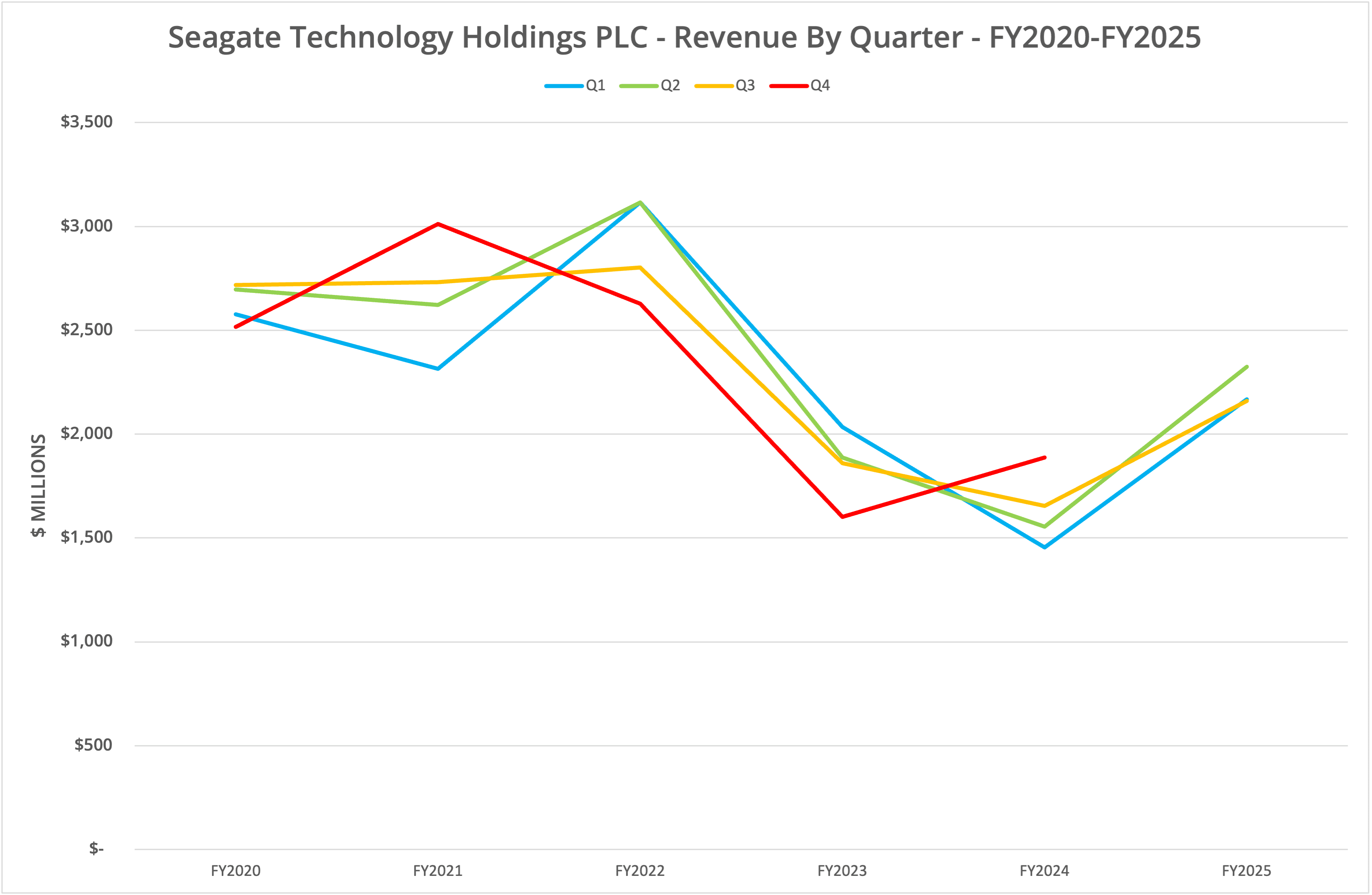

Seagate Technology Holdings PLC has announced financial results for the third quarter of FY2025, ending 28 March 2025. Revenue rose 30.5% year-on-year to $2.16 billion but declined sequentially by 7.1%. Is this a blip in the data or the end of the refresh period for the hyper-scale community?

