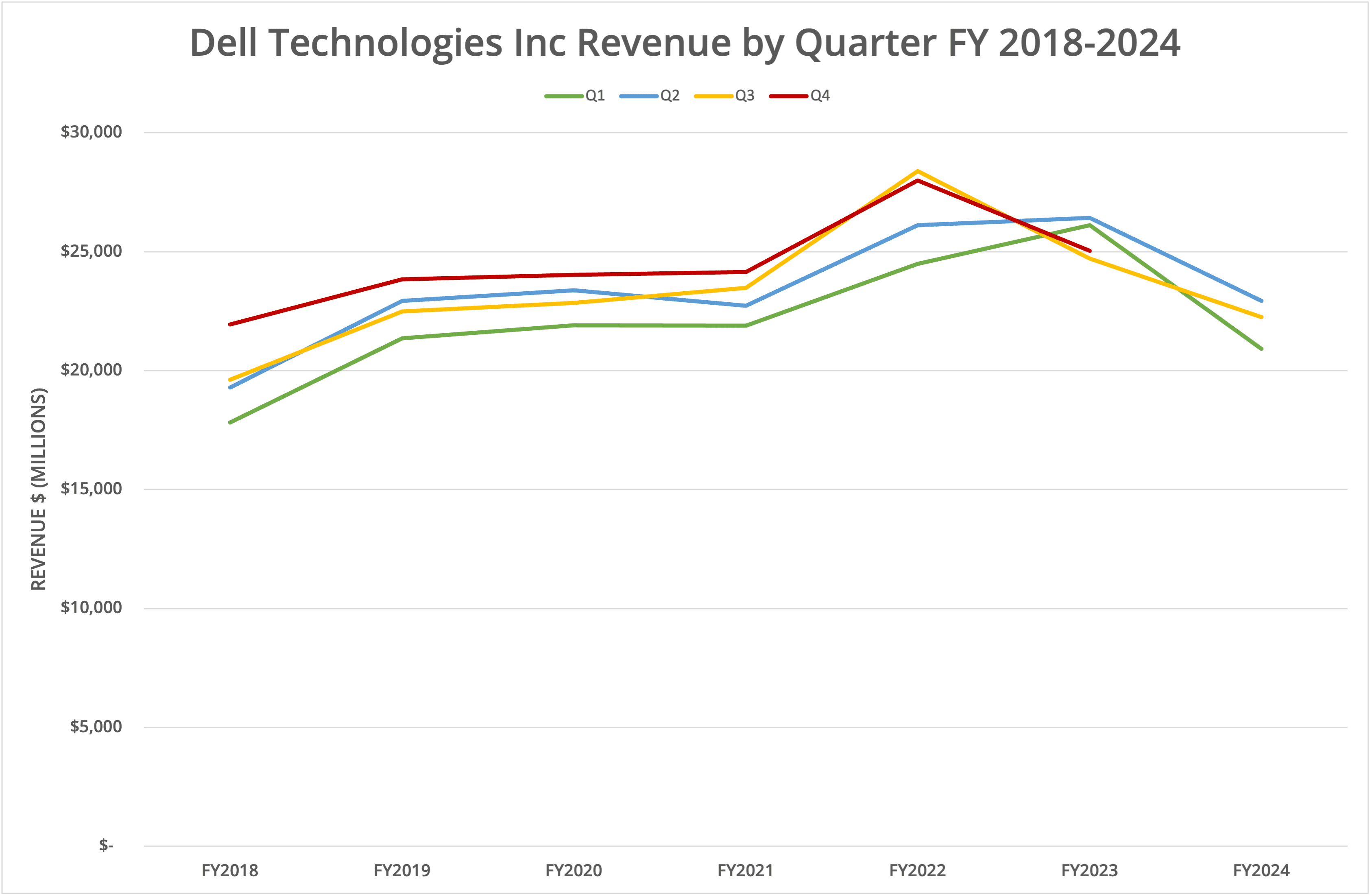

Dell Technologies, Inc. has announced Q3 FY2024 results, with a 10% decline in revenue year-on-year and a 3% decline sequentially. ISG revenue is down 12% year-on-year (flat sequentially), while CSG revenue is down 11% year-on-year and 5.1% down sequentially. Remember when we discussed the Q2 figures and highlighted that one set of improved data doesn’t represent a trend?

