Following the failure of a potential merger with KIOXIA, Western Digital has announced plans to split into two businesses, divided by media type (HDD and flash). What does this move mean for customers, shareholders, and the wider industry?

Background

At an Investor Day in May 2022, Western Digital announced plans for a review into the future of the business, with the aim of what is euphemistically called “optimising long-term value for shareholders”. The move was a response to intervention by activist investor company Elliott Management Corporation, well known for embedding itself into businesses where it believes more value can be gained by selling off assets.

Over recent months, we’ve discussed a potential merger between Western Digital and KIOXIA, a spinoff from Toshiba’s memory division. At the time of the spinoff in 2018, Bain Capital owned around 56% of the company, while Toshiba retained around 40.6%. Western Digital and KIOXIA have a joint venture, Flash Ventures, which does wafer manufacturing for both companies.

Merger talks were halted after SK Hynix objected to the deal. SK Hynix is a competitor in the flash business (it acquired Intel’s NAND business in 2021 for $9 billion) and an investor in KIOXIA through Bain Capital.

With the merger strategy now dead, Western Digital has unveiled plans to separate into two businesses, one focused on hard drives, the other on flash. This move effectively unbundles the assets from the acquisition of SanDisk in October 2015 and STEC in 2013.

Rationale

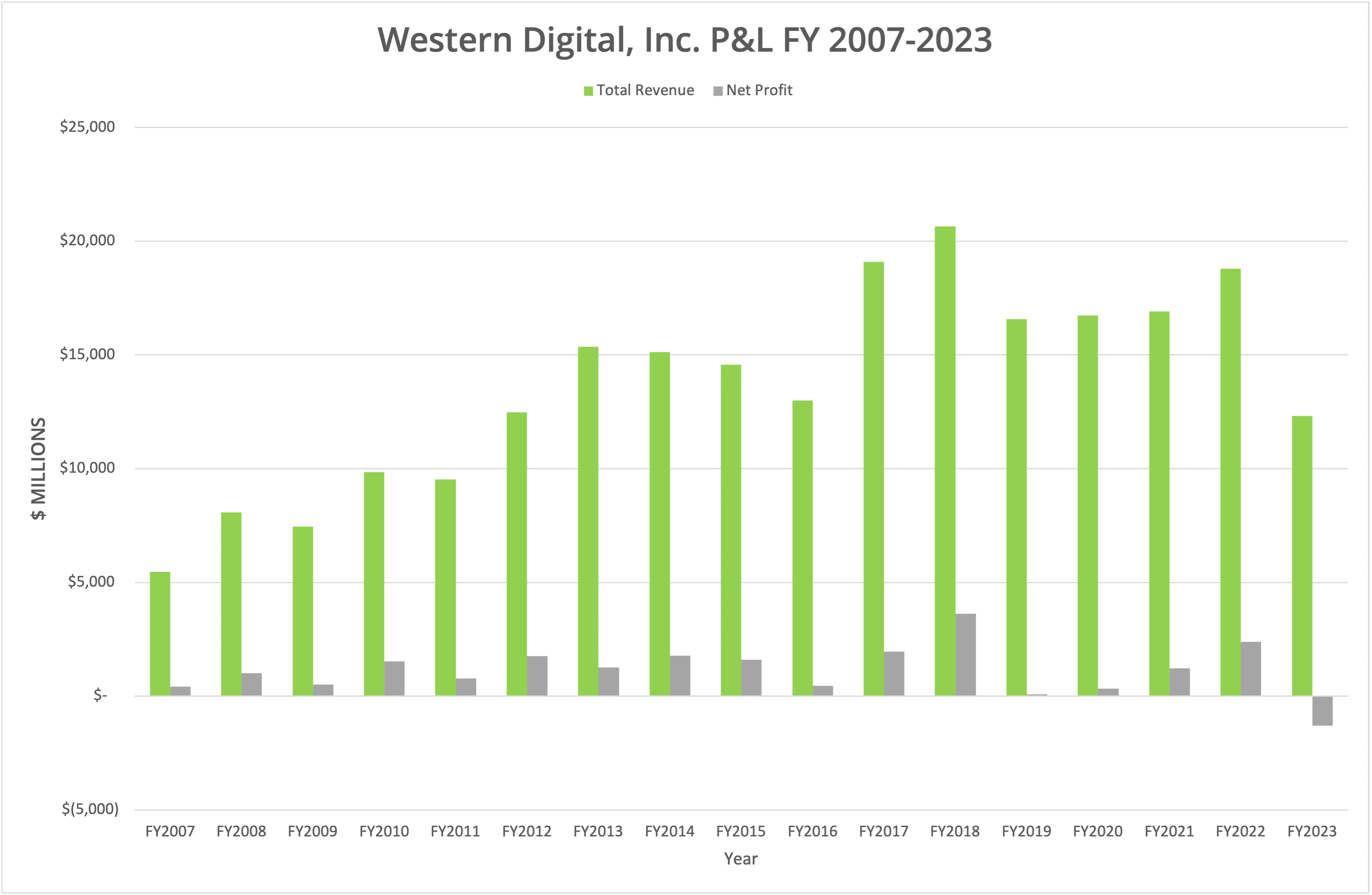

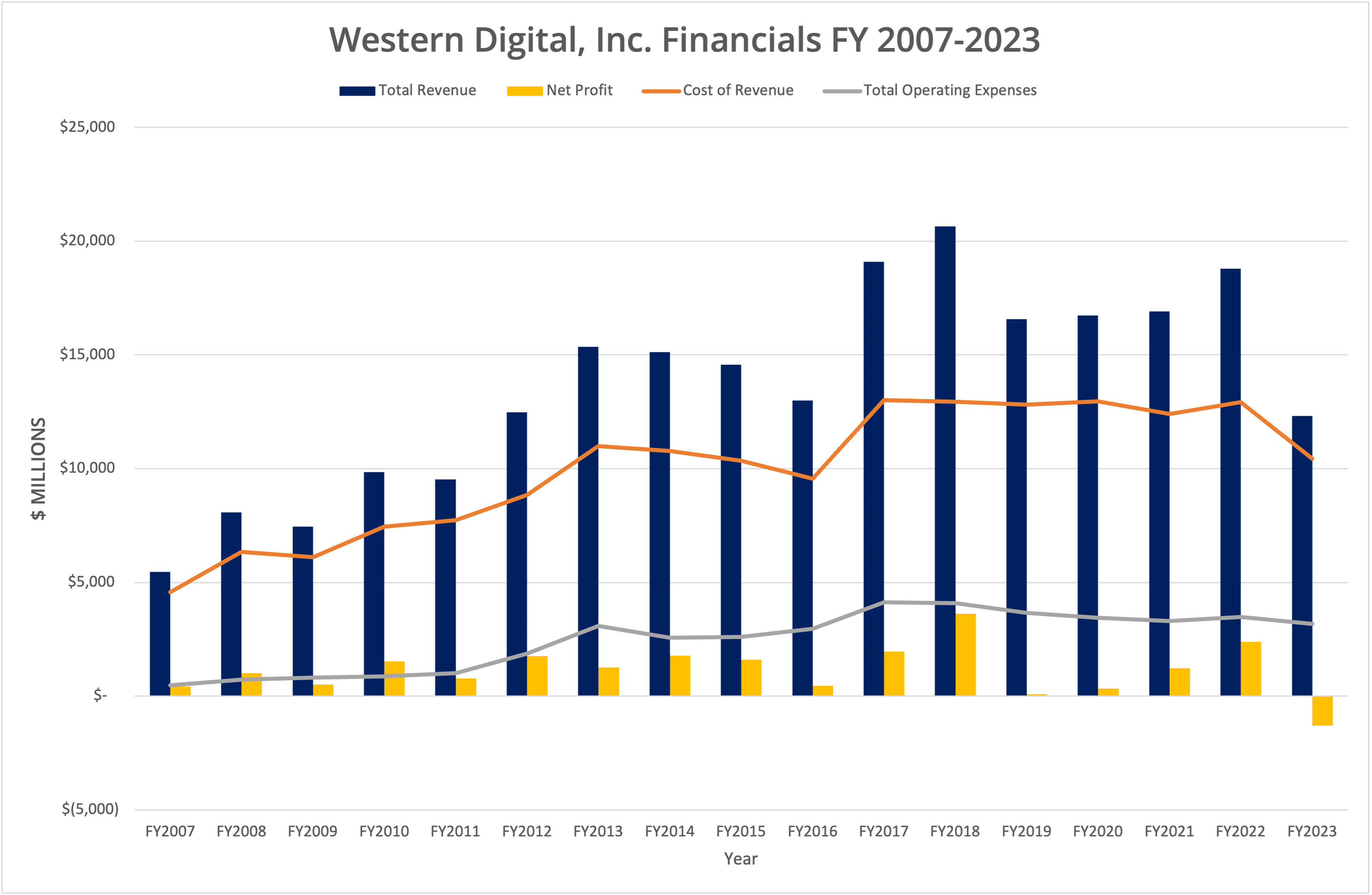

In an investor briefing on 30 October 2023, Western Digital claimed that the split of the business would create two industry-leading companies, one in the legacy hard drive market, the other in the flash market.

The post-pandemic landscape for NAND flash vendors has been challenging, with all the contenders in the market struggling to make money. However, the HDD industry hasn’t been immune to issues, mainly due to the slowdown of spending by hyper-scalers, arguably the biggest market for HDDs today.

