NetApp, Inc. has announced financial results for the fourth quarter and the full year FY2025. Revenue is at the highest ever for a single year at $6.57 billion, with a corresponding record quarter for Q4 ($1.73 billion revenue). However, gross margins continue to decline, so is the outlook for NetApp as rosy as it seems?

Background

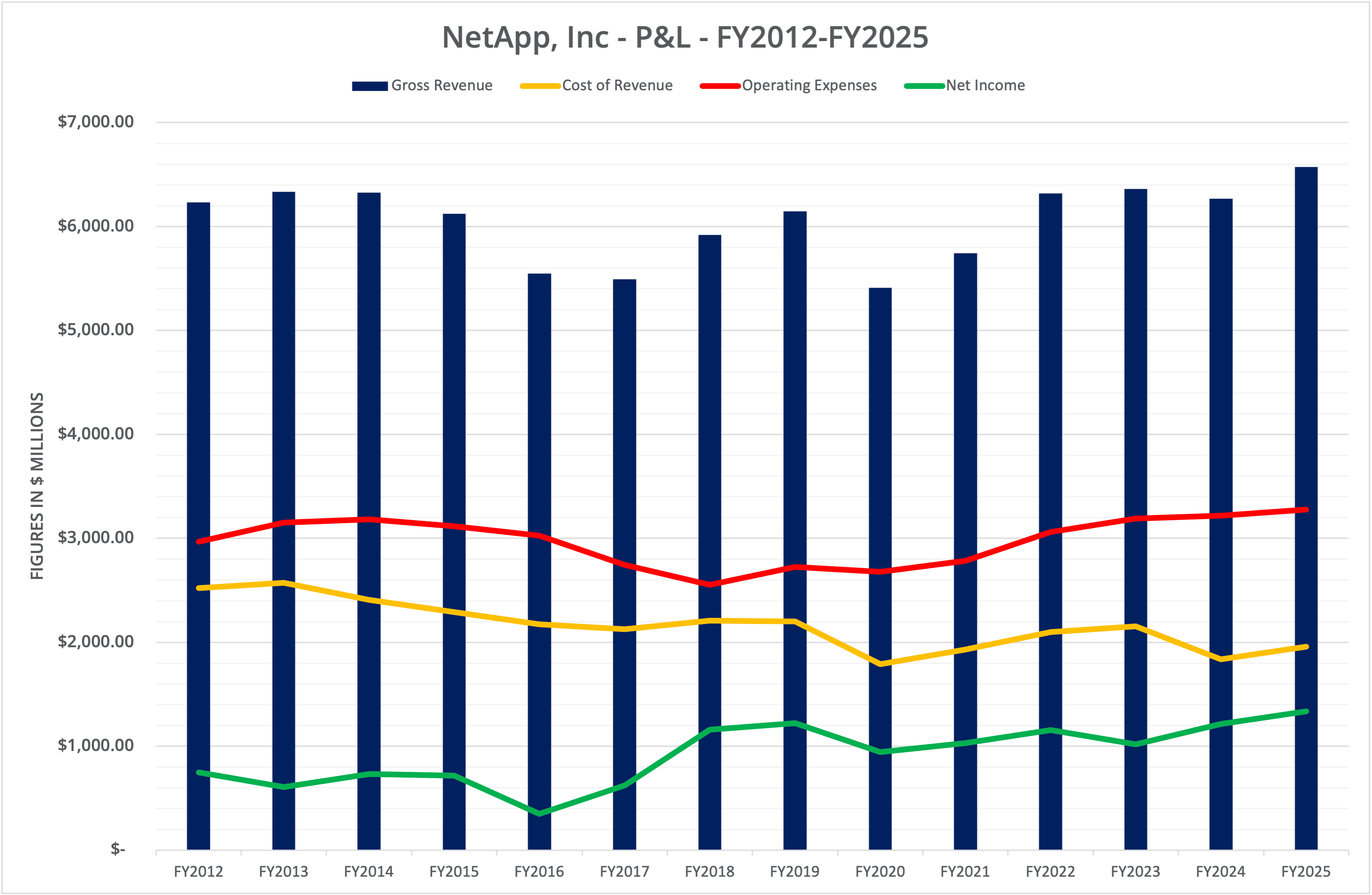

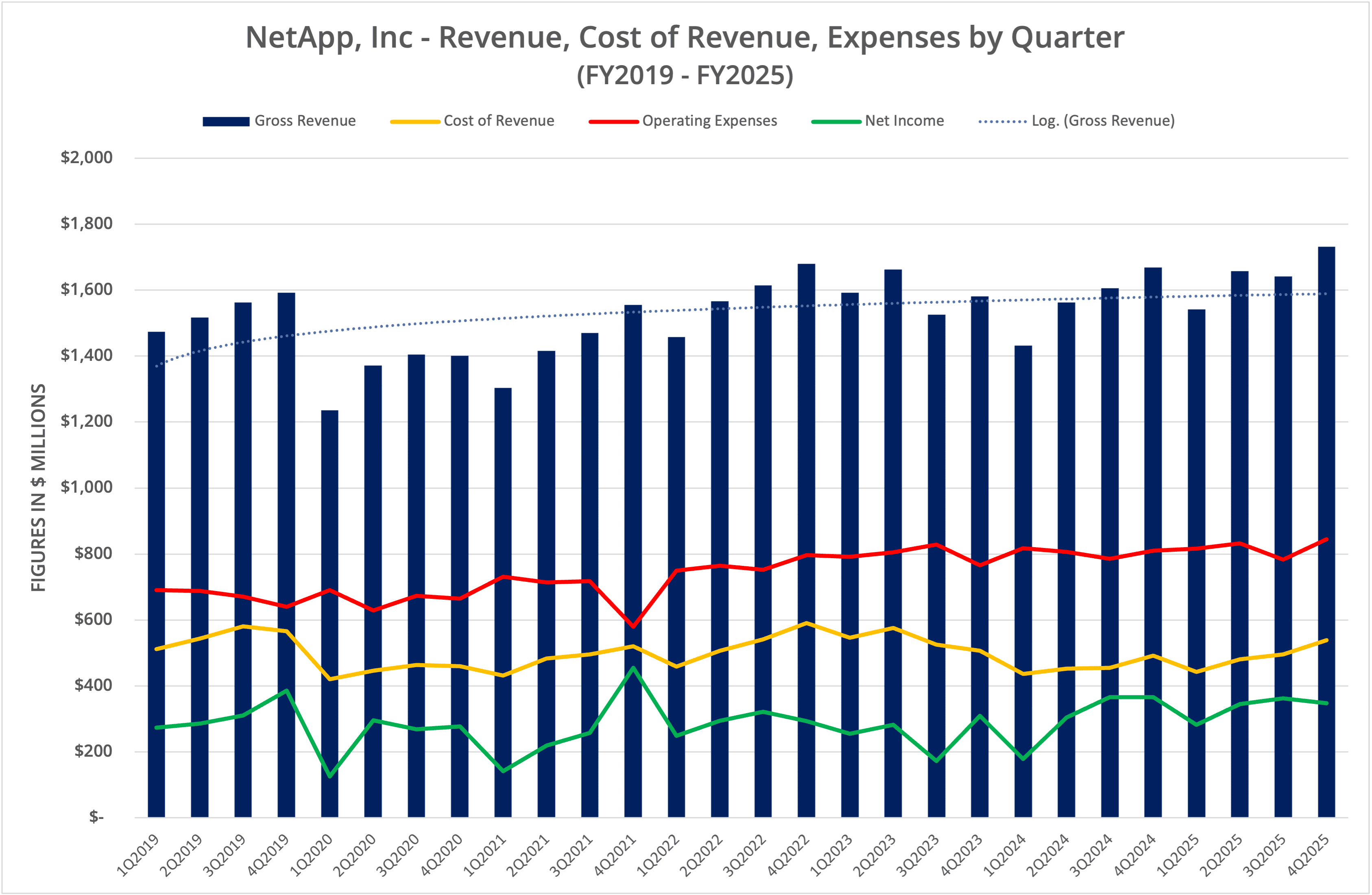

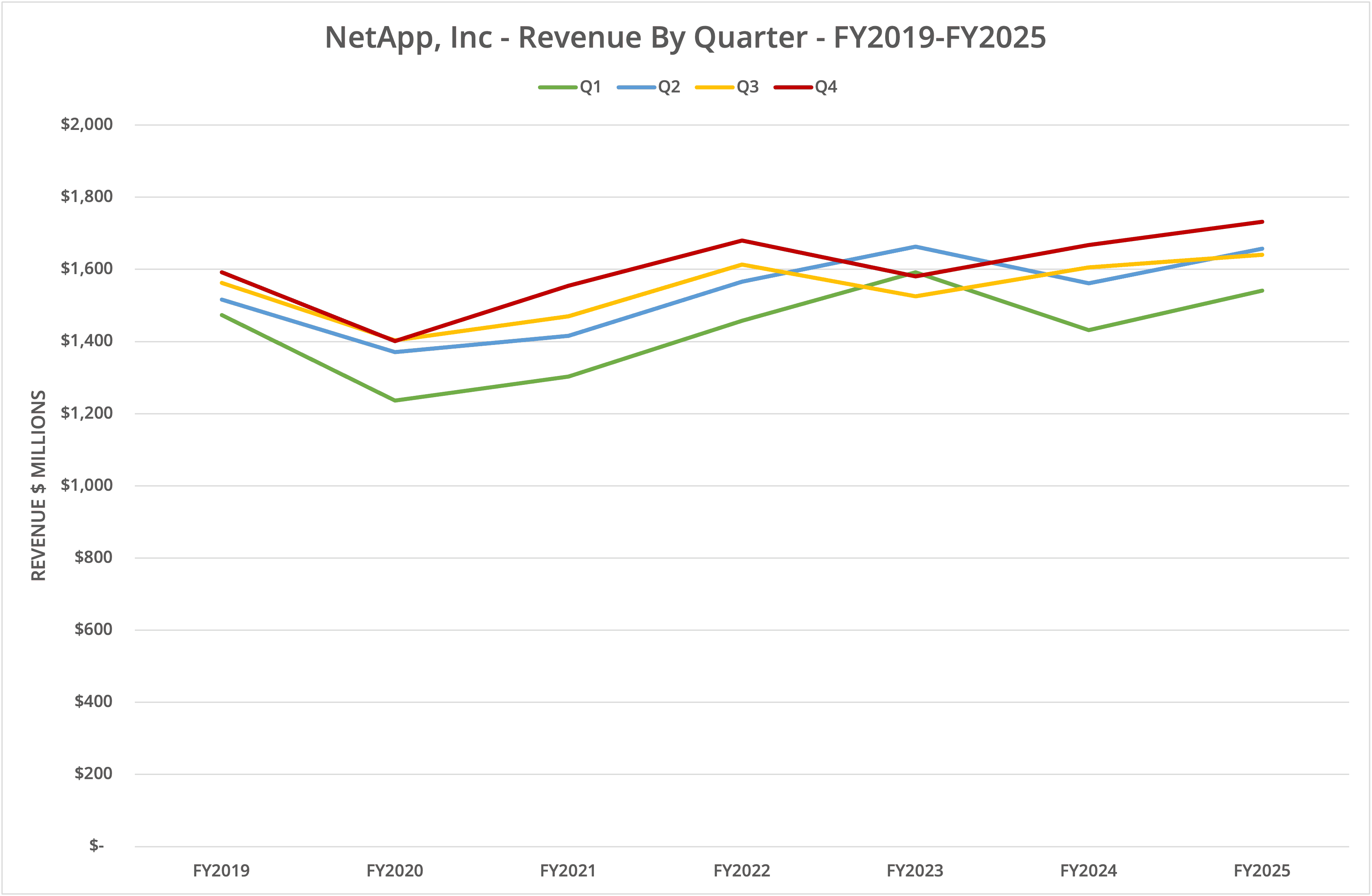

NetApp, Inc. published financial results for Q4 FY2025 and the full year, the period ending 25th April 2025, on 29th May 2025. For the quarter, revenue was $1.73 billion, up 3.8% year-on-year and 5.5% sequentially. For the full year, FY2025 revenue was $6.57 billion, up 4.9% on FY2024.

