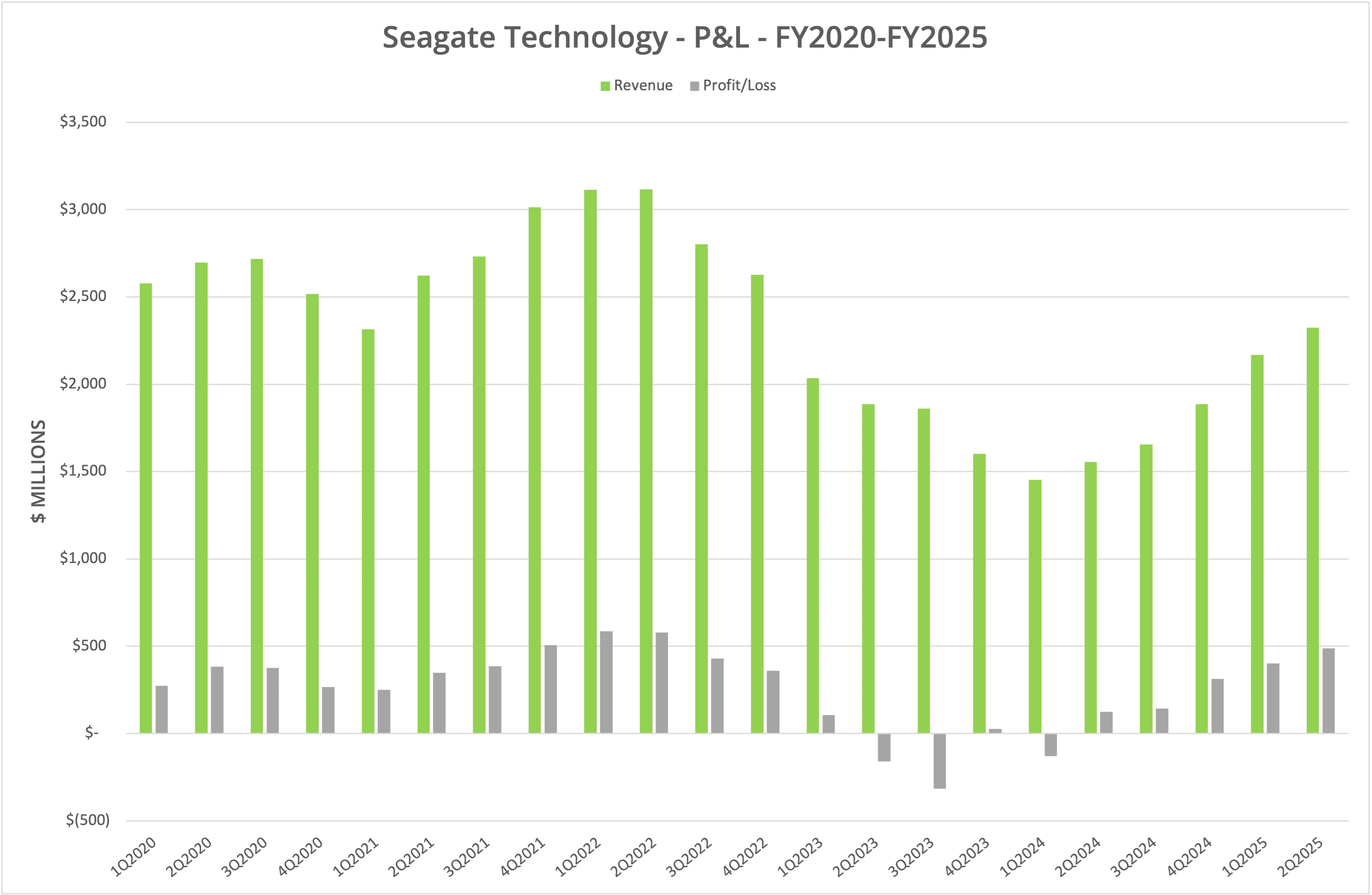

Seagate Technology Holdings PLC has announced financial results for the second quarter of FY2025, ending 27th December 2024. The data shows revenue of $2.325 billion for the quarter, up 49.5% year-on-year and 7.2% sequentially. Once again, business is up, but do the shipping numbers continue to indicate a change in the market?

