Western Digital Corporation has announced financial results for the first quarter of FY2025, ending on 27 September 2024. Revenue was $4.1 billion, up 48.9% year-on-year compared to Q1 FY2024 and 8.8% sequentially (compared to Q4 FY2024). As the planned demerger of the flash business looms, what can we learn about the future growth prospects for both aspects of the current business?

Background

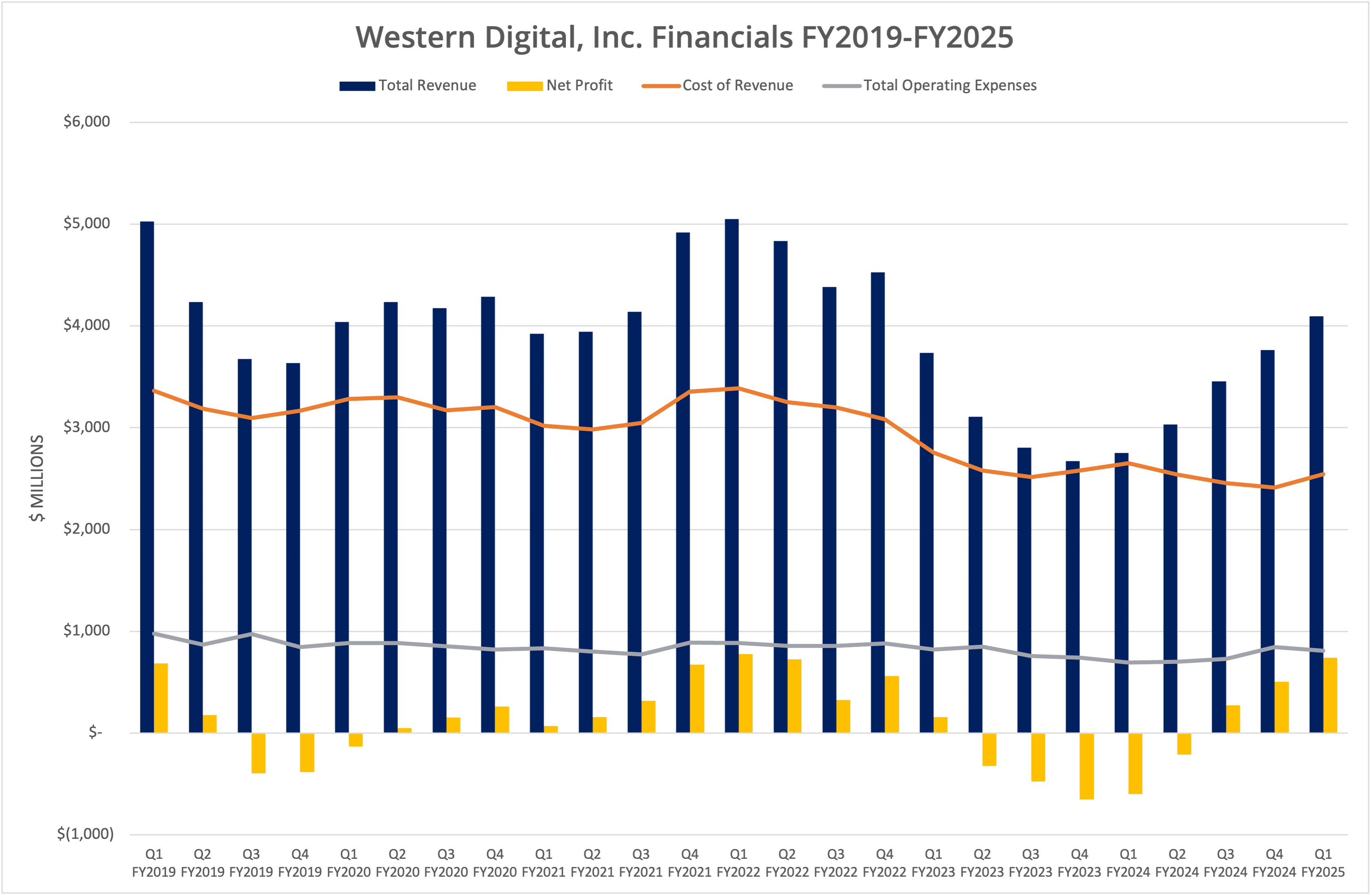

Western Digital has published financial data for the first quarter of FY2025, which ended on 27 September 2024. Revenue rose 48.9% year-on-year compared with the same period of FY2024 and 8.8% sequentially compared to the previous quarter. We present the data in 6 graphs, labelled Figures 1 to 6.

