Seagate Technology Holdings PLC has announced financial results for the fourth quarter and full year of FY2024. The data shows a mixed picture, with an annual decline in revenue of 11.3% but a Q4 year-on-year increase of 17.8% and 14% sequentially. Are we seeing a turnaround in the business?

Background

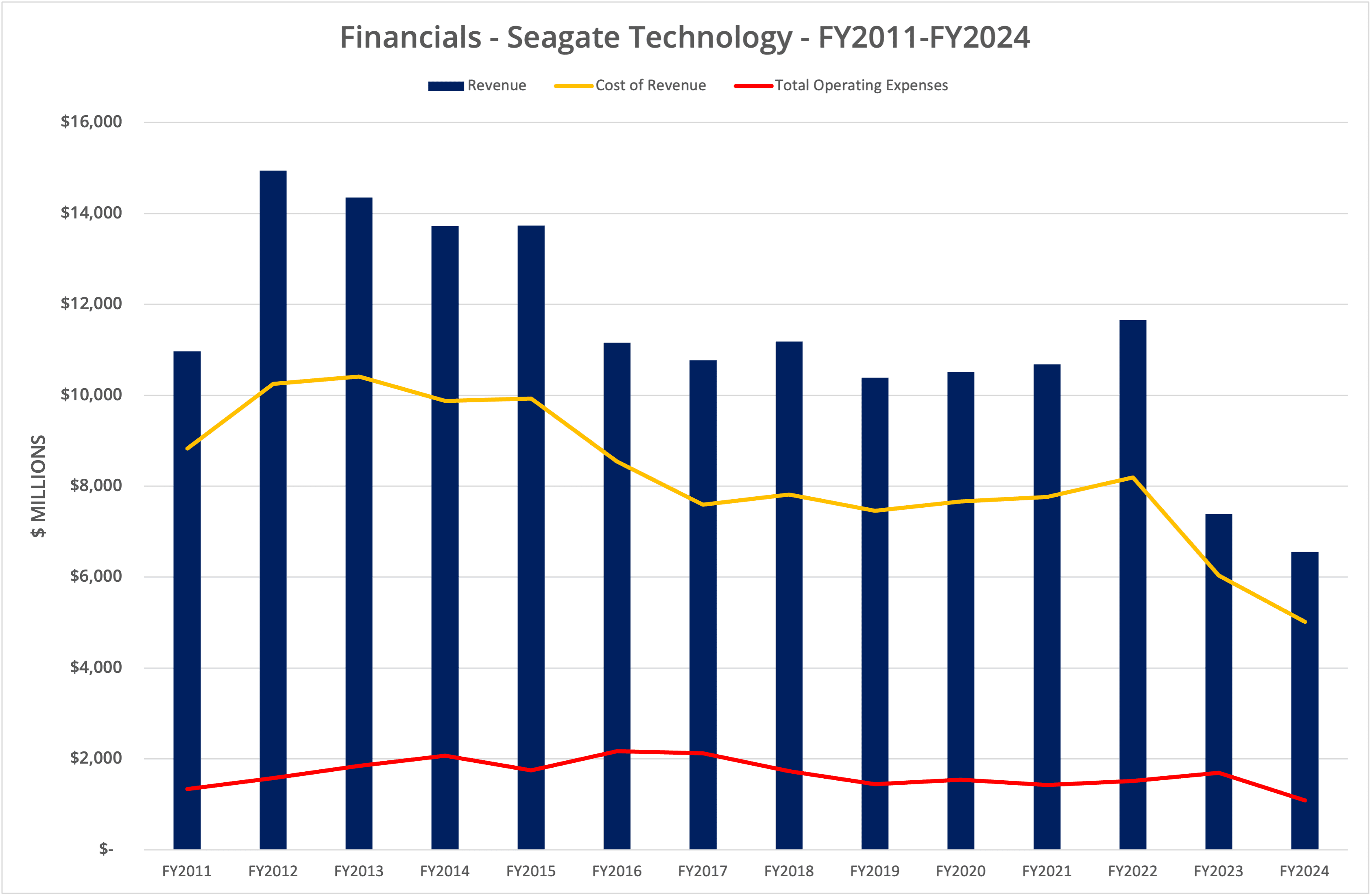

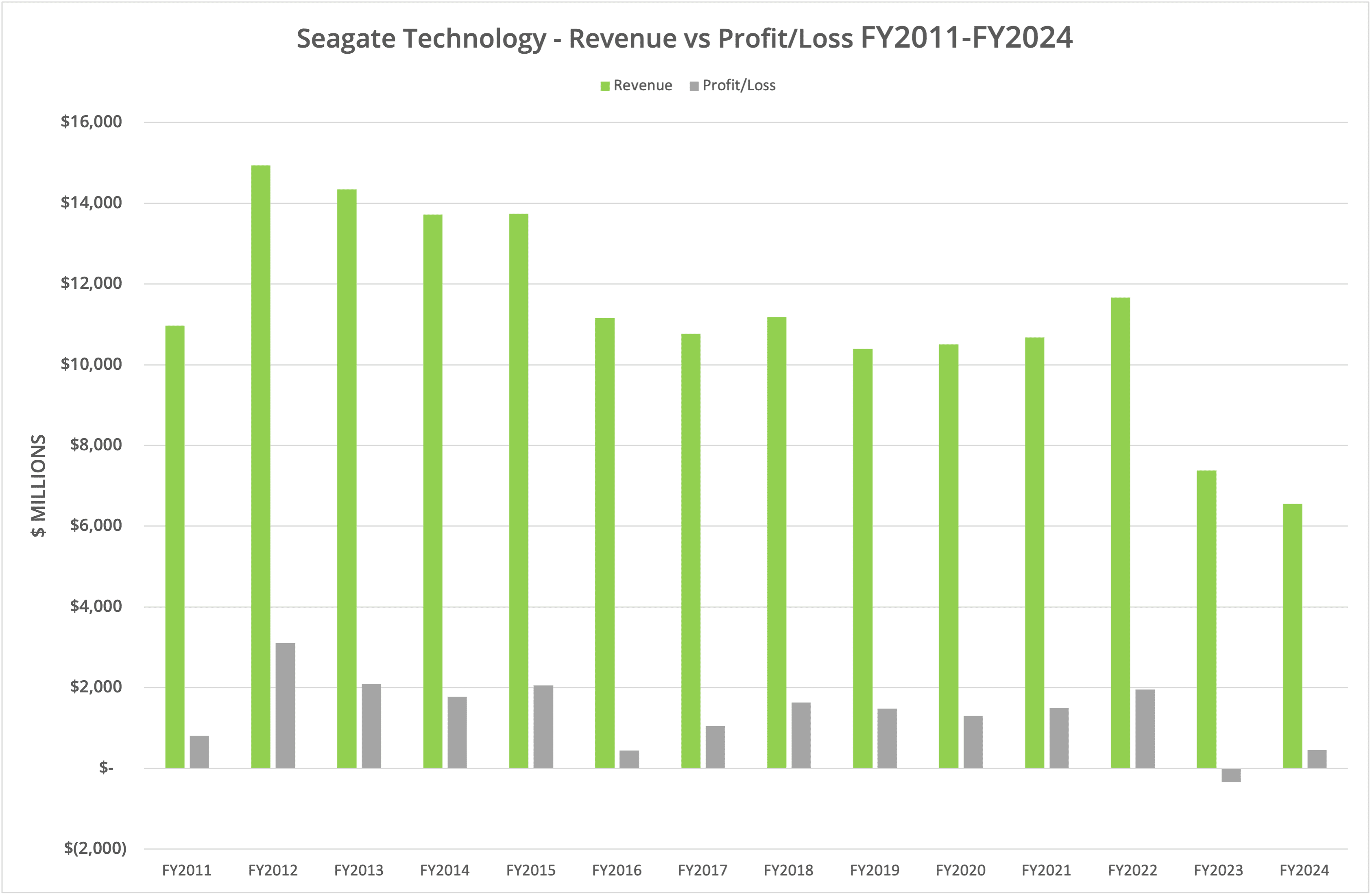

