In the last few days, we’ve seen announcements from Broadcom that simplify VMware licensing and move sales to a subscription model. EUC and Carbon Black have already been discarded as not strategic, with the likelihood of more rationalisation to come. Broadcom, a hardware company, is acquiring software assets not to create some business transformation but as a source of cash generation.

Background

Since 2018 and the acquisition of CA Technologies, Broadcom has continued to grow its software assets, including acquiring VMware and the security business of Symantec. At first, it may seem that Broadcom has decided to move into software as an alternative strategy for hardware acquisition. Many industry observers cite the failed attempt to acquire Qualcomm as the pivoting factor. However, we don’t believe this is the case.

History

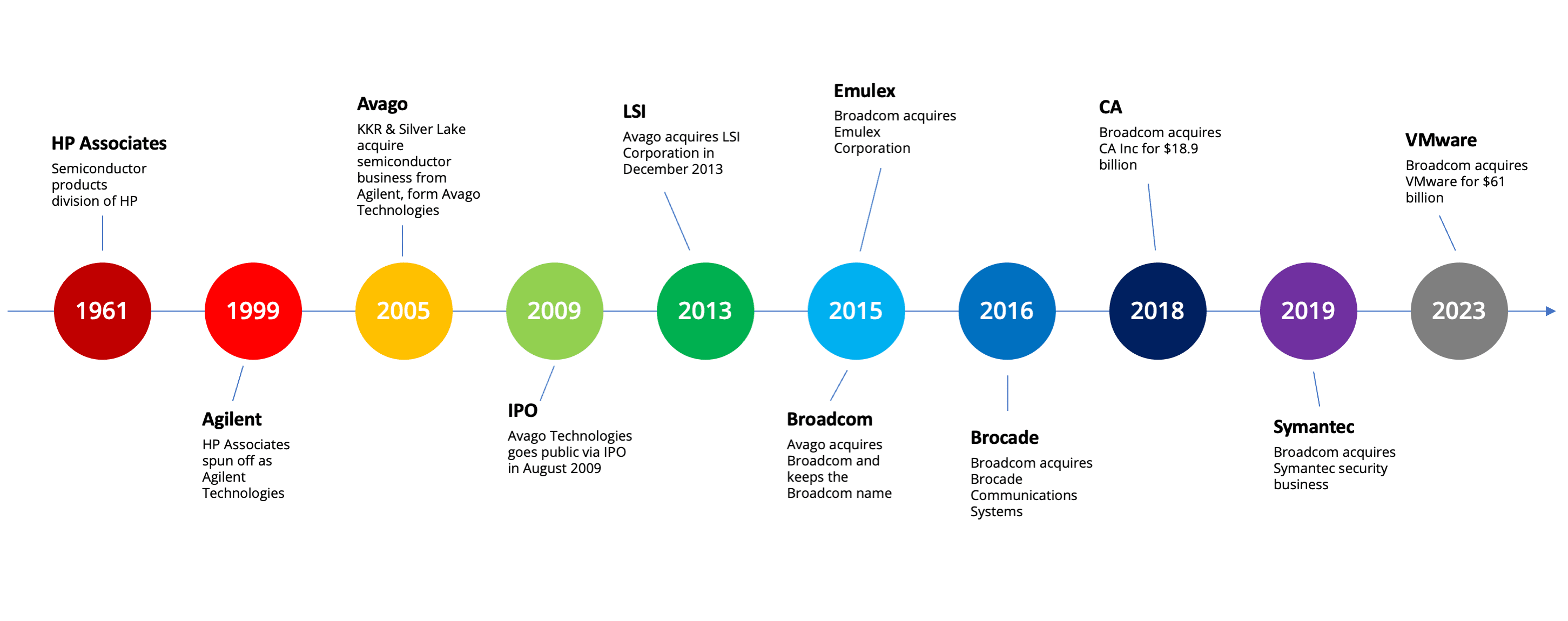

The Broadcom of today has an fascinating history. The origins start with HPE (HP at the time) and the spinoff of HP Associates to form Agilent Technologies. Agilent sold its semiconductor business to private equity (KKR and Silver Lake Partners), forming Avago Technologies, operating as a private business. At this point, current Broadcom CEO Hock Tan was recruited to run the company. Avago was floated, and through IPO, became a public company in 2009.

In 2015, Avago acquired Broadcom Corporation, becoming Broadcom Limited. The company also acquired Emulex Corporation. In order to acquire Brocade Communications, in 2016, Broadcom Limited moved its headquarters from Singapore to the US, becoming Broadcom Inc.

Software

Up to this point, Broadcom’s business appeared to focus on acquiring and extending hardware assets and technologies. An attempt to acquire Qualcomm in 2017 was blocked by the Trump administration in the US, citing national security concerns. Media speculation suggested that Broadcom turned to the software market as an alternative way to grow the business. As we’ve highlighted already, Broadcom acquired CA in 2018, Symantec assets in 2019 and VMware in 2023.

Why would Broadcom decide to acquire what can only be described as legacy assets by buying CA and Symantec?