Background

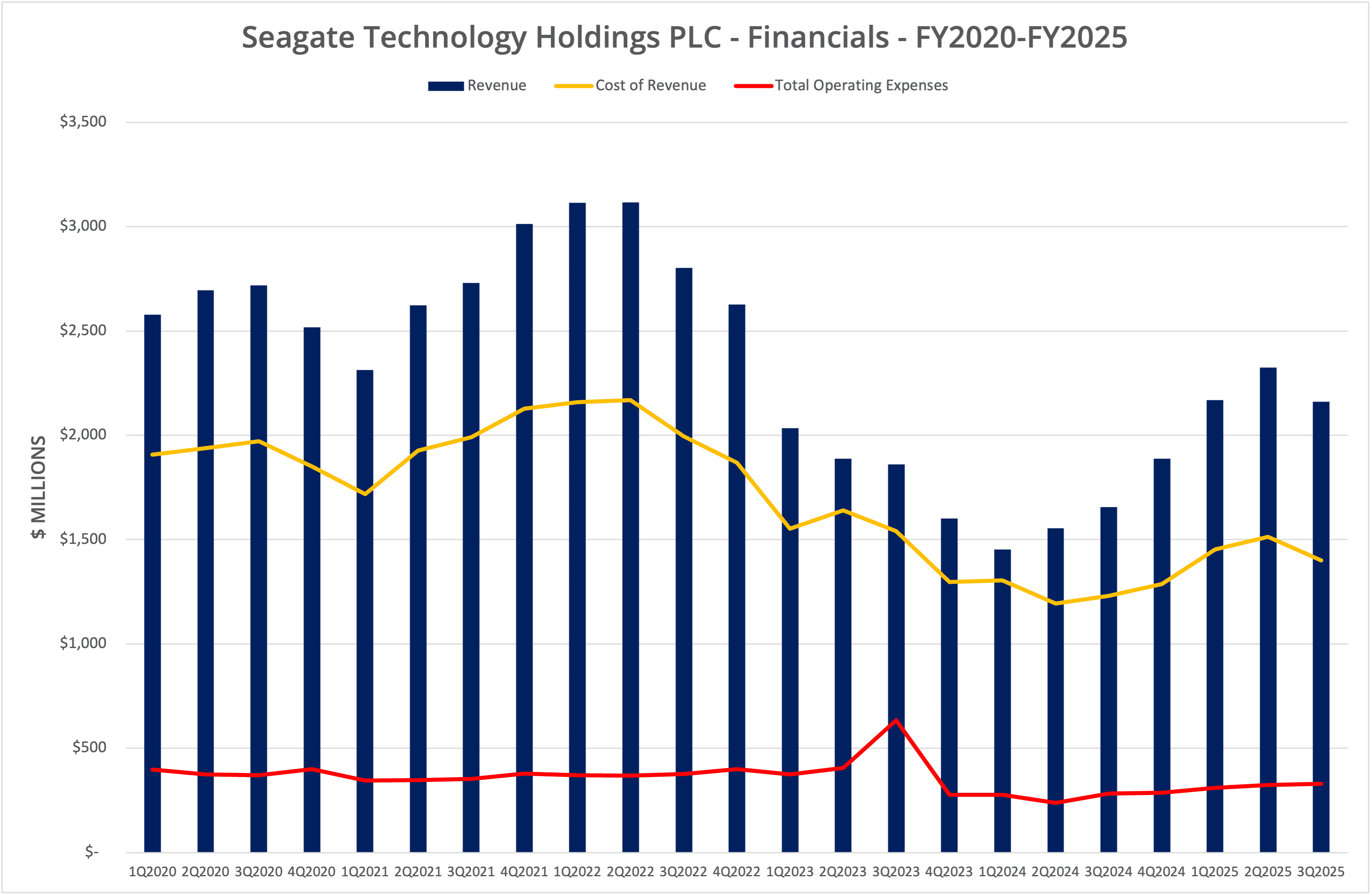

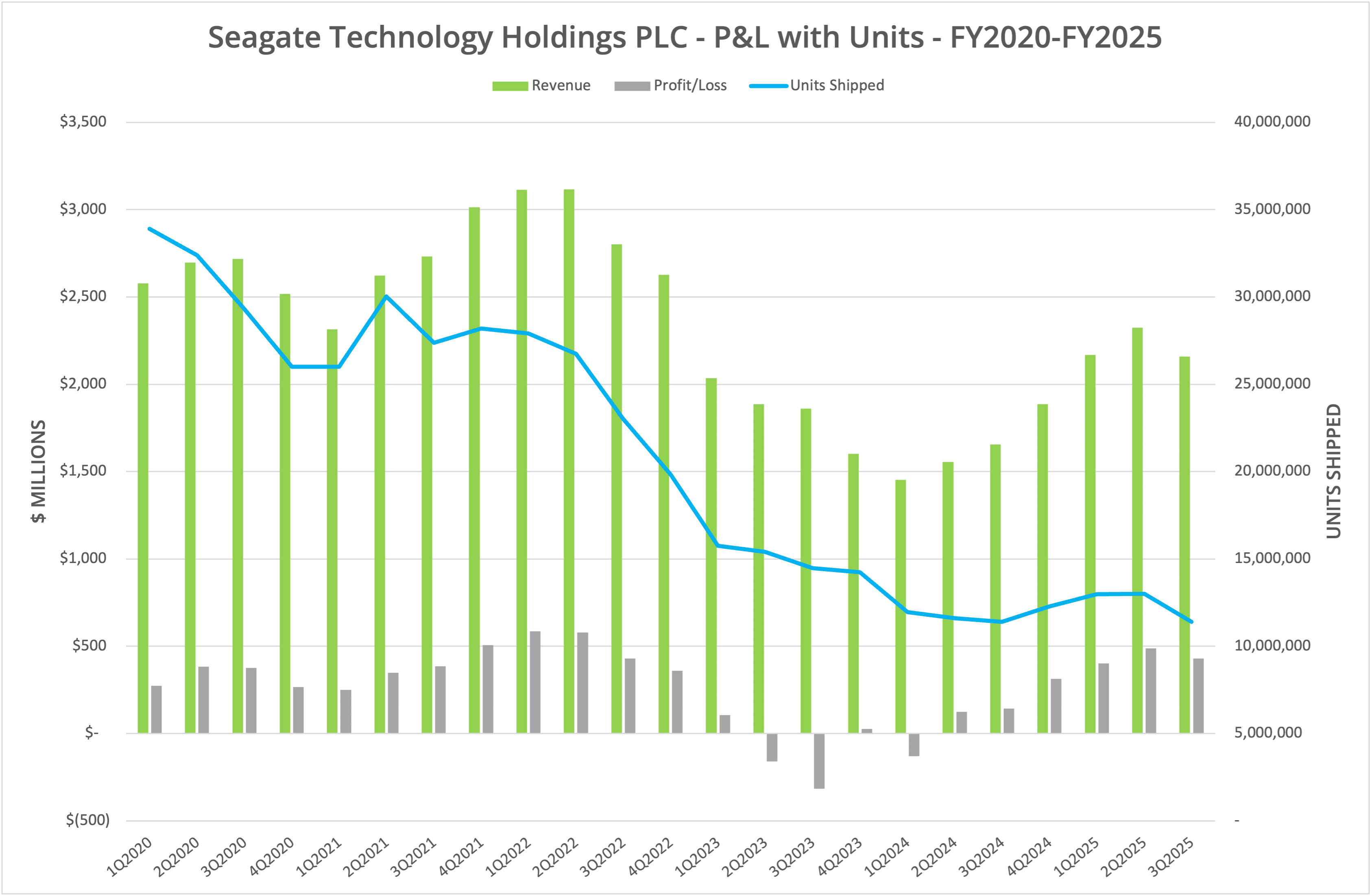

Seagate Technology Holdings PLC declared financial data for Q3 FY2025, ending 28 March 2025 on 29 April 2025. Total revenue rose 30.5% year-on-year to $2.16 billion, although sequentially this represented a decline of 7.1%. Profits tripled compared to Q3 FY2024 to $431 million and were up 11.7% sequentially, driven by a 35% gross margin (26% in Q3 FY2024).

