Seagate Technology Holdings PLC has announced financial results for the fourth quarter of FY2025 and the full year, the period ending 27th June 2025. Revenue is up by 29.5% at $2.44 billion for the quarter, and up 38.9% for FY2026 at $9.1 billion. Is this a long-term revival or short-term gain due to current hyper-scale activity?

Background

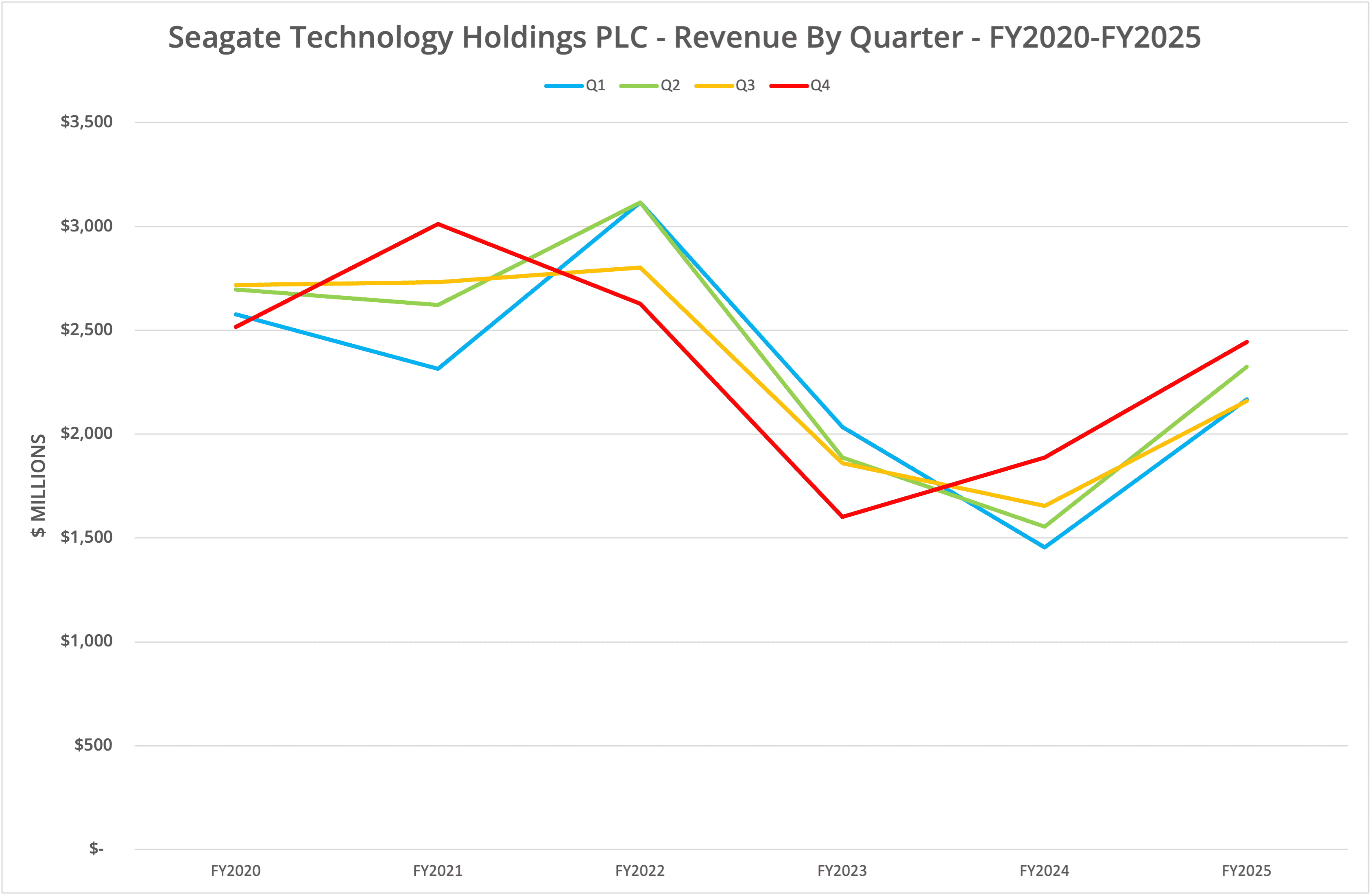

Seagate Technology Holdings PLC declared financial results for Q4 FY2025 and the full year, the period ending 27th June 2025, on 29th July 2025. Revenue increased by 29.5% for the quarter to $2.44 billion, compared to Q4 FY2025. For the full year, revenue was $9.1 billion, an increase of 38.9% compared to FY2025.

