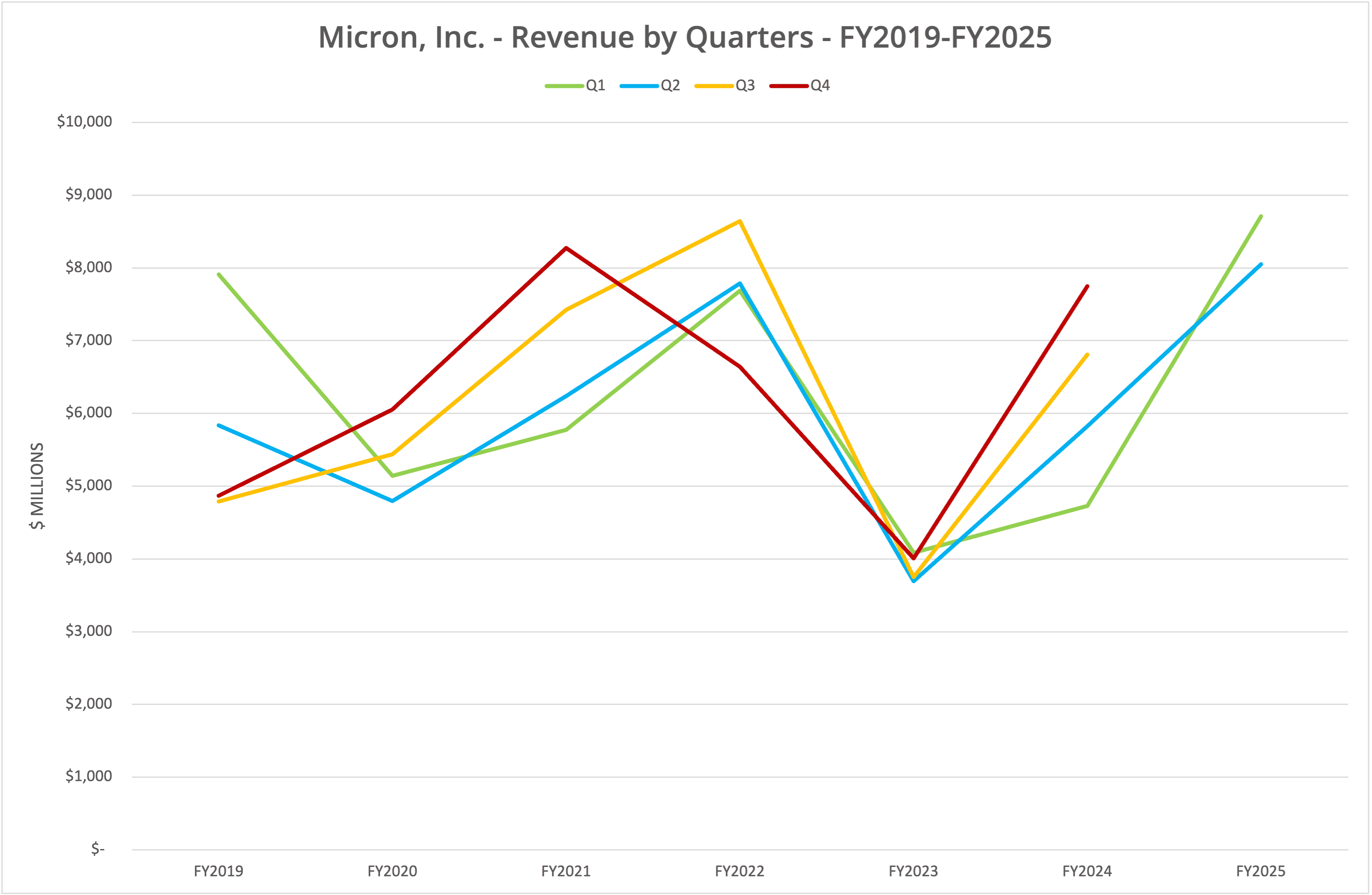

Micron Technology, Inc. has announced financial results for the second quarter of FY2025, ending 27 February 2025. Revenue for the period was up 38.3% compared to Q2 FY2024, at $8.05 billion. However, revenue declined sequentially by 7.5% compared to Q1. Micron is heavily dependent on the high-performance memory business, which could represent a benefit or disadvantage based on the current US tariff policy.