The last four quarters have seen a positive revenue revival for Western Digital, with the last three quarters showing a profit. The issues of NAND oversupply have been banished, with a return to similar gross margins for both the HDD and flash parts of the business (38.1% and 38.9% respectively, 38.5% overall).

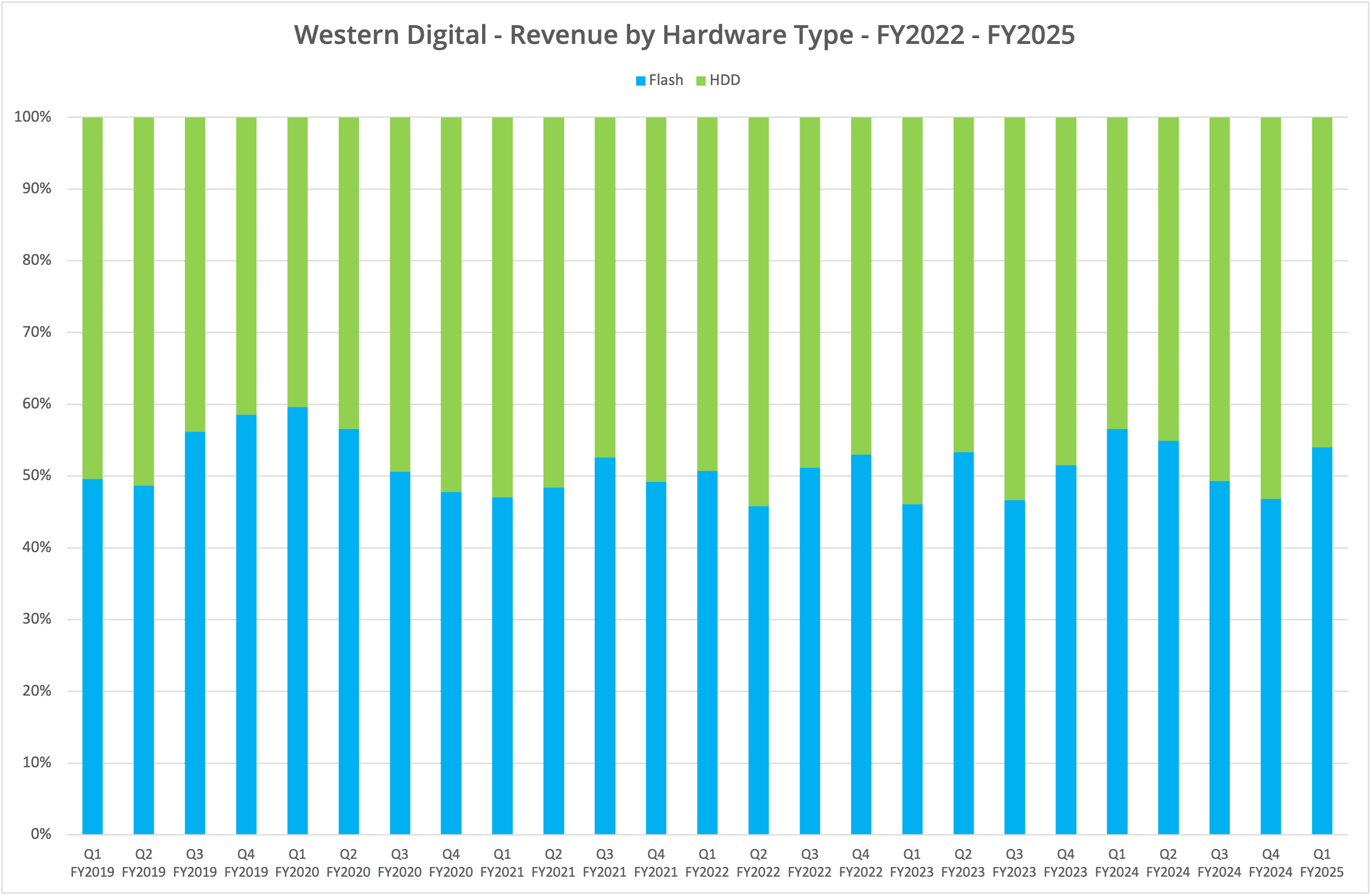

Looking at the data in Figure 4 we can see that the flash and HDD businesses both contribute around 50% to overall revenue, and have done for about the last five years (data prior to that is not available).

