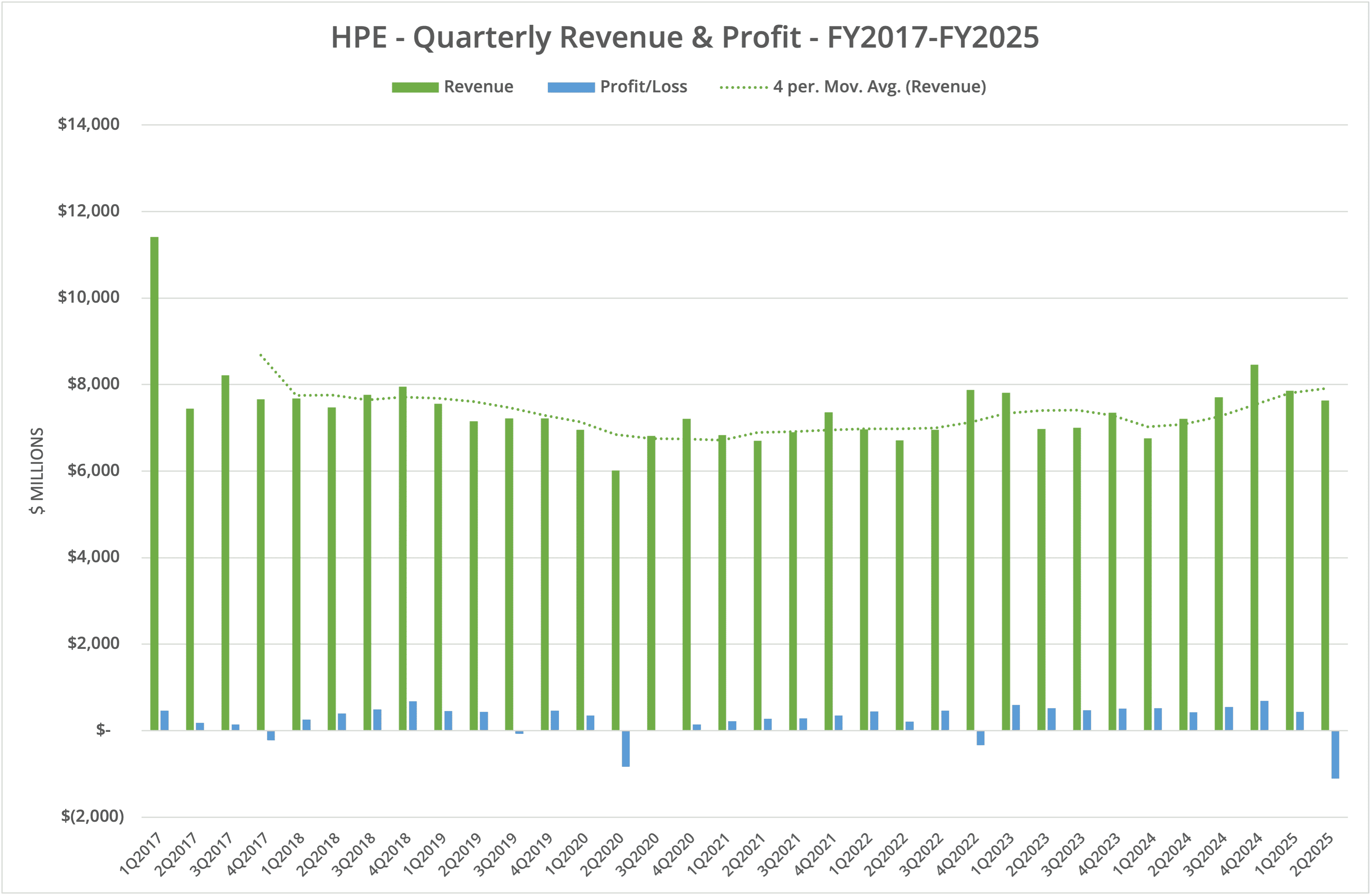

Hewlett Packard Enterprise Company has declared financial results for Q2 FY2025 (the period ending 30th April 2025) on 3rd June 2025. Revenue rose 5.9% to $7.63 billion during the quarter, although that was down 2.9% sequentially. A non-cash impairment of goodwill charge pushed HPE into a technical loss for the quarter, which otherwise would have been profitable.

