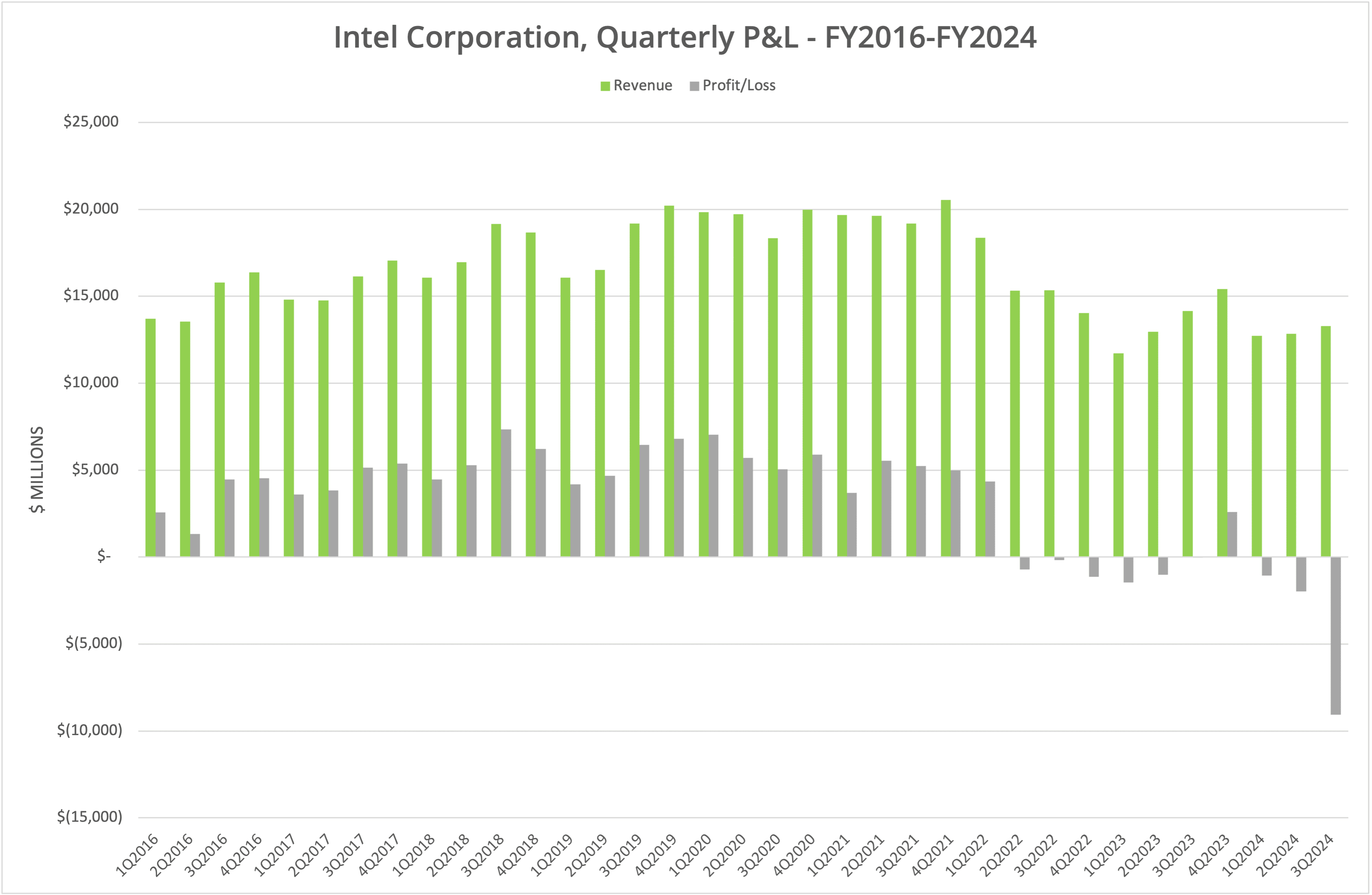

Intel Corporation has announced financial data for the third quarter of financial year 2024, and the results make for grim reading. Revenue declined 6.2% year-on-year (although it was up 3.5% sequentially) at $13.3 billion. Cost of revenue due to restructuring charges was higher, resulting in a gross margin of only 15%. Overall, with other additional impairments, Intel declared a $16.6 billion loss. However, with significant restructuring behind it, is there light at the end of the tunnel?

