Pure Storage, Inc. has announced financial results for the first quarter of FY2026, the period ending 4th May 2025. Revenue is up 12.3% year-on-year, with Subscriptions revenue up 17.4%. Subscriptions ARR continues to grow, up 18%. However, Cost of Revenue for Products increased from 29% in Q1 FY2025 to 38% in the current quarter. Is this a rise in component costs coming through, and what are the implications?

Background

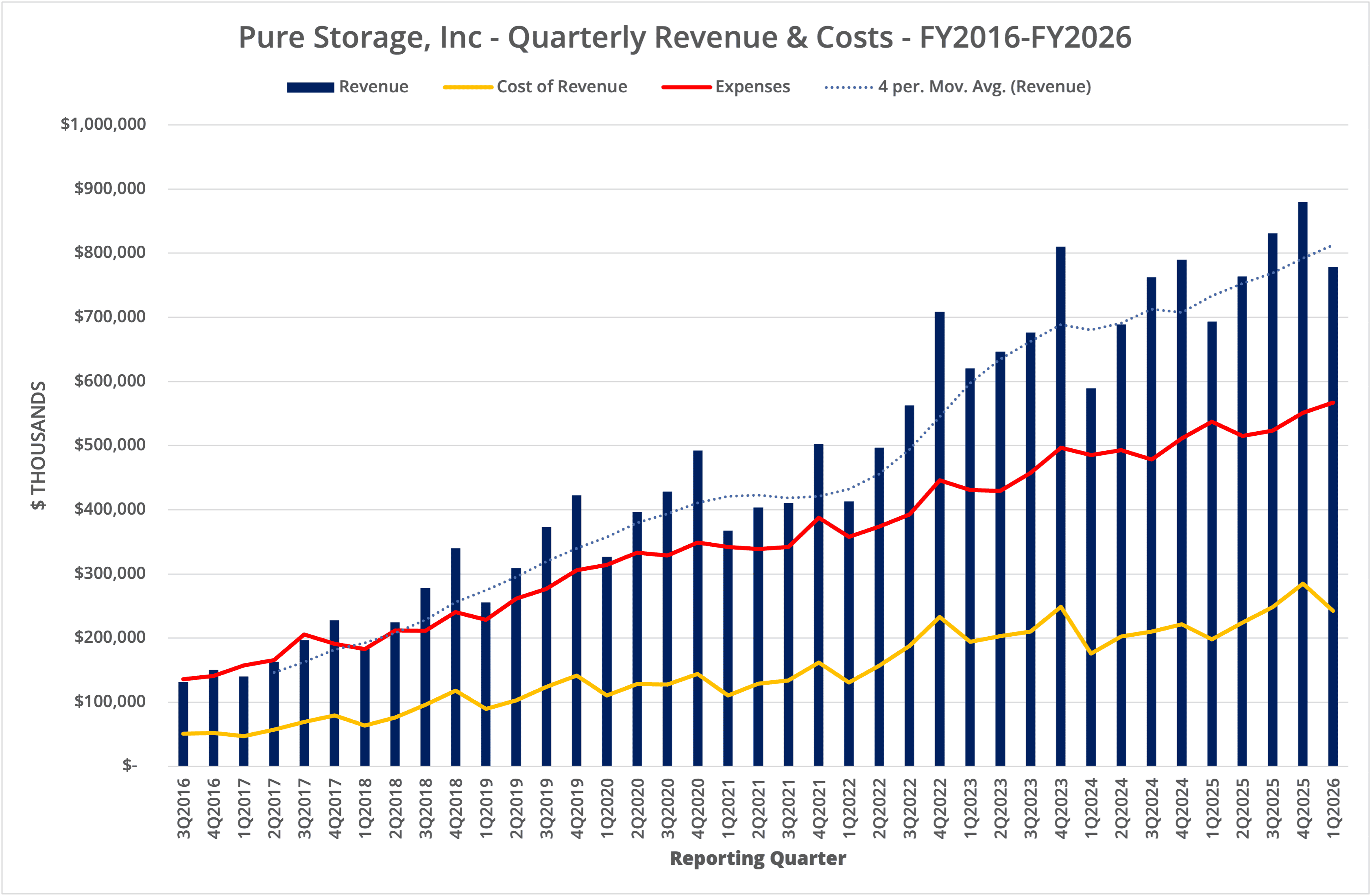