We present the data in five graphs labelled Figures 1 to 5.

Nearline

Approximately 83.4% of Seagate HDD shipments in Q3 FY2025 were nearline drives, defined by the company as 3.5” form factor drives at 7,200 RPM spin speed. These mass capacity drives also represent 87% of Seagate’s revenue for the last three quarters and are now essentially the core of the business. By comparison, in Q3 FY2025, “Systems SSDs and Other” represented just 7.3% of revenue and was flat for the quarter at $157 million.

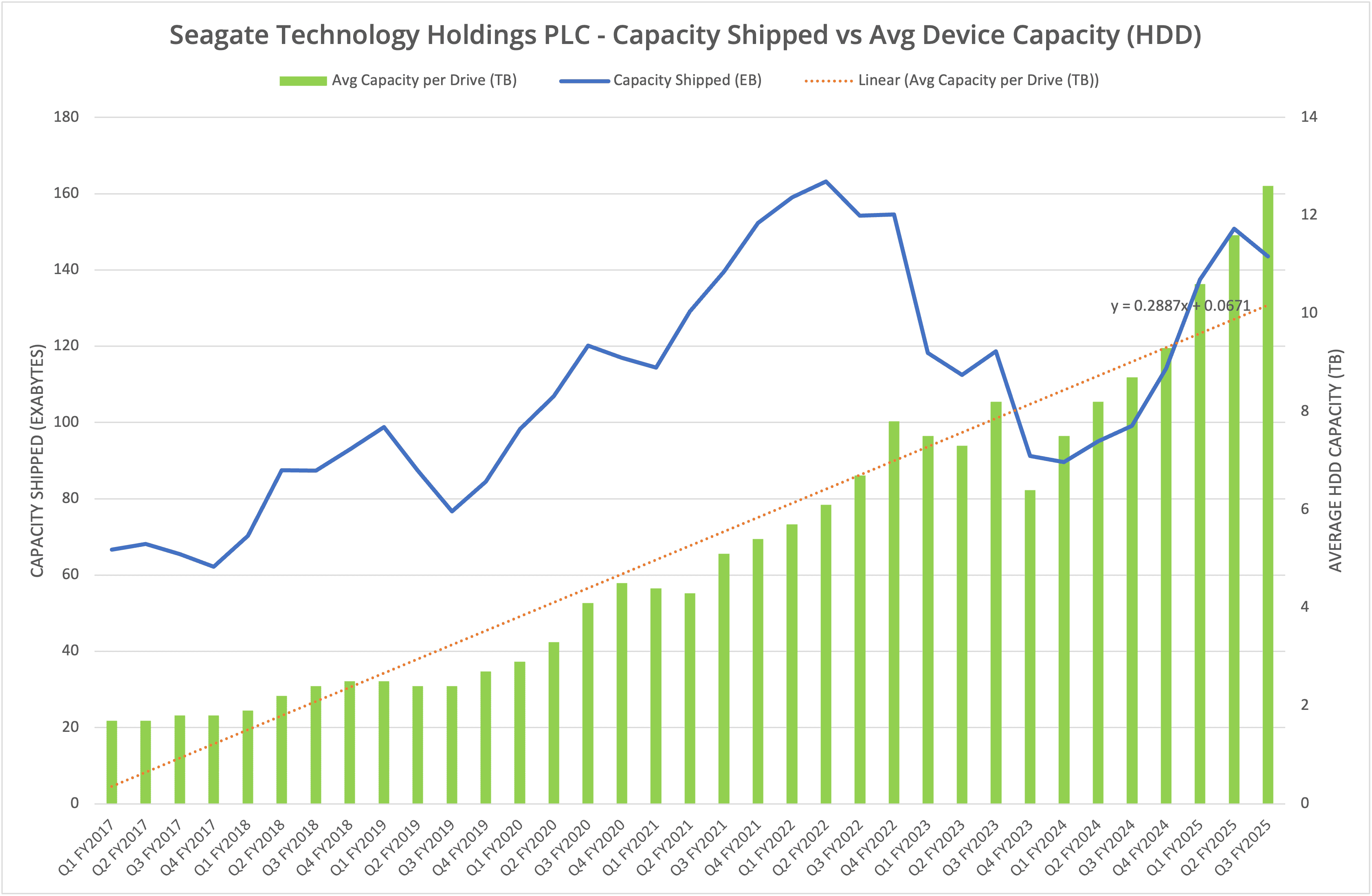

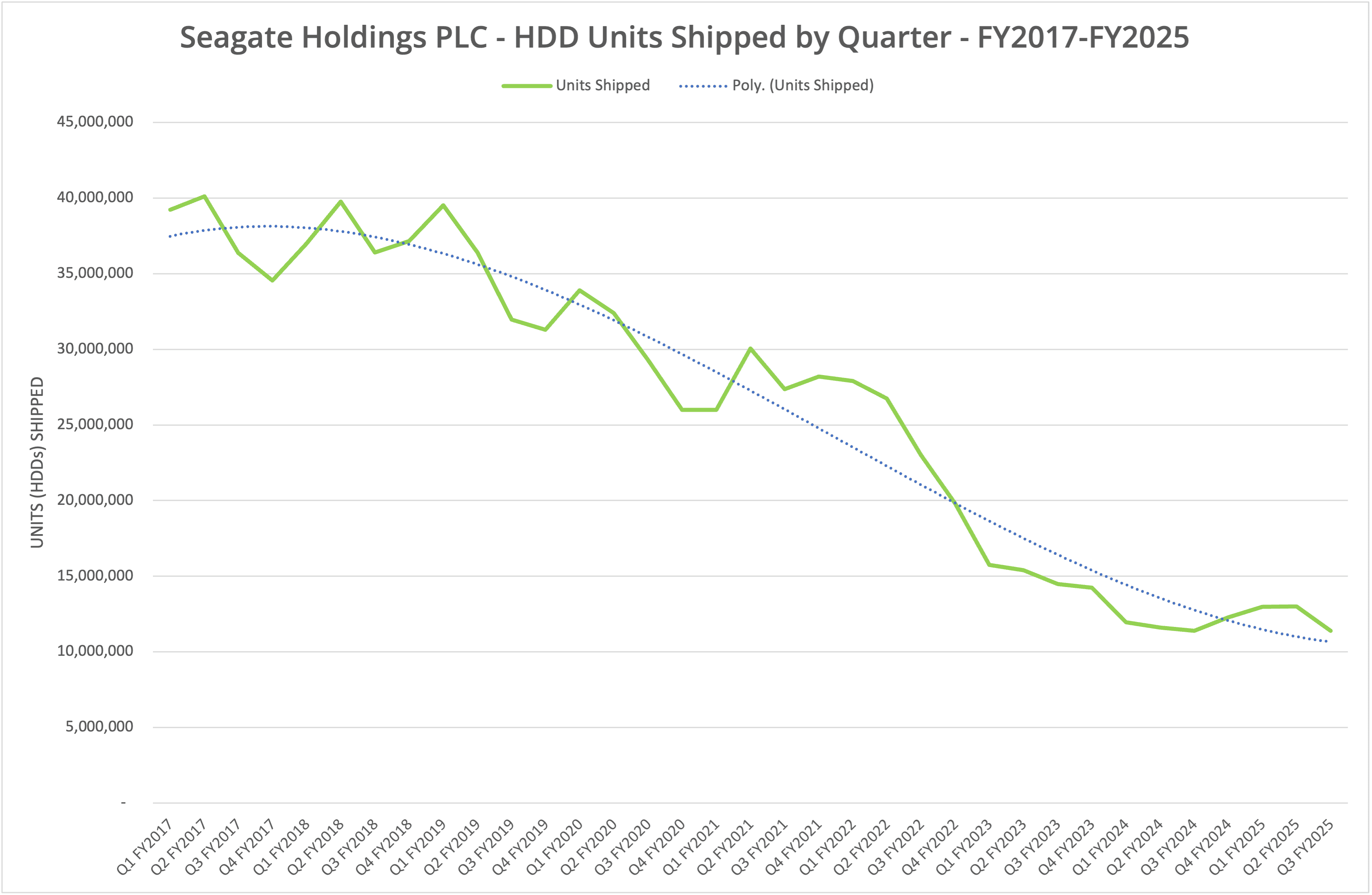

As shown in Figure 4, the average capacity shipped per drive continues to increase (now 12.6TB) as mass capacity drives (and HAMR) continue to be an increasingly larger percentage of drives shipped to customers. However, as we have highlighted in the past, the unit cost of drives is relatively constant, so the decline in absolute units shipped (Figure 5) is reflected in the decline in revenue for the current period.

Hyperscale Demand

Seagate’s business has become one that is driven almost exclusively by the demand of nearline drives by hyperscale customers. Although one swallow doesn’t make a summer, the published revenue and shipping numbers imply that we may have seen the peak of demand in Q2 FY2025. Seagate points to “supply constraints” in recent quarters, which could have an impact on shipping numbers.