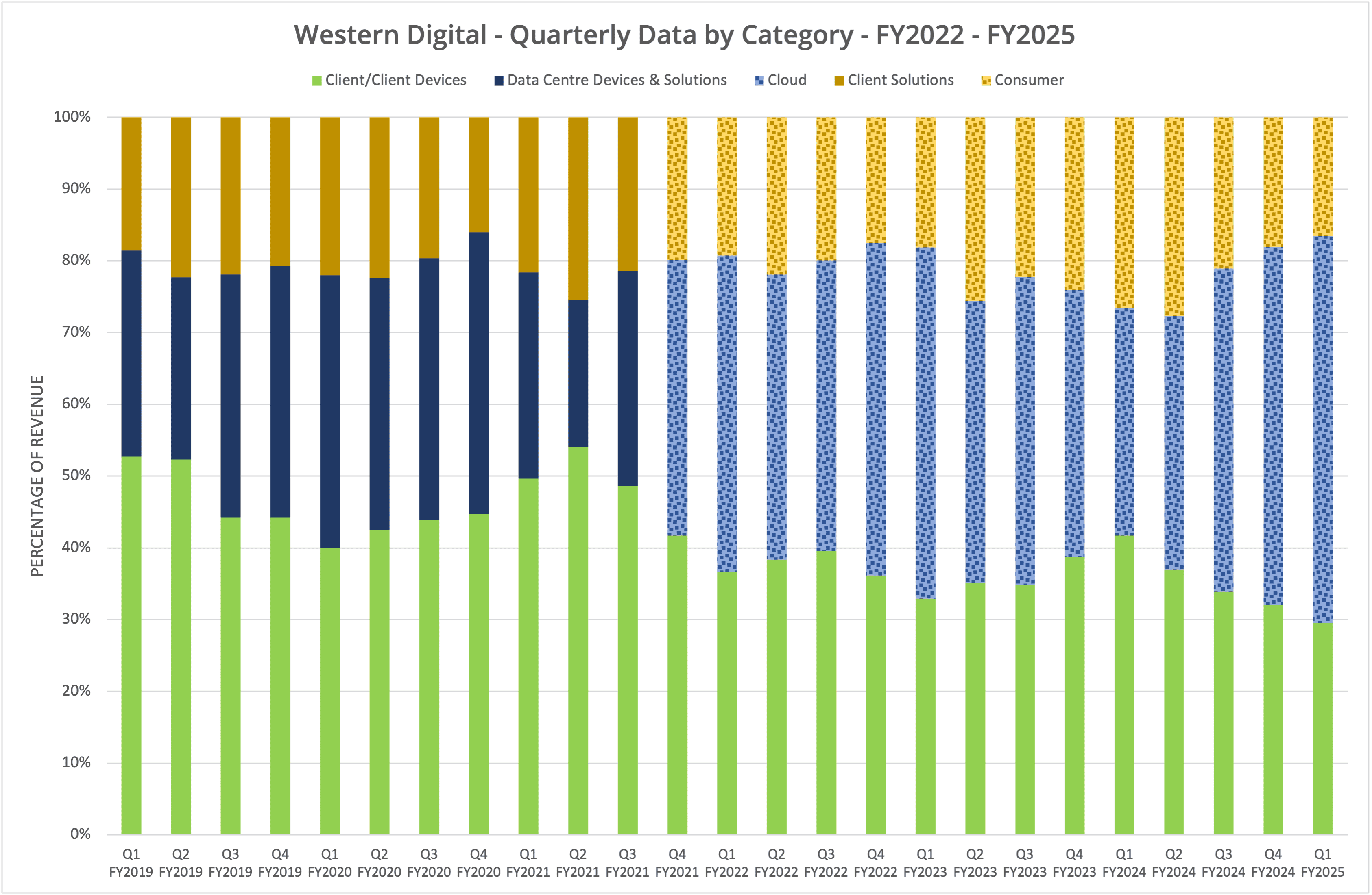

By segment (Figure 3), the data shows significant growth in the Cloud business while, as a percentage of overall revenue, the Consumer and Client business units are shrinking. In absolute terms, the Cloud business grew 153% year-on-year, while Client grew 5% and Consumer declined 7%.