Background

Dell Technologies, Inc. has reported financial data for the third quarter of FY2024. Overall, revenue declined 10.0% year-on-year to $22.3 billion, while operating income (profit) was down 15.7% year-on-year at $1.5 billion (or 6.7% of revenue).

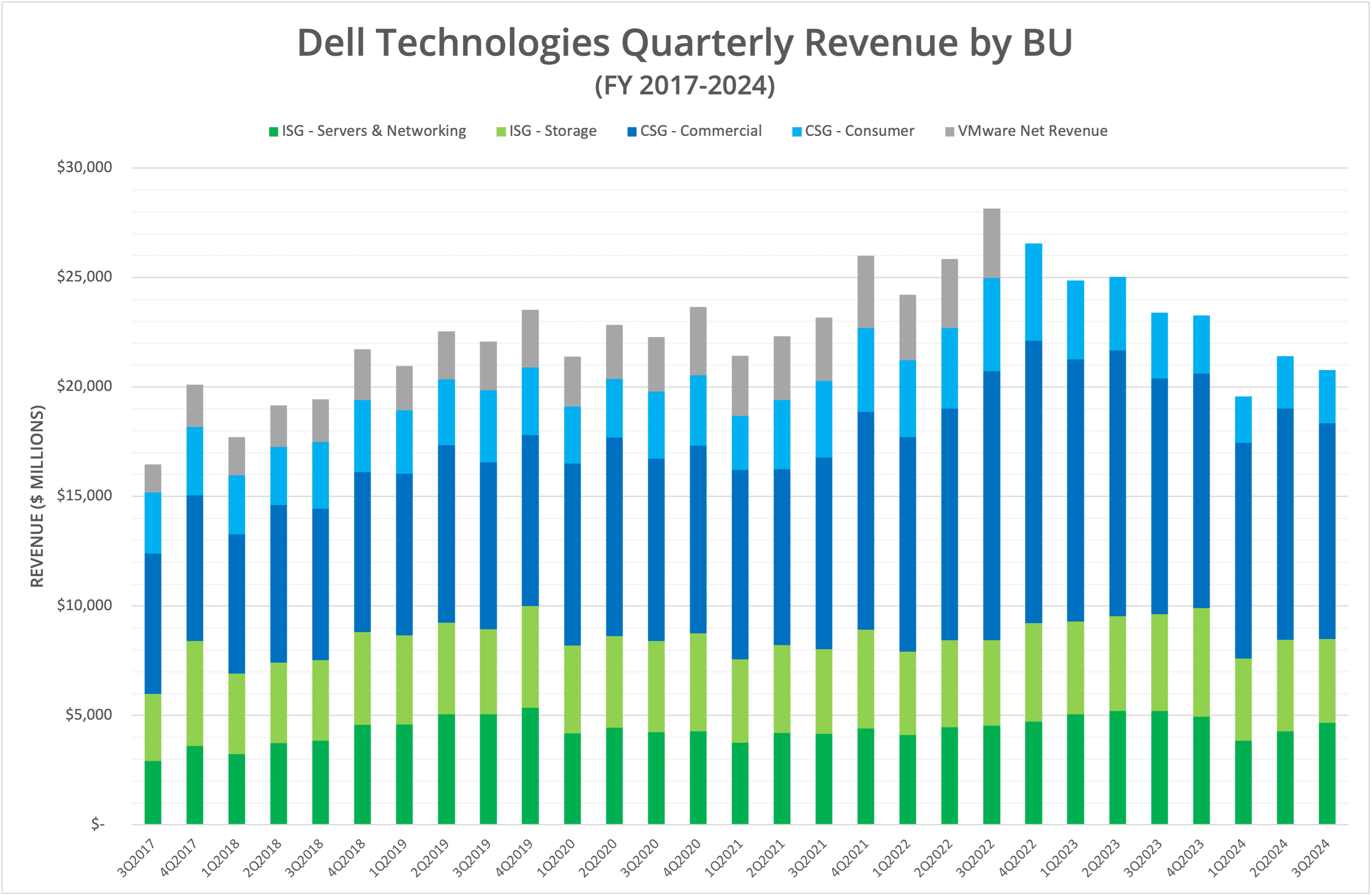

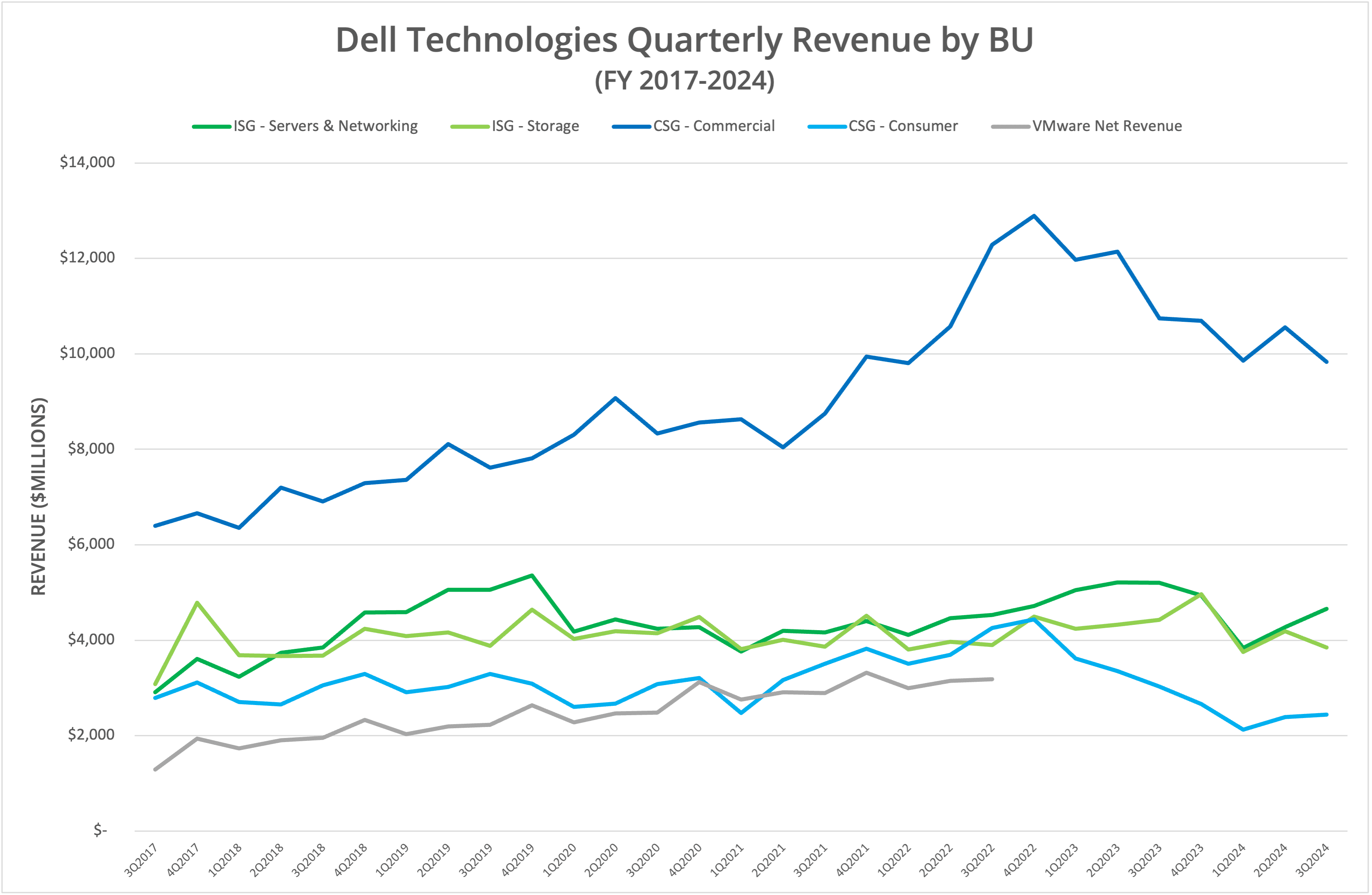

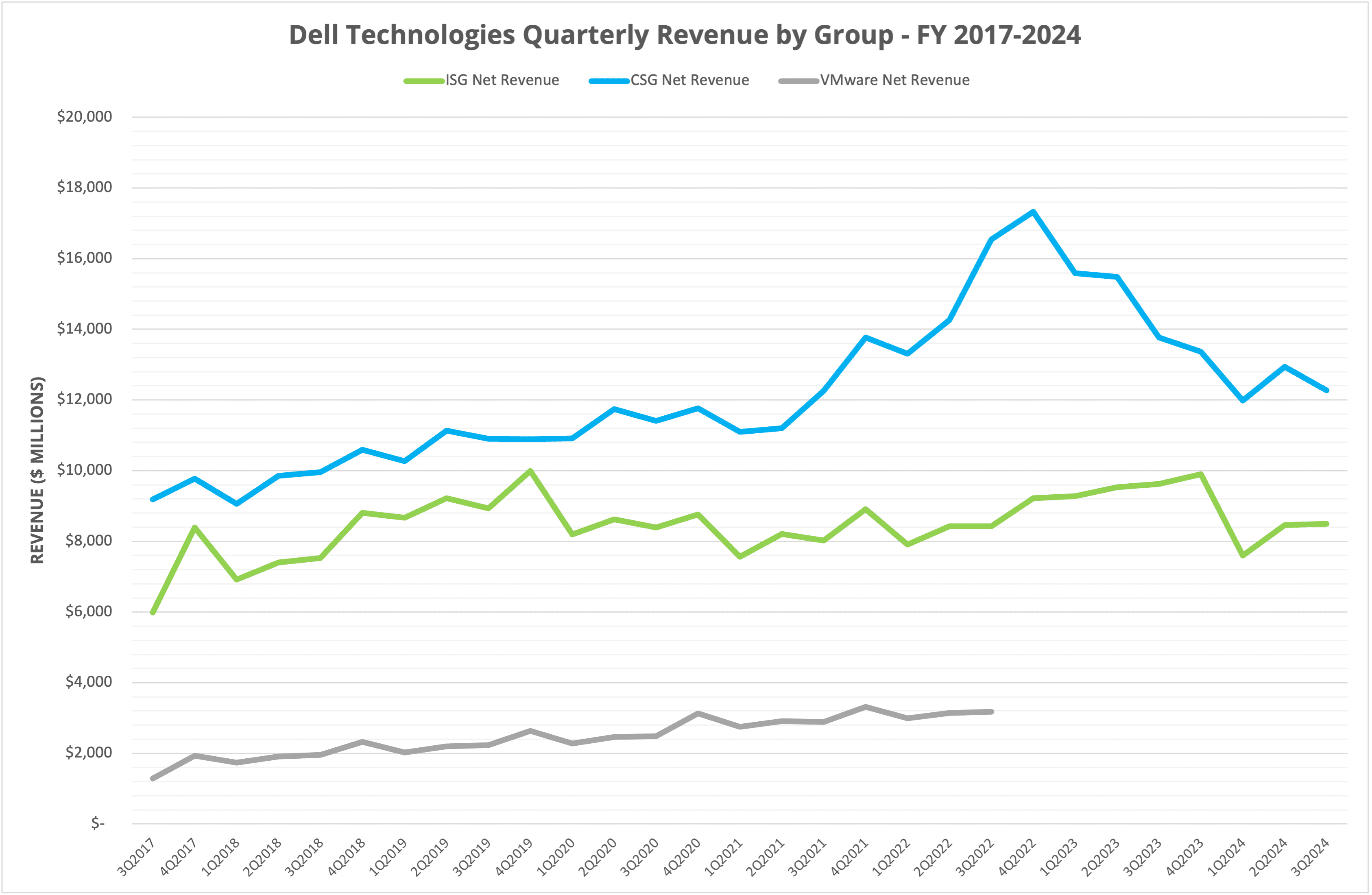

By business group, ISG (Enterprise servers, storage & networking) declined 11.7% year-on-year and was flat sequentially, while CSG (endpoint devices, laptops, and desktops) declined 10.9% year-on-year and 5.1% sequentially. Within the business groups, in ISG, Servers & Networking improved, while Storage sales declined. In CSG, Consumer sales improved, while Commercial sales declined.

