Dell Inc has announced second quarter FY2023 results. Revenue is up, operating income is up, although net income and earnings per share are down (all compared to the previous quarter year-on-year). What can we determine by reading between the lines of the published data?

Back in May 2022 we reviewed financial data from Dell Inc, with respect to the announcements coming out of Dell Technologies World. As we highlighted, two-thirds of Dell revenue comes from the Client division (CSG) and a third from the infrastructure division (ISG). Each division is further subdivided into two business units – CSG has Commercial and Consumer (selling to business and end users respectively), while ISG has Servers & Networking and Storage (all enterprise sales).

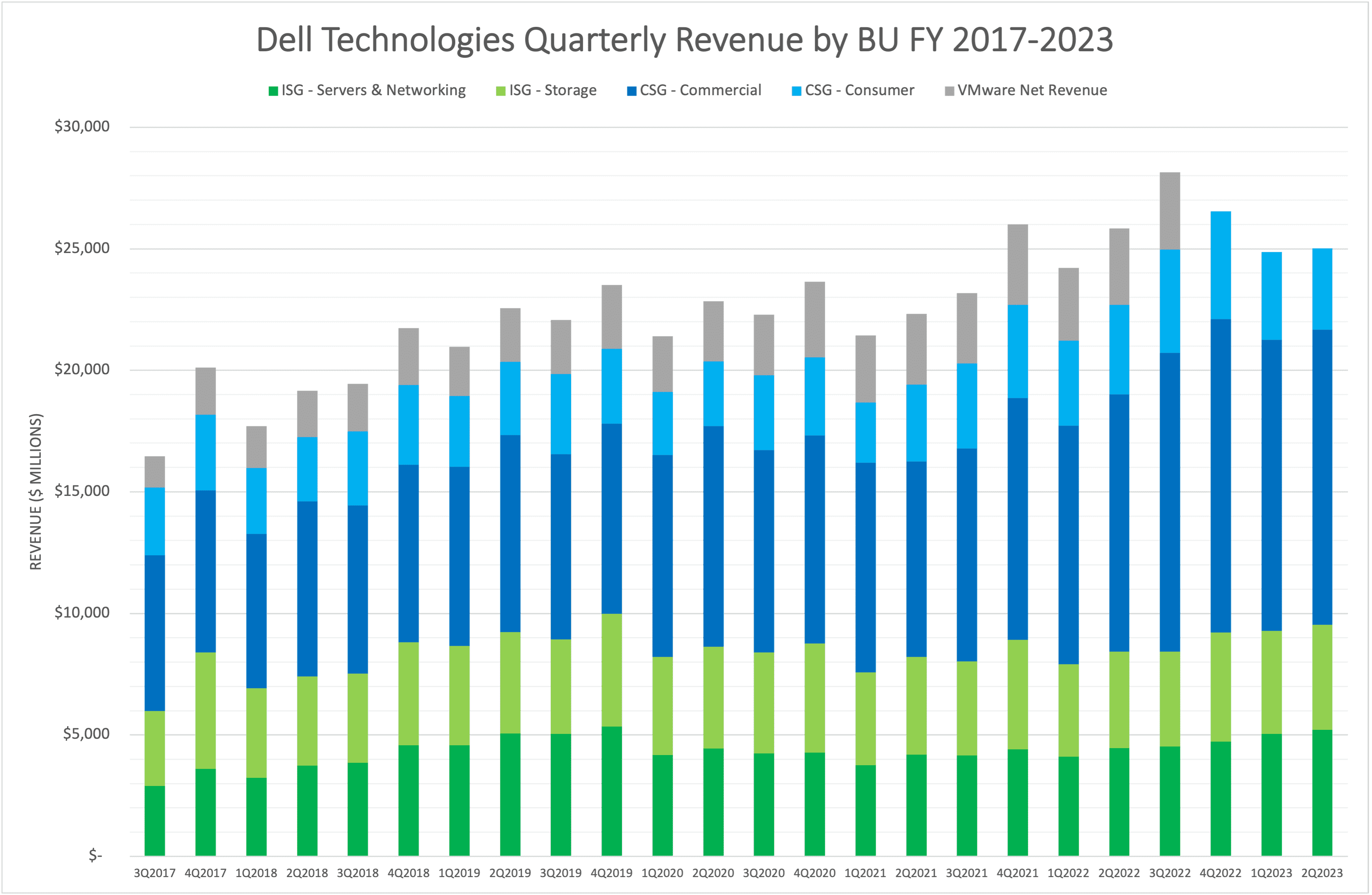

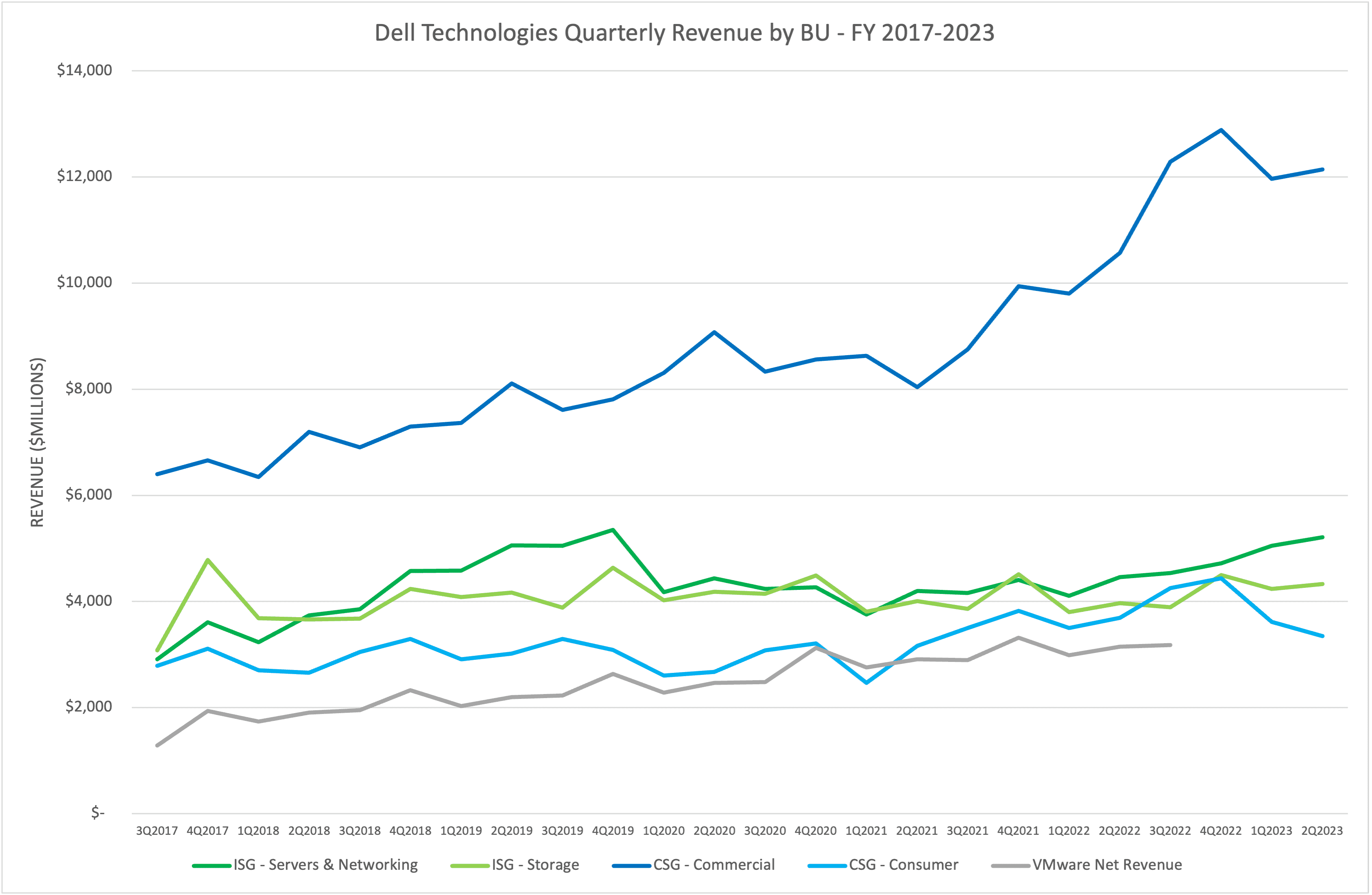

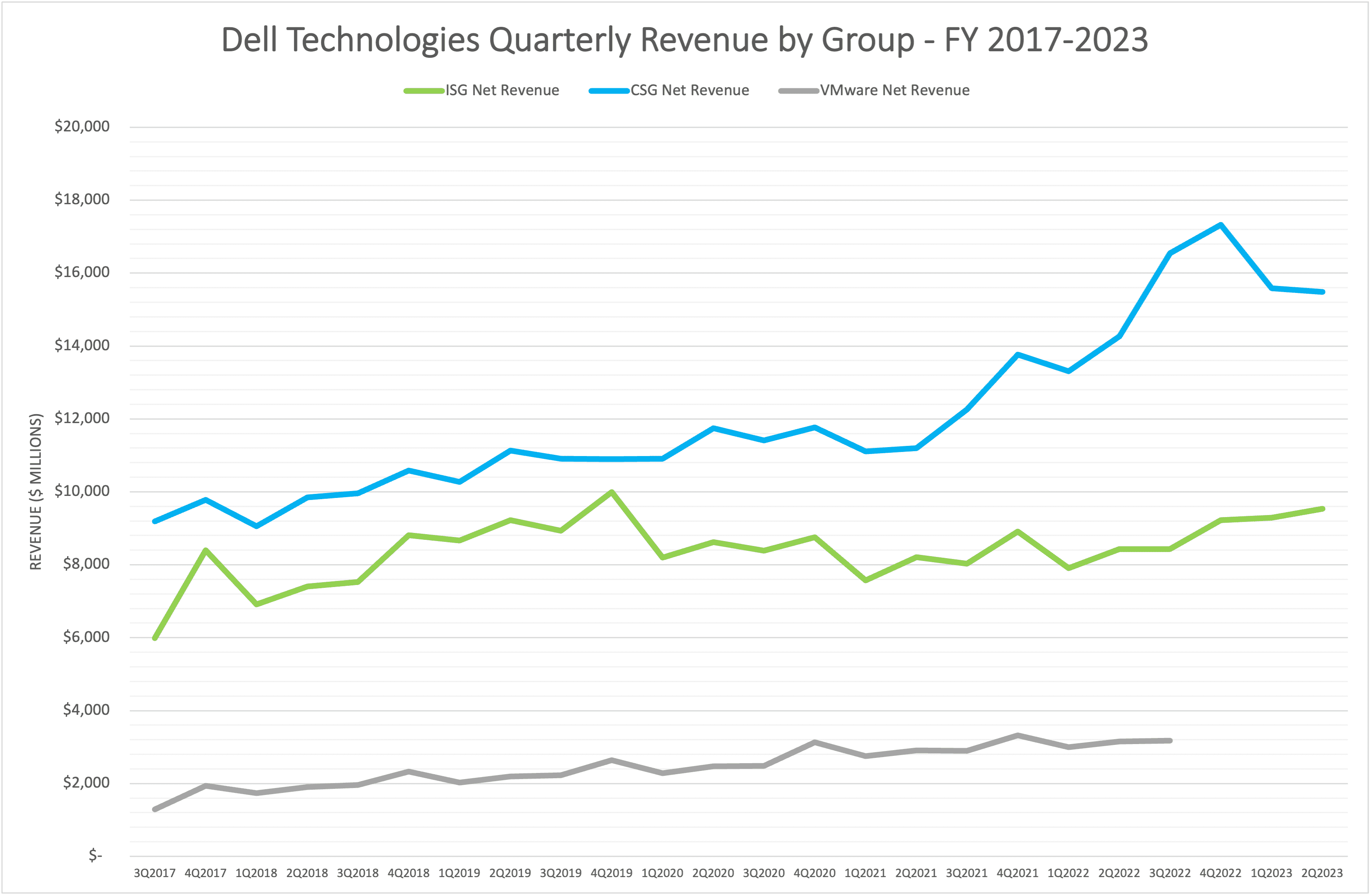

Figures 1, 2 & 3 show quarterly revenue by group and business unit, up to the current quarter’s results. Data for VMware is available up to Q3 FY2022 when the business was spun off (November 2021). The data shows growth in ISG quarter by quarter, but a drop in CSG. However, taken as a quarterly comparison with the equivalent time 12 months previously, then both groups show an increase.