Cloud

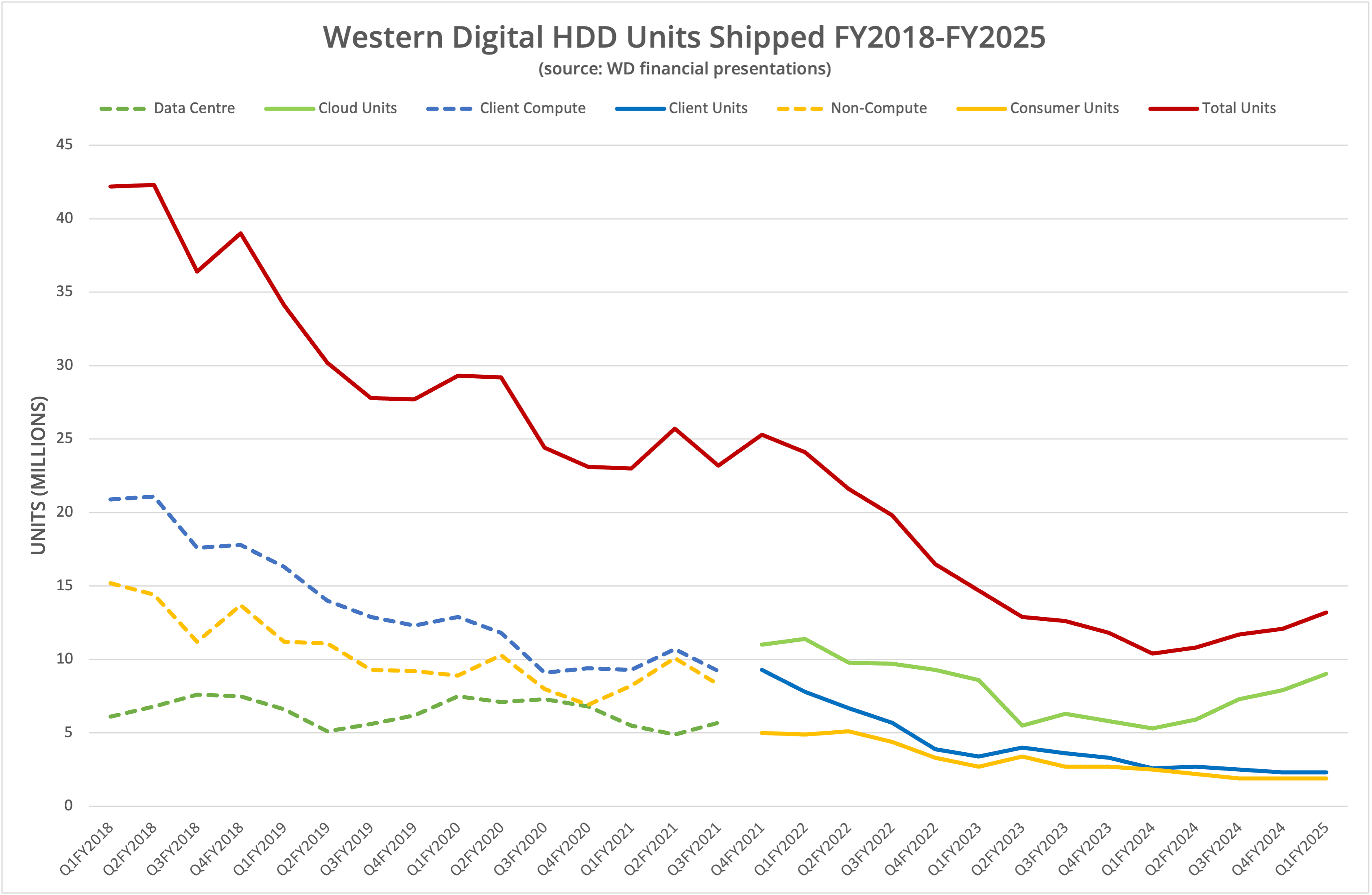

For our research, we follow the Cloud business, to understand the adoption of storage media in both the enterprise and public cloud. Figure 5 attempts to show HDD units shipped since the start of FY2018. Western Digital changed the classification of products mid-FY2021, although we believe that the previous “Data Centre” classification mostly aligns to Cloud, Client Compute aligns to Client Units and Non-Compute aligns with Consumer Units. These categories don’t line up exactly, with some revenue definitely moving between them.

