HPE, Inc. has declared financial results for Q1 FY2025, ending 31 January 2025. Overall revenue is up 16.3% year-on-year at $7.9 billion, driven by a 28% increase in server sales. Networking fared less well, down 4.6%, while Hybrid Cloud grew by 12.6%. The data shows a mixed picture with a poor outlook forecasted. Is the AI server hype peaking, and if so, what does it mean for HPE’s business?

Background

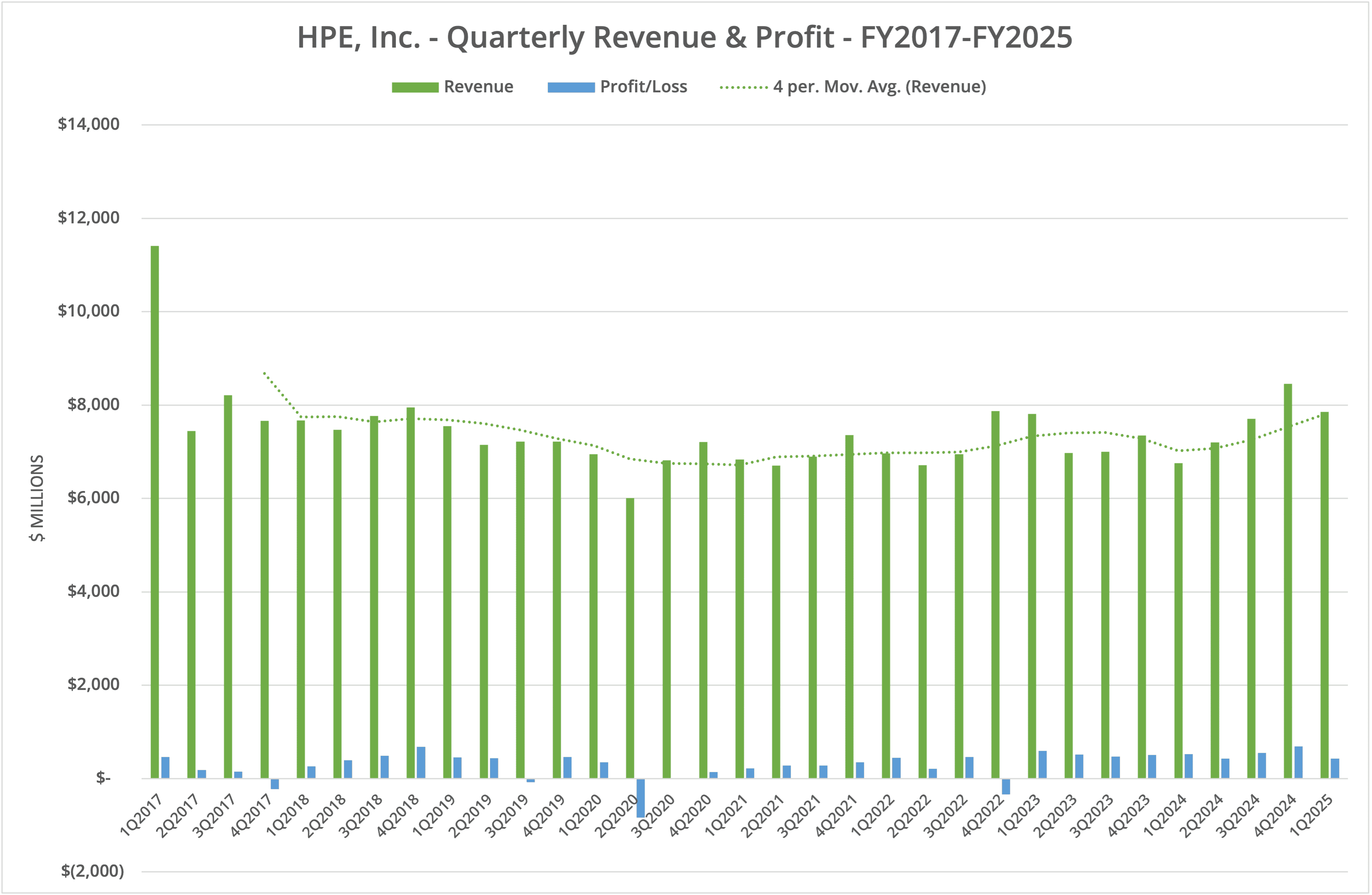

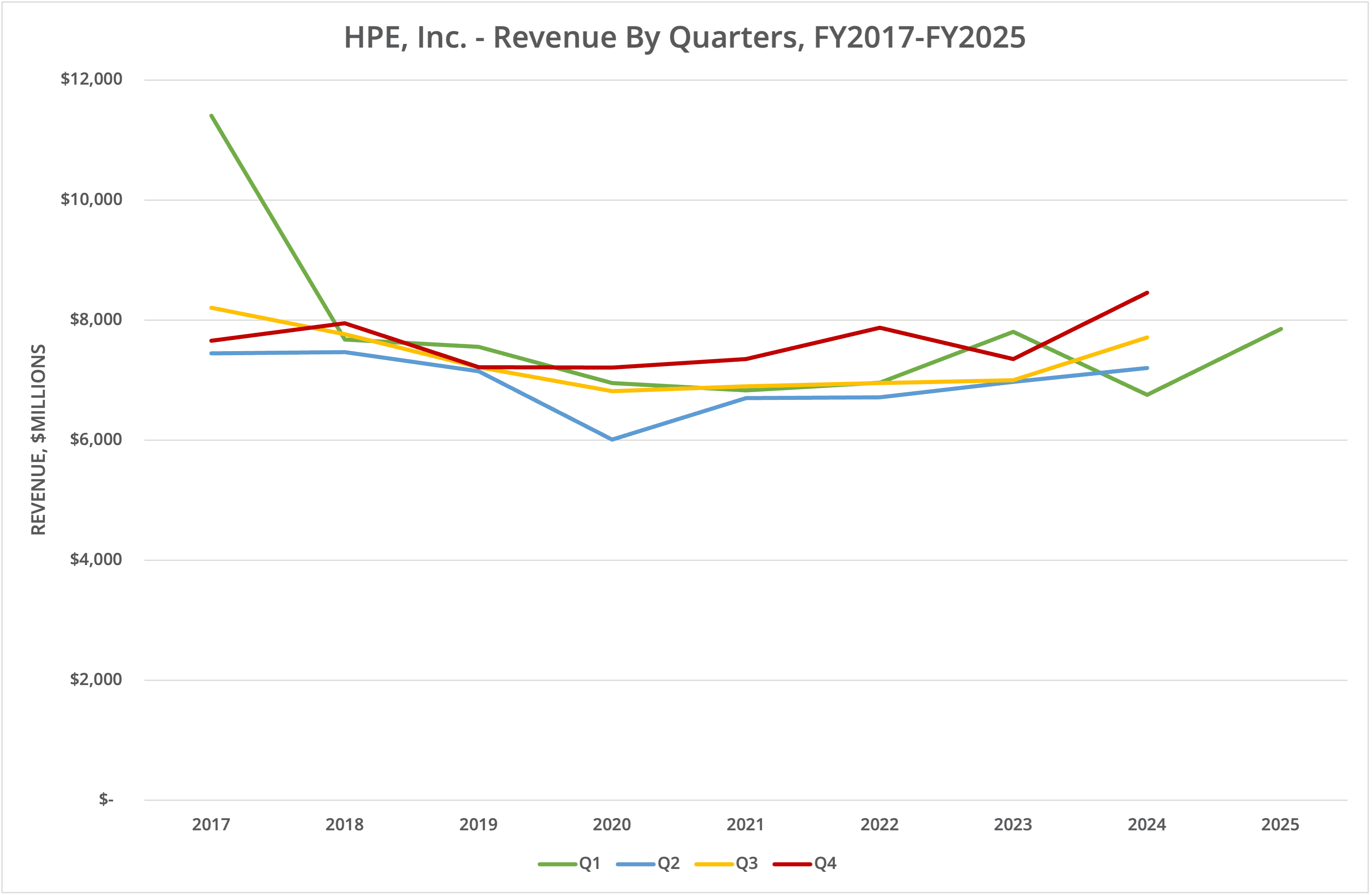

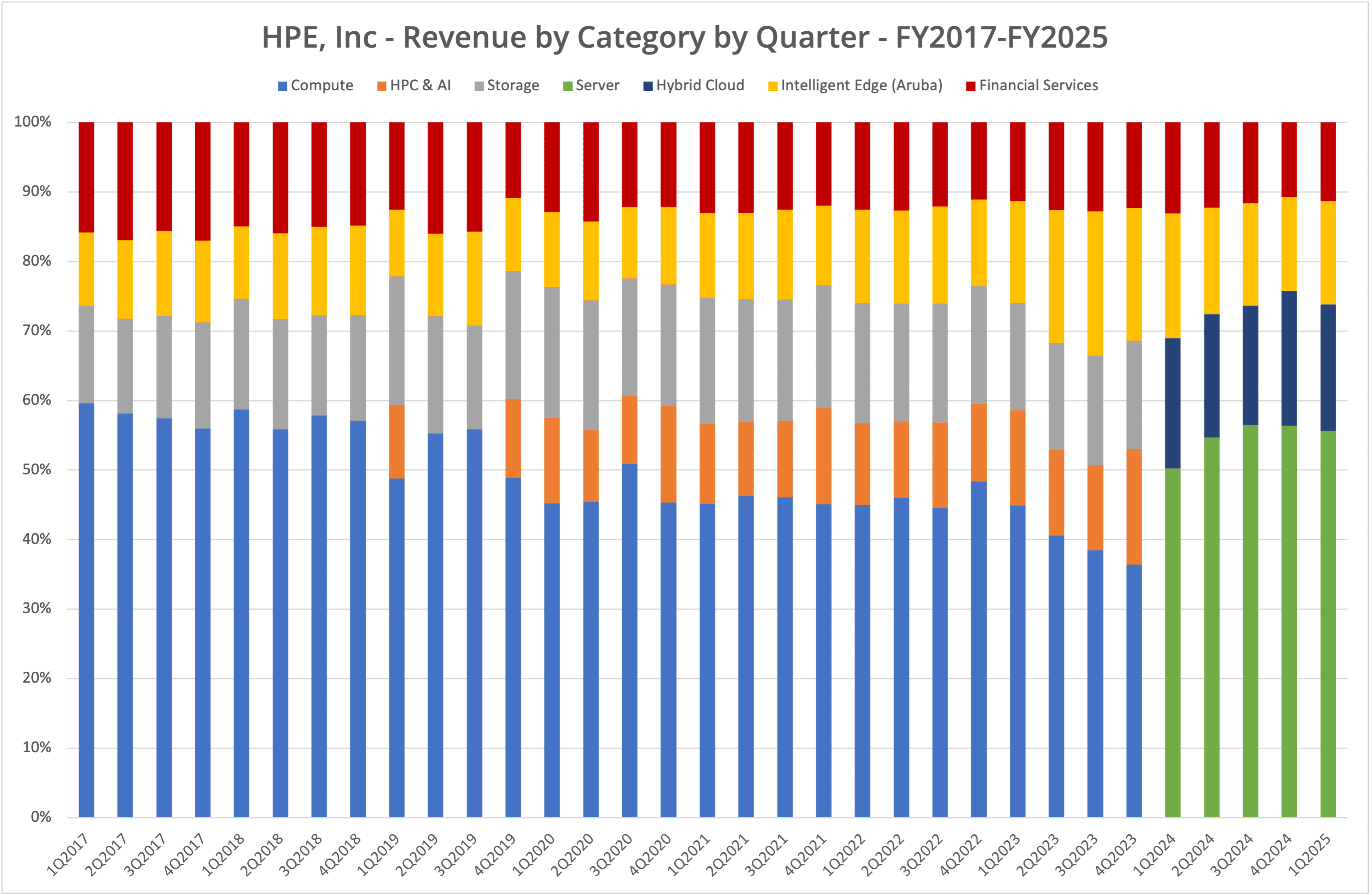

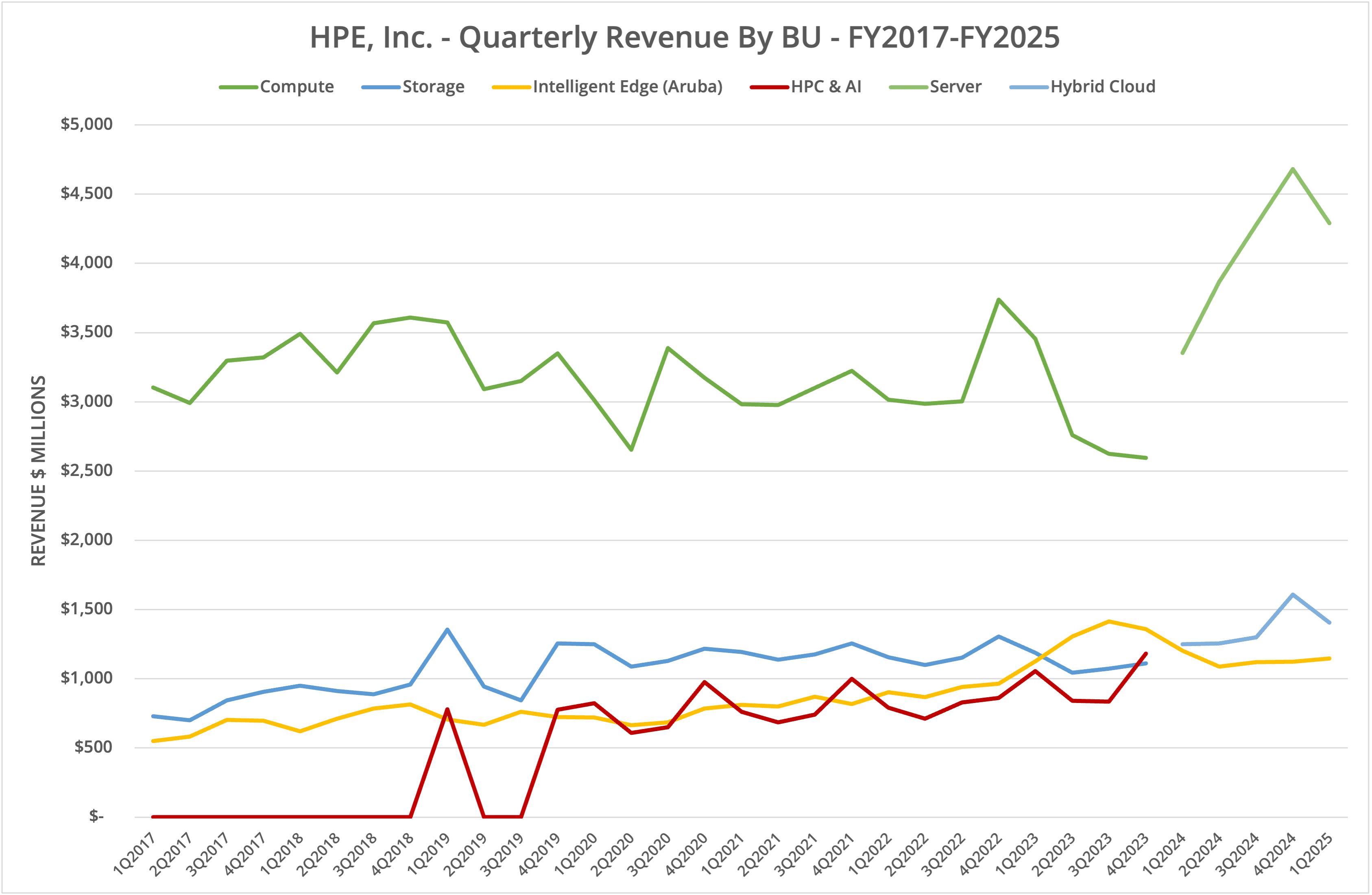

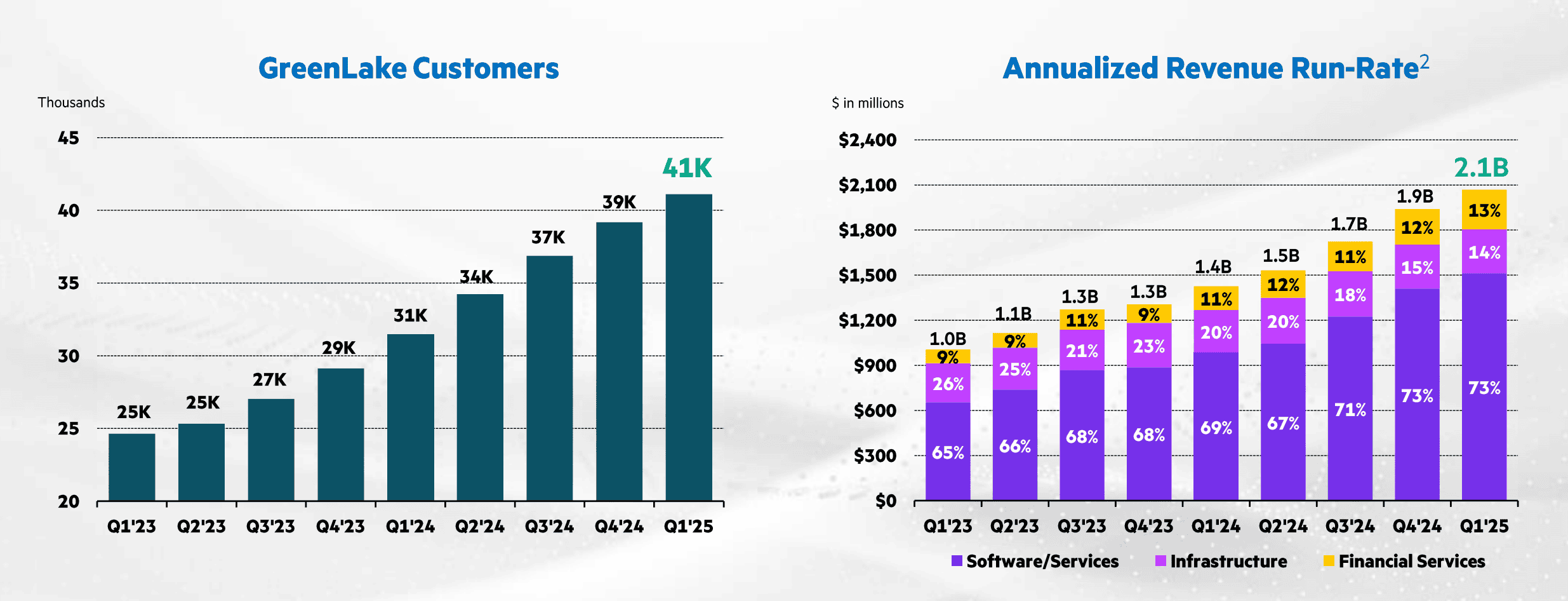

HPE, Inc. published financial data for Q1 FY2025, the period ending 31 January 2025, on 6 March 2025. The results show revenue rose by 16.3% year-on-year to $7.85 billion for the quarter but declined sequentially by 7.2%. Within those figures, the Server division increased revenue year-on-year by 28% but declined sequentially by 8.4%. Hybrid Cloud grew year-on-year by 12.6% but declined sequentially by 12.6%. Intelligent Edge (networking) fell by 4.6% year-on-year but grew sequentially by 2%. This mixed set of data is presented in four graphs labelled Figures 1 to 4. For annual data, see our previous analysis post here.

Two Steps Forward

HPE’s business continues to be a mix of rising and declining fortunes. Although the server business is up over the year, it is possible the peak has been reached, as highlighted in Figure 3. Similarly, the Hybrid Cloud division, which includes storage, saw increases in revenue over the last year, but has fallen back from the Q4 FY2024 peak (but is still up 12.6% over the year). The networking division (Intelligent Edge) appears to have flattened out in terms of revenue, slightly up sequentially but down compared to Q1 FY2024.

