Nutanix, Inc. has announced financial results for the second quarter of FY2025, which show revenue up by 19% to $654.7 million compared to the same period last year. Gross margin increased slightly to 87%, with a profit of $65.4 million. The numbers look good as on-premises virtualisation continues to evolve.

Background

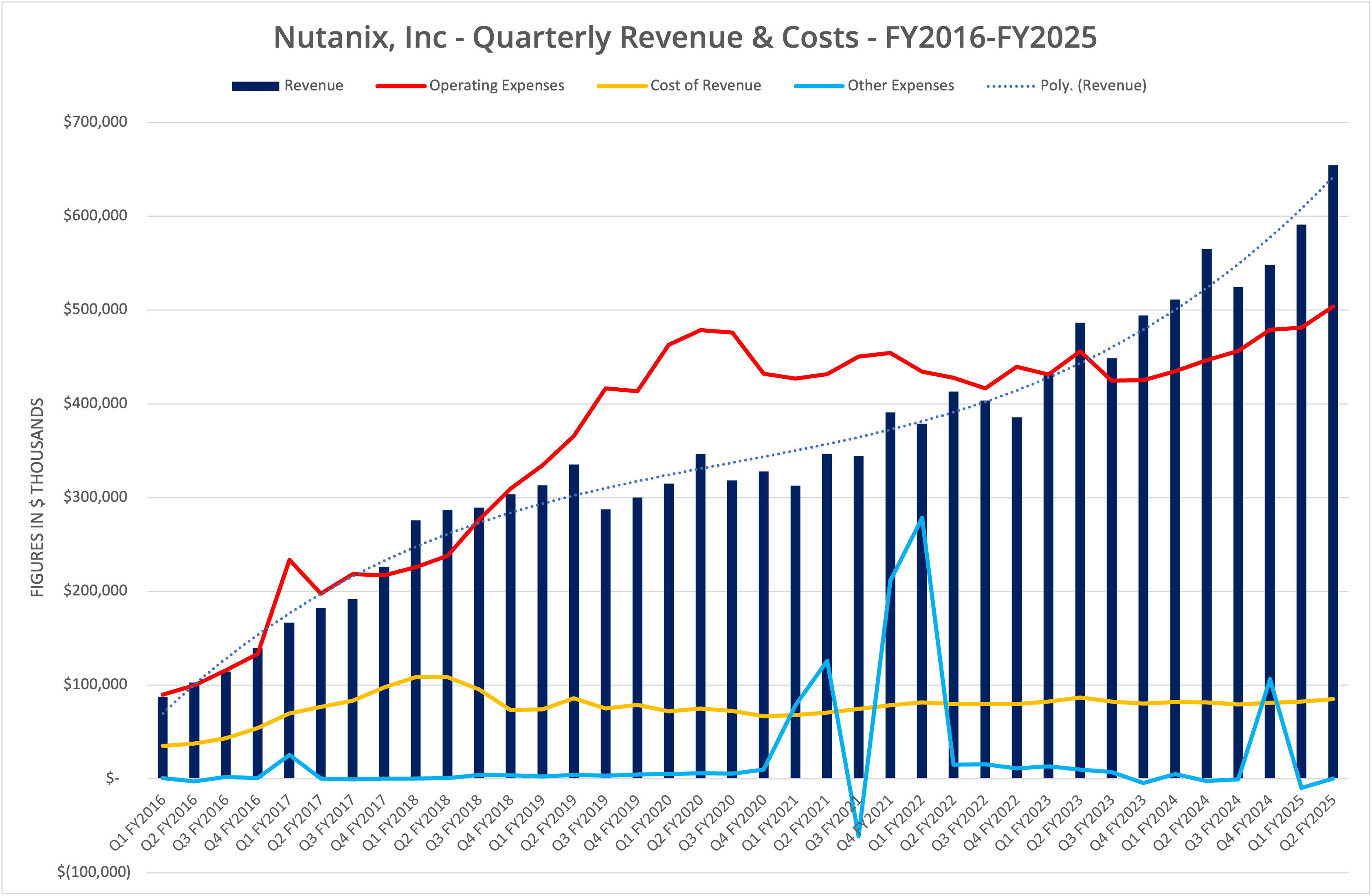