Background

HPE has published financial data for the second period of FY2025. Revenue rose 5.9% to $7.63 billion but was down 2.9% sequentially. All divisions reported year-on-year growth (except Financial Services), with Server increasing 4.9% to $4.01 billion, Hybrid Cloud up 15.7% to $1.45 billion and Intelligent Edge up 7.0% to $1.16 billion. An impairment of goodwill charge in Hybrid Cloud pushed HPE into a technical loss of $1.1 billion for the period.

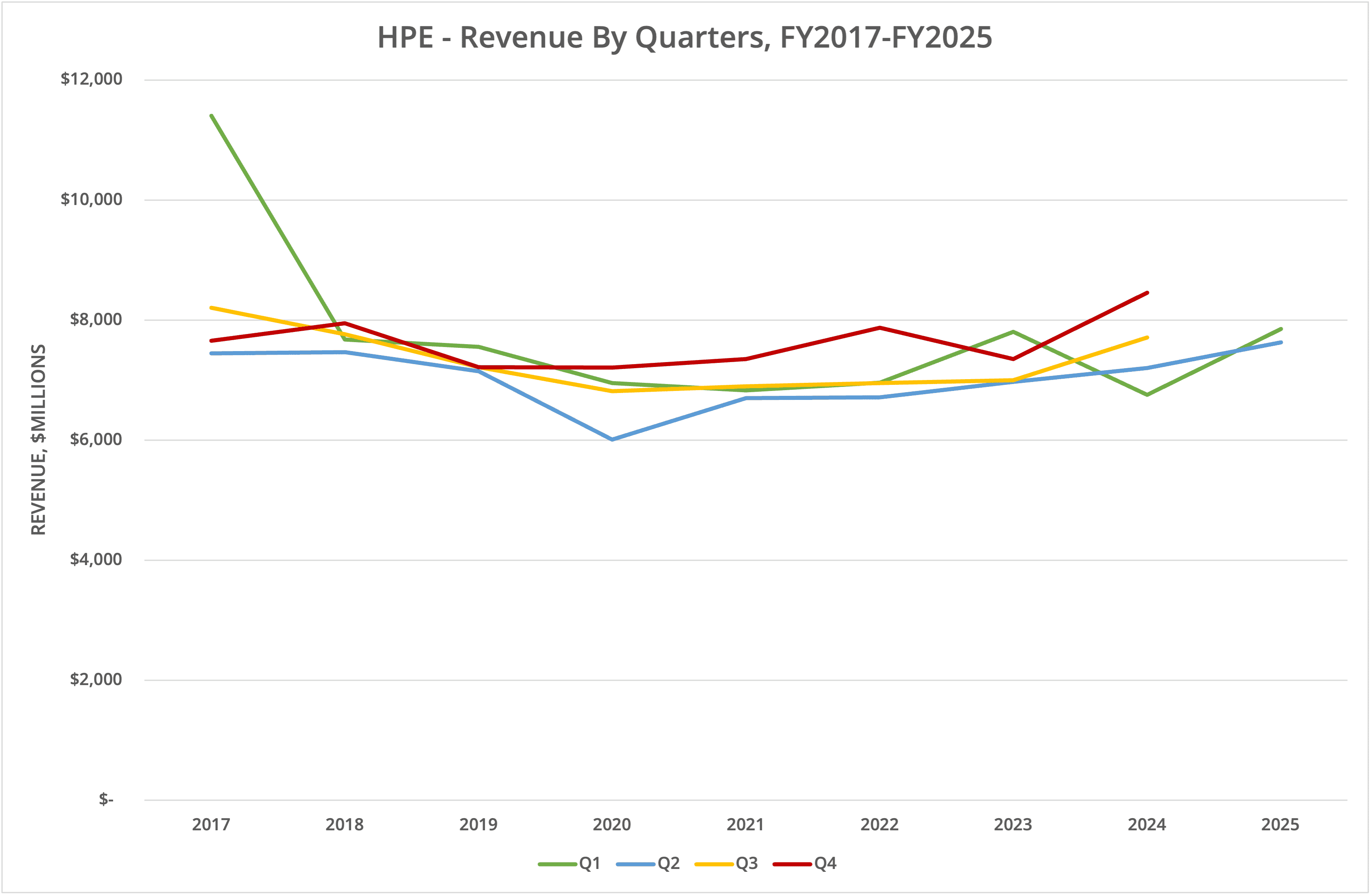