However, US tariffs could also impose a challenge for Seagate and similar component vendors, depending on whether the US government decides to follow through with the currently suspended tariff taxes initially imposed in April 2025. Therefore, further headwinds could be ahead.

The Architect’s View®

From a financial position, Seagate has improved gross margin and operationally the business looks strong. However, the dependence on nearline sales is a long-term concern for several reasons.

Firstly, revenue for nearline drives is based on units shipped, with a relatively constant $/unit sales price. We can see that from Figure 2, where sales drop as shipments decline. As HAMR increases the capacity per drive, fewer drives will be sold, as we’ve seen a long-term decline in units shipped (see Figure 5). The implication here is a long-term decline in revenue for Seagate without alternative product sales.

Second, the nearline business accounts for 83% of sales, while HDDs represents 93%. The SSD and systems business unit isn’t increasing its share of revenue at all. Bear in mind the majority of enterprise customers are shifting data to flash-based systems and consequently the outlook for Seagate’s systems business is poor.

Third, we need to remember that SSDs continue to make inroads into the HDD market. Large-capacity SSDs now represent a 3-4x capacity benefit over the largest capacity HDDs in the market. As a result, the TCO and business case for using SSDs continues to grow for an increasing number of workloads.

The logical result of this trend is a decline in the market share of HDDs compared to SSDs. Any increase in the $/TB cost for HDDs will only further justify a move to SSDs, making it hard (or impossible) for Seagate to raise unit prices significantly (unless SSD prices also increase).

While it makes sense for Seagate to optimise its business financially, the long-term trend still remains one of declining revenue, cyclically based on demand from hyper-scale customers. Unfortunately, we have seen those hyper-scale clients starting to discuss the use of QLC SSDs to further replace existing workloads using HDDs and expect this trend to continue.

While the HDD won’t die off tomorrow, next week or even in the next five years, the trend is clear. As revenue and sales decline, will there be sufficient funding to develop the next series of innovations after HAMR?

Our view on the future of Seagate, Western Digital and Toshiba’s business is one of consolidation. Three will become two, with a relatively even split of revenue for the remaining two players. After that, the future of the market depends on whether business regulators across the world judge a single supplier as an unacceptable monopoly.

Does Seagate want to reinvent itself and eventually leave the HDD market behind, or is the company forever linked to selling hard disks? At this point in time, we see no attempt to transition into a different business, and it may be too late to achieve a pivot in the future.

Copyright (c) 2007-2025 – Post #2ab6 – Brookend Ltd, first published on https://www.architecting.it/blog, do not reproduce without permission.