Background

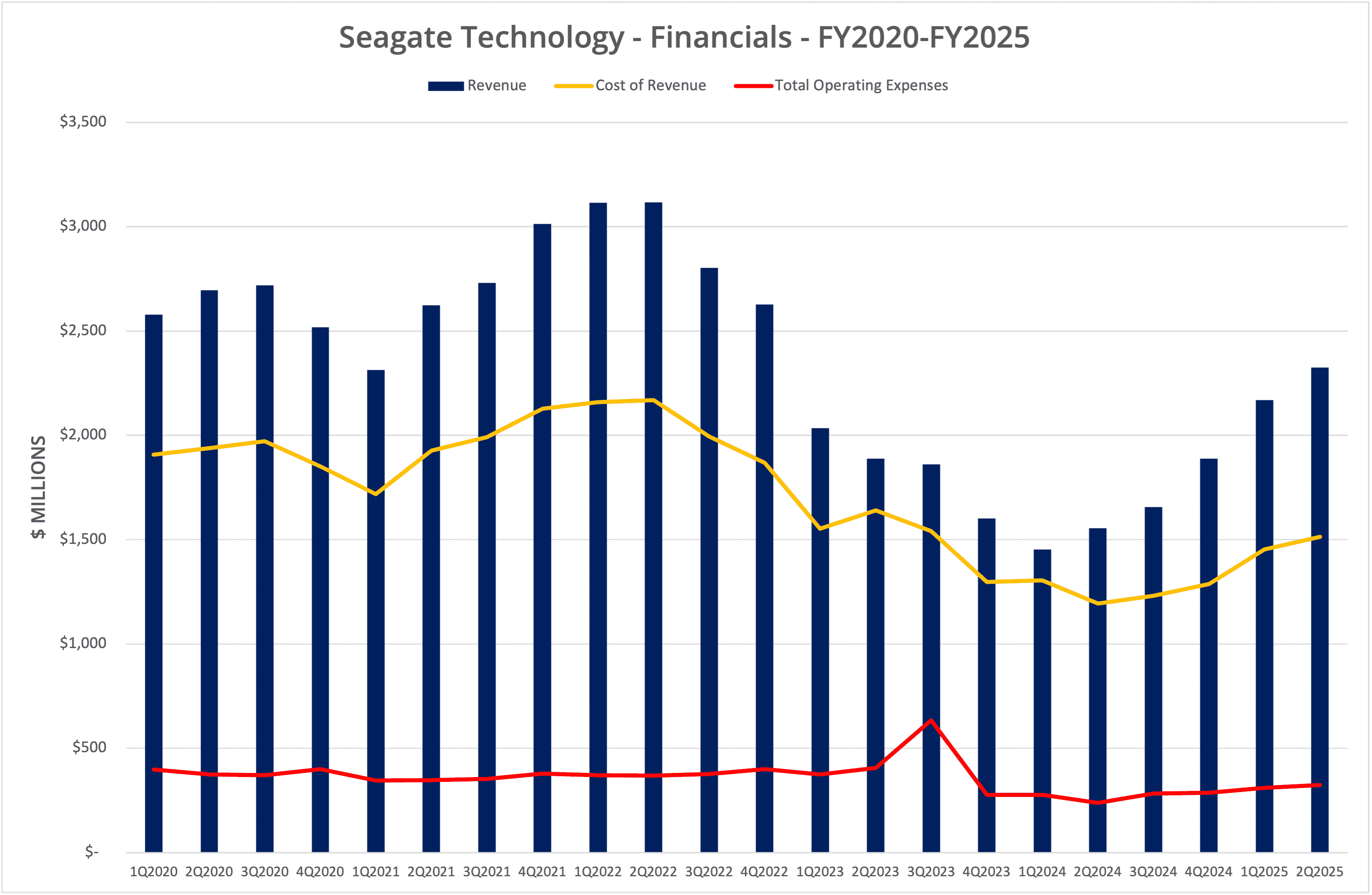

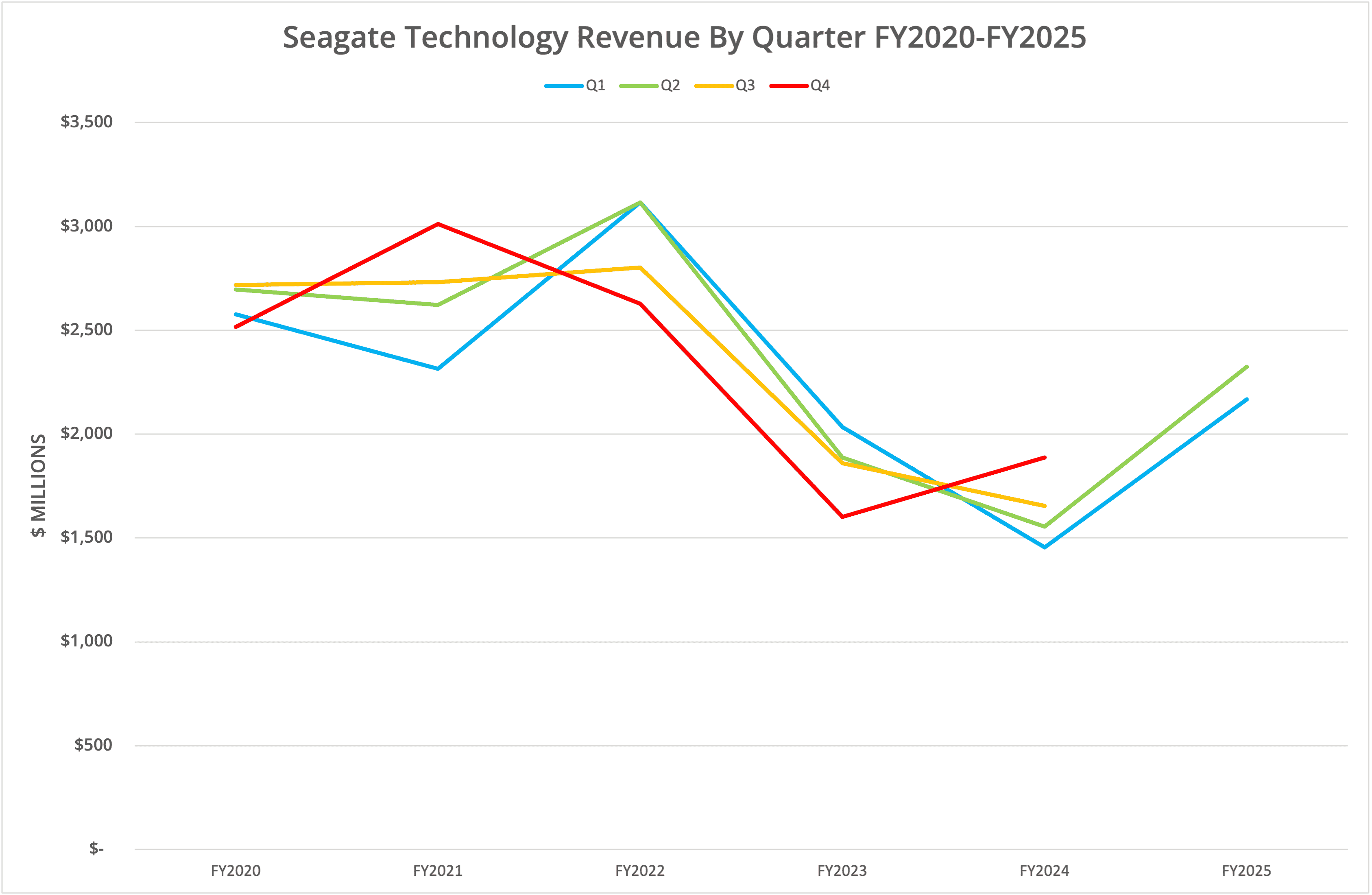

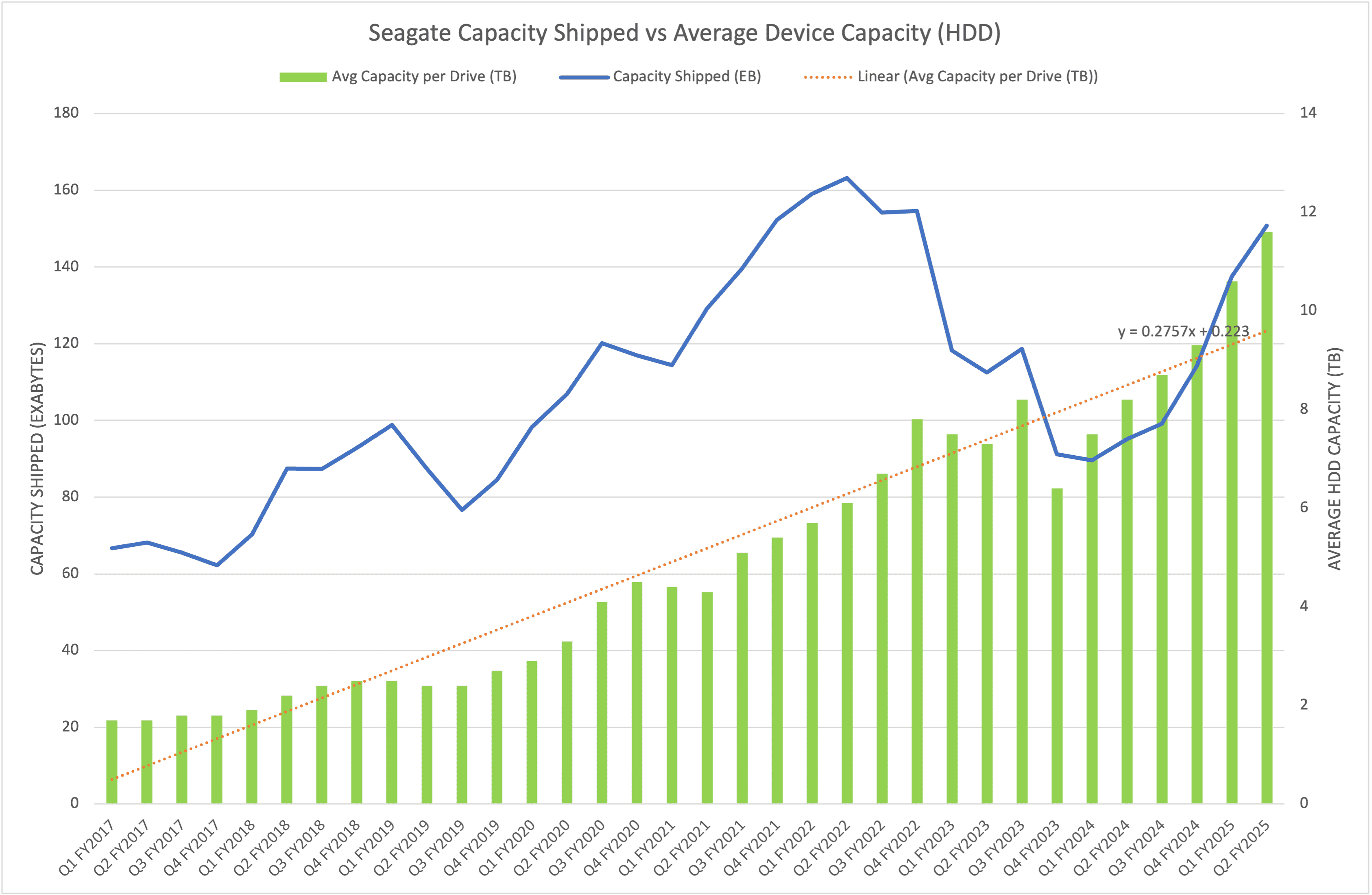

Seagate Technology Holdings PLC has published financial data for the period Q2 FY2025, which ended on 27th December 2024. Revenue for the period was $2.325 billion, up 49.5% compared to Q2 FY2024. This is the second consecutive quarter with close to 50% year-on-year growth. Sequentially, growth was 7.2% compared to Q1 FY2025. Gross margin increased slightly to 35%. We show the data in six graphs, labelled Figures 1 to 6.