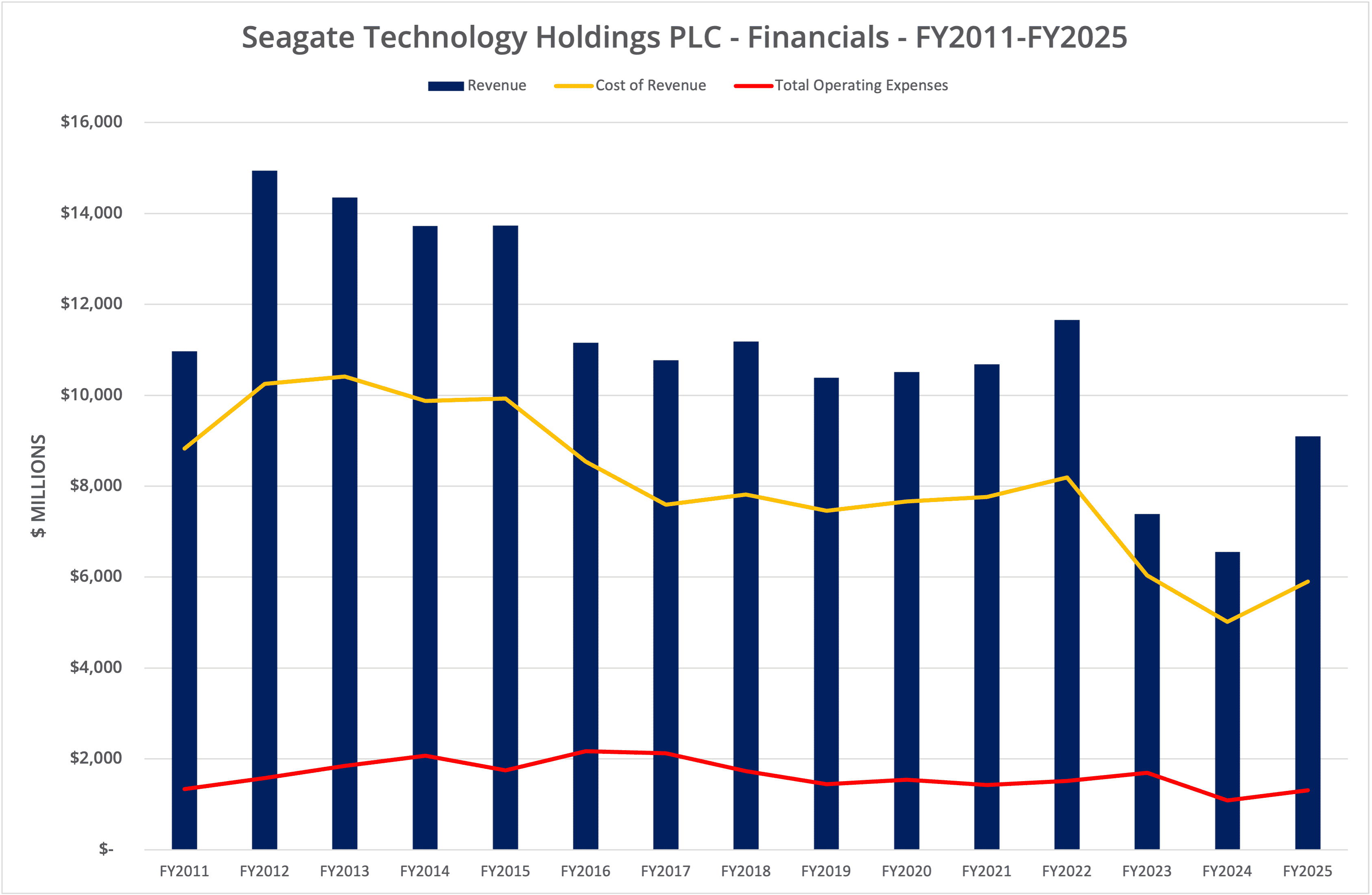