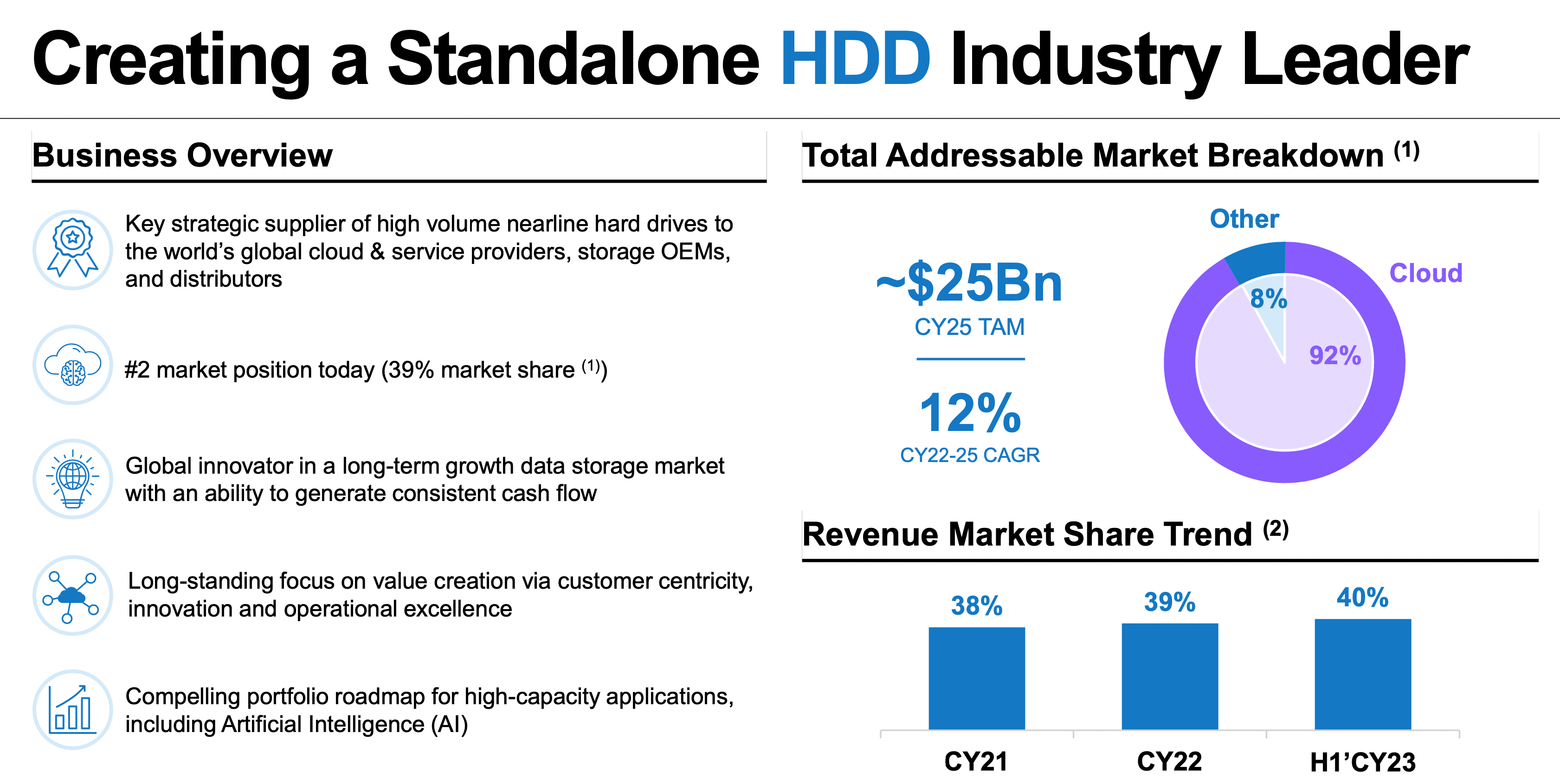

Going forward, Western Digital predicts the HDD business will have a 40% market share, and be number two in the market with a CY2025 TAM of around $25 billion. This data is based on an assumed compound annual growth rate (CAGR) of 12% between 2022 and 2025.

