AMD, Inc. has announced financial results for the fourth quarter of FY2024 and the full year ending 28 December 2024. Revenue rose 13.7% over the year, with 24.2% growth year-on-year for Q4 FY2024. The company continues to see improvements in Data Centre and Client businesses, while Gaming and Embedded saw further declines.

Background

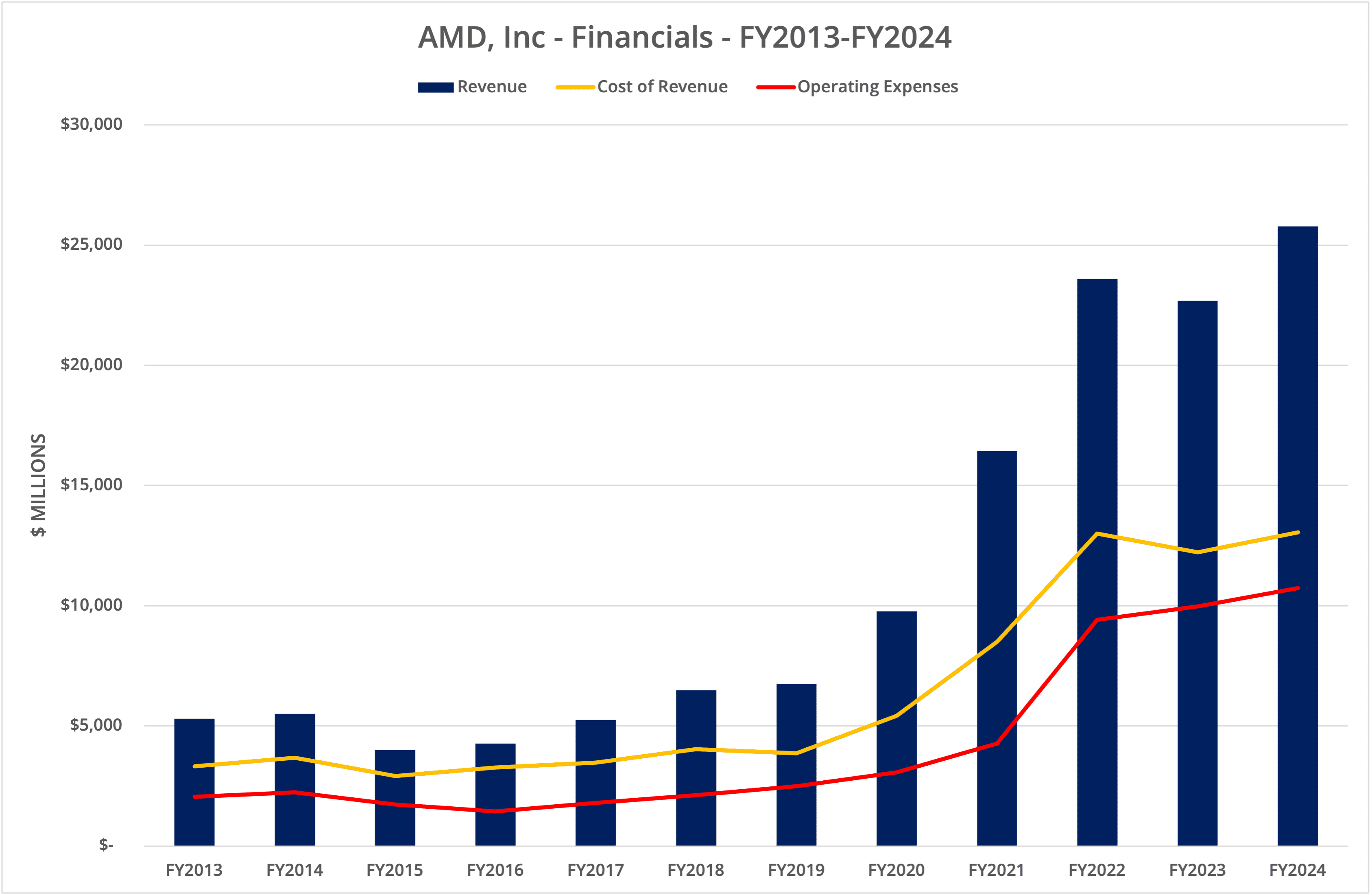

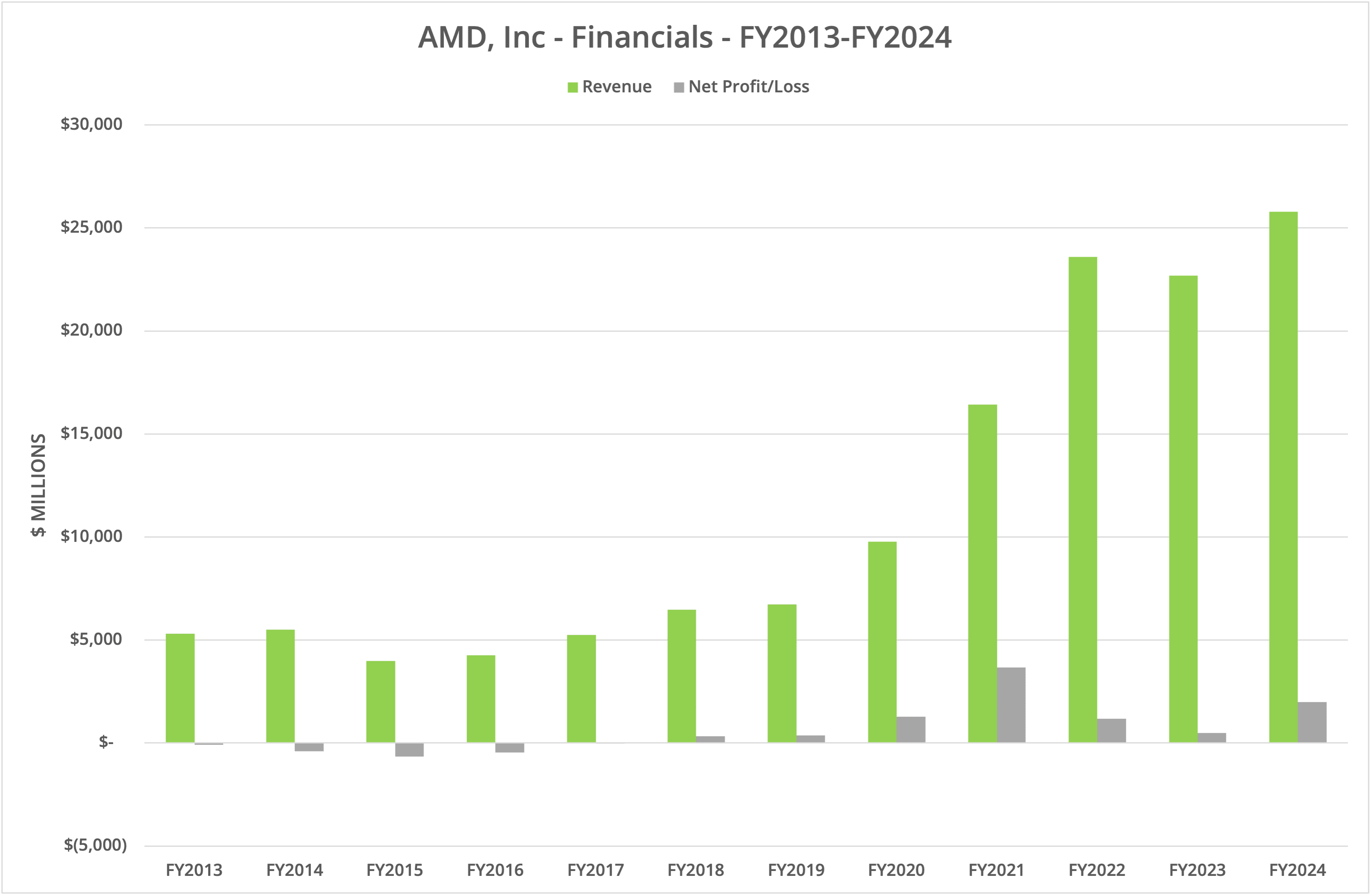

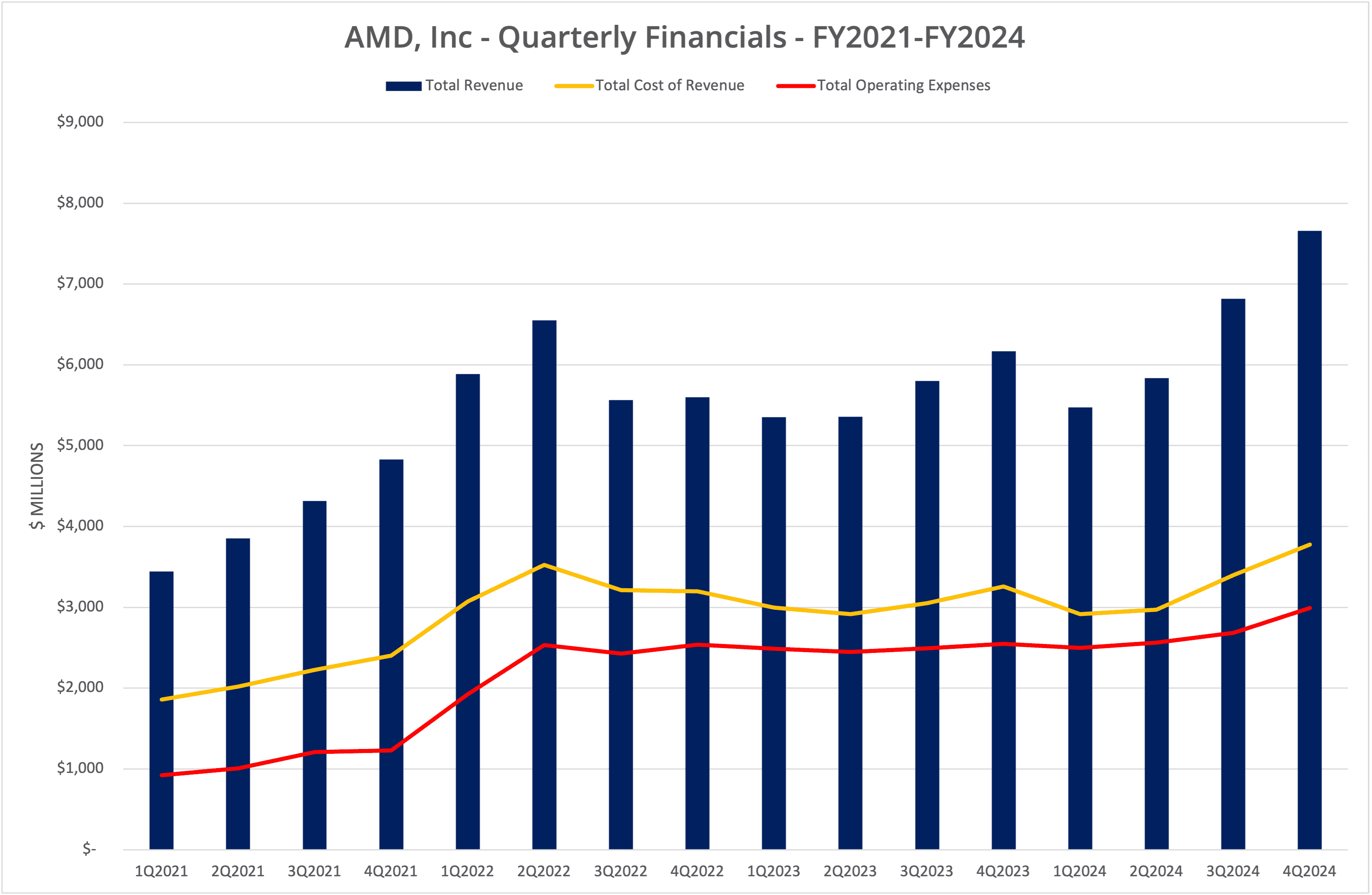

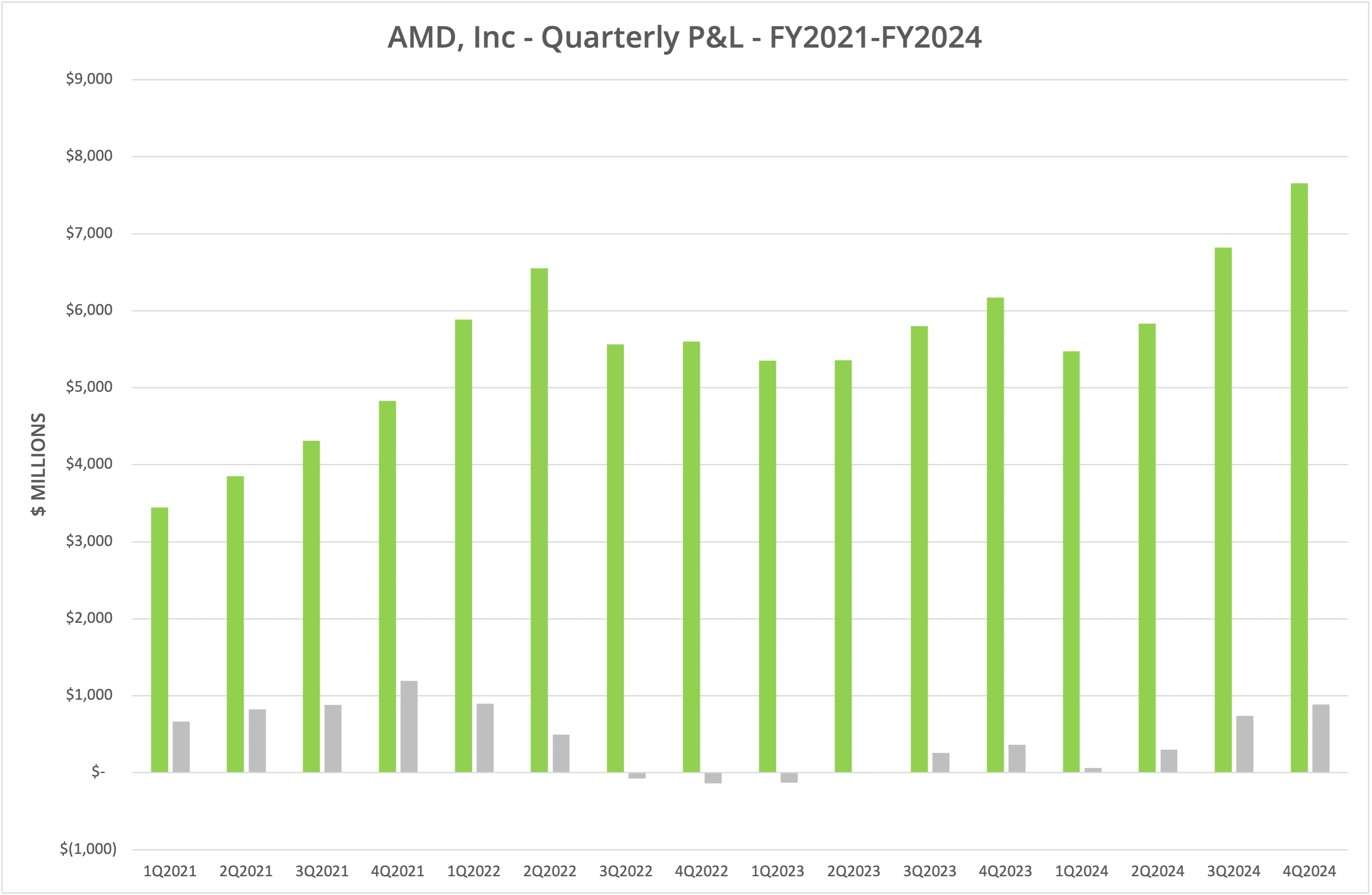