Background

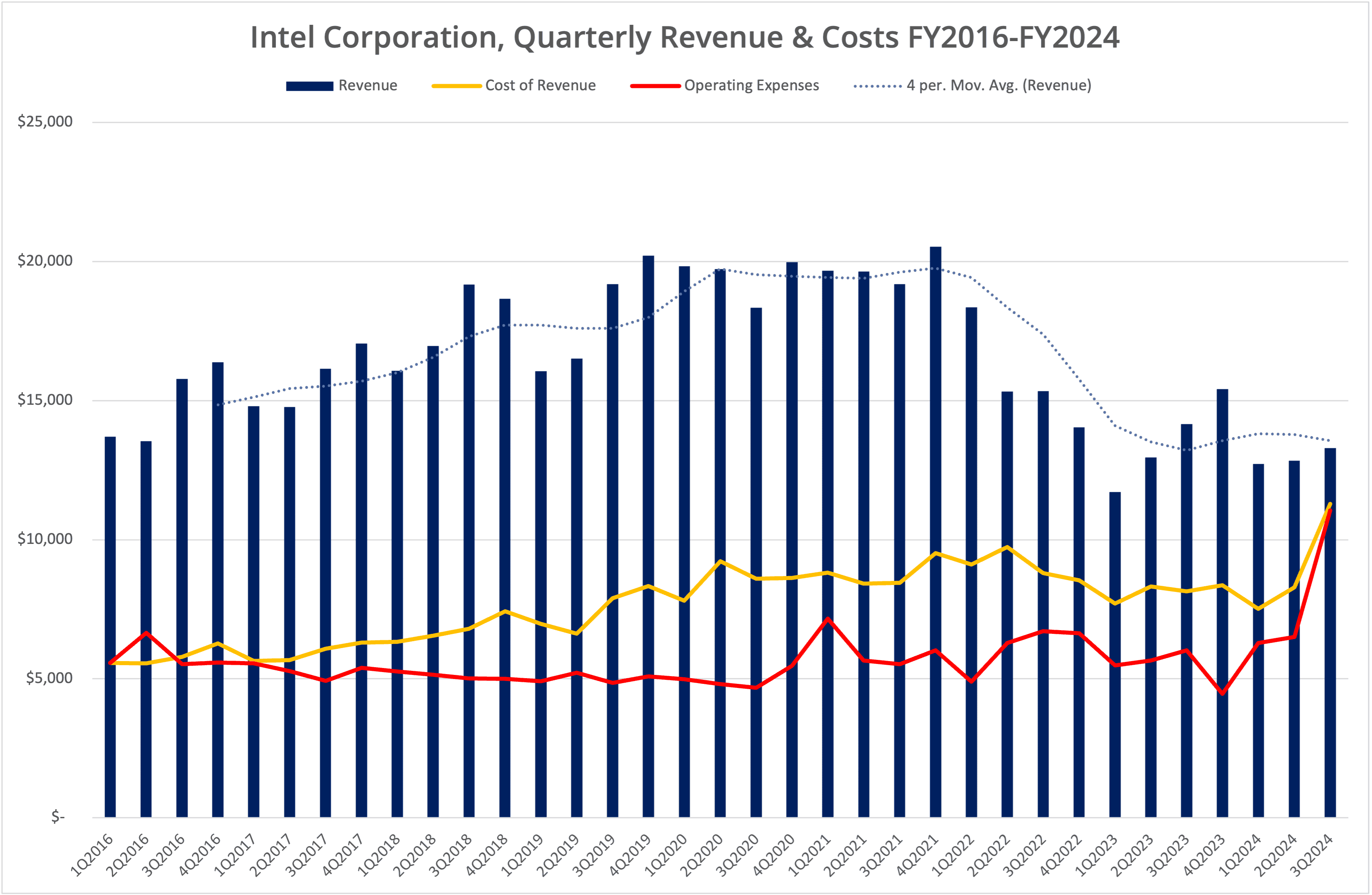

Intel Corporation announced financial results for Q3 FY2024, the period ending 28 September 2024, on 31 October 2024. Revenue was down 6.1% year-on-year compared to Q3 FY2023 at $13.3 billion but up 3.5% sequentially compared to the previous quarter. However, cost of revenue was up significantly, resulting in a 15% gross margin, compared to typical quarters of between 35-40%.