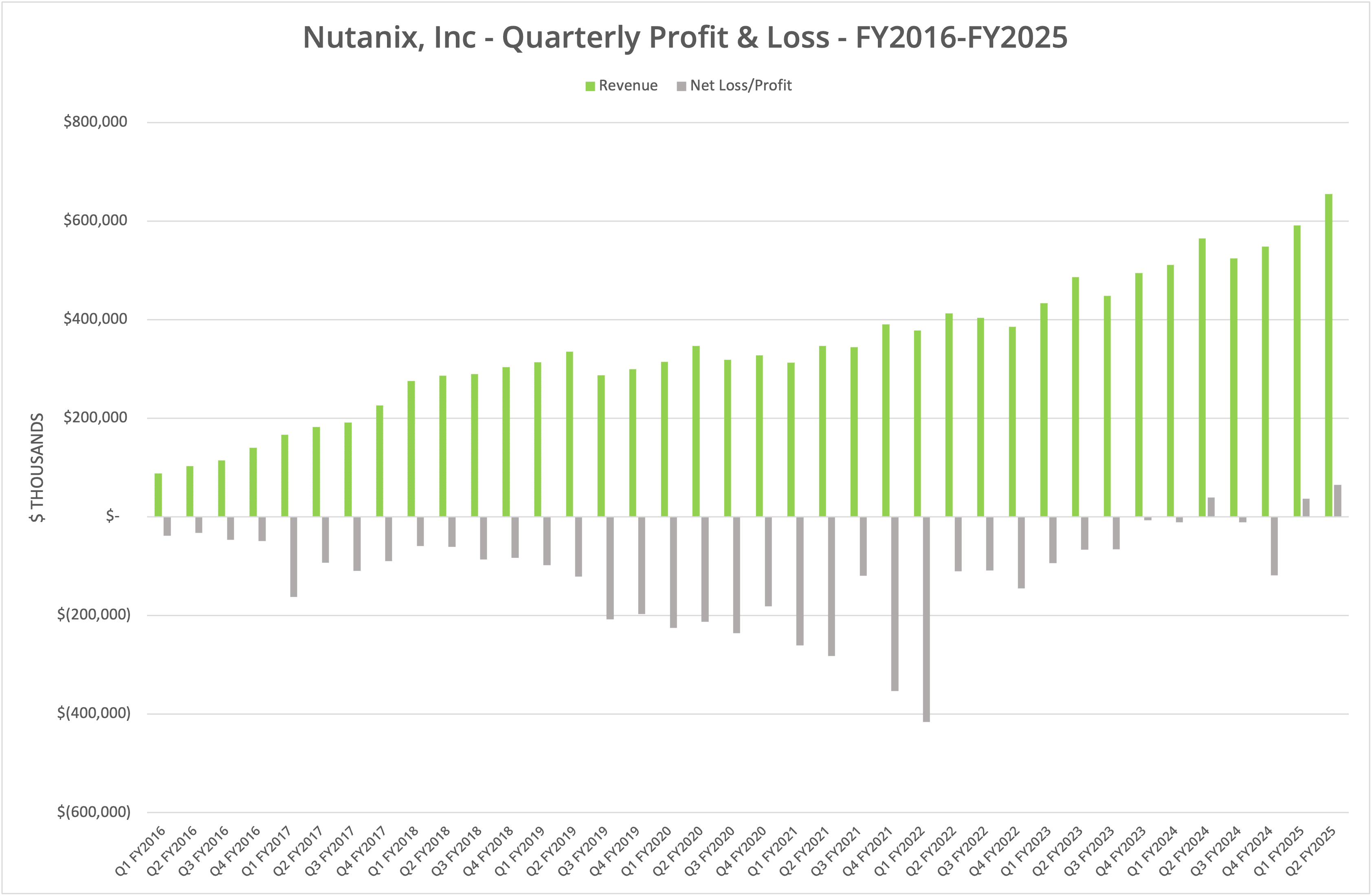

Nutanix, Inc. published financial results for Q2 FY2025 (the period ending 31 January 2025) on 26 February 2025. Revenue for the period was $654.7 million, up 19% year-on-year compared to the same period in FY2024 and 10.8% sequentially. Net profit increased 76.6% to $65.4 million compared to Q2 FY2024. We present the data in five graphs labelled Figures 1 to 5.