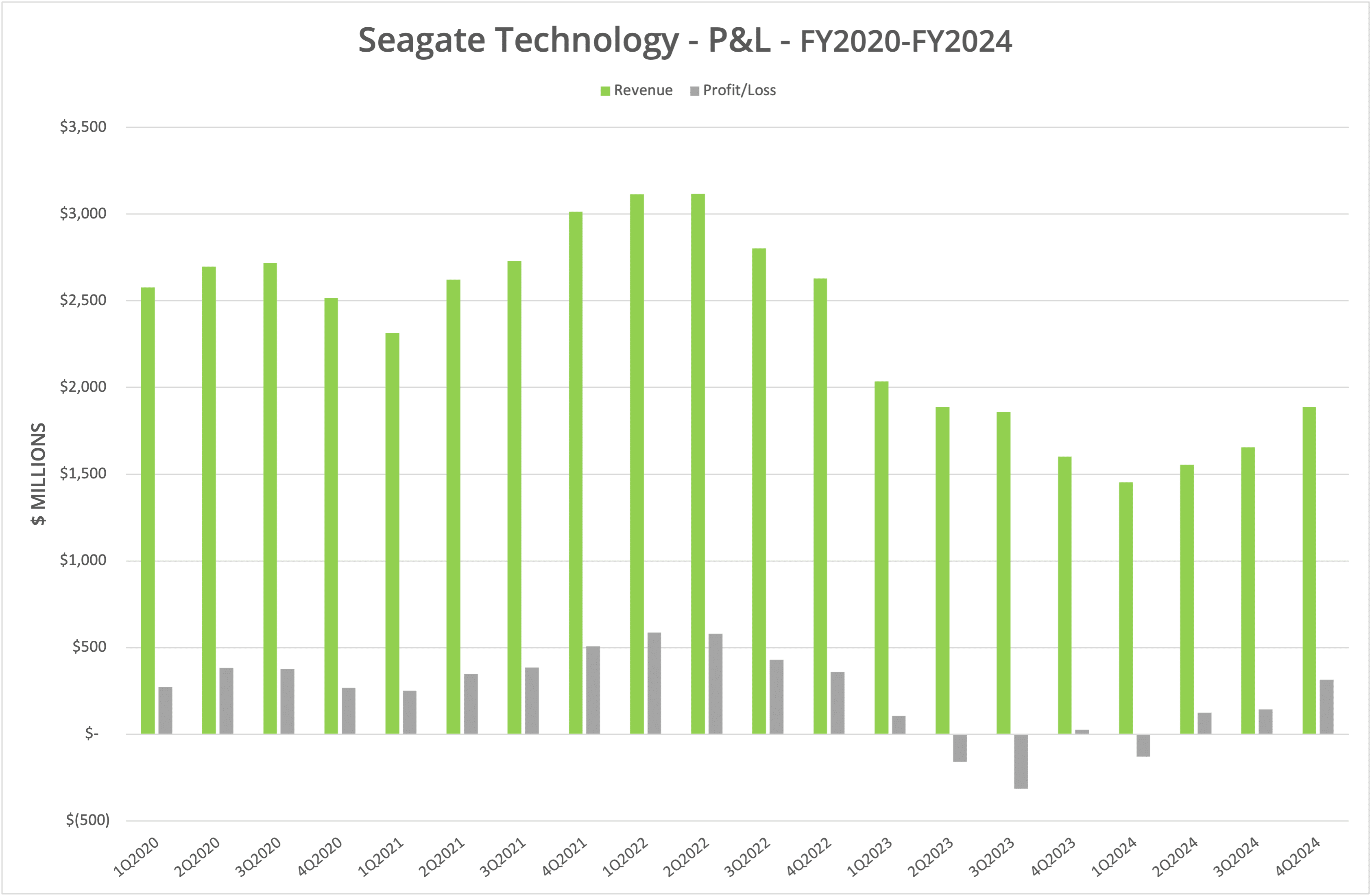

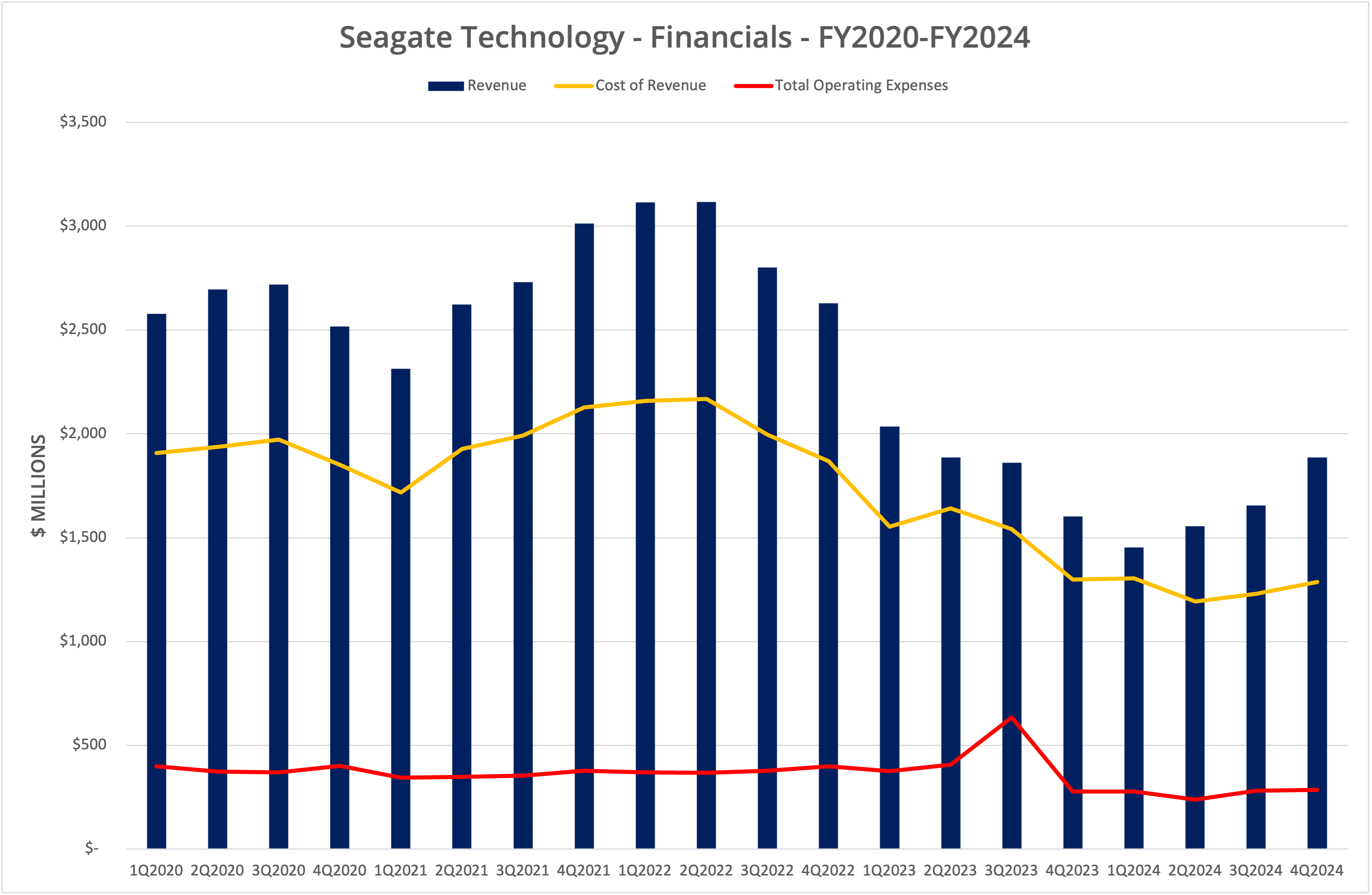

Seagate has announced financial results for Q4 FY2024 and for the full financial year. The data shows revenue declined 11.3% to $6.55 billion compared with FY2023. However, the quarterly data shows an improving picture, with the third consecutive quarter of revenue growth and profit, at $1.89 billion for Q4.