We present the data in six graphs, labelled Figures 1 to 6.

Growth

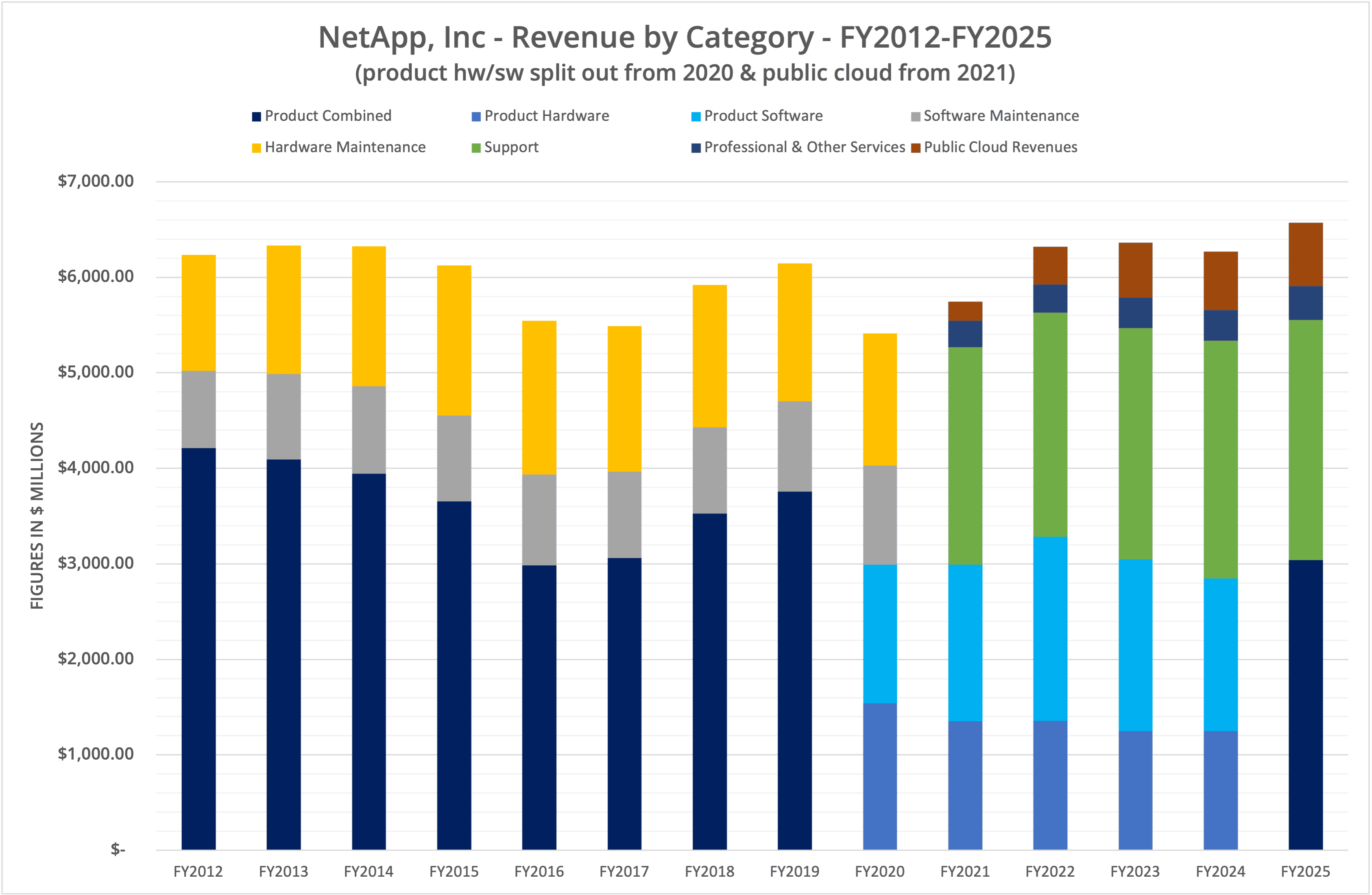

The positive news for NetApp is the overall growth in revenue achieved in Q4 and for FY2025 in total. Looking at the details, Product sales accounted for 46% of revenue, Support approximately 38% and Public Cloud 10.1%. For FY2025, NetApp combined the previous categories of Product Hardware and Product Software, so we have no specific details of what did well within the product mix.

However, NetApp highlighted all-flash array ARR at $4.1 billion (up 14% year-on-year) and record first-party and marketplace Public Cloud revenue of $416 million, up 43% year-on-year.