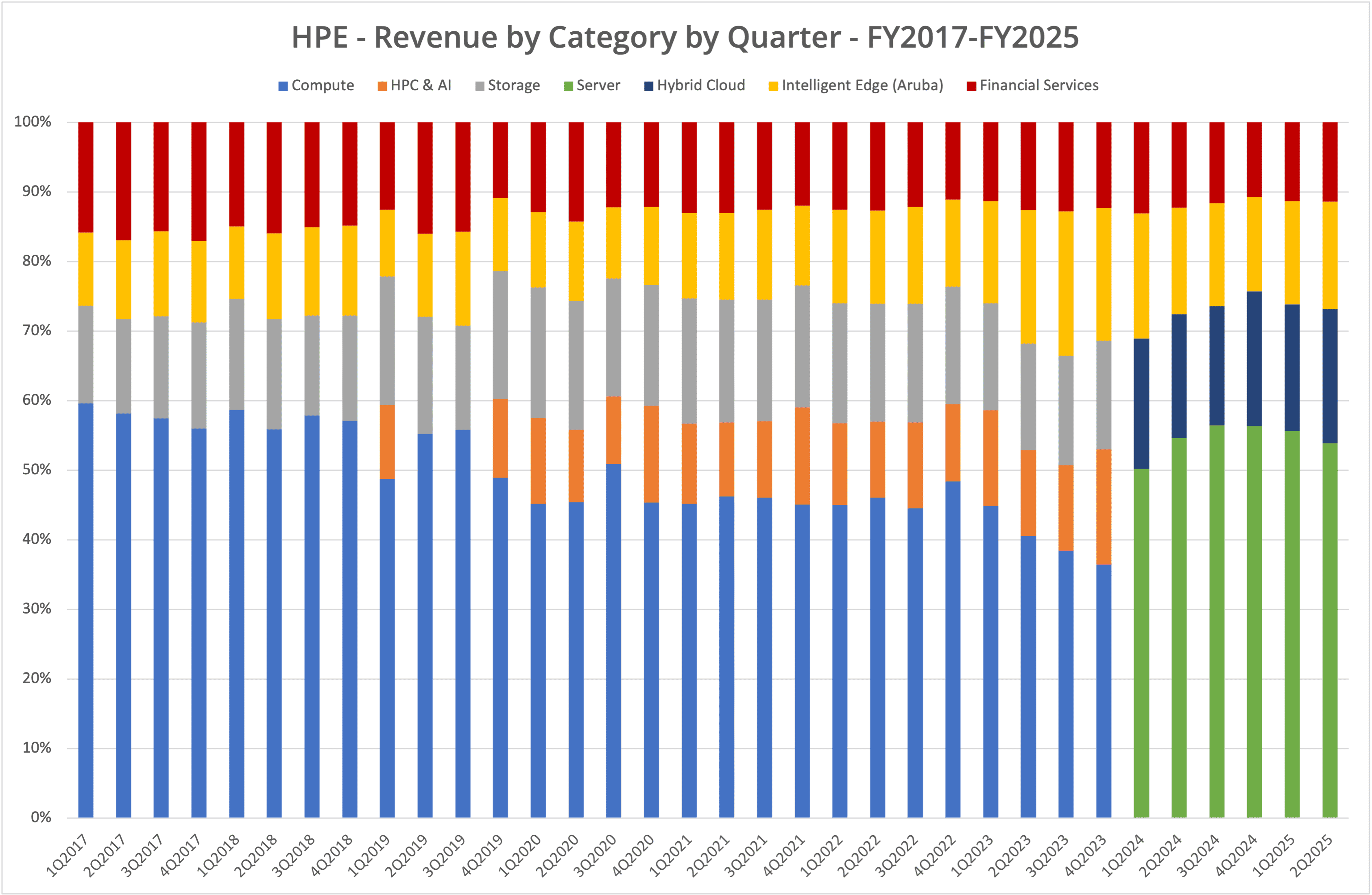

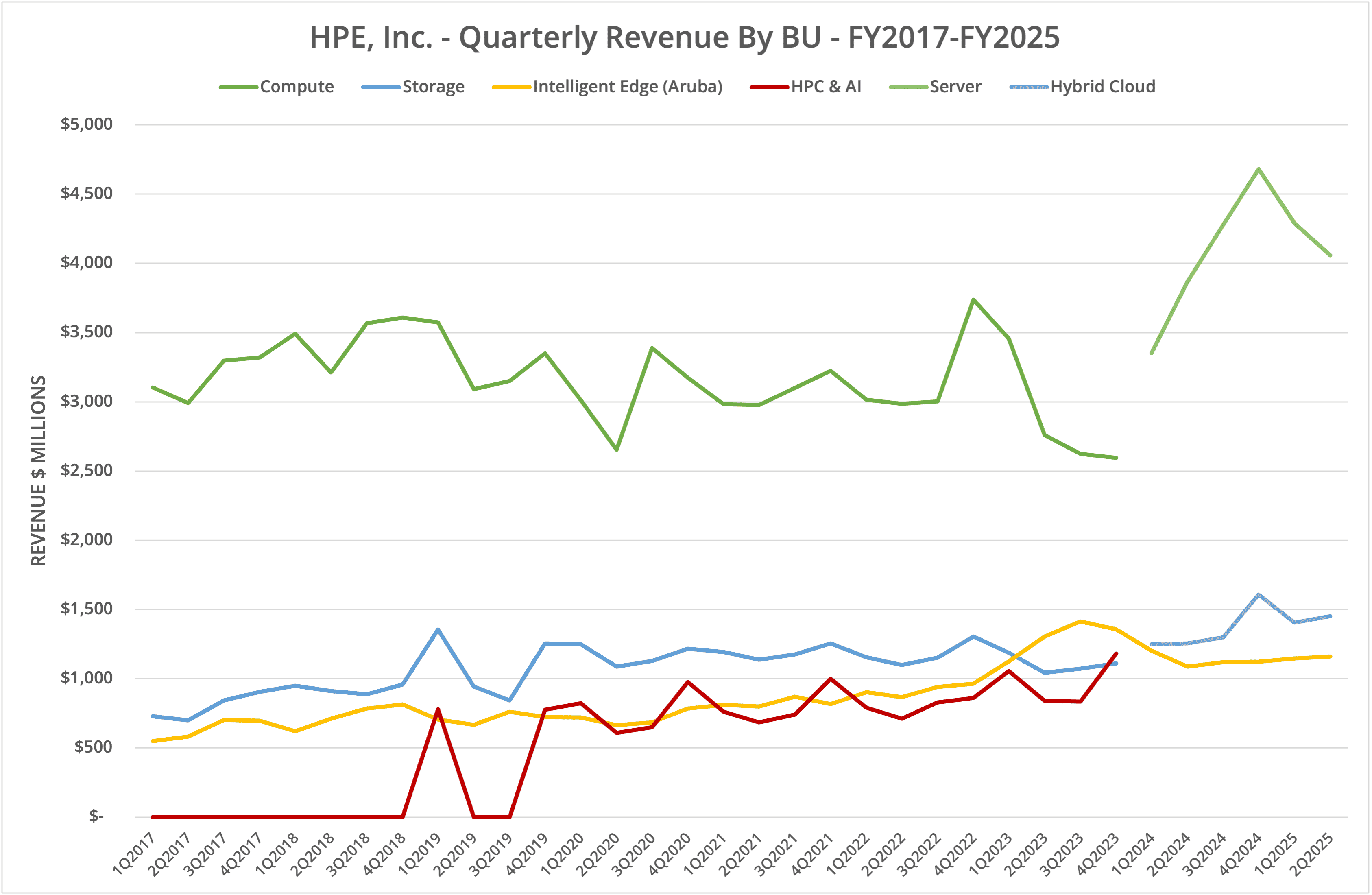

We present the data in five graphs, labelled Figures 1 to 5.

Three Steps Forward

Although Server revenue is up 4.9% year-on-year, the trend is currently downwards from a peak in Q4 FY2024. We don’t show it in our graphs, but this trend is also accompanied by a reduction in operating margin to 5.9%. CEO Antonio Neri addressed the issue in the post-earnings call, indicating that by Q4, this figure should be back closer to 10%.

Hybrid Cloud has also seen operating margin decline sequentially, although it is up year-on-year, due to a terrible dip to 1% in Q2 FY2024. The revenue trend for the hybrid cloud business is slightly upwards, as is Intelligent Edge, both helping to counter the loss in revenue from the Server division.

Growth

It is interesting to note that in a market where AI is the dominant discussion, HPE is not seeing a growth in sales that aligns with the fortunes of GPU manufacturers such as NVIDIA and AMD. This translates into two possibilities. First, that most of the GPU demand is being delivered into the public cloud, and second, that HPE is experiencing traditional server sales decline in favour of AI servers (those with embedded GPUs).

However, on a positive note, the networking business is recovering slightly, while Hybrid Cloud, which includes storage and the heavily promoted VM Essentials, also grew revenue – 15.7% year-on-year or 3.4% sequentially.