Growth

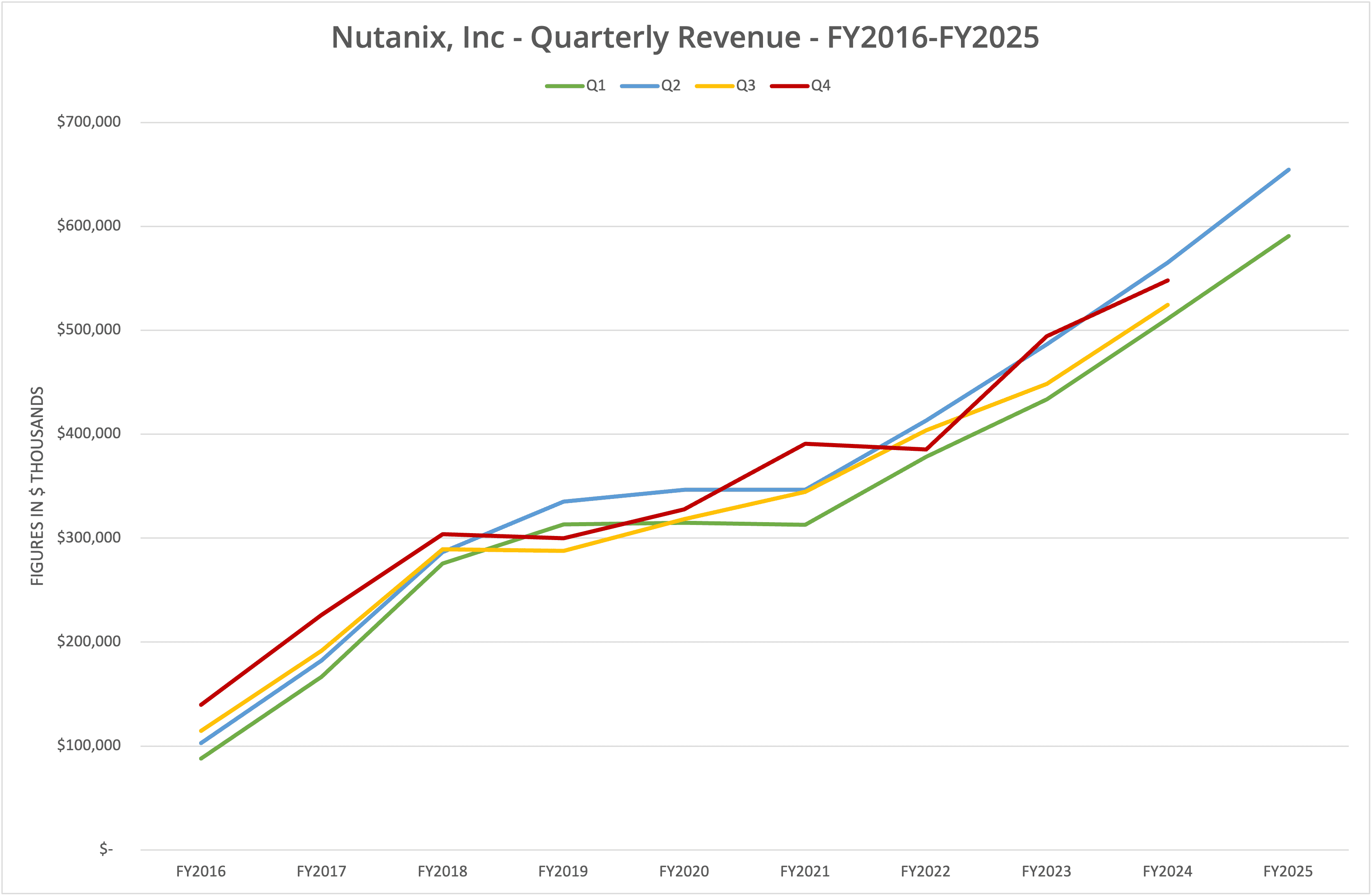

The current story of Nutanix is one of consistent revenue growth. As shown in Figure 1, the rise in revenue has been remarkably consistent over the last five years, after flattening slightly during the COVID-19 period. Nutanix now quotes an ARR (annual recurring revenue) figure of just over $2 billion.