Cloud

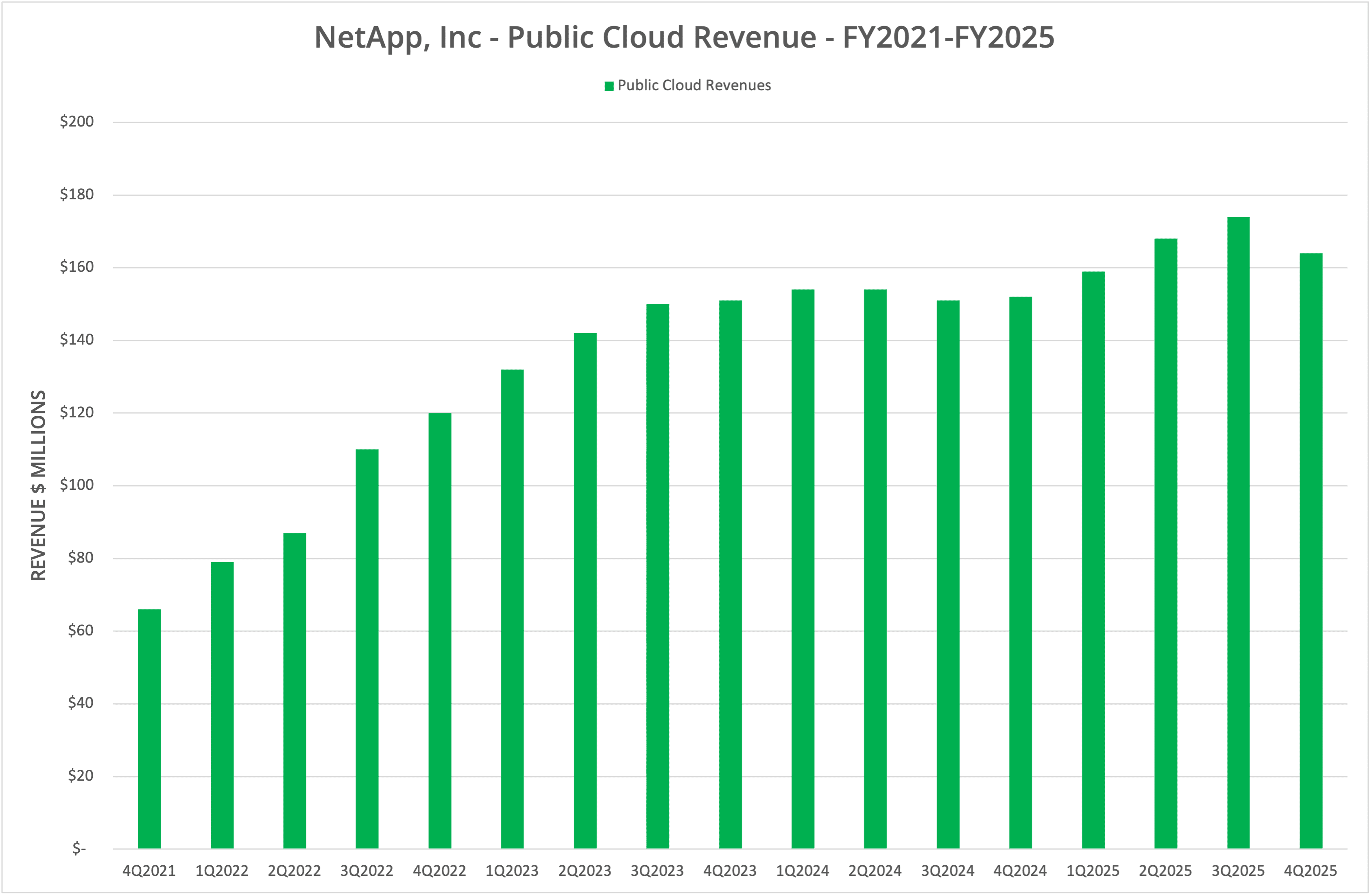

Looking at Public Cloud in particular, revenue grew 8.8% for the year to $665 million. As we show in Figure 6, Public Cloud revenue grew steadily until the end of FY2023, then plateaued and returned to growth until the current quarter, which saw a 5.7% decline.

Some of this reduction in revenue could be attributed to the sell-off of cloud-based services to Flexera in January 2025. We will need to wait and see how the next quarter looks. In the post-announcement transcript, NetApp highlighted that excluding the Spot business, Public Cloud revenue grew 22% year-on-year.