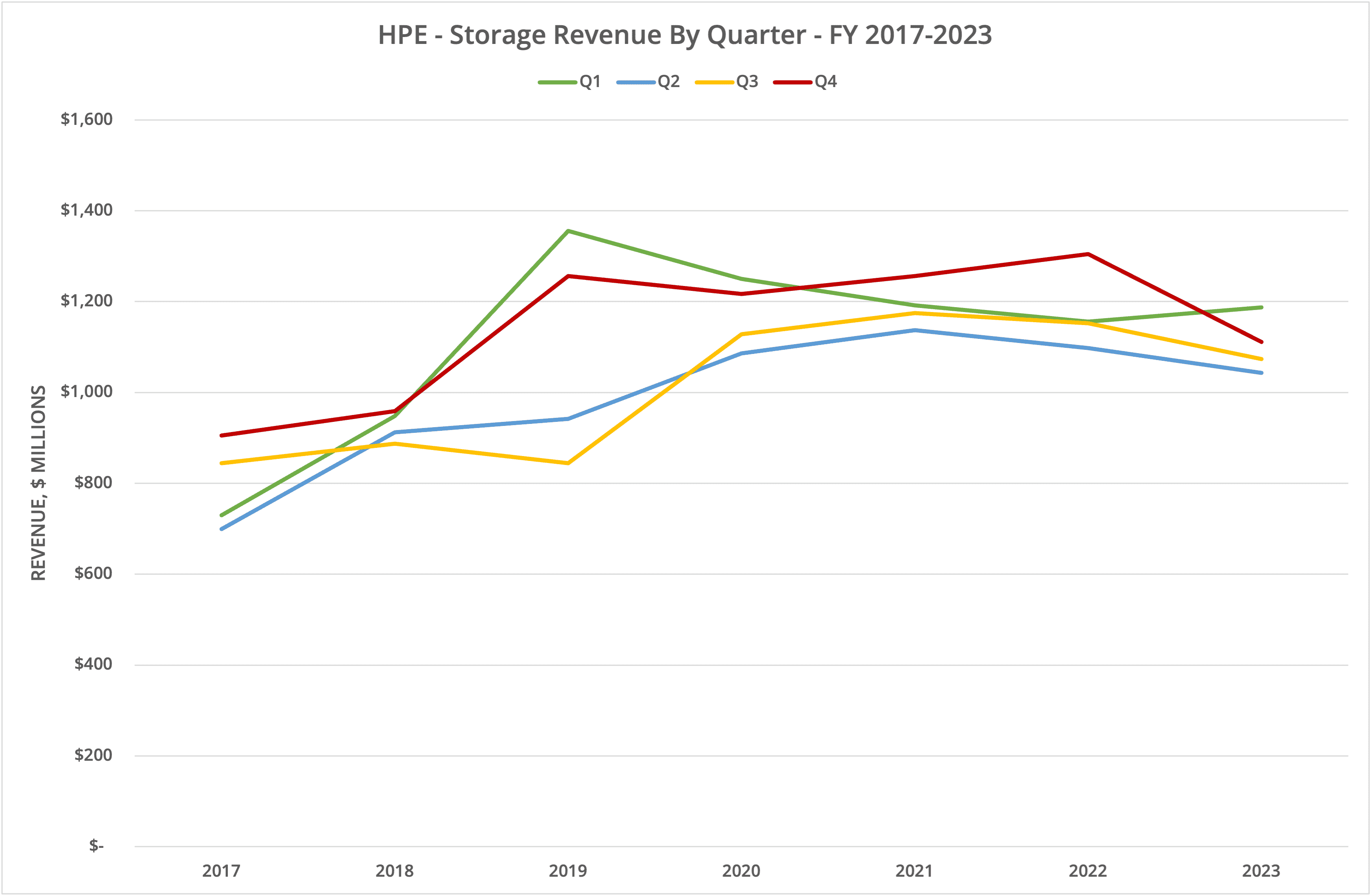

Storage

Although the storage business gets a brief mention (another quarter of double-digit growth in Alletra and triple digits with Alletra MP, which seems mathematically impossible), we have no real clarity as to how much contribution storage sales make to the Hybrid Cloud mix.

HPE is keen to talk in percentages when discussing the Alletra product line but not to publish any actual data. We can, therefore, only speculate that storage sales are much less than the $1.45 billion recorded in the quarter, which put the company in a definite third place behind Dell Technologies and NetApp and possibly in fourth place behind Pure Storage, depending on the contribution of Storage into Hybrid Cloud.