Background

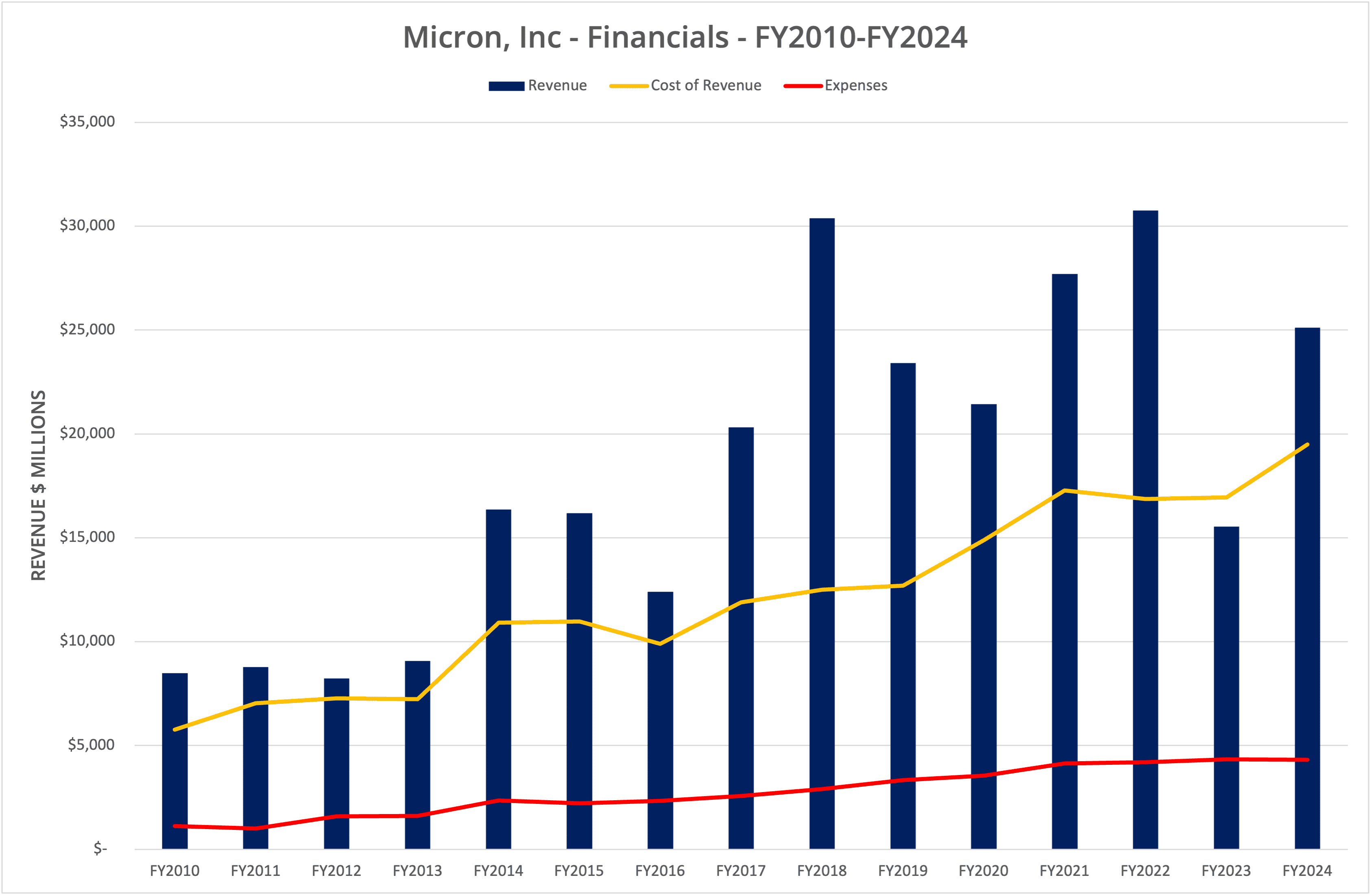

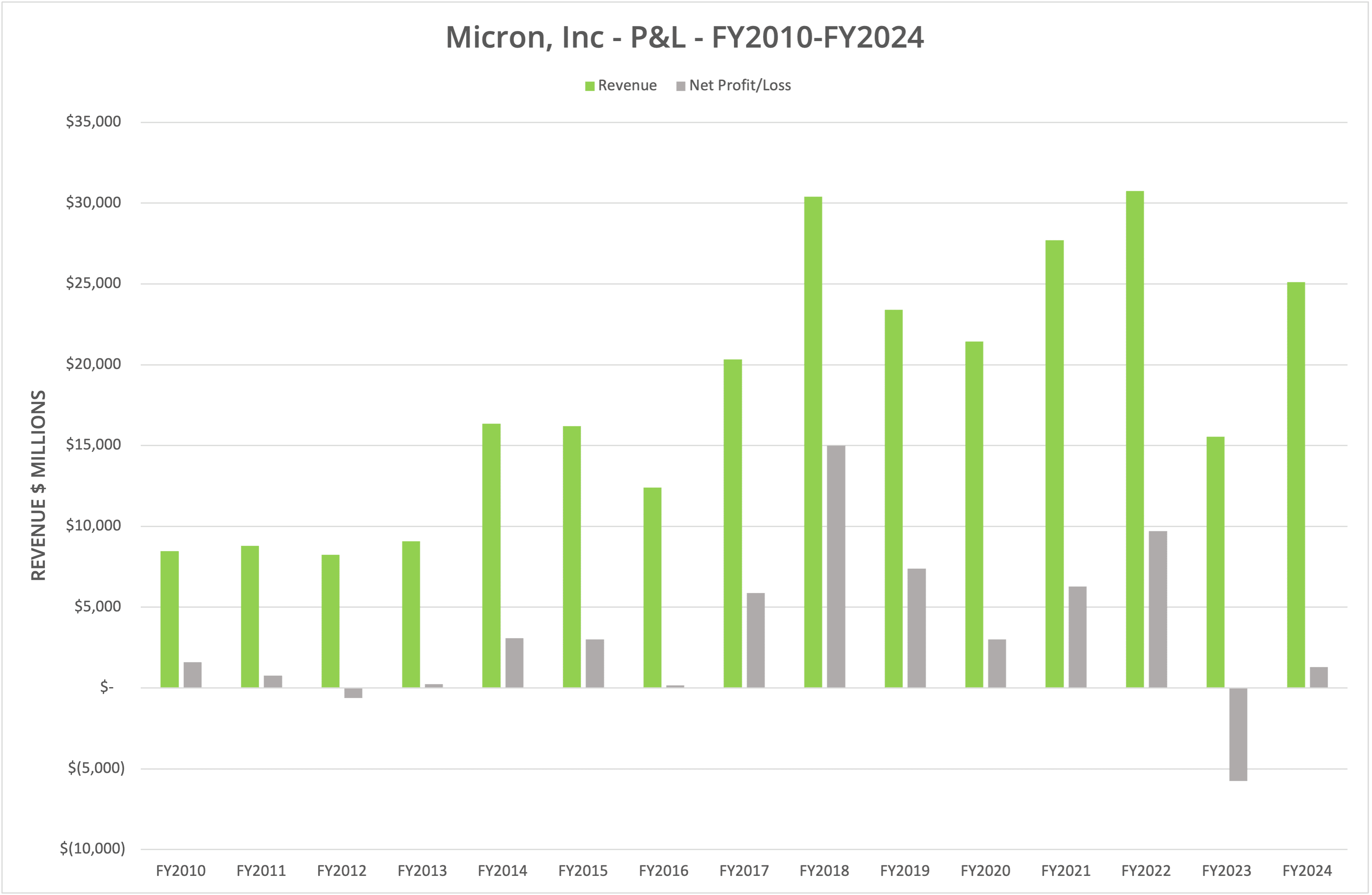

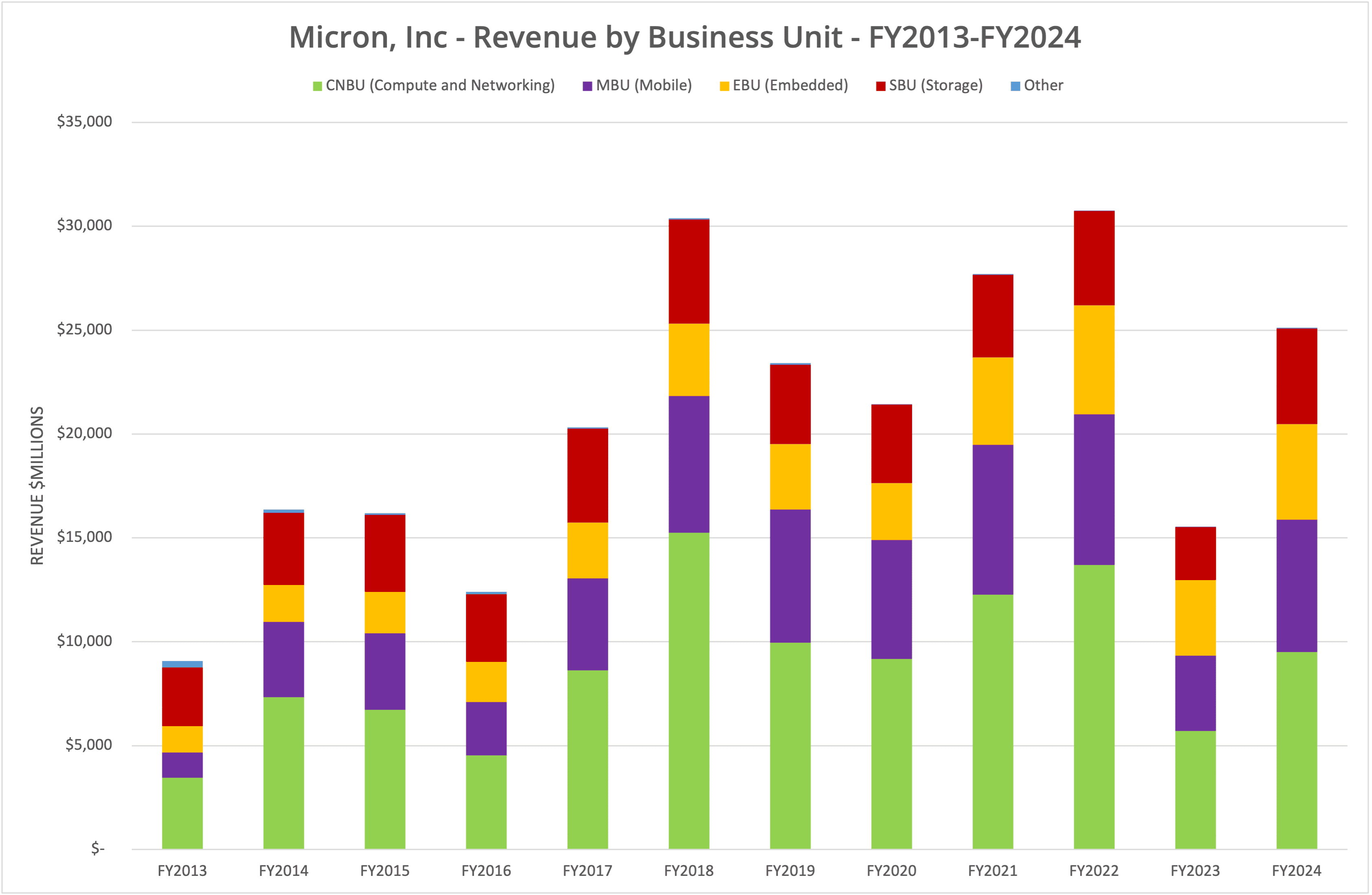