We show the data in seven graphs, labelled Figure 1 to Figure 7.

Turnaround

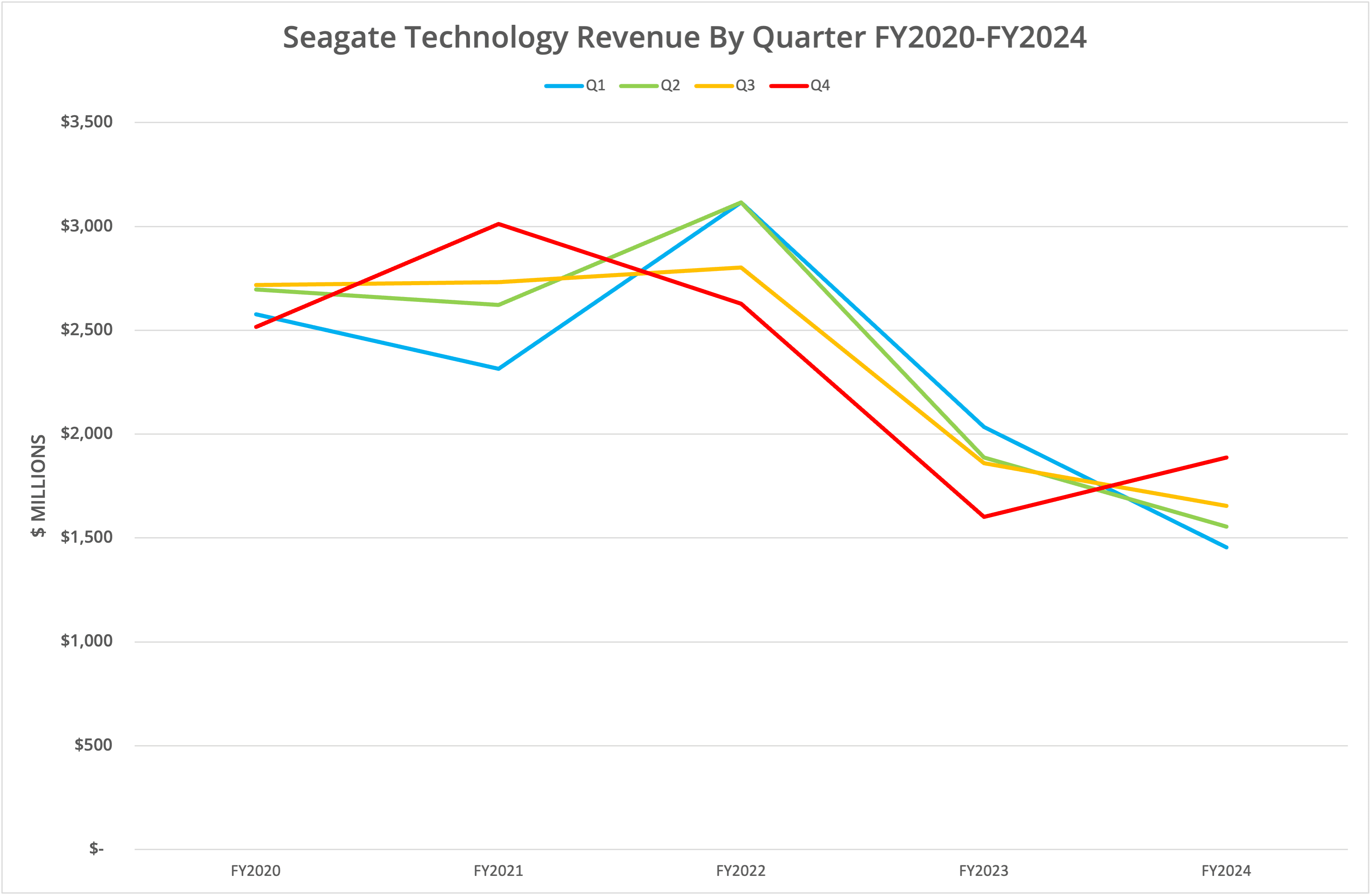

Although annual revenue has declined when compared to the previous period, the quarterly data shows that FY2024 was the extent of the trough (Figures 3 & 4), with a steady return to growth over the course of the financial year. This change is similarly highlighted in Figure 5, which shows the revenue figures by quarter. We can see a clear upturn for Q4 in the current period, compared to the previous one. This transformation follows many periods of decline.