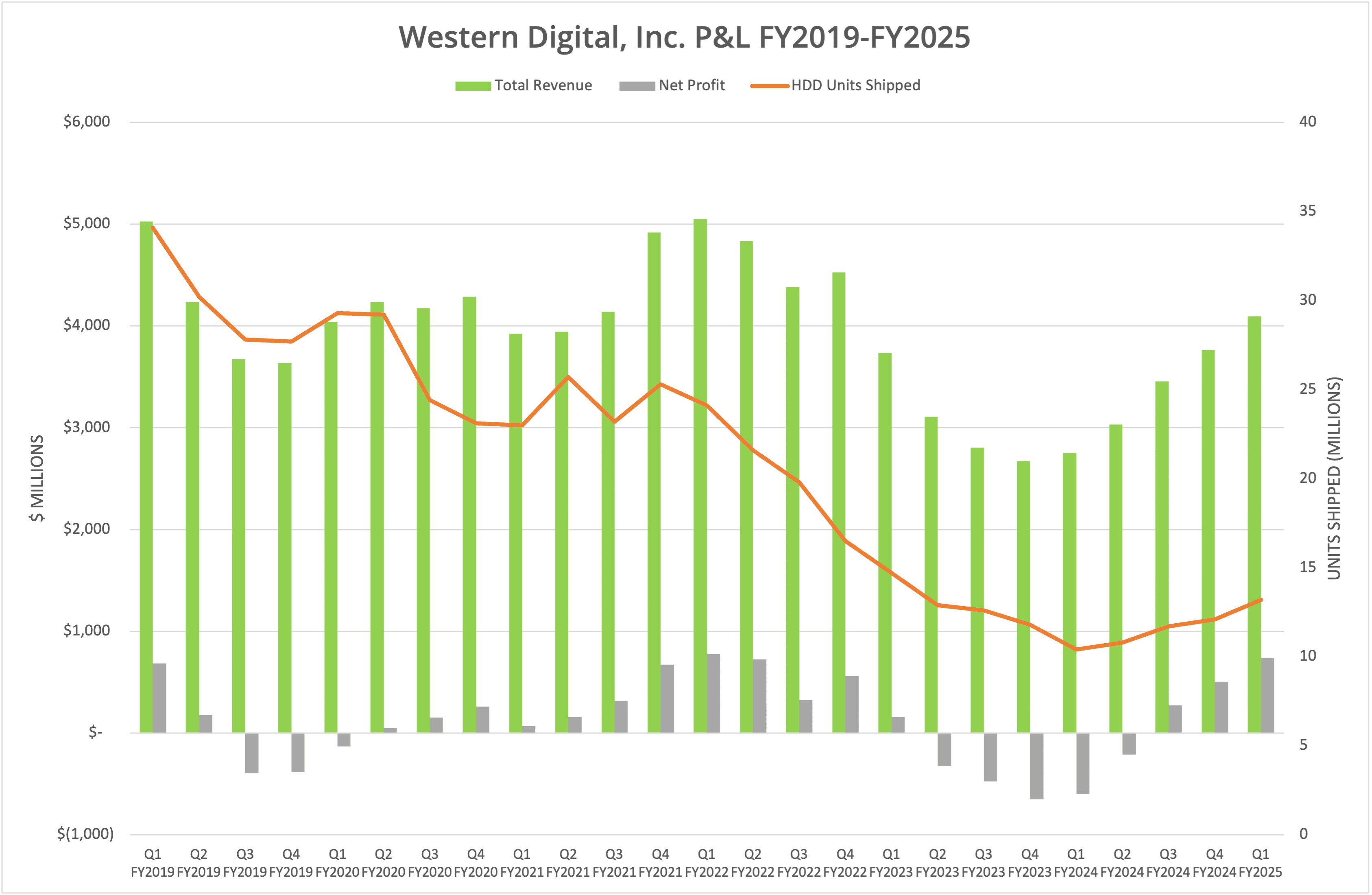

Remarkably, as shown in Figure 2, the revenue achieved by Western Digital tracks approximately to the number of HDD units sold, at least for the last five years of data we have available. This is interesting as 50% of the business revenue comes from flash, which implies that the demand for flash has followed a similar path to that of HDD.

Seagate

In addition to the apparent correlation between HDD unit sales and revenue, both Western Digital and Seagate ship approximately the same volume of HDD units, with similar revenue from each. Seagate operates on gross margins of 33%, while Western Digital achieves slightly higher numbers; around 38%.

Both WD and Seagate are currently (at the time of writing) valued at similar market capitalisation (approximately $23 billion). If Seagate is valued correctly, then this assumes the Western Digital HDD business accounts for the entire company valuation, and therefore, the flash business is valued at close to zero. It is, therefore, obvious why WD is being pushed to demerger both parts of the business, as the resulting companies will clearly be worth more than their currently combined value.

HDD Trends

Western Digital is a commodity business, retailing both hard disk drives and solid-state disks. Revenue tracks HDD unit sales and vice versa. It will be interesting to see how the divided businesses will operate, including whether the flash WD business (which we expect to be called SanDisk) will publish SSD unit sales.

From the data we have, it appears that SSD demand over the last few years has been similar to the demand for HDDs. This implies there is no real renaissance in HDD purchasing, but more likely a refresh of existing technology with larger capacity drives as part of a consolidation exercise in the public cloud.