Metrics

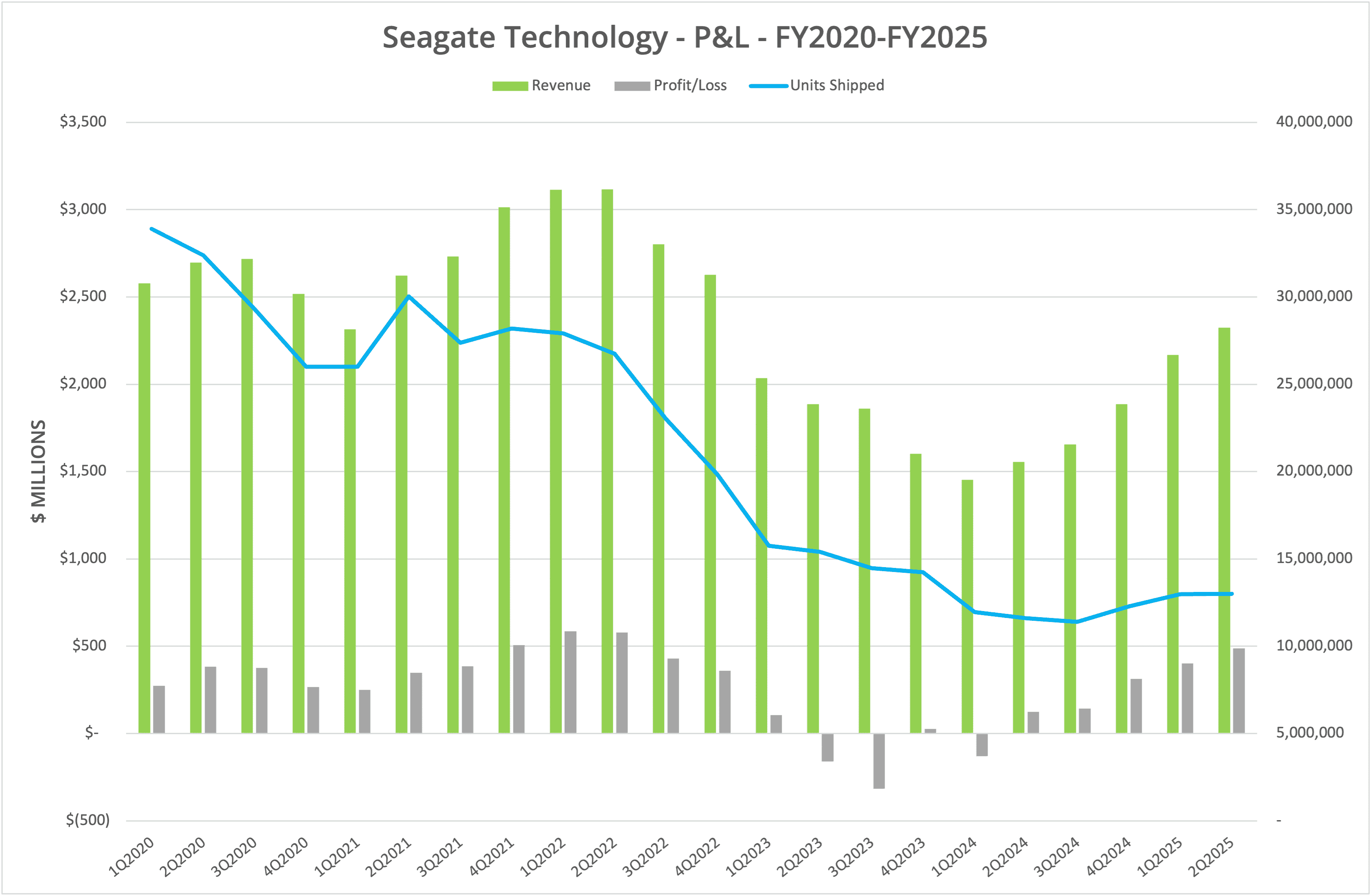

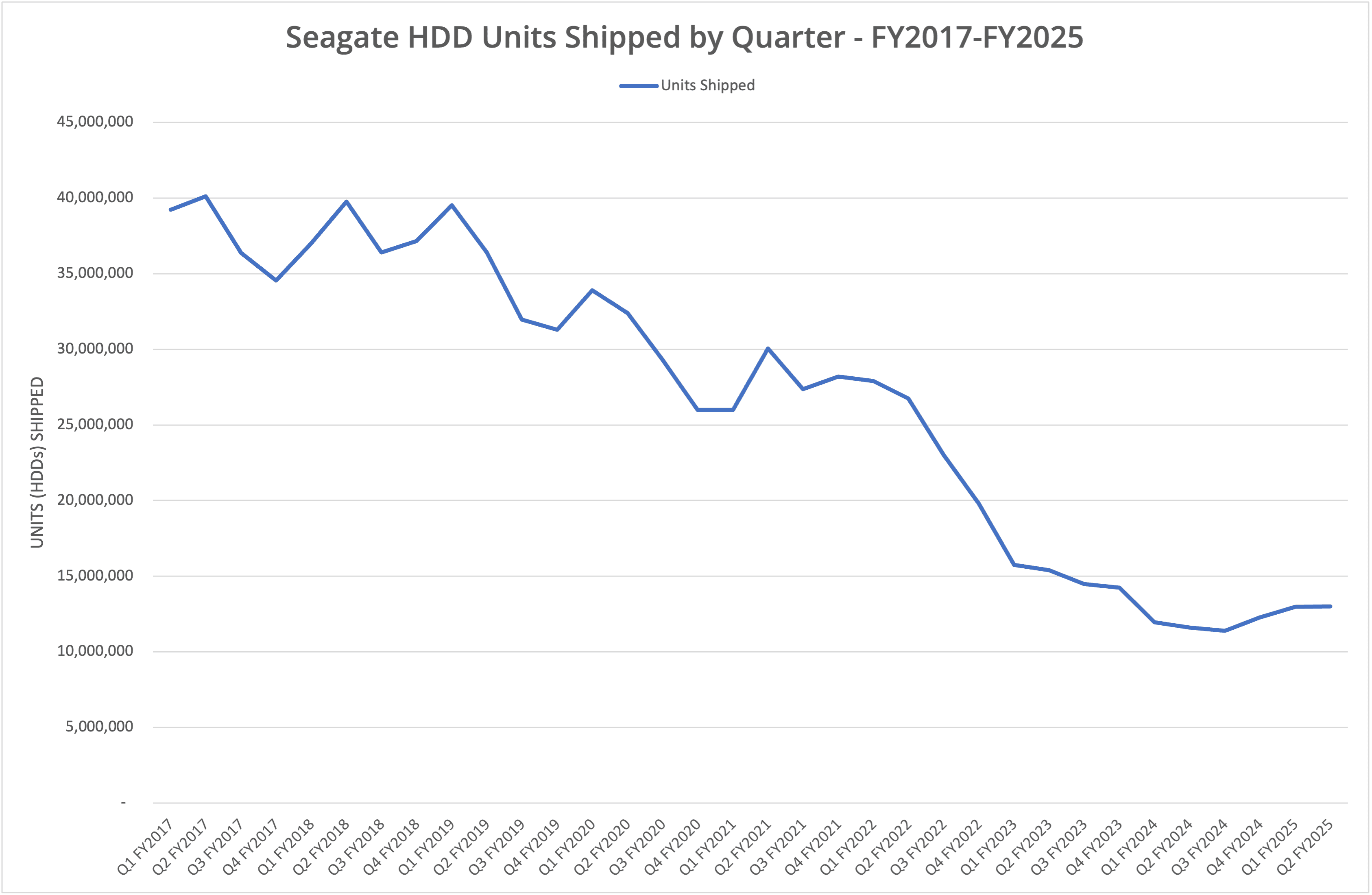

As we highlighted in our last reporting, Seagate is not seeing a massive upswing in HDD units shipped. Instead, as shown in Figure 2, the improvement in revenue is being achieved from higher-priced and higher-capacity drives. The average drive capacity shipped during the quarter was 11.6TB (up from 8.2TB a year previously).

HAMR

The rise in average capacity per unit shipped can be attributed, in part, to the introduction of HAMR technology and the Mozaic architecture we discussed this time last year (see here). A year on from that announcement, Seagate has 36TB drives based on the Mozaic3+ technology, currently in sampling with customers. These HDDs are expected to made available to customers in the second half of 2025.

According to the Seagate press release accompanying the announcement of 36TB drives, the Mozaic architecture has reached densities of 6TB per platter in lab conditions, essentially a 60TB drive when built with 10 platters.

Mass Capacity

Seagate clearly sees the future of the hard disk as an archive device with a focus on mass capacity products. In the earnings call following the financials announcement, CEO David Mosley highlighted hard drives “serving as central repositories when these data sets are not actively being