Overall, the revenue increase is 9% from the same quarter a year previously – excluding the revenue for VMware. If the VMware revenue is included, then this reduces to just 1.1%. It’s generally accepted accounting practice to compare like to like, but sometimes the absolute data provide additional colour.

ISG

ISG data was generally positive, with 6% year-on-year growth in Storage and 16% in Servers & Networking. Dell Inc highlights improvements to PowerMax and continued adoption of PowerStore as drivers of growth. Unfortunately we don’t see any data on hybrid or public cloud revenue, which may still be too small to provide meaningful value.

Deltas

One interesting aspect that arises from the restatement of financial data excluding VMware is that we have an opportunity to look at the deltas and determine the “cost” of the VMware business. For example, looking at the differences in Q2 FY2022, selling, marketing and admin expenses drop from $5.1 billion to $3.8 billion. Research & development drops from $1.5 billion to $700 million. VMware had a strong gross margin (around 30%), so it’s no surprise that marketing and R&D spending was so high. Of course we could find these figures directly in the VMware filings, but seeing the data in comparison shows how Dell Inc’s traditional business differs from the VMware software model.

Growth

This area is where Dell’s strategy will be something to watch. The combined R&D spend with VMware included was 6%. Restated numbers excluding VMware for Q2 FY2022 are 2.9% and for Q2 FY2023 have dropped to 2.4%. While we can argue that server and networking hardware (in which we include storage) doesn’t demand much R&D as a percentage of sales, the transformation of business to the public cloud does require much greater investment.

As an example, Amazon and Microsoft both spend around 11-13% annually on R&D as a percentage of revenue. Alphabet (Google) has similar investment (15% in 2017). NetApp, which we reported on yesterday, invested 15% in the current reporting period.

The Architect’s View®

As covered in our Dell cloud strategy post, we don’t see significant long-term growth in ISG revenue, especially Storage, where the trend has been flat for several years. CSG did well in the pandemic years, but that gain seems to have stalled. The current quarter’s data just re-emphasises our previous statements. Dell Inc will need to work hard on evolving its cloud strategy, because there’s little or no growth in on-premises infrastructure. This assertion, of course, applies to any business in competition or looking to co-exist with the public cloud hyper-scalers.

Post #795d. Copyright (c) 2007-2022 Brookend Ltd. No reproduction in whole or part without permission. The Architect’s View is a registered trademark of Brookend Ltd.