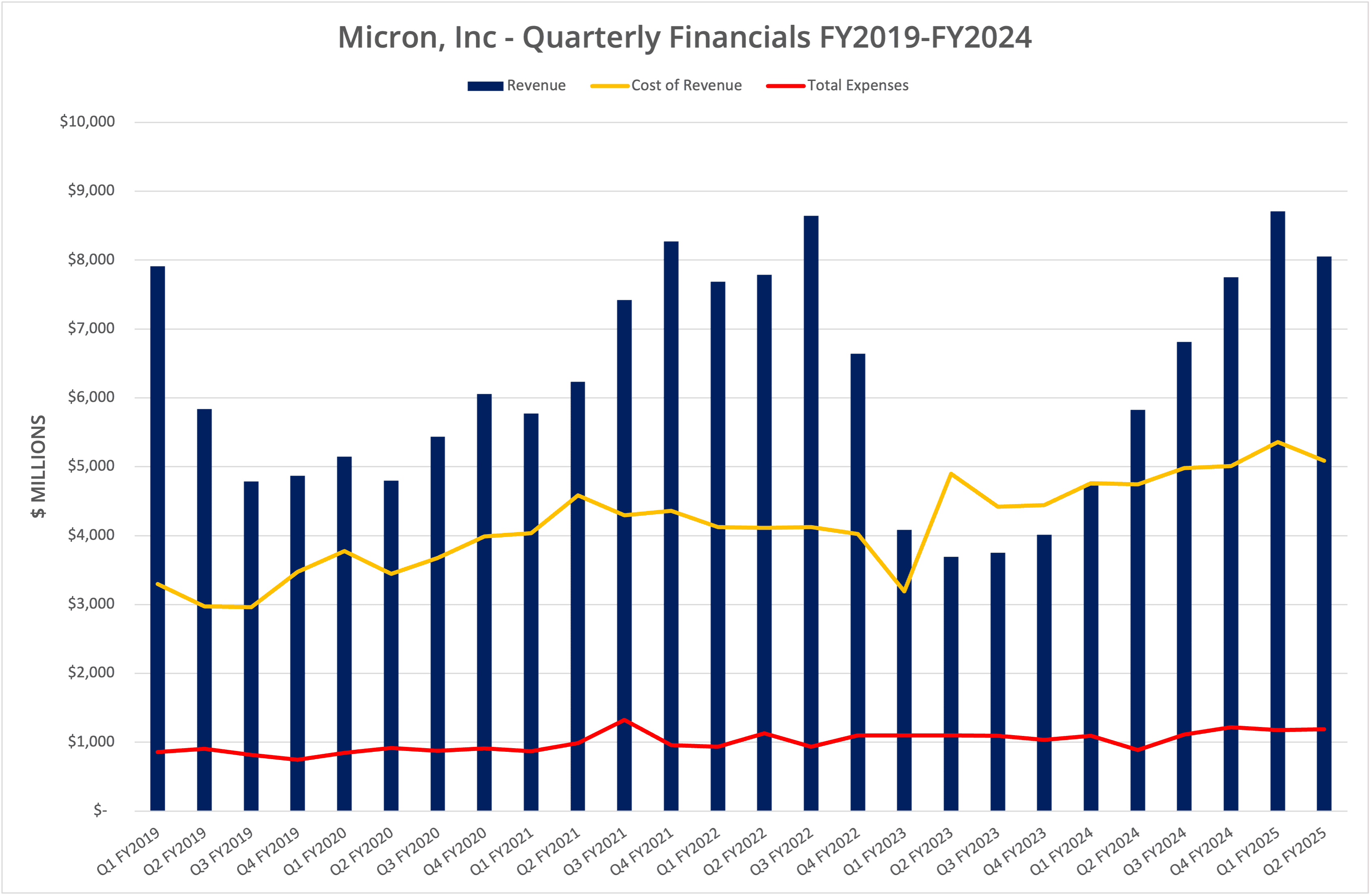

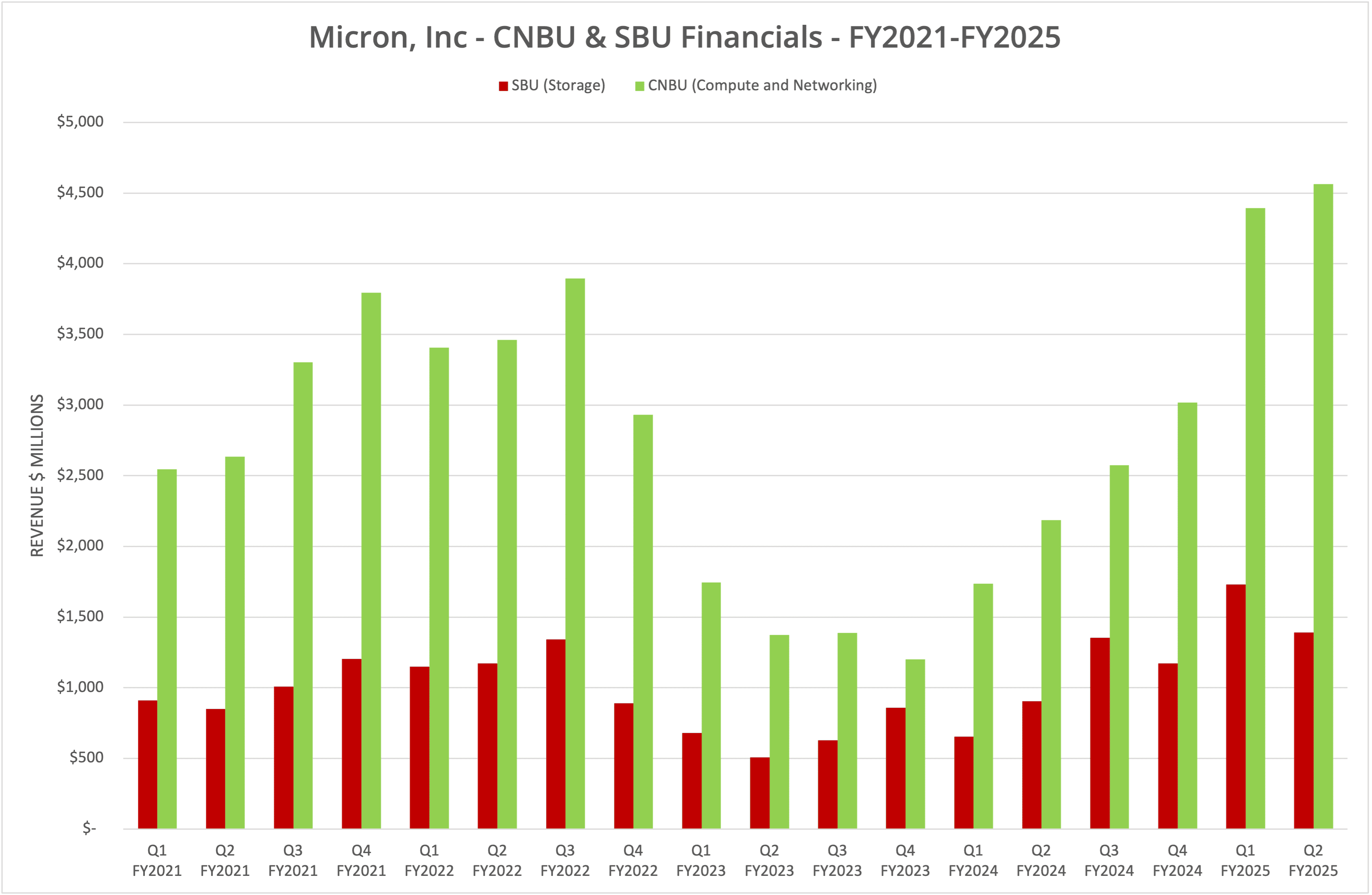

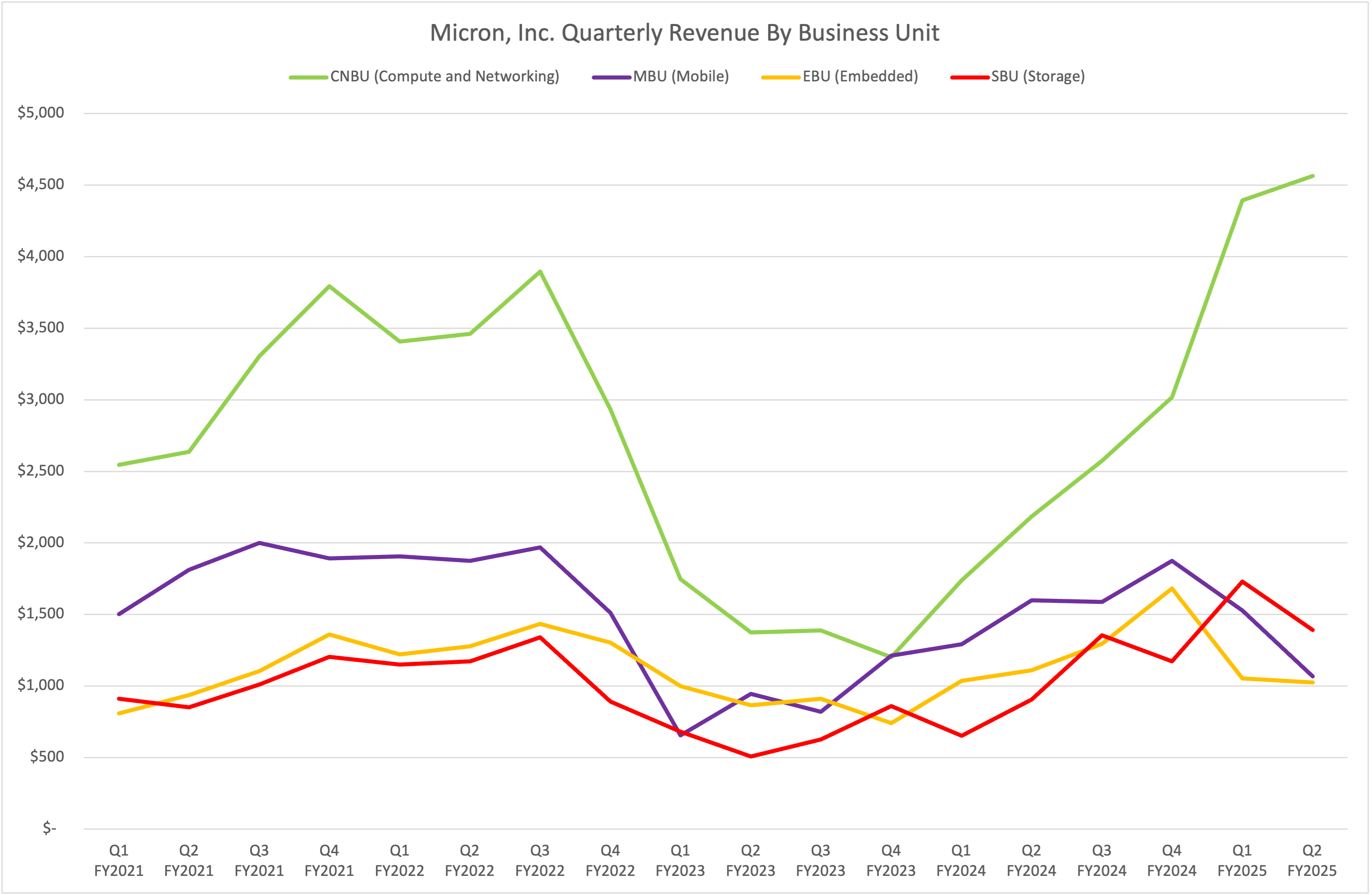

Micron Technology, Inc. declared financial results for Q2 FY2025, the period ending 27 February 2025 on 20 March 2025. Revenue grew by 38.3% to $8.05 billion compared to Q2 FY2024 but declined sequentially by 7.5% (Q1 revenue was $8.71 billion). By division, the Compute and Networking business unit (CNBU) grew by 109%, while storage rose by 54%. Mobile and Embedded business units both declined by 33.2% and 7.7%, respectively.

We present the data in eight graphs, labelled Figures 1 to 8.