Intel also took significant impairments (which we will discuss in a moment), resulting in a net loss before tax adjustments of $9 billion and an overall loss of $16.6 billion, which includes almost $8 billion in adjustments for deferred tax asset benefits. We are not financial analysts, so we recommend reading the post-announcement call transcript, which provides more details and can be found here. We present the details from the announcement in 4 graphs, labelled Figures 1 to 4.

Restructuring

There are significant restructuring costs in the Q3 financial results, stemming from the reduction in workforce numbers announced earlier in the year. This amounted to $2.2 billion in the period, mainly attributed to cost of revenue (hence the reduced margin). There was also $2.6 billion of goodwill impairment attributed to the Mobileye subsidiary.

Of more interest is the information provided on the write-down for the transition from Intel 7 process towards 18A, which resulted in a $3 billion impairment. Additionally, CEO Pat Gelsinger indicated that the AI Accelerator products (Gaudi 2 & 3) would not achieve the expected $500 million in revenue predicted for 2024. Contrast this with the results of AMD, also announced this week, where the data centre business attributed significant revenue growth (122% in the Data Centre Segment) from the competing MI300X products. One issue here appears to be the quality of software tools used to exploit the Gaudi products.

Growth

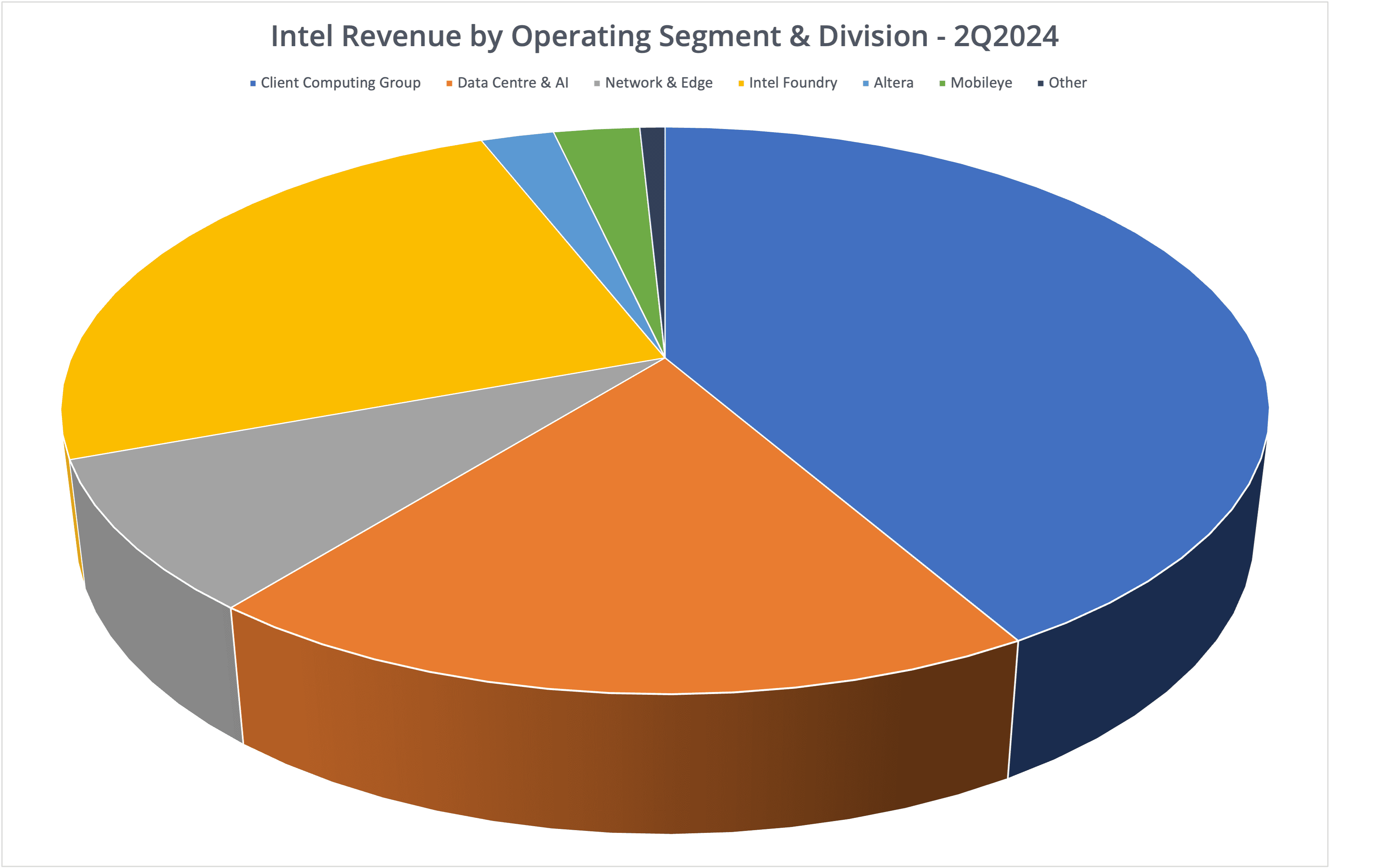

Not all the Intel news was negative. The Data Centre & AI business grew 8.8%, while Networking & Edge improved slightly at 4%. However, Client Computing, the most significant contributor to Intel’s revenue, was down 6.8%, and Intel Foundry declined 8.0%. The subsidiary businesses (Altera and Mobileye) also declined by 43.9% and 8.5% respectively.

The Architect’s View®

At first glance, these numbers look pretty bad, but we should be asking whether the business strategy being pursued will lead to better products and services for customers. Intel is confident that 2025 will see a successful transition to 18A process manufacturing, with 14A further down the line. CEO Gelsinger also confirmed the company is on track to sell a cumulative total of 100 million Intel-enabled AI PCs by the end of 2025.