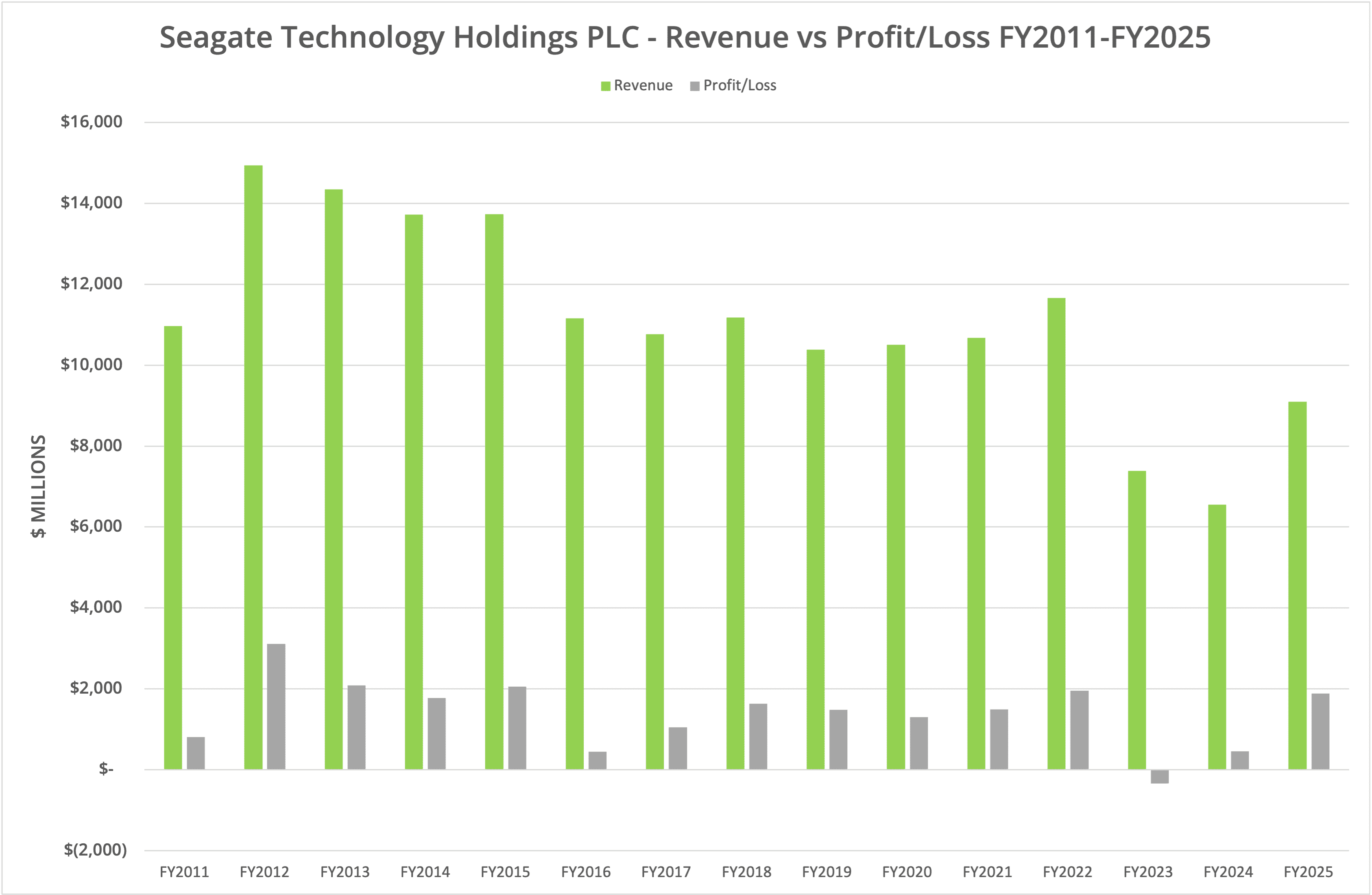

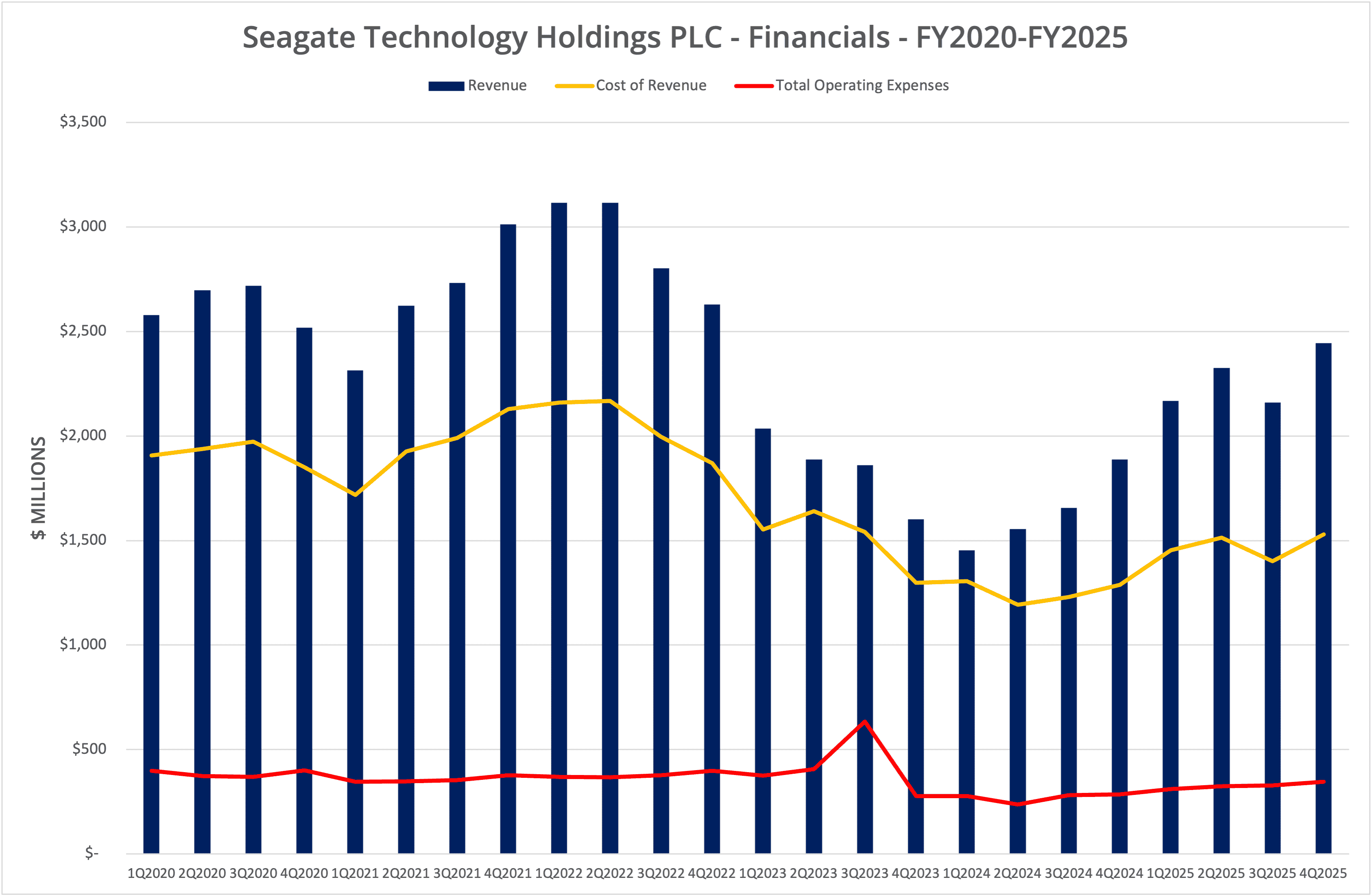