HBM

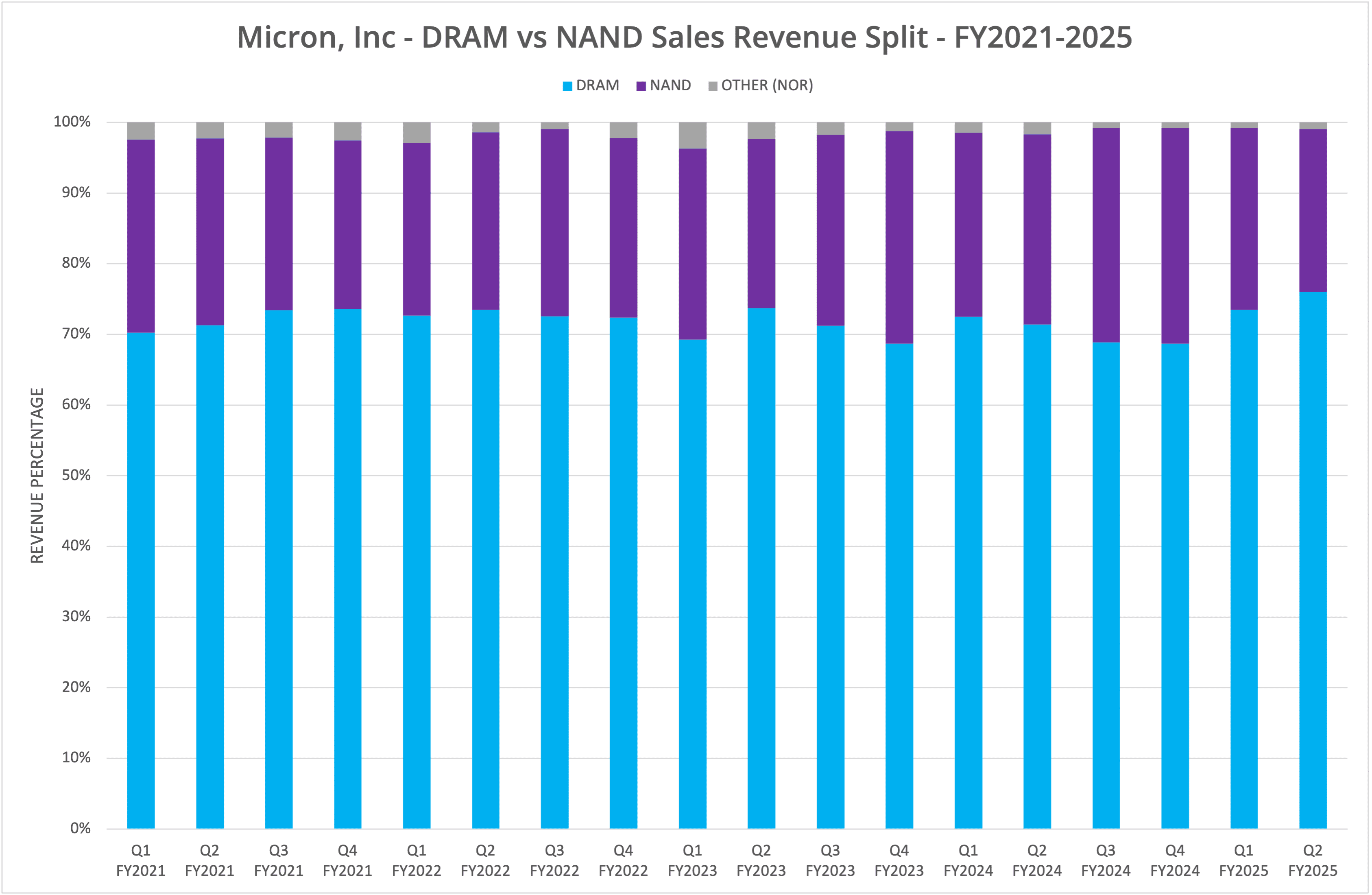

Micron divides its revenue by semiconductor product type, specifically DRAM (memory), NAND (storage) and Other (mostly NOR). Historically, DRAM has represented around 75% of Micron revenue – 76% in the current reporting period (see Figure 7). This makes the business heavily dependent on DRAM production, which is focused on the value High-Bandwidth Memory (HBM) market. HBM is in big demand for incorporation into GPUs and other similar products.

To that extent, in the current reporting period, Micron indicated that its entire 2025 calendar year inventory of HBM is already sold out, with strong demand for 2026. Micron DRAM is built on process nodes in the 10-19nm range, which was initially named 1x, then 1y and 1z. The naming has continued with Greek letters, specifically 1-alpha, 1-beta and the latest iteration, 1-gamma, which is the first Micron DRAM to use EUV (extreme ultra-violet) etching technology. 1-gamma delivers around 30% bit-density improvement over 1-beta, with 20% lower power consumption and 15% improved performance.

NAND

Volume production of Micron’s 9th generation NAND (branded G9 NAND) was announced in July 2024, with the release of the 2650 NVMe SSD. The 2650 is an M.2 (“gumstick”) format SSD with TLC NAND, up to 1TB capacity and 6,200 MB/s sequential read capability. In the data centre, Micron claims its 9550 NVMe SSD is the fastest on the market, delivering 14,000 MB/s sequential read throughput. The 9950 uses G8 NAND, supports a PCIe 5.0 interface and capacities up to approximately 31TB.

Tariffs

Clearly Micron has competitive products, selling HBM3E 8H (eight stacks) to NVIDIA for incorporation into the GB200 GPUs and HBM3E 12H for the GB300. In the NAND market, Micron has a long partnership with Pure Storage, announcing further collaboration in a press release in January 2025. G8 NAND is currently used in Pure Storage’s 150TB DirectFlash Modules.