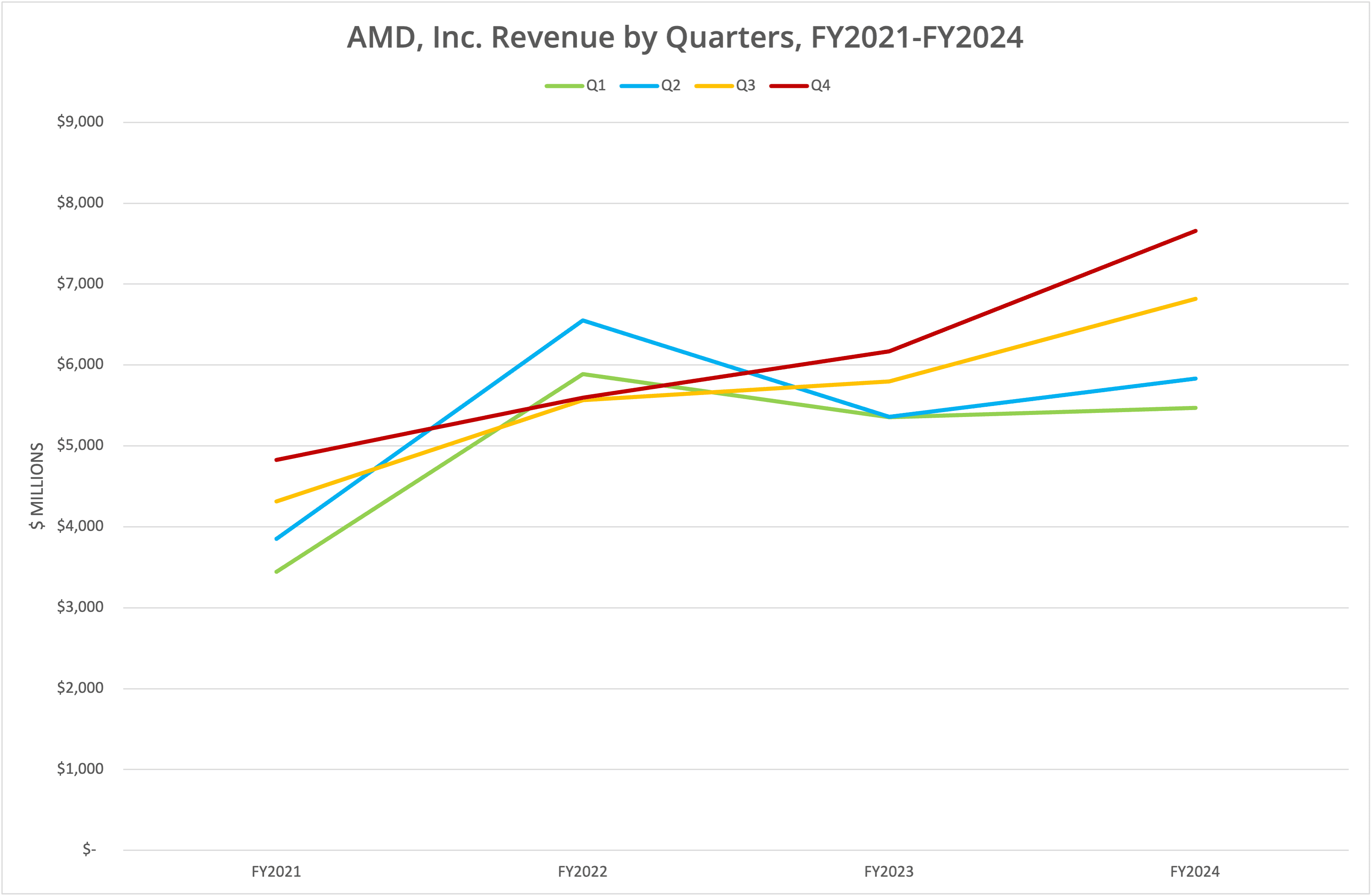

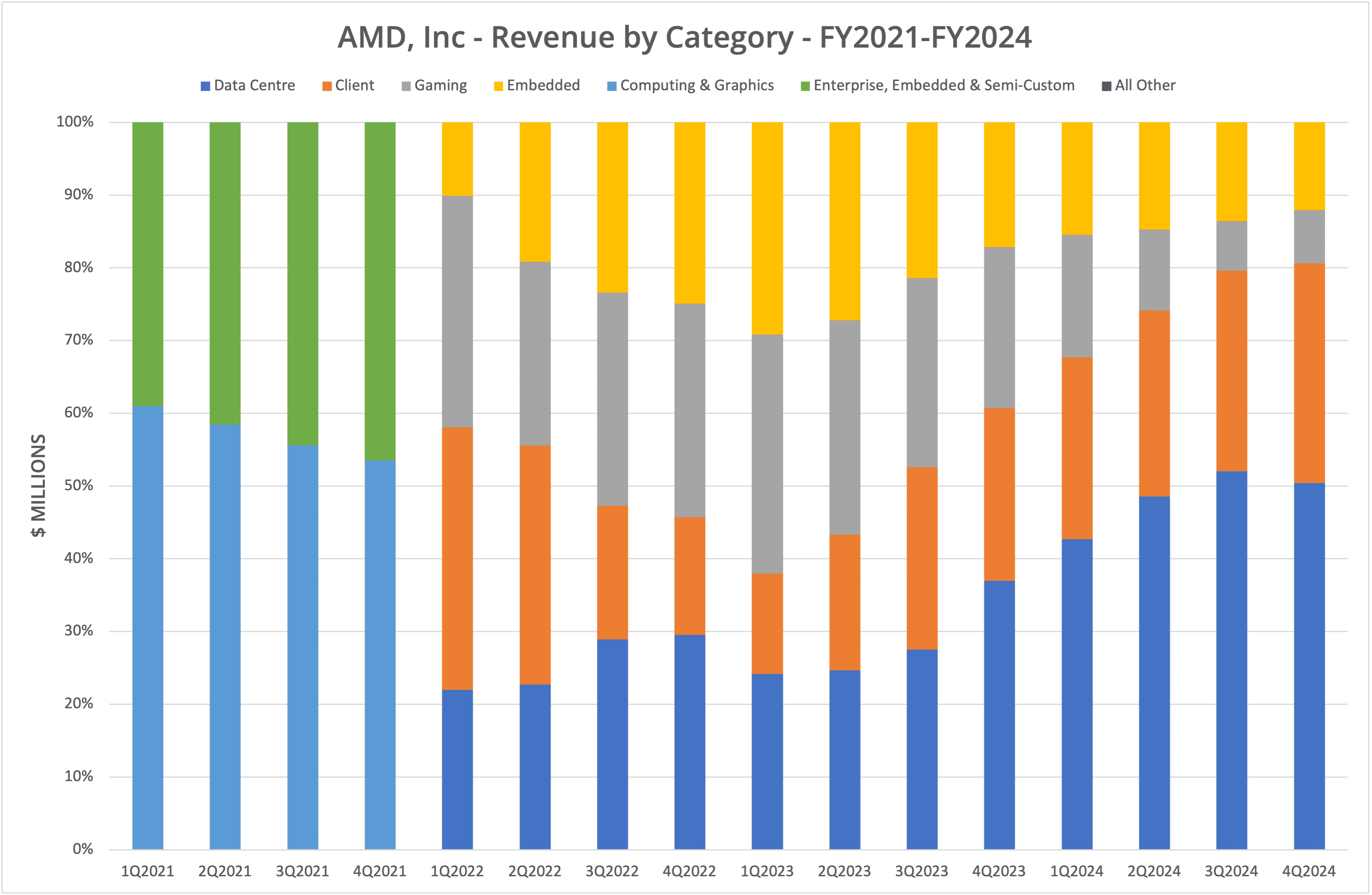

AMD, Inc. reported financial data for the period Q4 FY2024, ending 28 December 2024, on 4 February 2025. Revenue for the quarter was $7.7 billion, up 24.2% year-on-year. For the full year FY2024, revenue was $25.8 billion, up 13.7% on the previous year. By division, Data Centre revenue increased 93.6% and Client 51.7%. However, these gains were at a cost to Gaming (down 58.2%) and Embedded (33.2% down).

We present the data in 6 graphs, labelled Figures 1 to 6.