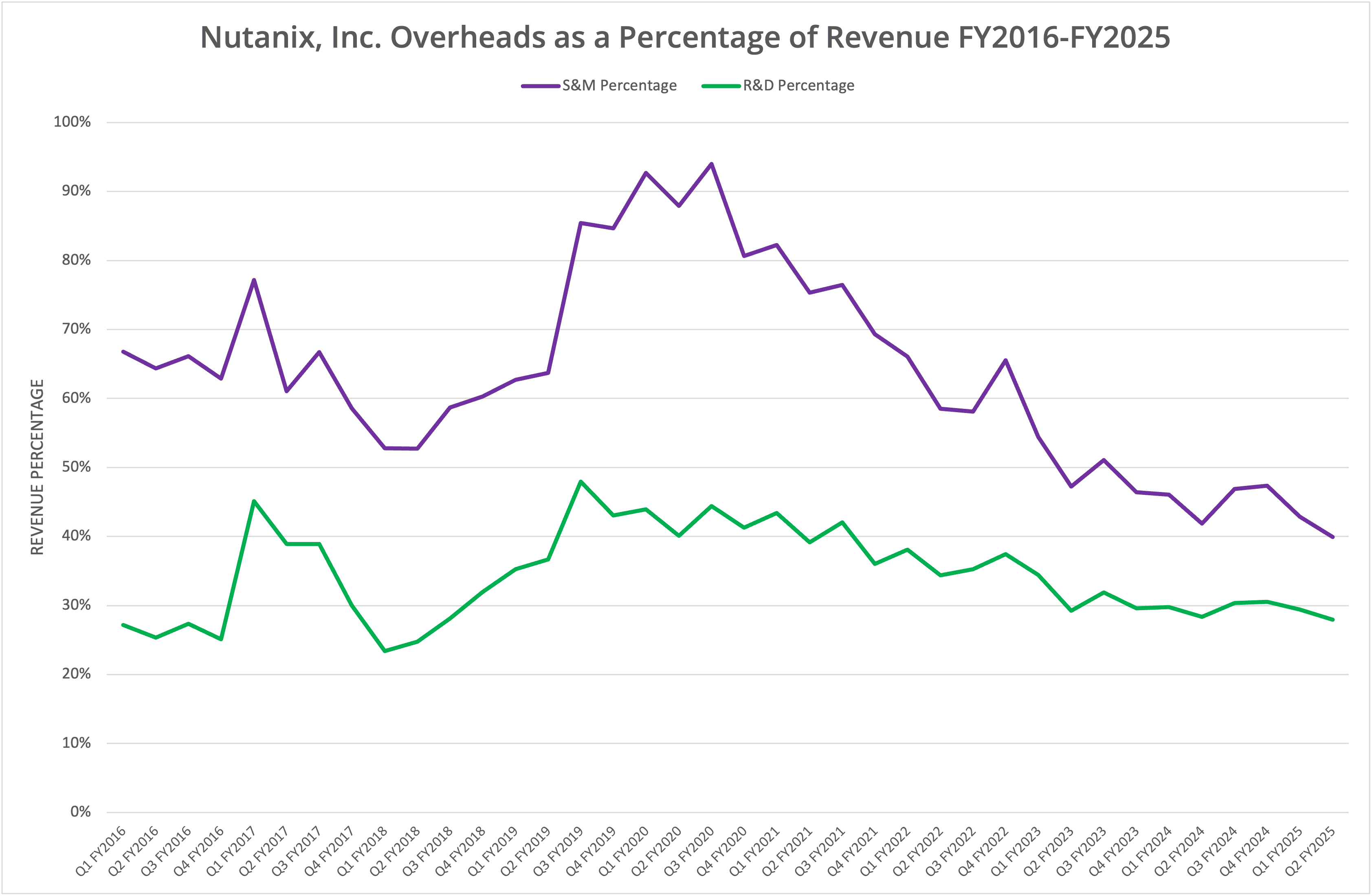

Selling virtualisation is an expensive business. Sales and Marketing overhead is well over $1 billion annually, running at 40% of revenue and 46% of gross margin in the current quarter. However, that said, Nutanix is managing to make a small profit more frequently than it did in the past.

VMware

We might assume that there has been a flight away from VMware, from which Nutanix is benefiting. Determining that will get more difficult in the future, as Broadcom has announced VMware will not be reported separately in financial data, but instead, the figures will be integrated into the software business.

“As we are now past one year following the close of the VMware acquisition starting in Q1 of fiscal 2025, we will no longer break out VMware revenue and costs on a stand-alone basis.” (Kirsten Spears, Broadcom CFO & CAO, Q4 FY2024 Earnings Call)