Two Steps Back

Despite the goldrush in AI, HPE has only partially benefited from the demand for AI servers. In the current period, although revenue increased, margin in Server declined, from 11.4% to 8.1%. However, Hybrid Cloud saw a significant increase in margin from 4.0% to 7.0%.

On a post-earnings release call, CEO Antonio Neri blamed a wide range of issues for the profit fall, including aggressive pricing by competitors and inventory issues, as customers wait for the next generation NVIDIA GPU solutions.

Hybrid Cloud

In the Hybrid Cloud division, HPE highlighted “hundreds” of customers interested in evaluating its own homegrown KVM-based hypervisor, introduced last November. Incredibly, Alletra MP storage continues to grow at triple-digit rates despite adding little or nothing to the overall revenue growth of the Hybrid Cloud division. To us, this means that the latest new hardware is simply replacing sales of the old products, rather than adding incremental benefits.

HPE did introduce a new object storage platform in November 2024 (our coverage here). It appears this solution is built entirely from HPE intellectual property and not a partner-rebranded design (like the file-based platform which uses VAST Data). This solution will take time to contribute to the bottom line as customers evaluate its features and functionality.

The Architect’s View®

HPE’s business continues to look fragile, with Q2 and FY2025 projections suggesting that server sales will actually decline. HPE CFO Marie Myers stated on the earnings call that Q2 revenue forecast would be between $7.2 billion and $7.6 billion, with Server revenue declining in FY2025. Similarly, Hybrid Cloud revenue is also expected to decline, an issue attributed to seasonality (despite the push to an ARR model with GreenLake).

As a result of the “challenging” outlook, HPE will reduce headcount by 2,500, plus another 500 in attritional loss, and look to make savings of $350 million by FY2027, although the cost of reduction will cancel these savings out in FY2026.

One aspect of HPE’s business (and Dell Technologies for that matter), is the yin/yang of the collective business units within the company. As the Server business grows, networking declines and vice-versa. Each of these business units operates in a cyclical nature, but none appear to be able to maintain long-term growth.

The problem appears multi-fold. Much of HPE’s business is shipping hardware, with any value (e.g. software) added elsewhere. Hardware sales are always a slow race to the bottom, with constant cost-cutting and price reductions. This has been highlighted as a problem in the current period. AI servers are popular at the moment, but this trend will not last, once the AI boom blows itself out.

Second, HPE’s product portfolio isn’t competitive. Although the storage solutions have been revamped, for example, the new Alletra MP architecture, the underlying offering is still based on 3PAR technology (or VAST Data). The decision to create an entirely new object storage solution in a mature market is also confusing, as HPE is essentially starting from scratch (much as Dell did with PowerStore).

In our opinion the challenge for HPE will continue to be one of innovation and competitiveness. HPE storage is “good enough”, but not special enough to gain traction with a significant volume of new customers. Community engagement and product marketing are in a mess (topics we’ve covered many times), putting additional challenges on sales teams to evangelise a less-than-interesting set of products.

No wonder, then, that in the storage market, some vendors are growing revenue consistently, while others are flat or lose customers through ongoing attrition.

The current mindset within HPE is to focus primarily on hardware infrastructure. However, even with the unprecedented focus on AI, this strategy hasn’t delivered meaningful revenue growth because hardware is a conduit for the value component in software. The money made in AI will not be from servers, but from the software and unique components like GPUs.

We continue to see tough times for HPE, in a market that is increasingly commoditised and challenging for all but the most innovative customers. In our view, nothing will improve this situation until the company mindset changes and HPE returns to the concept of solutions provider, rather than box shifter.

Related Posts

- Analysis: HPE, Inc. announces Q4 FY2024 and full year financial results

- Research Note: HPE announces a new object storage platform at Discover Barcelona 2024

Copyright (c) 2007-2025 – Post #6b98 – Brookend Limited, first published on https://www.architecting.it/blog, do not reproduce without permission. HPE is a Tracked Vendor by Architecting IT in storage systems and software-defined storage.