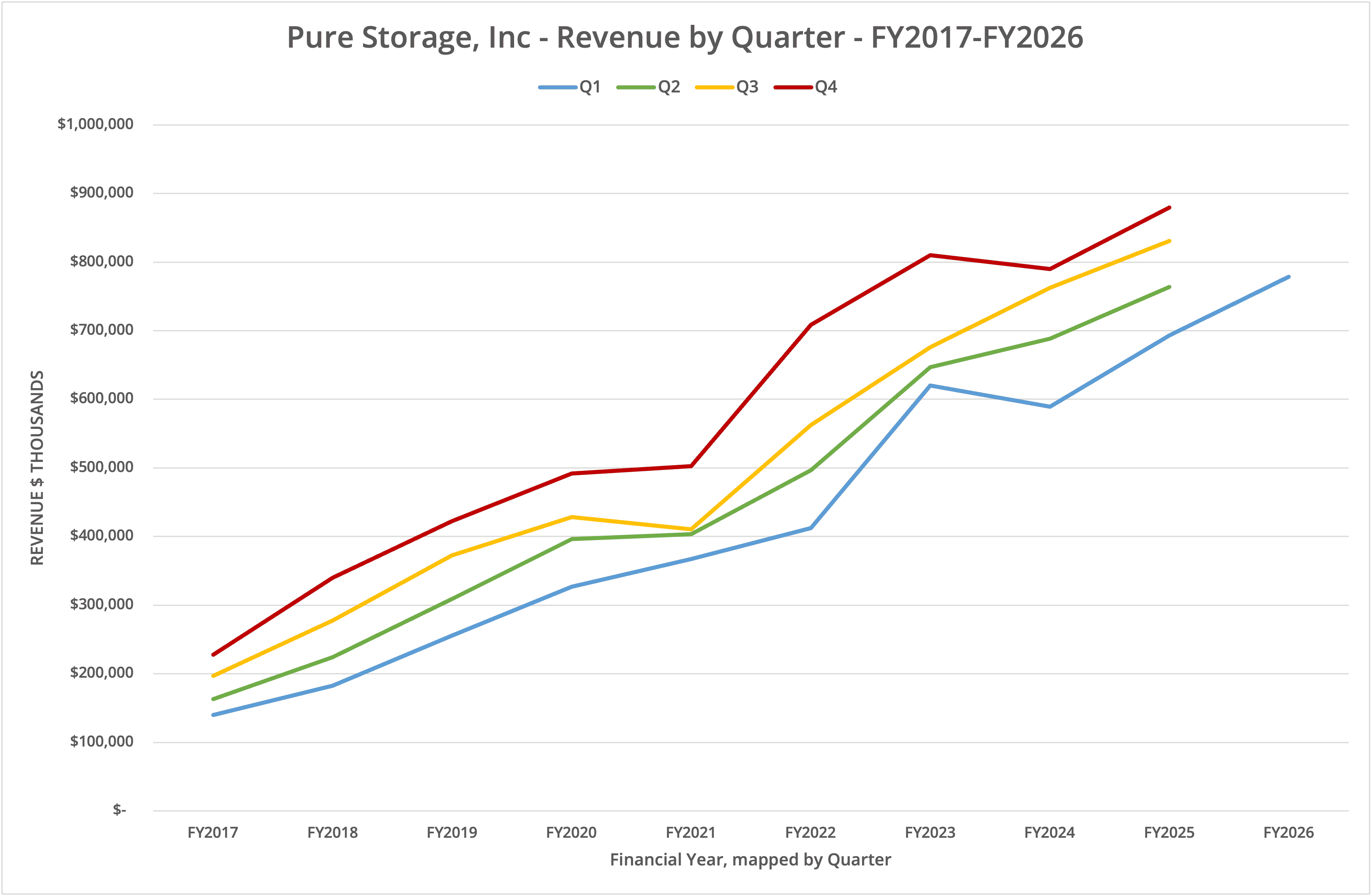

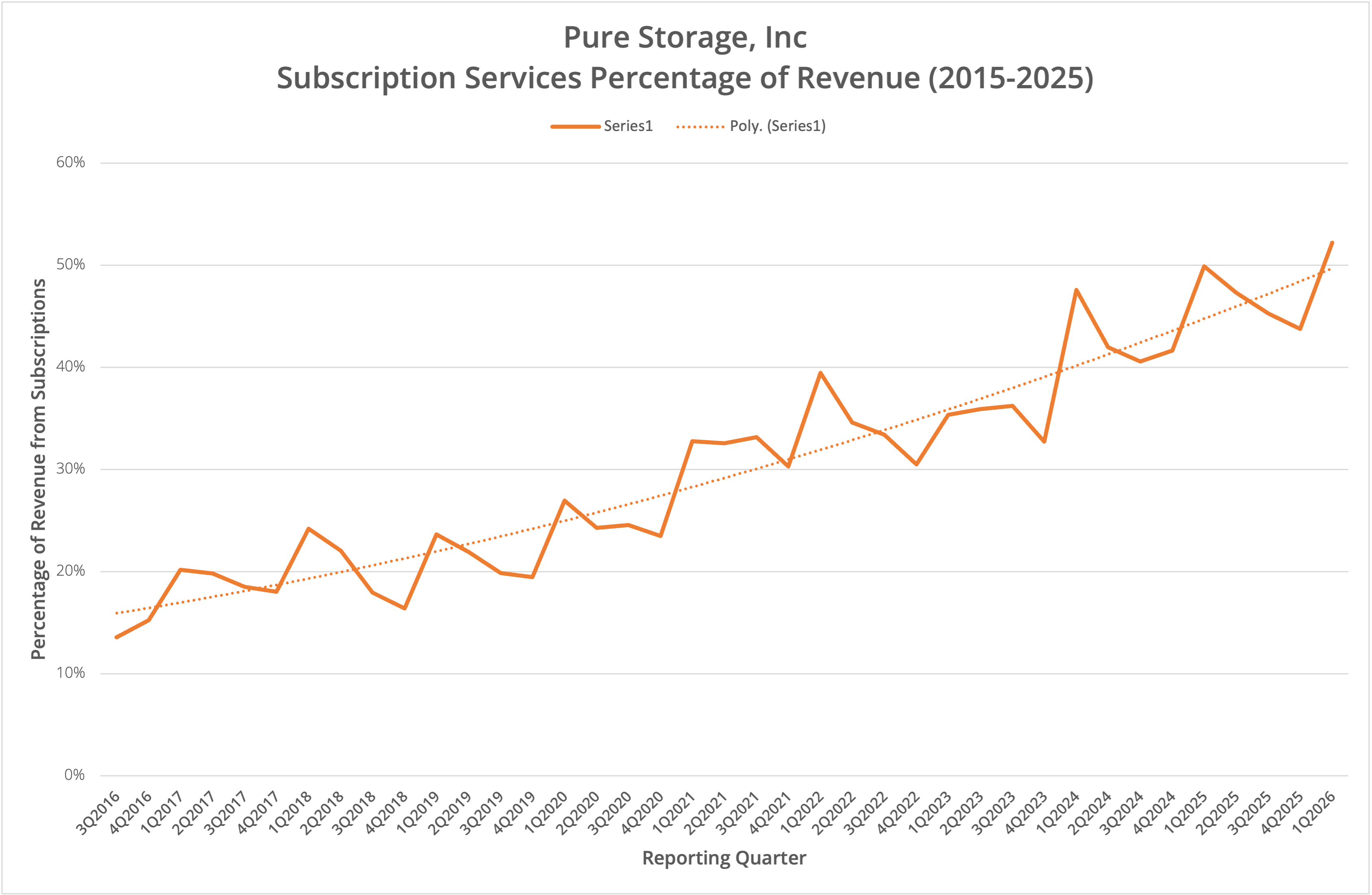

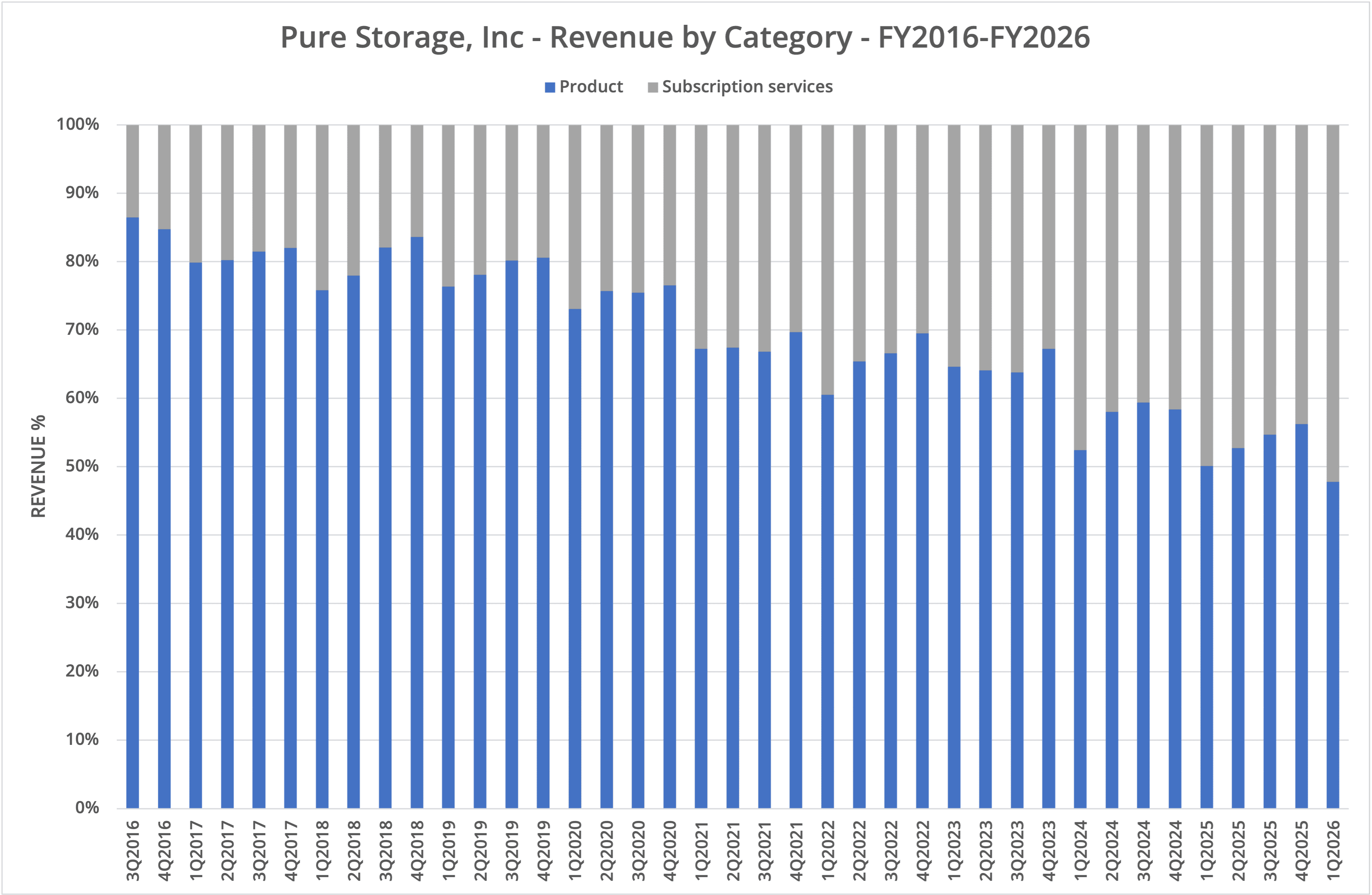

Pure Storage announced financial results for Q1 FY2026, the period ending 4th May 2025, on 28th May 2025. Year-on-year, revenue increased by 12.3%, with Product revenue up 7.1% and Subscriptions revenue up by 17.4%. Subscriptions now account for 52% of revenue contributions, the highest amount to date for the company (Q1 FY2025 was 50%).