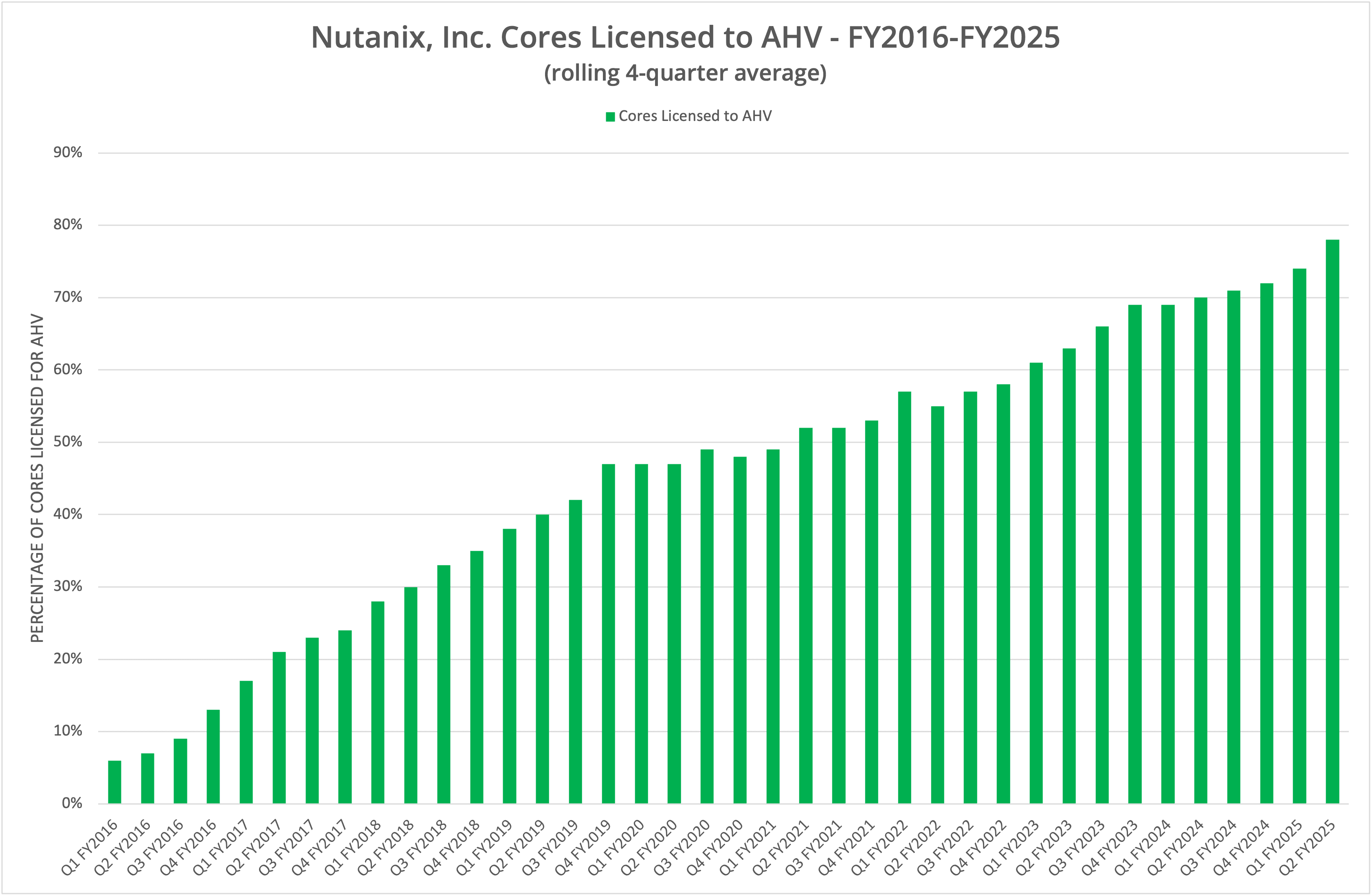

Undoubtedly, Nutanix has gained VMware customers. The data showing CPU cores (Figure 5) using AHV continues to trend towards 100%, now at 78% in the current period. That mix must include customers leaving VMware and wishing to move away from licensing VMware on Nutanix. Reaching 100% would be quite an achievement, but perhaps the gains are better explained by the undesirable rise in VMware licensing costs, which are obviously the main reason for customers to move to Nutanix (from VMware).

We believe that there could also be other factors (the current US administration) affecting the current take-up of on-premises server virtualisation. On-premises infrastructure offers more security than the public cloud, while providing greater control over costs. This positioning isn’t about moving away from the public cloud, but more about “rightsizing” infrastructure and costs while managing risk.

The Architect’s View®

While Nutanix looks to be doing well, so are other server virtualisation vendors, such as VergeIO, which reported record customer growth and ARR in February 2025. In our opinion, Nutanix needs to continue with innovation while making the transition for new customers as seamless as possible.

Part of this opportunity could be to focus on SaaS-based management of on-premises infrastructure. This is an area that UK-based SoftIron Ltd has successfully developed. A SaaS portal provides the capability to integrate more advanced reporting and to continuously update the management software without requiring server upgrades. It also reduces the burden on the hardware purchased specifically to deliver server virtualisation.

A second area of focus should be accommodating shared storage. This is a tricky area for hypervisor vendors, as part of the key tenets of the platform (certainly in the early days) was the ability to eliminate the cost overhead of shared storage and move to a simpler server & storage model.

Naturally the biggest question to ask is whether Nutanix can maintain momentum and for how long. We believe the answer is to ask whether VMware will revamp its licensing stance or whether the company will continue to focus on high value customers.

Currently, Nutanix earns around $71,000 per customer per year. One year ago, that figure was $68,500, while two years ago it was $58,400. The revenue per customer is certainly increasing. However, those figures represent perhaps $300-$1000 per core, depending on the features chosen. So, the average customer still only operates a small to medium sized environment. This could indicate Nutanix has room for growth, but that business is also being chased by Proxmox, VergeIO, NodeWeaver, Scale Computing and others.

We believe the prospects for Nutanix are good for the next 18-24 months, by which time existing VMware customers will have re-evaluated options and reach the end of existing 3-year licensing terms. At that point, the impact on Nutanix will be interesting to watch.

Copyright (c) 2007-2025 – Post #9ac3 – Brookend Limited, first published on https://www.architecting.it/blog, do not reproduce without permission.