Micron, a US enterprise based in Boise, Idaho, currently manufactures around 10% of its output in the US. The company received around $6.1 billion in CHIPS Act funding, announced in April 2024, that will be used to build fabrication plants in New York state and Idaho. Although agreed with the previous US administration, the current Trump government in the White House will be keen to see these new facilities producing products, which are expected in the next two to three years and aim to reach 60% of production in the US.

Of course, many uncertainties remain. Can Micron produce products of the same quality and cost as its overseas facilities? It is clear that partners like Pure Storage will be keen to see the availability of both DRAM and NAND products without tariffs, as the storage appliance market (for example) remains highly competitive.

The Architect’s View®

Although we’ve followed Micron as a business for many years, we are only just beginning the alignment of our business coverage of the company with the technology. As a result, this post represents a stake in the ground from which we will continue to build more detail.

Micron clearly has strength in two major component markets that are being strongly driven by the AI hype cycle. As with any component business, both revenue and profit trends are generally cyclical. We will continue to focus on Micron as a technology business and report financials as a reflection of the strength of that technology in the market.

Related Content

- Micron discontinues 3D XPoint – what next for Intel Optane?

- Micron ushers in the era of QLC SSDs

- Flash Diversity: High Capacity Drives from Nimbus and Micron

Copyright (c) 2007-2025 – Post #38c3 – Brookend Limited, first published on https://www.architecting.it/blog, do not reproduce without permission.