We present the data in six graphs, labelled Figures 1 to 6.

Subscriptions

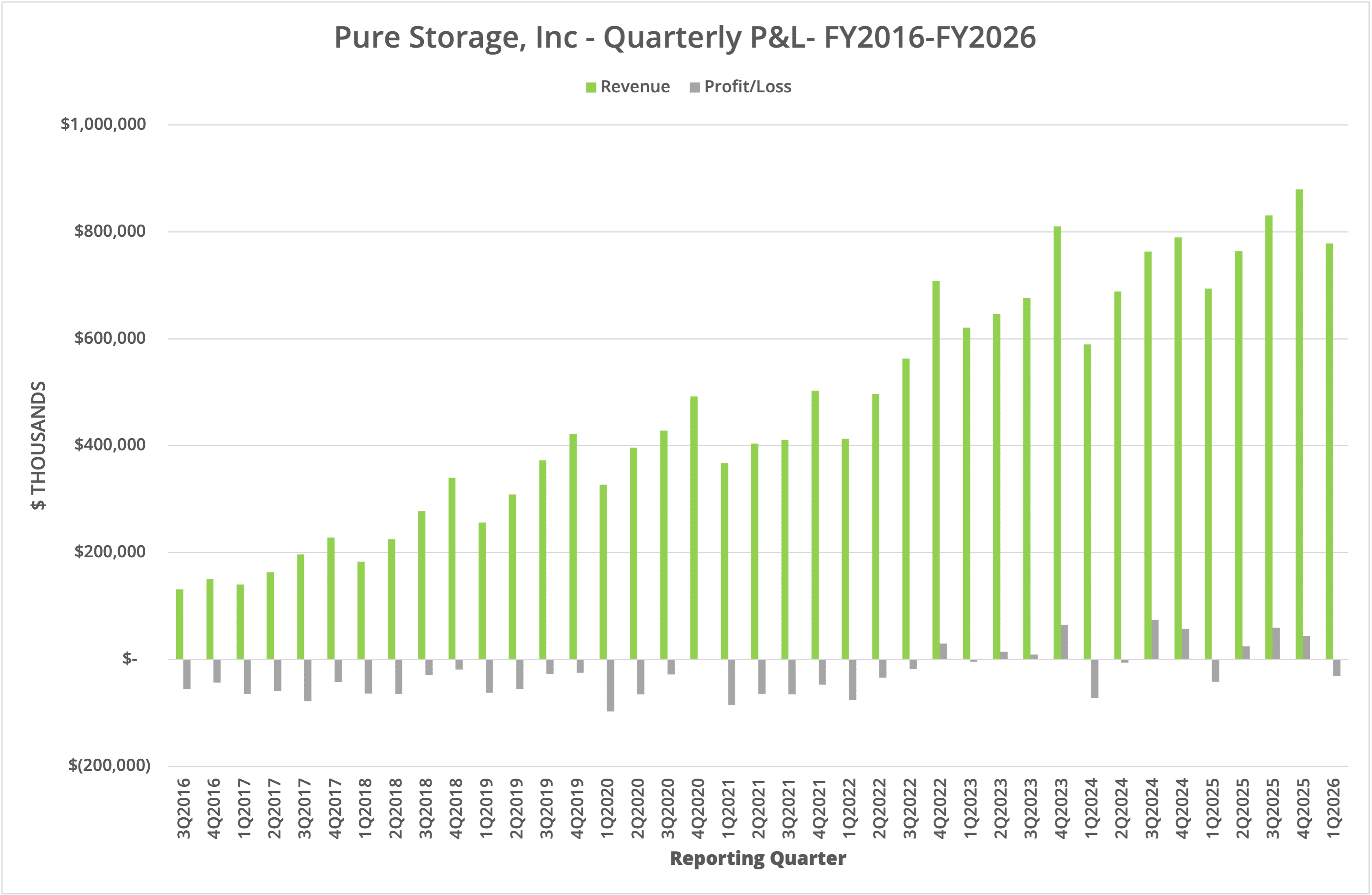

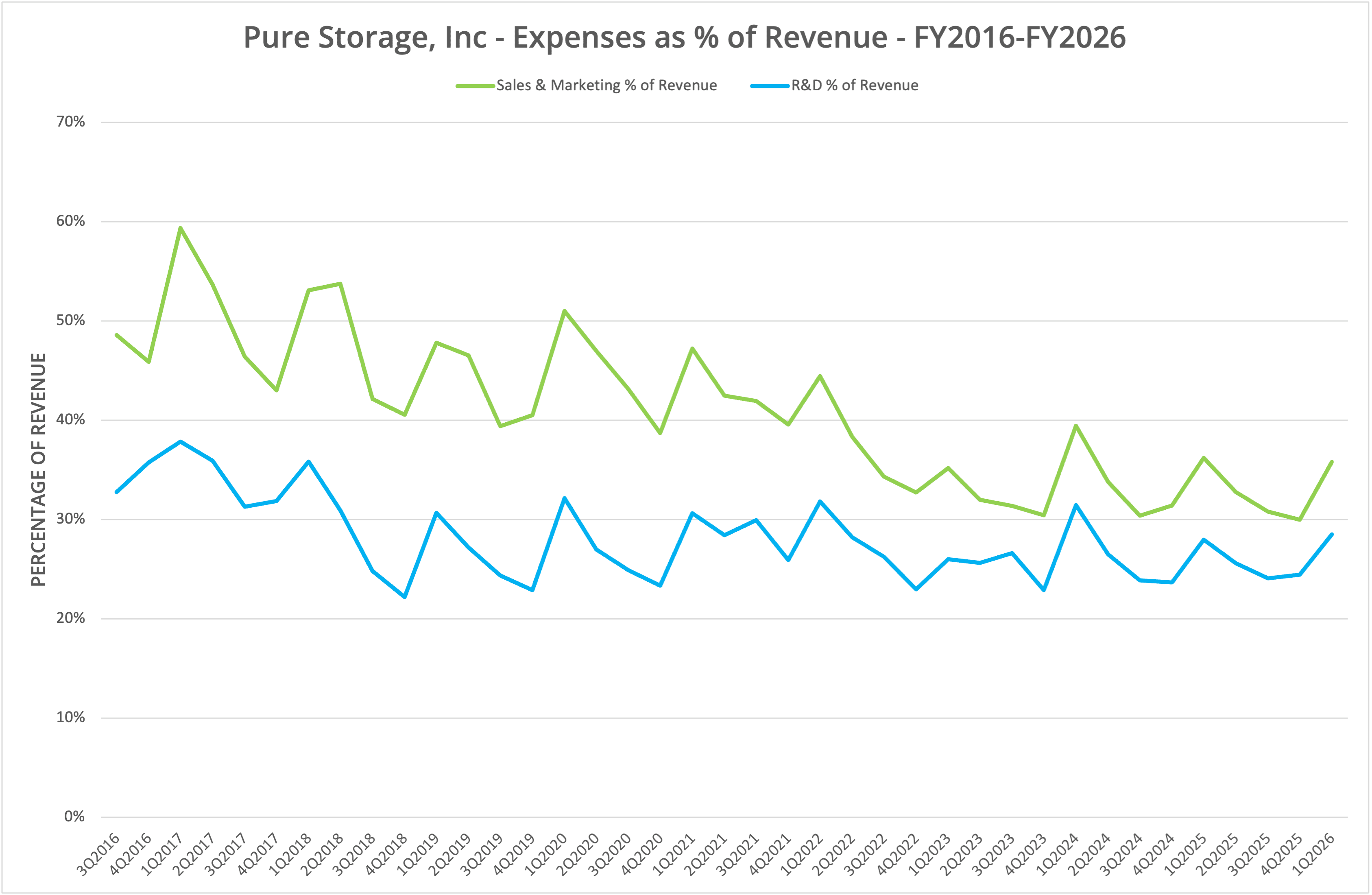

The Product vs Subscriptions mix is fascinating to watch, as clearly it is becoming more expensive to service direct hardware sales. This is borne out by the increase in Cost of Revenue for Products at 38% for the last two quarters. By comparison, the cost of servicing Subscriptions has fallen slightly from 28% in Q1 FY2025 to 25% in the current period. By having almost equal income from two diverse revenue bases, Pure Storage can mitigate the cost of delivery and smooth out any impact. This benefit is reflected in the overall profit/loss statement, which shows a slight loss but better than the equivalent quarter of FY2025 and a historical norm.

Momentum

Pure Storage continues to be one of the few storage companies with an active product and features cadence. During Q1 FY2026, the company announced FlashBlade//EXA, a solution targeted at larger organisations looking for large, cost-efficient scale-out unstructured data stores (coverage here).

The company partnered with Nutanix to integrate FlashArray into NCI, enabling the use of external storage rather than the HCI model typically employed by Nutanix (press release here and our coverage here).

Pure Storage also announced Portworx 3.3 and a series of certifications and extended partnerships (see the press release for the Q1 FY2026 announcement here).

The Architect’s View®