Computer Associates

It’s worth spending a moment looking at the history of Computer Associates from the perspective of acquisitions. This page on Wikipedia attempts to capture the acquisitions made by CA from its inception in 1976 to its acquisition in 2018. Two notable companies stand out for me personally. Those are Uccel and Legent Corporation.

- Alternatives to VMware: Introduction

- Alternatives to VMware: Nutanix

- Incremental improvements from VMware at Explore 2023 ahead of the Broadcom acquisition

- Will customers really jump ship when VMware is acquired?

In the late 1980s, I started my career in the mainframe world. For the next decade, every mainframe environment I encountered used CA-1, CA-7, and CA-11 software, with around 50% using ACF2 in place of IBM’s RACF. All of these products came from the CA acquisition of Uccel in 1987. Over that time, those products barely changed, and from what I’ve read in the current documentation, they look pretty similar today.

CA had a history of acquiring mainframe assets, including Legent Corporation, which produced Multi-Image Manager (MIM). Licensing was generally based on MIPS (effectively a measure of compute capacity), so bigger mainframes attracted higher licensing charges. MIM was one product I removed from multiple sites when the cost of licensing became excessive due to hardware refreshes.

Fortunately, IBM had a software solution called GRS, which was functionally equivalent to MIM and was included in base licensing. However, IBM either had no equivalent for the CA-1/7/11 products or had solutions that were so poor, they offered no practical alternative to staying with CA.

The lack of product diversity was a significant issue in the mainframe world, where software development was closed and expensive. In the early 1990s, when I was looking to install a quota management system for mainframe storage, I invented a fake software company to be the competitor for a software solution I was hoping to buy. Senior management wouldn’t buy software without a product “bake-off”, so creating a fake product and company was the only route forward for me. (Incidentally, my strategy worked, and we got the software I wanted.)

Subscriptions

The lack of product diversity was an issue for mainframe users but a massive opportunity for Computer Associates, which bought up many software companies over the period of almost 30 years. By the time the company was acquired in 2018, 79% of revenue came from subscriptions ($3.326 billion out of $4.235 billion), with annual profits of around $1 billion. The last annual 10-K from VMware (March 2023) shows revenue of $13.35 billion and income (profit) of approximately $2 billion. Around 30% of VMware’s revenue came from subscriptions at that time.

Both VMware and CA are/were profitable companies with significant subscription businesses. VMware has plenty of scope to move from the perpetual licensing model to subscriptions, which is the basis of the most recent announcement from Broadcom/VMware.

When acquired, CA had plenty of scope to reduce costs, spending $1 billion annually on sales, $406 million on administration and $642 on product development. Similarly, VMware has opportunities for rationalisation, a goal stated by Broadcom when the acquisition was first announced in May 2022.

VMware and CA have lots of similarities and opportunities for rationalisation. However, the most important comparison we can make is to highlight that both companies are dominant in their respective industry segments – CA due to lack of competition and VMware as the market pioneer and leader.

Expansion

Broadcom CEO Hock Tan clearly has an acquisitive nature and sees that route as one way to grow his business. Do the current Broadcom software business and VMware have any synergies? Probably not. But we can be sure that VMware was at a pivotal moment in its history when the acquisition deal was announced.

Firstly, Michael Dell and Silver Lake Partners had clearly decided many years ago that VMware was not in the long-term vision for Dell Inc, with many diverse financial instruments used to eventually transfer VMware’s value away from Dell EMC (the tracking stock being one example).

Secondly, VMware had arguably lost its way, with a raft of software solutions and packages that were difficult to understand. Tanzu, for example, hasn’t worked as a Kubernetes competitor, having too many dependencies on vSphere and being top-heavy on infrastructure requirements.

We believe that VMware’s best days are behind it, but the company still has a huge install base of customers and products. In the same way that the mainframe market offered little or no alternative solutions to CA products, moving from VMware to an alternative solution is a daunting prospect for many large enterprises. Broadcom has found the next CA, a company that can be used to generate long-term income, perhaps for the next one or two decades.

The Architect’s View®

What next for Broadcom and VMware? The speed at which licensing announcements have been made indicates that the subscription migration plan has been in process since the acquisition was first announced. It appears that Broadcom always intended to extract maximum value from customers who can’t easily migrate elsewhere. The lock-in pill has been sweetened slightly with a reduction in subscription costs compared to before the announcement.

Will Broadcom invest in VMware? It’s our belief that the VMware business is just another cash generator to fund future acquisitions. There’s no product strategy we can see other than acquiring assets with a long tail of reliable subscription revenue. There will definitely be some investment, but exactly how much, we can’t say. However, we would suggest that VMware by Broadcom is unlikely to be an industry pioneer over the next decade.

For many enterprises, some or all of their business will stay with VMware because the cost of transition is too complex or too expensive. However, the mainframe market is a shadow of the size it was in the 1980s. Server virtualisation will be the same in the future. Natural attrition and evolution will eat away at VMware’s revenues. But by the time it matters, Broadcom will have recouped its investment many times over.

Copyright (c) 2007-2023 – Post #3270 – Brookend Ltd, first published on https://www.architecting.it/blog, do not reproduce without permission.