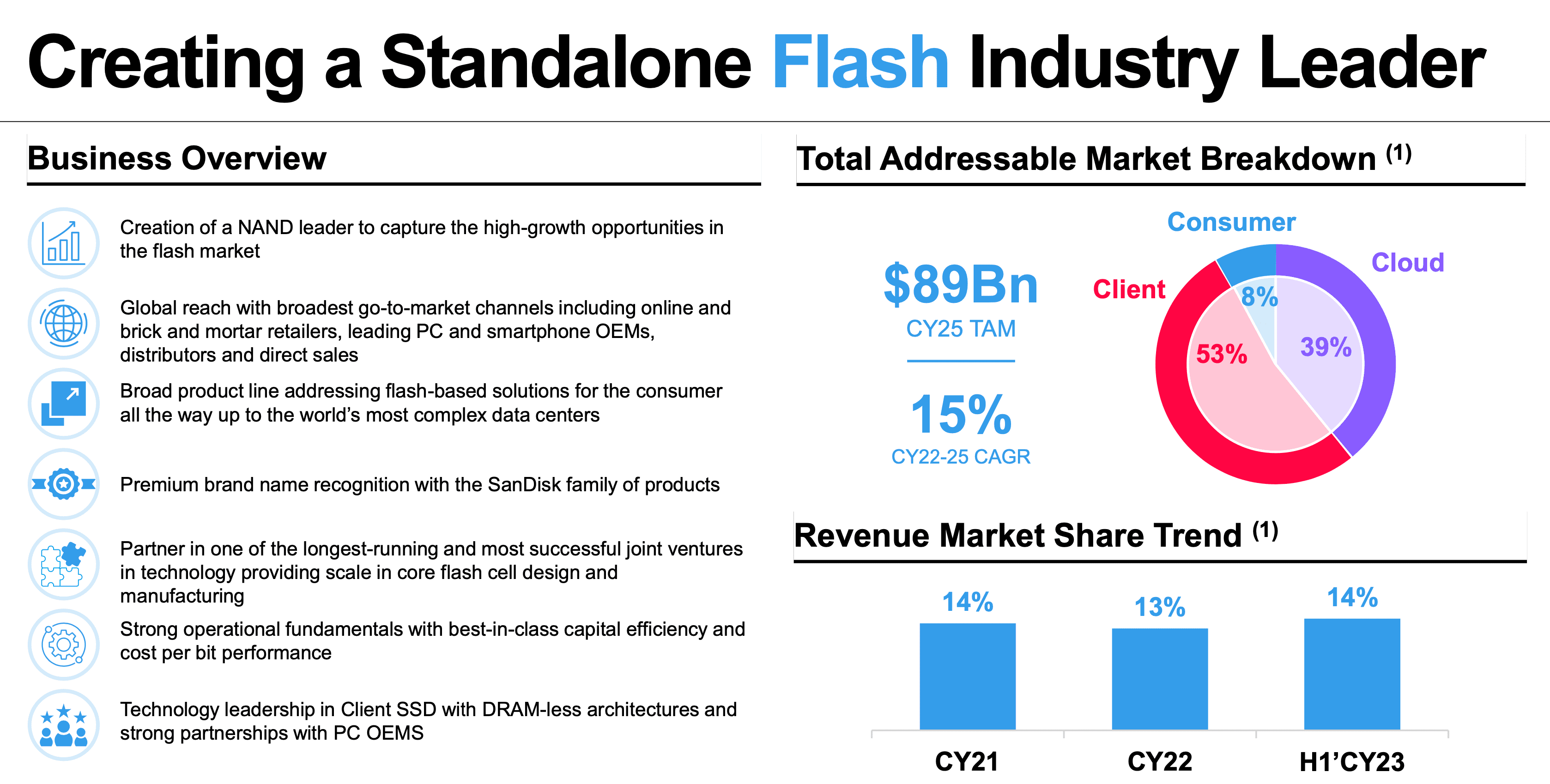

In the NAND flash market, the new company would have around 14% market share in a total addressable market of $89 billion (CY2025), with an estimated CAGR of 15% between 2022 and 2025 (no market position was quoted).