As we highlighted in the last quarter review, one quarter doesn’t represent a trend. The gains made in CSG and ISG in the last quarter have been erased by poor performance in the current period, which was a guidance miss based on the Q2 Performance Review. Full year guidance has also now been downgraded.

AI

Like most technology companies, Dell Technologies is attempting to ride the wave of AI and the expected benefits that it delivers in terms of additional hardware revenue. The company has released (or at least announced) new hardware solutions, including a new ObjectScale XF960 all-flash object storage platform and partnerships with LLM creators. Dell Technologies is also hoping that the “as-a-service” model will make APEX a success, countering some of the migration to the public cloud.

Strategy

However, we see three primary issues with Dell Technologies’ strategy.

- APEX is similar to HPE’s GreenLake in that it provides an alternative leasing framework but isn’t a true “as-a-service” solution. New offerings such as APEX Cloud Platform for Microsoft Azure and Red Hat OpenShift are simply bundles of software and hardware that have been pre-validated, similar to the days of converged infrastructure (which we rarely hear about now).

- Dell Technologies has no believable public/hybrid cloud strategy. To date, cloud storage solutions are repositioned software products that didn’t previously drive much revenue. The strategy so far feels like a “me too” or box-ticking exercise. Customers are unlikely to be interested when there’s no compatibility with the primary solutions sold on-premises and other much more superior offerings already available in the public cloud.

- Generative AI needs more than validated hardware designs. Instead, customers need end-to-end solutions with data management, zero-ETL, workflow and other features to help build and manage models. Those features don’t appear to be easily consumable on-premises compared to the public cloud.

On the last point, we’ve just seen a swathe of AI-related announcements from AWS at Reinvent in Las Vegas. The overwhelming feeling from those new product solutions is a move towards building much greater lock-in for applications and data, making it harder for on-premises vendors to offer anything equivalent.

The Architect’s View®

One of the greatest challenges for on-premises infrastructure vendors is how to counter the growth and appeal of the public cloud. In the early days, AWS, Azure and GCP could have been considered alternatives for on-premises virtual infrastructure. The public cloud offered convenience but wasn’t particularly mature compared to on-premises platforms. However, as we highlighted in this blog post, cloud hyper-scalers had a plan to build services on top of infrastructure, starting with platforms like databases but spanning all aspects of the developer lifecycle and experience.

Over the last 12 months, generative AI has exploded, with GPU demand skyrocketing and products hard to source. The public cloud has been able to meet customer requirements for AI training and inferencing, partly by developing in-house alternatives to GPUs from NVIDIA and Intel.

At AWS, we saw Amazon cement the end-to-end capabilities available for building and deploying large AI models, with capabilities that simply don’t currently exist on-premises or would be expensive and complex to deliver by hand.

Therein lies the problem for Dell, HPE and other infrastructure providers. What steps can they take to counter the pull of the public cloud when it comes to Generative AI? HPE has already taken steps to deliver LLMs as a service offering. What is Dell doing? As far as we can see, only partnering with selective companies rather than developing entire ecosystems.

Could Dell Technologies create products and solutions to rival the public cloud? Currently, spending on R&D is only 3% of revenue (compared to Pure Storage at 24%). With such a small gross margin (around 23%), we can’t see how Dell Technologies could match the spending power of the public cloud while continuing to pay off the debt from the EMC acquisition in 2015/2016.

There will be some return to growth in 2025 for Dell Technologies, as all infrastructure businesses are cyclical. However, we continue to believe the long-term outlook will be one of continuing decline as new business growth is claimed by the public cloud.

X-Ray: Dell Technologies, Inc.

This Architecting IT report takes a deep dive into Dell’s history, products, services, and future outlook. This report is only available for download via paid subscription.

Copyright (c) 2007-2023 – Post #d2a1 – Brookend Ltd, first published on https://www.architecting.it/blog, do not reproduce without permission.

This post is only available to Individual, Vendor or Enterprise subscribers. Restrictions on distribution are based on those licensing terms. Check our Terms of Service for details.