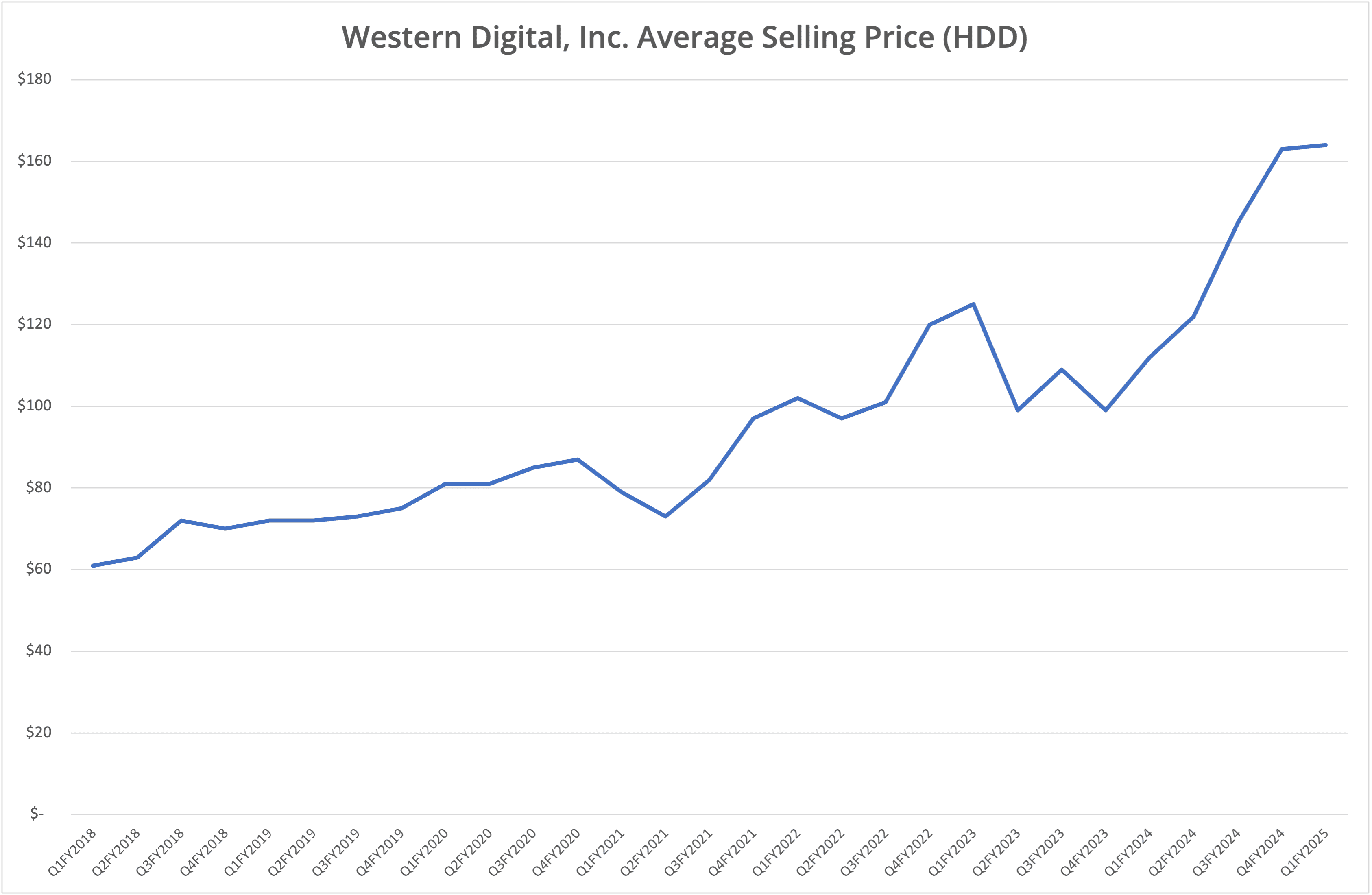

Another aspect of this data is shown in Figure 6, which highlights the average selling price of hard drives over the last six years. As the mix of HDDs has trended towards enterprise/cloud devices, so the average selling price (ASP) has increased, with a dramatic rise in the last four quarters (corresponding to the revenue increase). However, the ASP has increased significantly, resulting in a greater rate of revenue increase over recent quarters compared to the rate of units shipped.

The Architect’s View®

Demand for HDDs has returned, as we’ve seen from the WD and Seagate data this week. In terms of units shipped, the uptick is modest, although higher average selling prices have boosted revenue for both companies. Western Digital remains dependent on units shipped rather than total capacity, which represents a constant challenge as larger-capacity HDDs are developed.

The most interesting development for the company in the next few months will be the impending split into the HDD and flash businesses. Currently, either WD is significantly undervalued, or Seagate is overvalued. How will the WD SSD business perform?

The long-term view for Western Digital mirrors our comments for Seagate. Both companies have seen long-term decline in HDD demand, with a resulting drop in revenue. As these businesses become increasingly dependent on the public cloud, then the long-term future looks uncertain, as we expect public cloud platforms to invest in internal SSD development.

It’s an interesting time for an industry that is buoyed by the current uptick in demand for its products. However, we believe that there is turbulence to come, as the long-term trend towards solid-state media continues.

Related Posts

- Analysis: Western Digital Announces Q4 FY2024 and Full Year Results

- Western Digital Plans to Split Business in Two

- Western Digital Redefines DRAM Caching

- The Fall of STEC and Rise of Western Digital

Copyright (c) 2007-2024 – Post #4433 – Brookend Limited, first published on https://www.architecting.it/blog, do not reproduce without permission.