Elsewhere, we can see significant problems that need to be addressed, specifically in the AI Accelerator market. Gaudi 2 & 3 sales are not expected to reach $500 million, which, accompanied by a $300 million write-down of unsold inventory, translates into a dismal result for this section of Intel’s data centre market.

We see the following observations as areas of focus for our coverage of Intel over the next 12 months.

- Can Intel turn the tide on Gaudi by developing better products and improving the adoption, including the software stack?

- Can Xeon 6 compete successfully against AMD EPYC and still be efficient enough to counter the rise of Arm in the public cloud? EPYC is gaining market share (currently 34% and growing).

- Can Intel compete on the desktop and deliver products to better the competition in areas such as the AI PC? So far, this market seems to be a leapfrog between vendors, including AMD and Qualcomm.

- Can Intel successfully transition to 18A node manufacturing and sell this to external customers? This achievement seems critical to the success of the Foundry business.

The financial results from Q3 and upcoming Q4 are focused on restructuring the business to meet the challenges of the next half-decade. However, Intel still needs products to deliver in the short term, specifically in the x86 market (both enterprise and desktop) and crucially in the AI Accelerator market, which may have already escaped the company’s grasp.

The next few quarters are going to be very interesting to watch as the effects of the rebuilding of Intel take hold.

Related Posts

- Analysis: Intel paranoia gives birth to the x86 Ecosystem Advisory Group

- Analysis: Intel Corporation Announces Q2 FY2024 Financial Results

- Commentary: The rise of Arm on the desktop spells trouble for Intel

- Research Note: Intel Vision 2024 previews Gaudi 3, Xeon 6, and Lunar Lake Processors

Copyright (c) 2007-2024 – Post #c5c5 – Brookend Ltd, first published on https://www.architecting.it/blog, do not reproduce without permission.