GreenLake

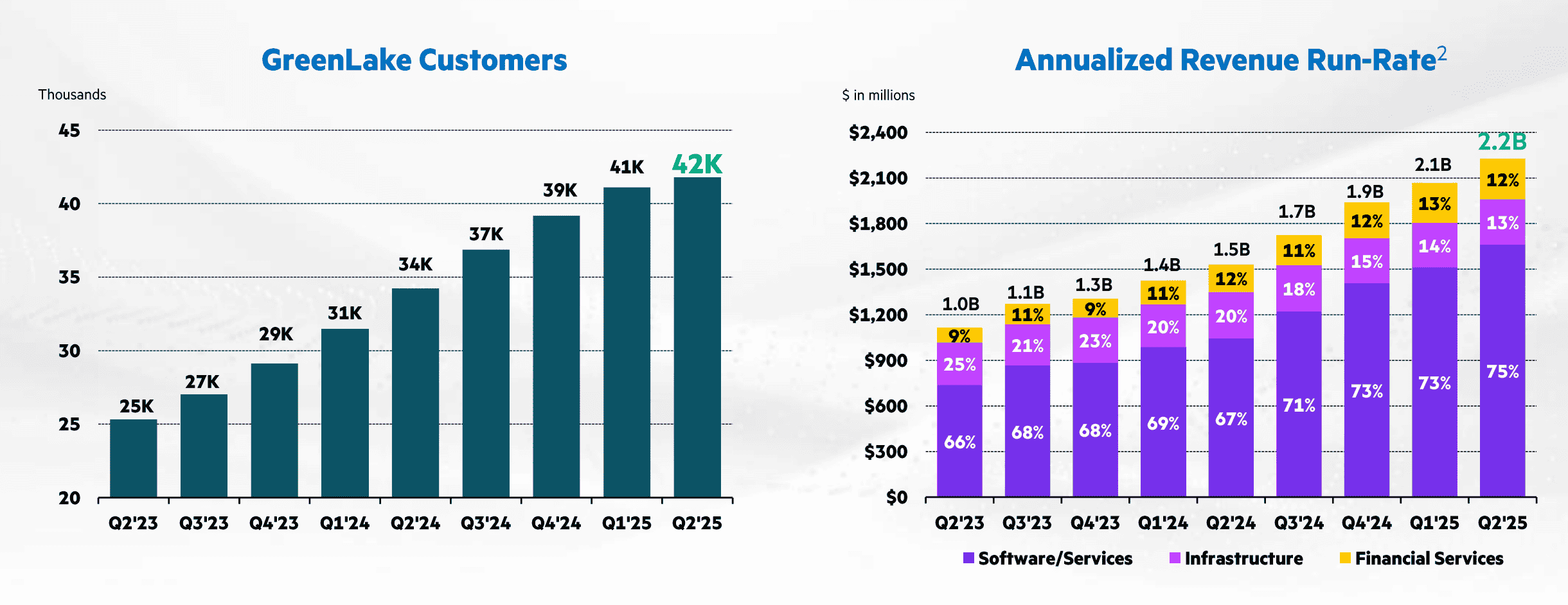

A quick word about GreenLake, the service offerings from HPE. In the current quarter, only 1,000 new customers were added (which could include existing HPE customers transitioning to the service model), which is a slowdown over the previous months. Additionally, revenue growth was slower at half the last three quarters (see Figure 6).

Bear in mind the data quoted for GreenLake is ARR (annual recurring revenue). With an expected 7-9% revenue growth for the whole of 2025, that currently puts GreenLake at only 7% of sales. This is six years after the strategy was announced and now three years after all services were expected to be delivered in GreenLake format (see this coverage for the details).

The Architect’s View®

Hardware infrastructure is a tough business, and as we can see from HPE’s annual results there has only been a marginal improvement in revenue (most of which is washed out by inflation). Up until the last quarter in which Storage was separately itemised, we could see flat revenue and no growth (see Figure 4 and Figure 5).

Neither the Server nor the networking business are the cash cows HPE would want. GreenLake could take another 20 or 30 years to transform HPE into a services-only business. So, what happens next?

The greatest challenge for HPE is the margin available from hardware sales and how much money is available to spend on research & development (HPE spends 2.5 times on Sales, General & Admin compared to R&D). However, service and software sales have greater margin, but therein lies the challenge. HPE has attempted to build the services/software business through GreenLake, but after six years has only 7% penetration on traditional sales.

Is HPE selling what customers want? VM Essentials is potentially a good example of a product that could drive more margin. However, HPE appears to have cut the marketing function so much that finding information on any product is a challenge.

We believe HPE needs to refrain from buying hardware companies and invest in more software rather than relying on partners (especially in storage). The company needs to return to selling solution stacks, particularly in direct competition with capabilities offered in the public cloud.

Unfortunately, like Dell Technologies, HPE has a heritage based on hardware infrastructure. Changing the company will be a hard sell. IBM (mostly) did it, shedding PCs and servers. Could HPE be just as bold? With Discover just about to start, it is time to see.

Copyright (c) 2007-2025 – Post #6b60 – Brookend Ltd, first published on https://www.architecting.it/blog, do not reproduce without permission.