Dell Technologies has announced Q1 FY2024 financial results and the details don’t look good. ISG revenue was down 18% year-on-year, while CSG was down 23%. Do these figures represent a trend or just a reflection of the post-COVID change in demand for IT hardware?

Background

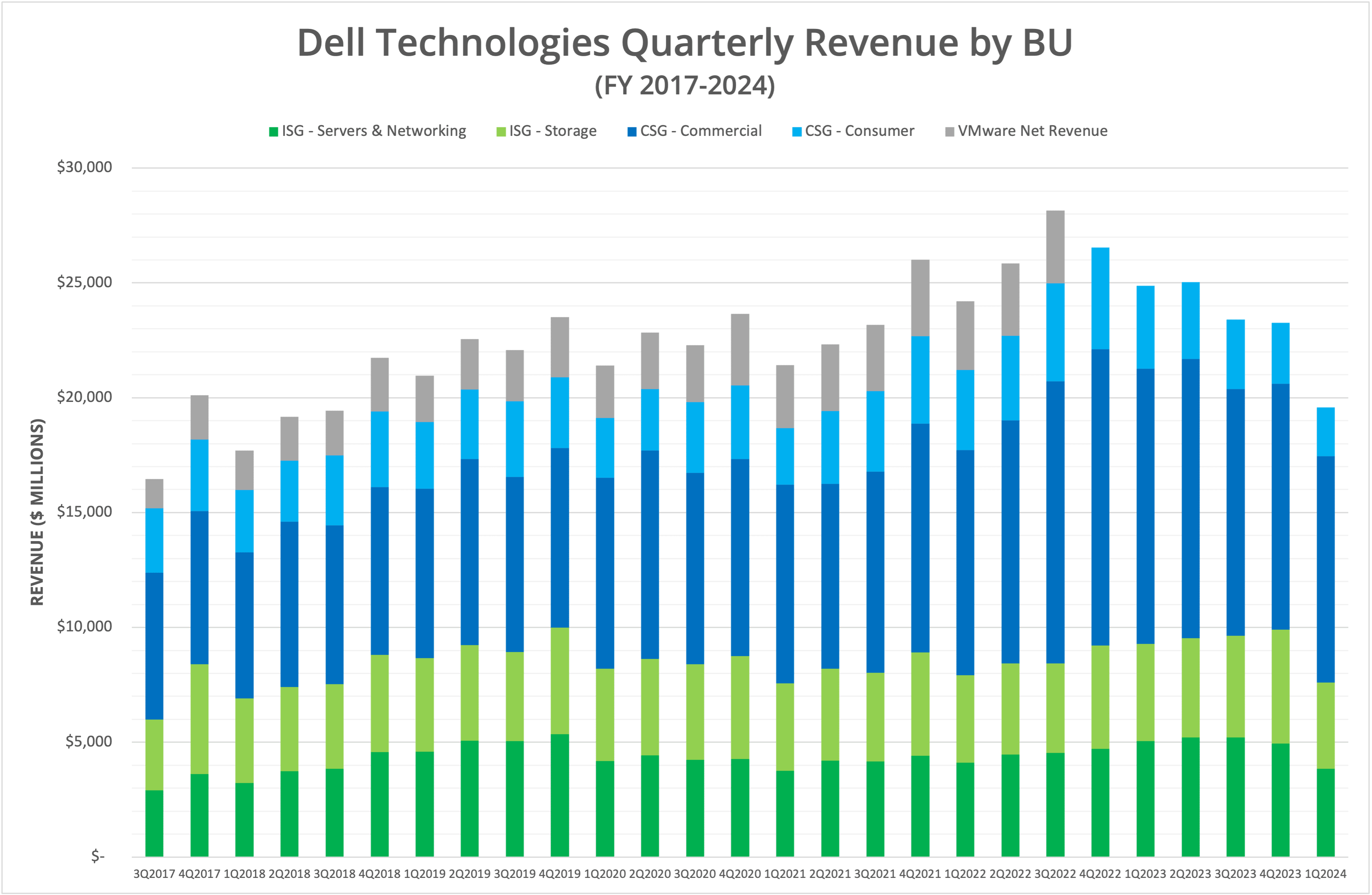

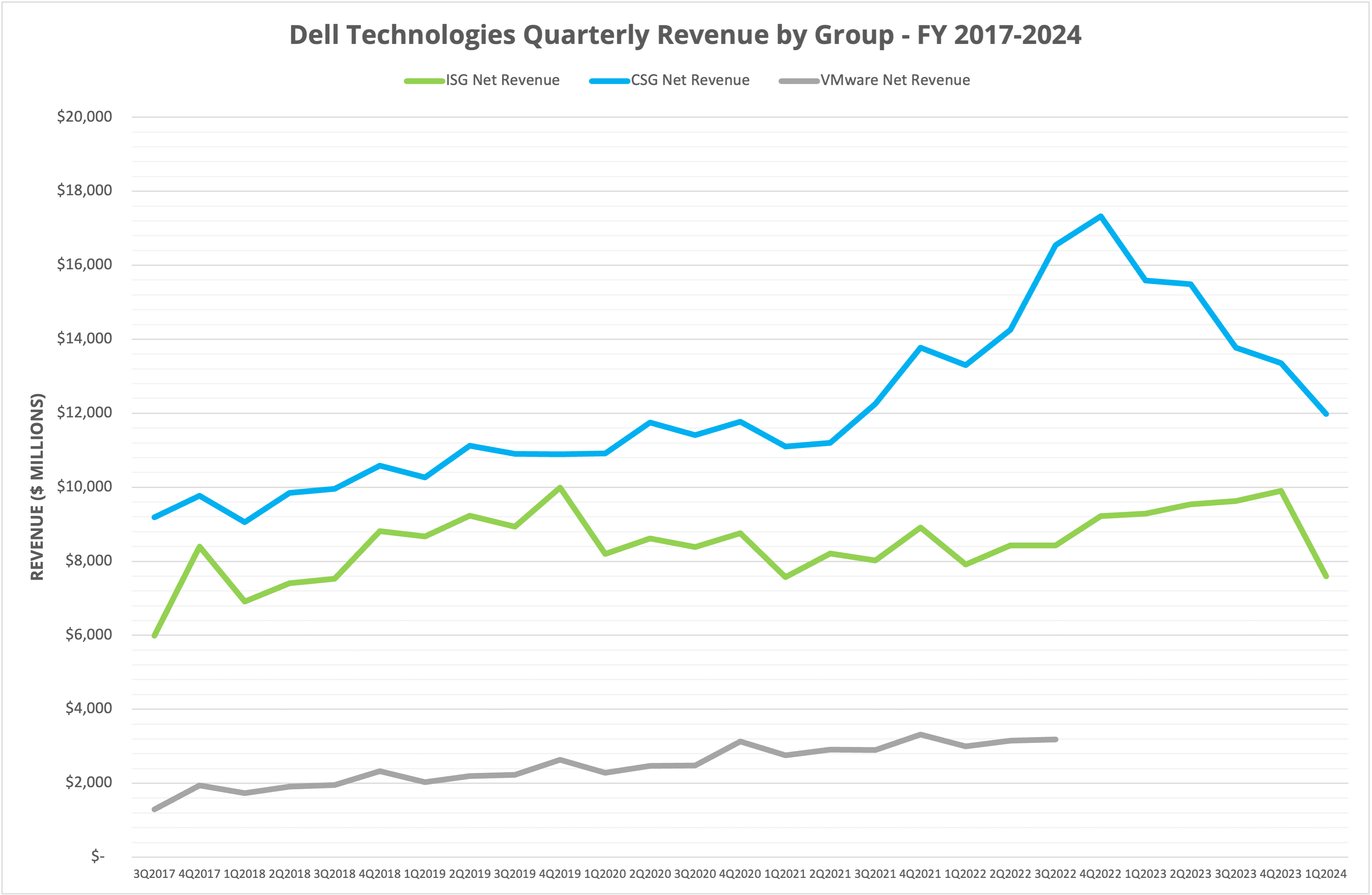

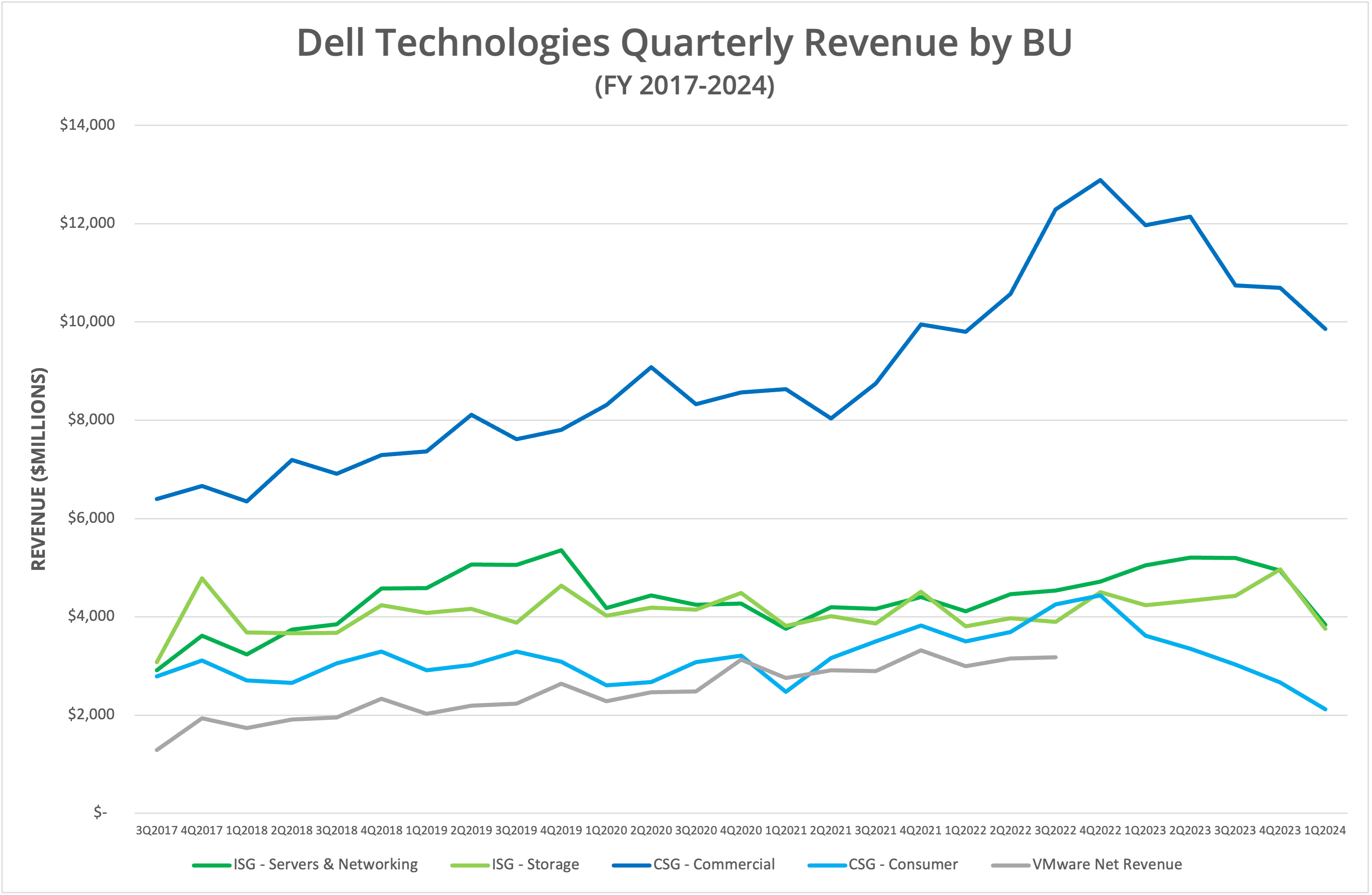

Dell Technologies recorded revenue of $20.9 billion for the first quarter in FY2024 (down 20% year-on-year). This translated into an operating income of just under $1.1 billion. The two main Dell divisions, ISG (Infrastructure Solutions) and CSG (Client Solutions) returned revenue of $7.6 billion (down 18%) and $12 billion (down 23%) respectively. Quarterly revenue by business unit is shown in figure 1, while figure 2 shows the data split across the individual quarters.

