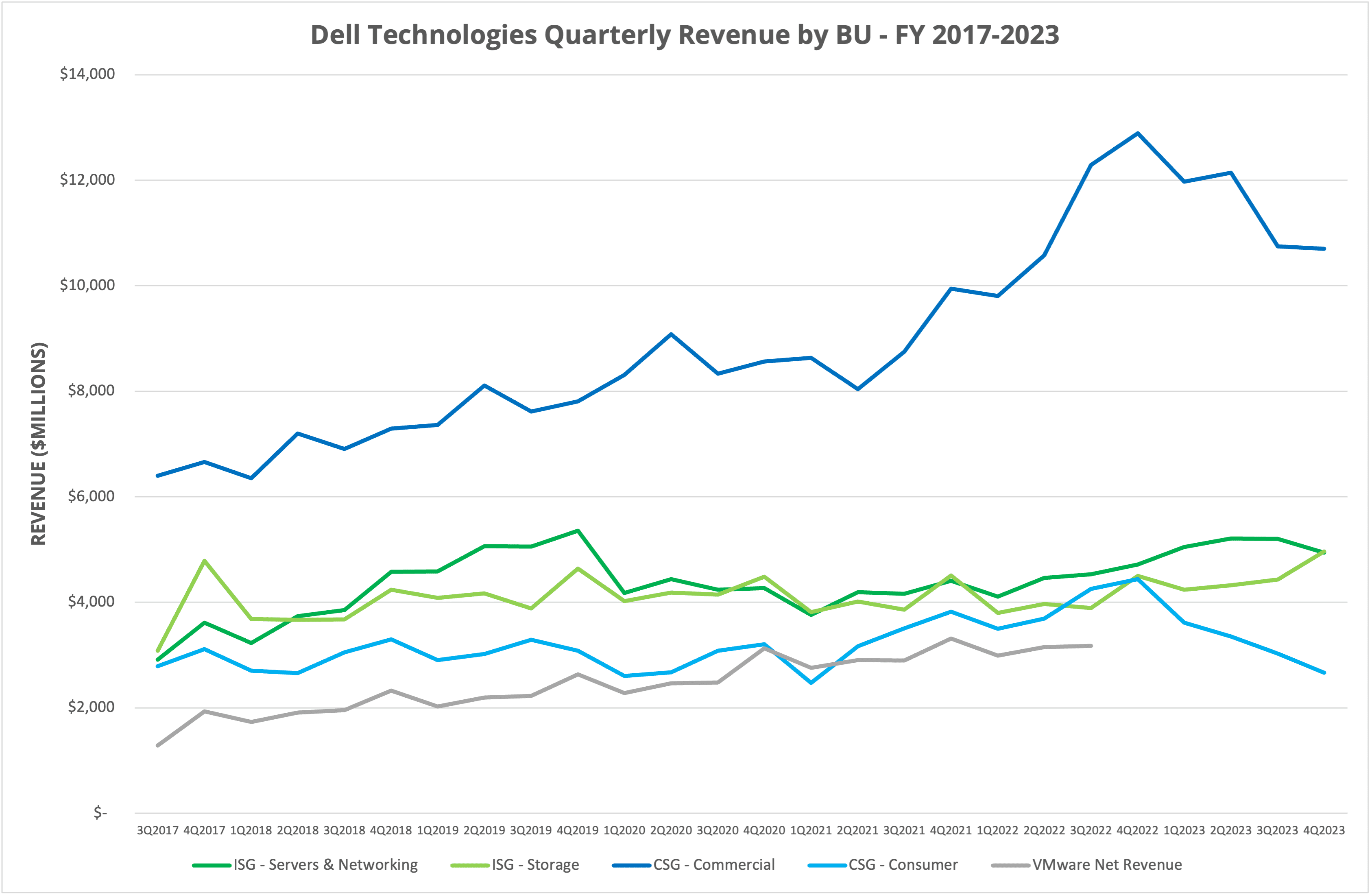

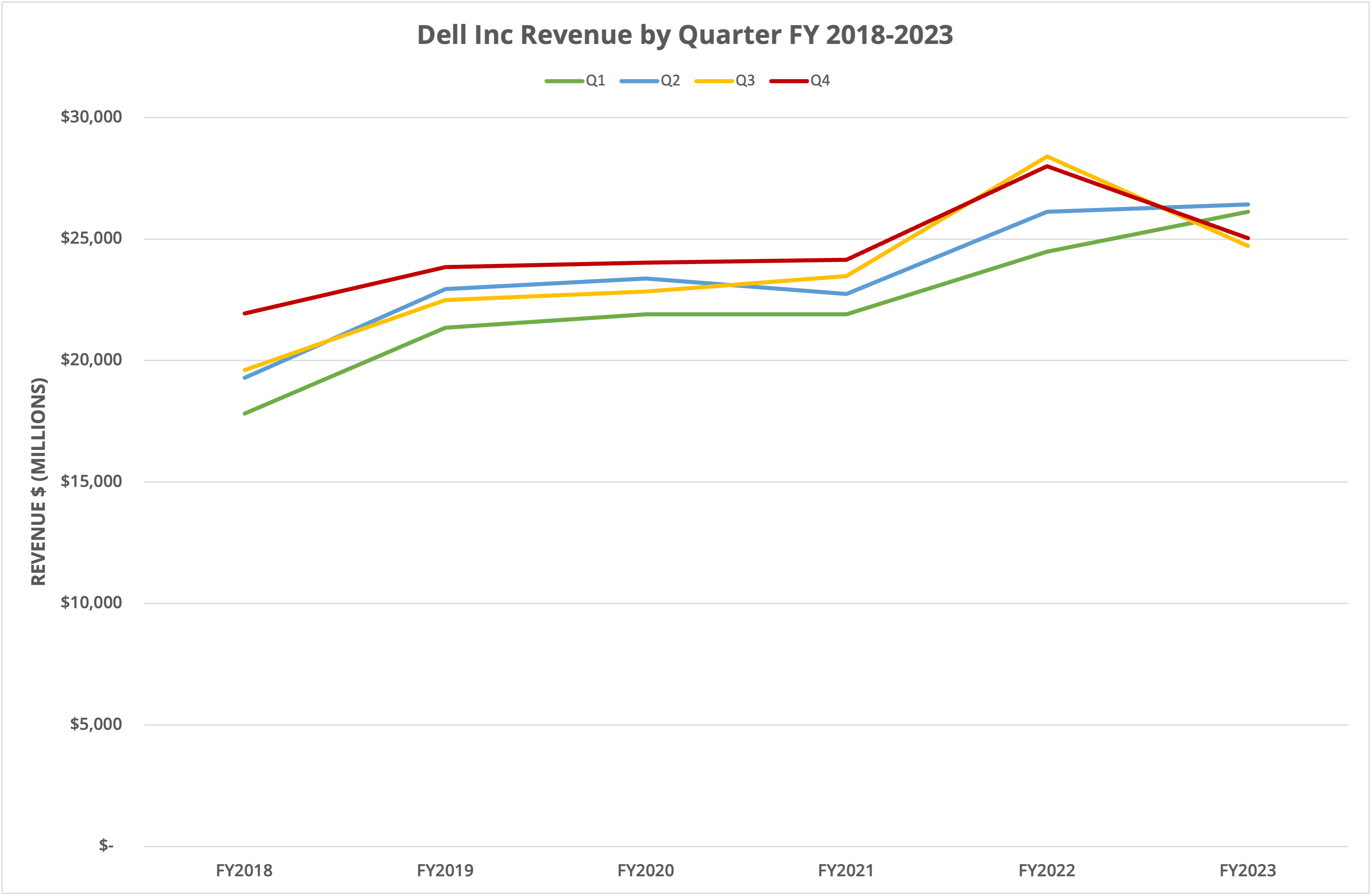

It appears Dell Technologies is firing on all cylinders. However, looking at figure 6, we see revenue growth in every quarter of FY2022, but in FY2023 overall revenue declined in the last two quarters. This makes us wonder whether that decline will continue into FY2024. The answer is determined, as always for Dell, by two separate businesses that don’t always trend in the same direction.

Historically, Dell’s server business has a good Q4, but didn’t in Q4 FY2023. The ISG numbers were saved by Storage. Storage is always strong in Q4 and continued that trend. What does that mean for APEX and “as a service” selling? Like the data for HPE, we can’t see much evidence of a transition to ARR yet, other than perhaps increased margin (as we mentioned above).

As usual, we will be looking at the news from Dell Technologies World, to see what progress has been made on Project Alpine (storage in the cloud), APEX and Project Frontier, which might open other revenue avenues at the edge. For now, it seems things are still a mixed picture for Dell Technologies.

Copyright (c) 2007-2023 – Post #4e53 – Brookend Ltd, first published on https://www.architecting.it/blog, do not reproduce without permission. Dell Technologies is a Tracked Vendor by Architecting IT in storage systems and computing infrastructure.