processed by GPUs”, referring to data used to train AI models. He also indicated a 6x difference in pricing per TB between NAND and HDD, which is expected to remain unchanged for the foreseeable future.

It has been evident for some time that the future of hard drives is the archive market, a topic we discussed some eight years ago. Increasing capacity also means decreasing I/O density, with fewer IOPS available per TB of capacity. A Seagate EXOS X24 24TB drive, for example, will take 24 hours to write completely at full speed. Higher capacity drives will take even longer, as the throughput is a factor of the increase in areal density, roughly the square root of the increase in capacity (at best).

Competition

In the near term, solid-state disks are unlikely to fully replace the HDD, but instead continue to make inroads into specific application use cases. SSDs are used for all high-performance applications, with higher capacity drives now being positioned to meet read-intensive workload needs.

Vendors such as Solidigm have announced 122TB SSDs in U.2 format (around ¼ the volume of a 3.5” drive and one third the weight) with competitive power utilisation (the Solidigm D5-P5336 consumes between 25-5W, the EXOS X24 between 6.5-9.8W).

Where recent HDD capacity improvements have been frequent and incremental, SSD capacities have typically doubled over longer time periods. We first reported on 30TB solid-state disks in 2018 (link), with another five years before 61TB drives arrived (link). Around 18 months later we have 122TB drives (link), with the growth in SSDs expected to continue – subject to demand, of course.

For every year capacities increase, the SSD market will displace more hard drives in scenarios where it makes more commercial and technical sense to move over to solid-state technology.

The Architect’s View®

Seagate is gaining good improvements in revenue from the renewed demand for HDDs, driven by secondary data requirements. Crucially, the units shipped per quarter may have plateaued, as the hyper-scaler refresh cycle declines. We will need to see what Q3 figures bring.

Elsewhere, the business in systems and SSDs continues to decline in revenue, now representing (in total) only 6.7% of sales for Q2 FY2025. Seagate does not provide specific details on the non-HDD revenue breakdown, so we can only speculate that the SSD and Lyve businesses aren’t gaining much interest from customers.

This position must be a worry. Seagate is “all in” on hard drives, and if that market falters, so does Seagate itself.

Copyright (c) 2007-2024 – Post #3edc – Brookend Ltd, first published on https://www.architecting.it/blog, do not reproduce without permission.