Gross Margin

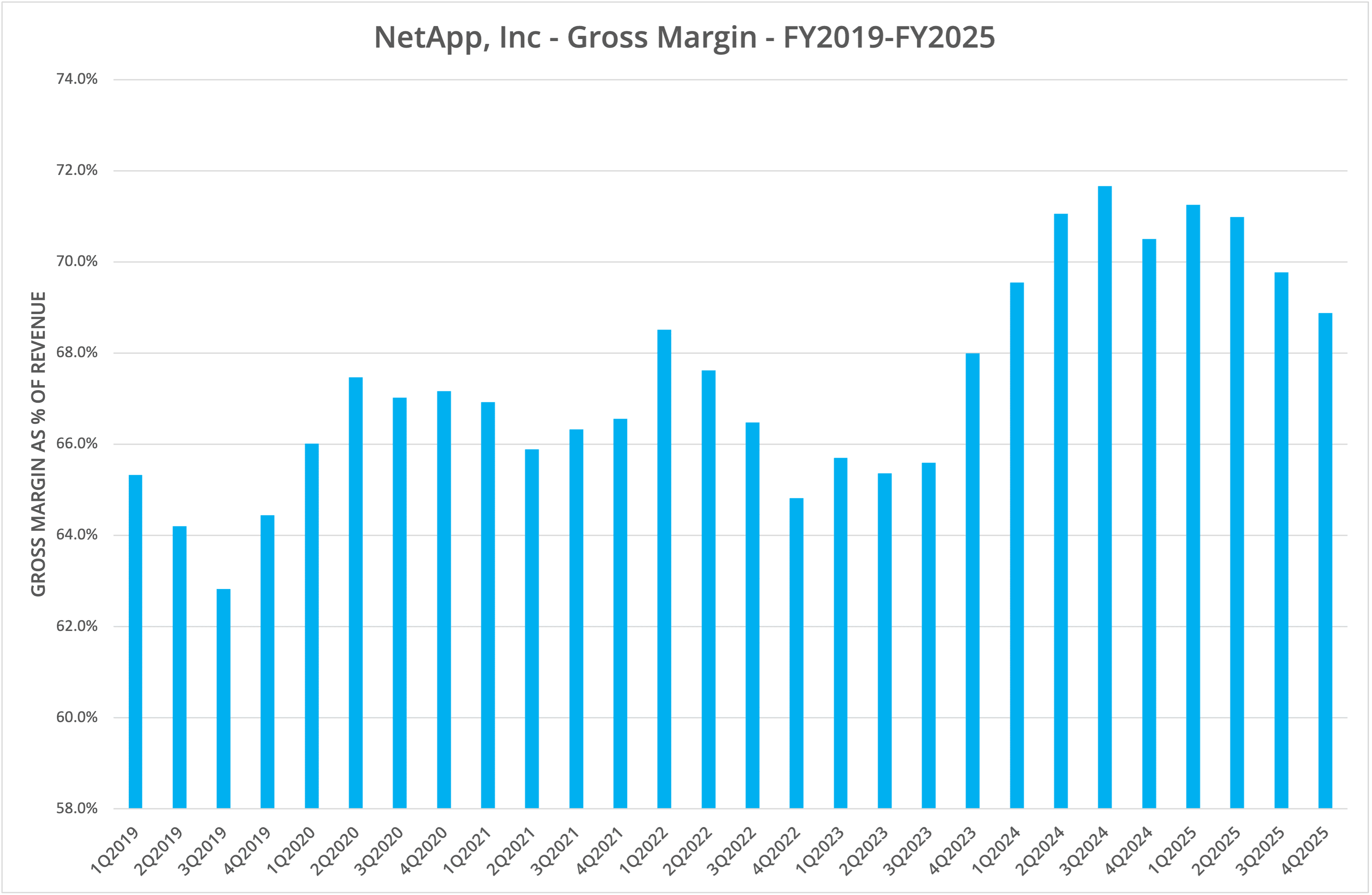

One particular aspect that looks concerning is the reduction in gross margin, which dropped to 68.9% in the current quarter (see Figure 5). Overall gross margin has been in decline since the start of the year. The post-announcement transcript tells us that Product margin is around 55.4%, while Public Cloud margin is 79.3%. Hybrid Cloud margin is somewhere in between at 68.4%.

Naturally, refocusing the business on hardware sales will have a direct effect on gross margin, which is reflective of the recent evolution of the company. However, NetApp expects to see gross margin improve during FY2026 to between 71% to 72%.

The Architect’s View®

During FY2025, NetApp refocused its business on hardware platforms, refreshing the entire range of solutions offered while continuing to expand segments such as the All-SAN Array (ASA). Much of the investment in the Spot business was sold off to Flexera in January 2025, although some components do remain. What’s left is now part of new solutions, such as the Workload Factory, rather than a separately marketed entity.

Undoubtedly, the financial numbers are good for NetApp, but what we are seeing is a return, once again, to core values, namely products and services based around ONTAP. The all-flash segment will eventually be the de-facto business, so reporting on this revenue will cease to be of value.

The big question to ask is whether the hardware strategy is the right approach for the business and for customers.

The emphasis on improving the range and capability of on-premises storage systems is definitely a win-win, both for customers and for NetApp. Customers who are bought into the NetApp ecosystem have more choice of products in a range of solutions that are continuously improved and upgraded. The result of this approach is clear as Product revenue continues to grow.

In the public cloud, while cloud-native implementations of ONTAP have been a relative success, growth has stalled, and it is unclear whether NetApp has managed to restart a positive trend upwards. Challenges for customers are the cost of the solution plus a degree of complexity when integrating with on-premises storage (one of the big selling points).

Remember that for many years, the cloud platforms regularly reduced the cost of storage, then evolved into a strategy of static costs while adding (or removing) functionality. Perhaps NetApp needs to do more of the same.

The elephant in the room, though, is the failed Spot strategy, where NetApp looked at the Public Cloud as a possible major revenue stream. That vision is all but dead with the sale of Spot to Flexera. So, what comes next? How will NetApp address future growth? This a question we will discuss in separate coverage.

Copyright (c) 2007-2025 – Post #66c6 – Brookend Limited, first published on https://www.architecting.it/blog, do not reproduce without permission. NetApp is a Tracked Vendor for data storage solutions.