Dependencies

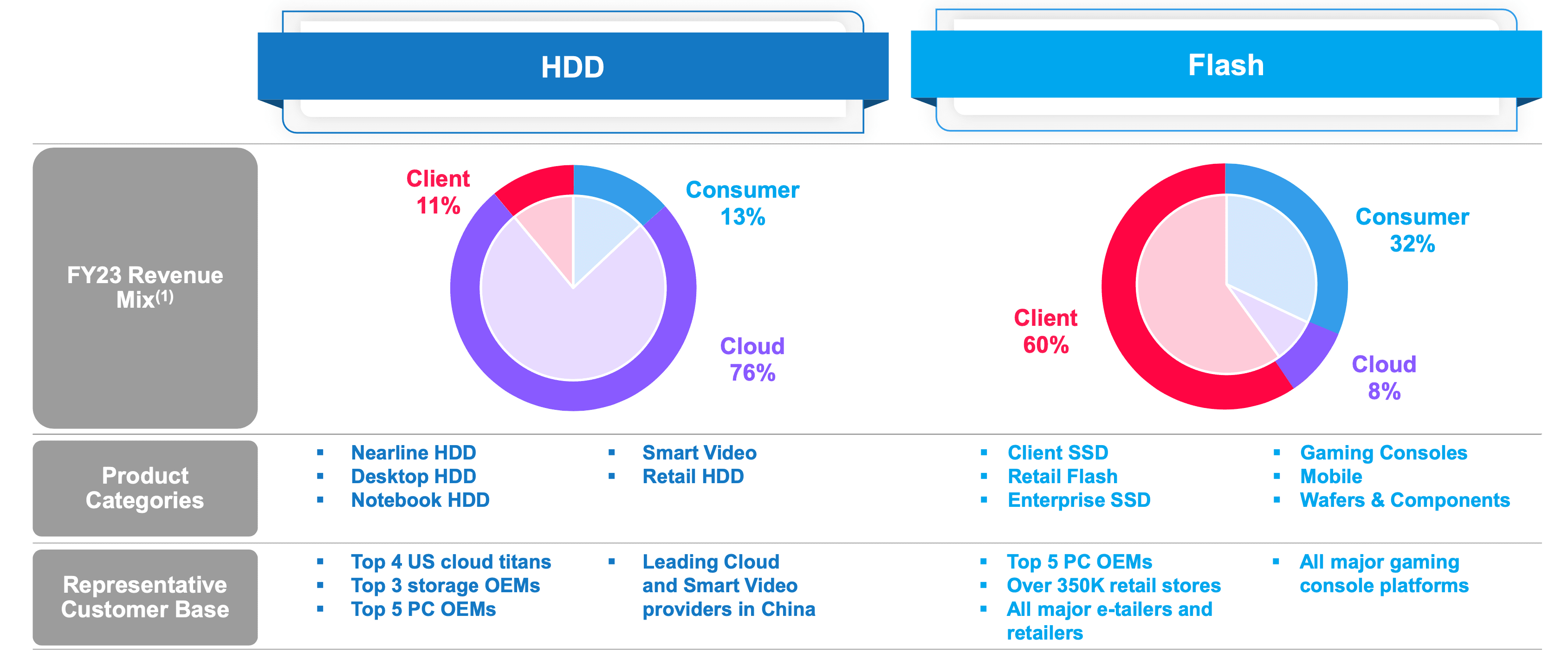

Two other points of note are interesting to highlight. First, Western Digital sees the HDD market as being 92% Cloud (public and private but all enterprise), while the flash business is only 39% Cloud, 53% Client (OEMs) and 8% Consumer, all by 2025. This breakdown represents a transition that increases Cloud sales at the expense of the Consumer market.

The Architect’s View®

The hard drive business is in long-term decline (see our X-Ray on Seagate), and with only three players in the market (Seagate, Western Digital, and Toshiba), being number two isn’t particularly market-leading.

Our view is that over the mid to long term, the HDD business will be much more focused on manufacturing than research and development of new products. Capacity growth will slow (in relative terms), and margins will continue to be challenged in a commodity business. The biggest customer for HDDs will increasingly be hyper-scalers as the consumer and on-premises enterprise markets continue the transition to all-flash.

In flash, the recent price drops have demonstrated that no vendor is immune to market trends. However, flash is the growth market for storage, and with nothing on the horizon to replace it, will be the dominant bulk active media for some decades.

It’s interesting to rationalise why a business split makes sense for Western Digital. From its own data, the HDD market is declining but has good margins (>20%), while the flash market is growing, but is currently showing negative margins. Splitting into two businesses creates one with long-term stagnation (but potential profits) while the other is increasing in a challenging financial market.

In our view, it would make more sense to continue to use the HDD business to fund the long-term development of the flash side of the house. Instead, the two independent companies will exist in two challenging markets with little buffer benefits from either.

What’s the future for an independent Western Digital HDD business? Financial data from Seagate shows a constant decline, which will undoubtedly accelerate as flash closes the TCO gap with hard drives. Two scenarios are then possible. First, Western Digital gets acquired or merges with Seagate/Toshiba. Second, a hyper-scaler like AWS picks up Western Digital as an asset to protect its requirement for hard drives.

In either event, whilst shareholders may benefit from the split with some short-term gain, the industry will lose diversity and innovation. The era of the hard drive could be coming to an end quicker than we think, particularly for its use in on-premises data centres.

Copyright (c) 2007-2023 – Post #44c4 – Brookend Limited, first published on https://www.architecting.it/blog, do not reproduce without permission.