AI

Growth in the Data Centre segment was driven primarily by sales of Instinct GPUs and increase in demand for EPYC CPUs. The MI300 series of GPUs have been popular, second in the market to NVIDIA and well ahead of Intel Gaudi, which failed to meet its $500 million sales target for FY2024. EPYC processors continue to compete with Intel, being first to PCI 5.0 support and typically offering greater I/O performance.

Where Intel has failed to capitalise on the AI boom, NVIDIA and AMD have been much more successful. However, it’s not all about GPUs and AI.

EPYC

Earlier this month, AMD announced new Google Cloud virtual instances powered by 5th Generation EPYC processors (codenamed Turin), with Oracle Cloud adding E6 Standard Shapes based on EPYC in March 2025. The 6th generation “Venice” processors based on Zen6 “Morpheus” cores are expected at some time in 2026. AMD continues to maintain a reliable cadence of new updates, keeping the pressure on its competition (essentially Intel).

The Architect’s View®

There’s little more to say in this analysis than to highlight the continued good work AMD is doing in the data centre market. However, even as AMD continues to grow the Zen architecture, we can’t help but think that competition from alternatives such as Arm and RISC-V could become significant in both the public cloud and on-premises data centres.

Should AMD counter this by working on alternatives, such as an Arm-licensed processor or even an in-house RISC-V? This is a difficult question to answer, as the tipping point away from AMD is not clear, while AMD continues to outperform Intel. For as long as AMD sees EPYC growth, then an alternative isn’t required. However, some form of low-powered processor is needed in the market, which AMD appears to be meeting with the “c” suffixed Zen designs.

For now, AMD seems to be delivering on all fronts with respect to enterprise computing, while making the most of the turmoil at Intel.

Copyright (c) 2007-2025 – Post #5ff4 – Brookend Limited, first published on https://www.architecting.it/blog, do not reproduce without permission.