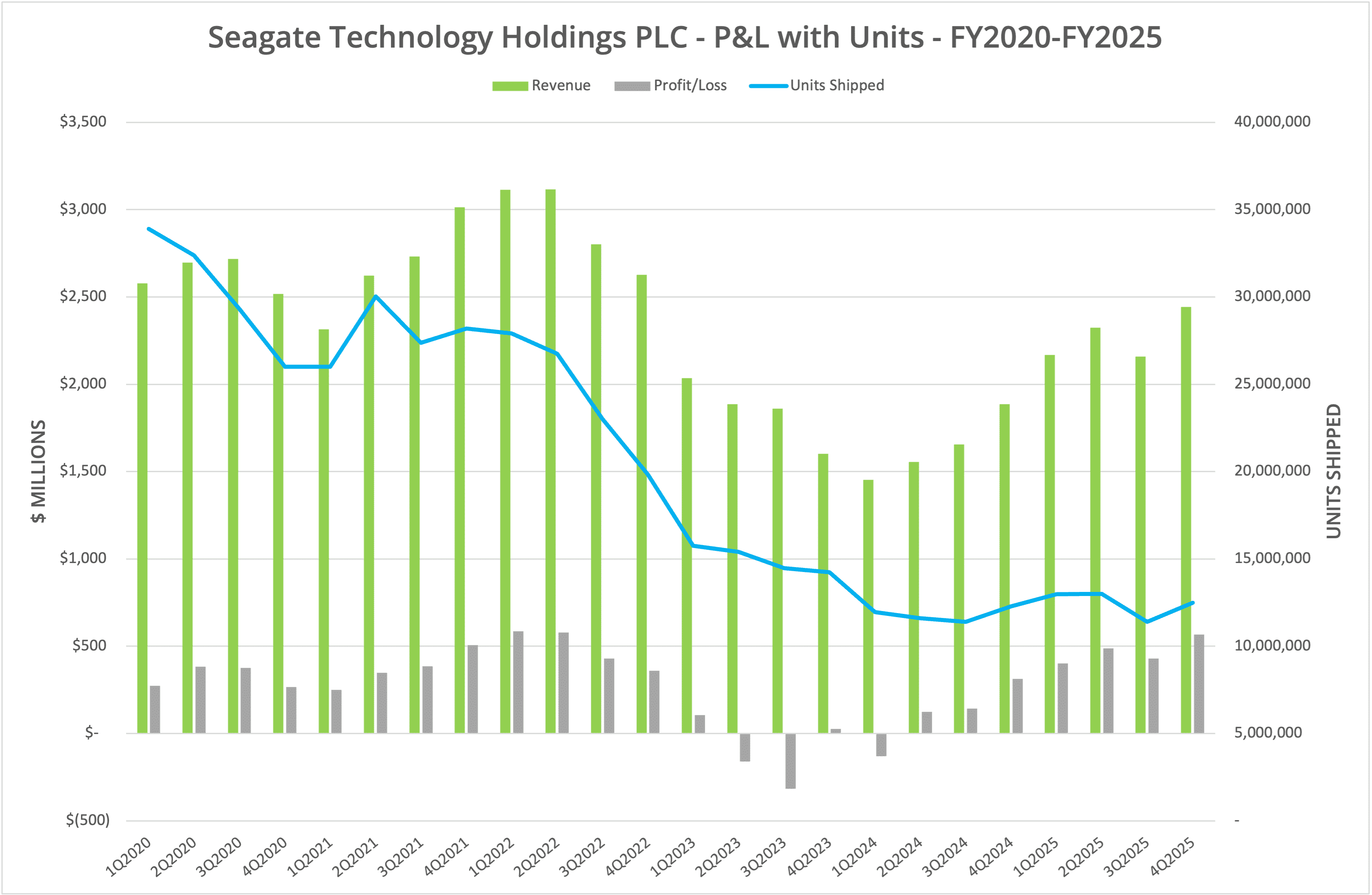

We present the data in six graphs, labelled Figures 1 to 6.