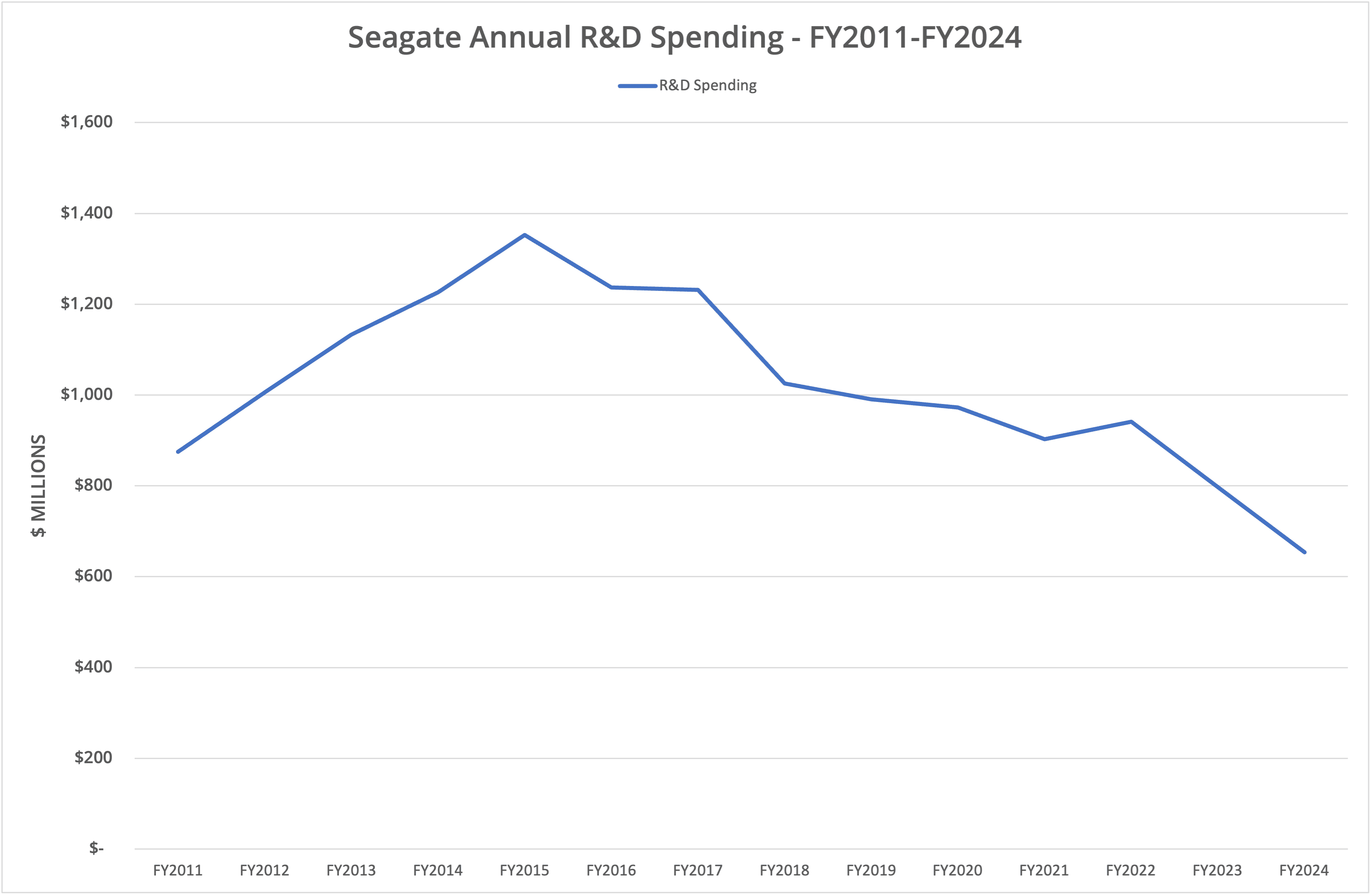

Should we be optimistic about the future of the business? It’s worth noting that during Q4, Seagate sold its system-on-chip business for $600 million, which puts the cash flow in a stronger place. However, R&D spending continues to decline (a 10-year reduction), while HDD exabytes shipped declined by 6.6% compared to FY2023. Again, the quarterly data shows a different story, with a year-on-year improvement in Q4 of 25%.

AI

Seagate attributes the growth in revenue to demand for products in both traditional and AI workloads, although the AI component is, at this stage, probably only a small percentage (see the post-announcement analyst call for details). The long-term focus for the company will be delivering mass capacity drives based on HAMR technology and Mozaic (3+ products later this year and higher capacity drives after that). Demand is expected to come from on-premises customers using HDD platforms to store inactive AI data. In reality, though, the majority of demand is driven by Cloud Service Providers, with a major vendor due to qualify Mozaic 3 devices in September 2024.

The Architect’s View®

Seagate continues to be highly dependent on the hard disk market. In the fourth quarter of FY2024, HDD revenue represented 91.5% compared to 87.6% in the period Q3 FY2024. As we reported in Q2 FY2024, HAMR drives will increase revenue as the replacement cycle for HDDs continues. Does this market have a long-term future?

In June 2024, Western Digital detailed its view of the NAND market and how the evolution of products is likely to transition. The company view suggests that the “layer wars” are over, with a move to more focus on a diversity of solutions to meet customer needs. We see this translating into new products (such as 128TB SSDs) that further erode the active workload use cases of HDDs.