It is easy to assume that the storage market is much less relevant than two decades ago, especially as much of the focus in the general IT industry has turned towards the hype of artificial intelligence.

That perception is reinforced by the discontinuance in storage segment reporting by HPE and IBM, previously seen as leaders in the market. NetApp sales have remained flat for more than a decade, hovering around $6 billion annually (see our last coverage here). In addition, Dell Technologies has seen little growth in storage revenue over the previous decade (see this analysis post for details), albeit with a significant lead over its nearest competitors by some margin.

However, Pure Storage stands out as a vendor that has managed to grow revenue relatively consistently every year. So, what is going on here?

As we mentioned earlier, momentum in feature and product releases is one aspect of the growth in Pure Storage’s business. Of course, starting from a smaller baseline does make a difference compared to an incumbent in the market. But Pure Storage has pulled annual sales of $3 billion from somewhere, either at the cost of their competitors or from growth in the market.

In our analysis, we believe the answer to Pure Storage’s success is differentiation.

- The use of custom hardware is finally paying off by providing economies of scale for larger customers, removing a dependency on storage media vendors and adding additional value in software using a universal FTL in Purity. (Background reading: here and here)

- The SaaS experience using Pure Storage is well ahead of its competitors. Fleet management visualisation and data management across multiple hardware instances is superior to every other vendor in the market, based on the demonstrations we have seen. (Background reading: here, here and here)

- The software abstraction of Purity provides the capability to address the needs of hyper-scalers and very large enterprises. This is a market that is almost impossible for a traditional vendor to target. VAST Data is another good example of a company winning in this segment of the market due to the strength of its software offering. (Background reading: here)

As usual, we always look to the “what next” question, especially with Pure Accelerate just around the corner. We have no crystal ball to provide the answers other than to highlight that Pure Storage addresses the most critical aspect of business – providing what the customer needs to increase their business and become more efficient versus their competitors. We’re sure that this year’s Pure Accelerate will be no different, making the event a must-watch for companies looking for the best solutions on the market.

X-Ray: Pure Storage, Inc. (Third Edition)

This Architecting IT report takes a deep dive into Pure Storage’s history, products, services, and future outlook. This report is only available for download via paid subscription.

Copyright (c) 2007-2025 – Post #22a4 – Brookend Limited, first published on https://www.architecting.it/blog, do not reproduce without permission. Pure Storage is a Tracked Vendor for data storage solutions.