Growth

There is no doubt that Seagate has managed to deliver stellar financial results, with a hefty 38.9% increase compared to FY2024. It should be noted, though, that historically, as shown in Figures 1 and 2, FY2025 is the third lowest revenue result of the last fifteen years (the others being FY2023 and FY2024).

Units

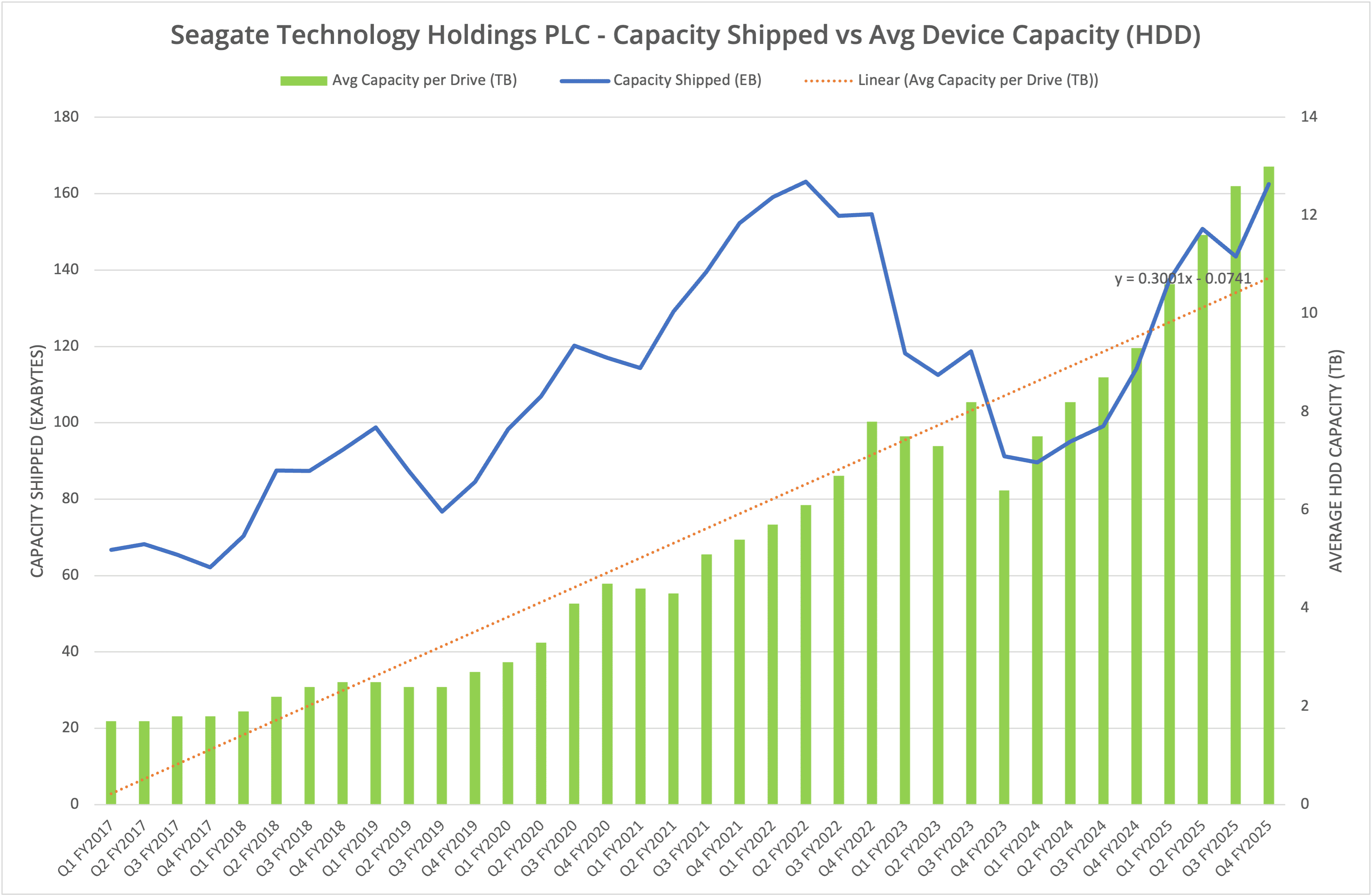

Looking at Figure 4, we display revenue with units shipped, and as we’ve highlighted before, the two have a strong correlation. Selling hard disk drives (which is 93% of Seagate’s revenue) is a commodity business, dictated by the quantity of drives sold to customers. Generally, this revenue has been independent of device capacity. However, in recent years, Seagate has managed to increase gross margin and revenue compared to a few years ago.

Unfortunately, Seagate has chosen not to publish the average selling price per drive in this current period, so we can’t see what improvement has been made with the rollout of HAMR. Naturally, the ASP could have increased simply due to the mix of drives sold. Data shown in the supplemental information supporting the earnings release (available here) shows (on page 6) that average capacity per drive has increased by 50% over the past year. We would therefore expect the ASP to grow further but decline as legacy and small capacity drives contribute less to the overall mix.

HAMR

The future of Seagate is predicated on the success of HAMR recording technology. Systems represent just 7% of revenue, while mass capacity drives are 88% of all earnings. HAMR is expected to expand into 40+ TB drive qualification in Q3 FY2025 (as indicated during the Seagate investor event in May 2025, slides here). 50+TB drives are expected in calendar year 2028, with a forecast of 80+TB drives somewhere between 2031 and 2032.

Disk vs SSD

Let’s put the Seagate growth claims into perspective against the NAND SSD market. We recently covered three new products from Micron, which offer drive capacities up to 122TB and 245TB on the horizon within the next 12 months. The relative density of SSDs compared to HDDs is much higher, with a greater growth percentage as new products are released.