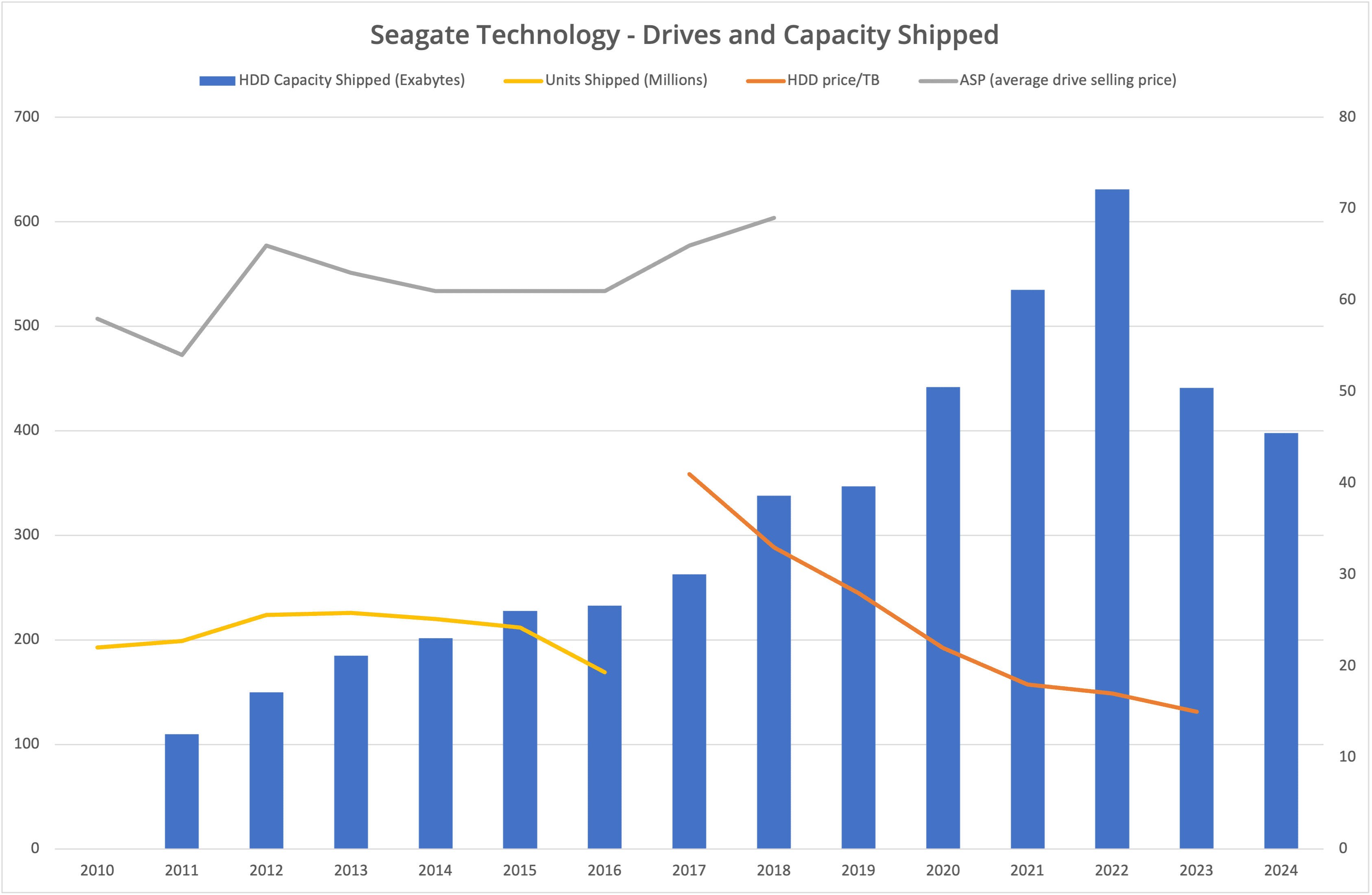

So, Seagate’s future business is dependent on successfully shipping Mozaic HAMR-based drives of 30+TB capacities. The bill of materials for 40/50TB drives is similar to those for the current 30TB drives. Therefore, units shipped (rather than exabytes) is a better measure of expected revenue. From the data we were able to find, Seagate stopped explicitly publishing units shipped in 2016. However, the latest annual results show 398 exabytes of capacity shipped with an average (in Q4) of 9.3TB per drive. That equates to around 43 million units shipped in FY2024, compared to 169 million in FY2016 (the last data we have). Of course, this is a rough estimate, not hard data.

Are we about to see significant growth in HDDs shipped? Evidence from analysts tracking the market implies that shipments continue to decline, although freely published data is approximately six months out of date.

We continue to believe the HDD market is in long-term decline. The NAND flash manufacturers will continue to build solutions for a wider breadth of use cases, pushing HDDs further into the margin of archive. The only justification for using hard disks over tape (or other media) will be for better random access over the sequential nature of tape, although with usage limits now also applied to HDDs, that difference continues to erode.

Over the next decade, we expect the number of HDD manufacturers to consolidate from three to two, perhaps eventually to just one. Research and Development spending for HDDs is declining. As a result, we envisage the development of new technologies in a post-HAMR world to be limited because the financial justification for the return on capital investment will be much lower.

Seagate lives in a cyclical business that just happens to be on an up-cycle. However, the long-term trend is definitely downwards for the foreseeable future, unless the business pivots to alternative technology.

X-Ray: Seagate Technology PLC

This Architecting IT report takes a deep dive into Seagate’s history, products, services, and future outlook. This report is only available for download via paid subscription.

Copyright (c) 2007-2024 – Post #49DC – Brookend Limited, first published on https://www.architecting.it/blog, do not reproduce without permission.