We can see from the data that Dell’s revenue has declined consistently since the sell-off of VMware. However, the detail of the decline requires more explanation.

COVID

Back in May 2022, we highlighted how CSG was the driver of Dell’s growth. The COVID pandemic abnormally increased demand for PCs and laptops in the rush to work remotely. Roll forward to the end of FY2023 (as reported here), and we see the initial decline in sales from weaker CSG demand. At the time, ISG demand seemed to be compensating for the drop in CSG revenue.

As we look at Q1 FY2024 data, the decline in CSG revenue has increased, while the growth in ISG revenue been drastically reversed. Servers and networking are down 24%, while storage revenue is down 11%. Traditionally, Q1 is not the strongest quarter for Dell, but putting that aside, these numbers look very poor (divisional data in figures 3 & 4).

Headwinds

What could be causing issues within ISG? One aspect is the delay in Intel releasing the Sapphire Rapids. architecture. Dell only announced products in January 2023, so any positive impact there may not have materialised yet. But generally, as we’ve reported, Dell’s hybrid cloud strategy was lacking a clear focus. New announcements from Dell Technologies World highlighted partnerships with Microsoft, Red Hat and VMware, that are essentially packaging of Dell hardware with vendor software. In these new configurations, Dell includes PowerFlex (the old ScaleIO) as a storage component. The hope is that additional take-up on-premises will align with the release of PowerFlex in AWS, providing a consistent look and feel to storage management across both ecosystems.

Projects

Much of the recent news from Dell has related to future projects, such as Project Fort Zero (zero trust), Project Helix (NVIDIA partnership) and the remaining expectations of Project Alpine. These are all great initiatives, but how much will they generate for the bottom line and how much new Dell IP is involved?

The Architect’s View®

Dell Technologies is, at heart, a hardware company that still has a huge dependency on the end-user device market. The CSG business is cyclical and currently in a greater than normal downswing, mirrored across the rest of the industry.

However, in the servers and storage market, things are rapidly evolving. AI and analytics are creating much of the hype and noise in the industry, while undoubtedly claiming significant amounts of IT spending. This is a growth area. Much of the traditional on-premises workloads can easily be replicated in the public cloud, while AI and HPC-based solutions are transitioning away from a dependence on x86. As a point of reference, the market capitalisation of NVIDIA is now 30x that of Dell and 7.5x that of Intel. In the server architecture market, the future players will not be the old guard.

As for storage, the future growth is unstructured data. In this market, new entrants like VAST Data have built solutions based solely on new technology (persistent memory and cheap QLC media), with business models to match. VAST now has a partnership to sell through HPE as a primary solution offering, with a business model to disaggregate hardware and software. PowerScale, however, is still hardware dependent. Dell also has to compete against Pure Storage and NetApp, both of which have released new products this year (FlashBlade//E and C-Series respectively). Pure Storage has invested heavily in hardware development, while Dell still uses commodity components.

Dell Technologies has a lot of work ahead to stay competitive. We expect CSG will recover eventually (but that could be a 2-3 year cycle). ISG has more difficult challenges ahead, with competition from all sides. The next few quarters could be interesting to see.

Copyright (c) 2007-2023 – Post #f33e – Brookend Ltd, first published on https://www.architecting.it/blog, do not reproduce without permission.

This post is only available to Individual, Vendor or Enterprise subscribers. Restrictions on distribution are based on those licensing terms. Check our Terms of Service for details.