In addition, performance is also improving exponentially with each step in PCIe adoption. PCIe 6.0 devices can achieve 28GB/s (approximately) of throughput and millions of IOPS. HDDs are stuck in the slow lane, with little or no performance improvement possible due to the mechanical nature of the technology. The current data available on the Seagate EXOS range doesn’t cover the latest HAMR drives. However, 30TB EXOS M drives show 275MB/s of throughput and only 170 random IOPS at 4.16ms latency (SSDs quote microsecond latency figures). These are the same performance metrics as drives from 15 years ago.

As the market for SSDs and HDDs evolves, performance and capacity improvements make it easier to justify SSDs for more active workloads, while HDDs become increasingly suitable only for archive data.

The Architect’s View®

Let’s not discount the work that Seagate has done to turn around the business. The current Seagate is a leaner operation that is returning to revenue and will also return value to shareholders. That’s good news if you are an investor.

But (and here’s the kicker) hard disk drives are headed towards the same market position as magnetic tape. Tape is now 100% an archive and backup medium, but also suffering the challenges of scalability and operability as generational performance improvements start to decline.

The HDD is heading the same way, and at some point in the (not too distant) future it will start to decline in value and growth. This is, of course, dependent on how growth is measured. In capacity terms, demand may increase. However, in units shipped, demand has consistently declined over the last five years, plateauing around 12-13 million units per quarter for Seagate, with similar quantities for Western Digital.

We’re left with two questions. First, what is the timeline for the decline in HDD demand? Second, what is the Seagate Plan B when this happens? The answer to question one is probably “within the next decade to fifteen years”. The answer to the second is unknown.

Copyright (c) 2007-2025 – Post #cd88 – Brookend Ltd, first published on https://www.architecting.it/blog, do not reproduce without permission.