HPE has announced Q3 FY2023 financial results with revenue up 1% year-on-year and annualised run rate (ARR) up 48% to $1.3 billion. Is the transition to operational expenditure with GreenLake working, or is the company simply in a holding pattern?

Background

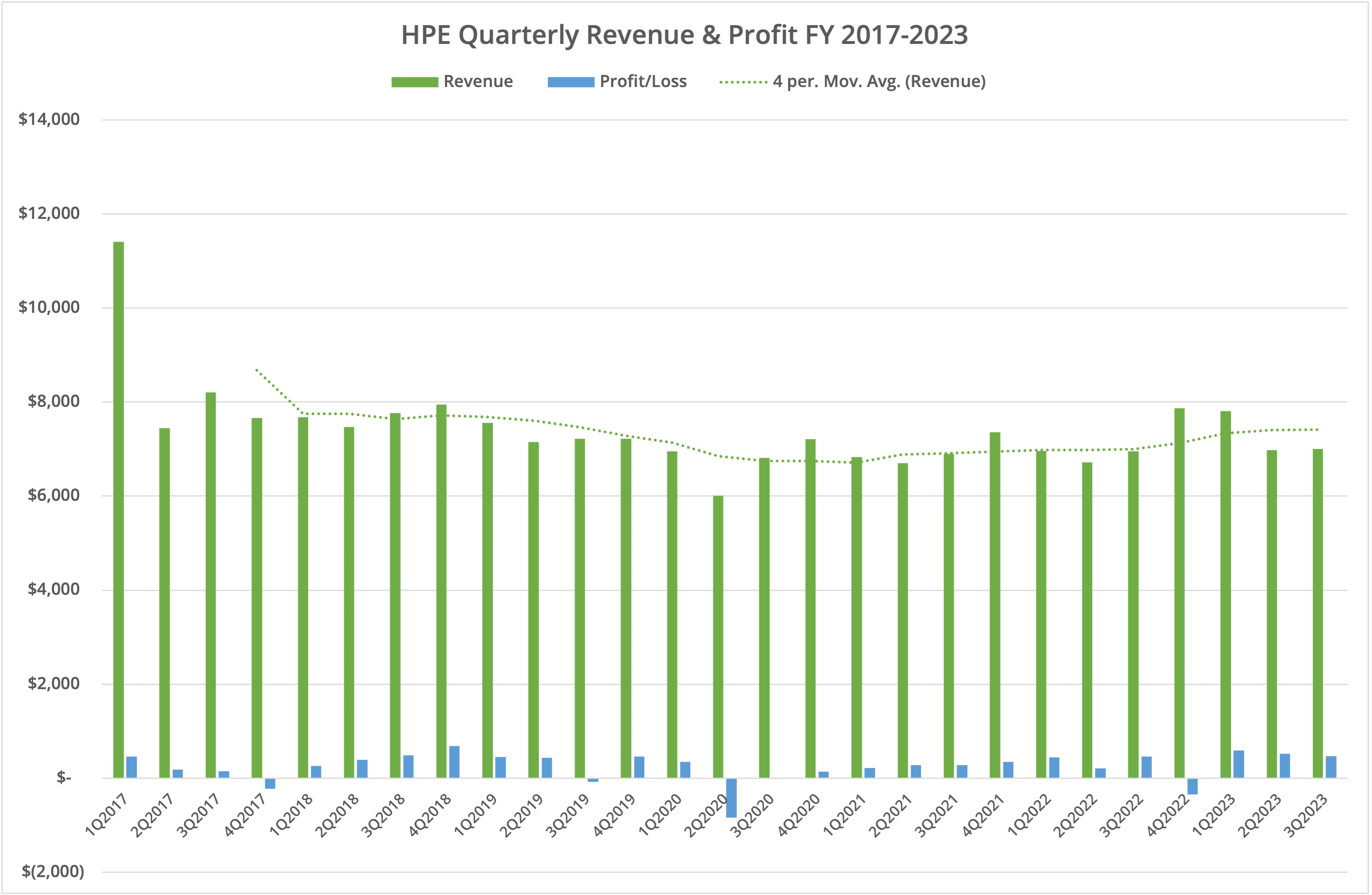

HPE reported revenue of $7 billion for Q3 FY2023, which represents a 1% growth compared to the same period last year. Gross and net profit were similar to the previous period in the previous year at 5% and 1% respectively. Although HPE reports that year-on-year gross margin has improved, the sequential data is down.

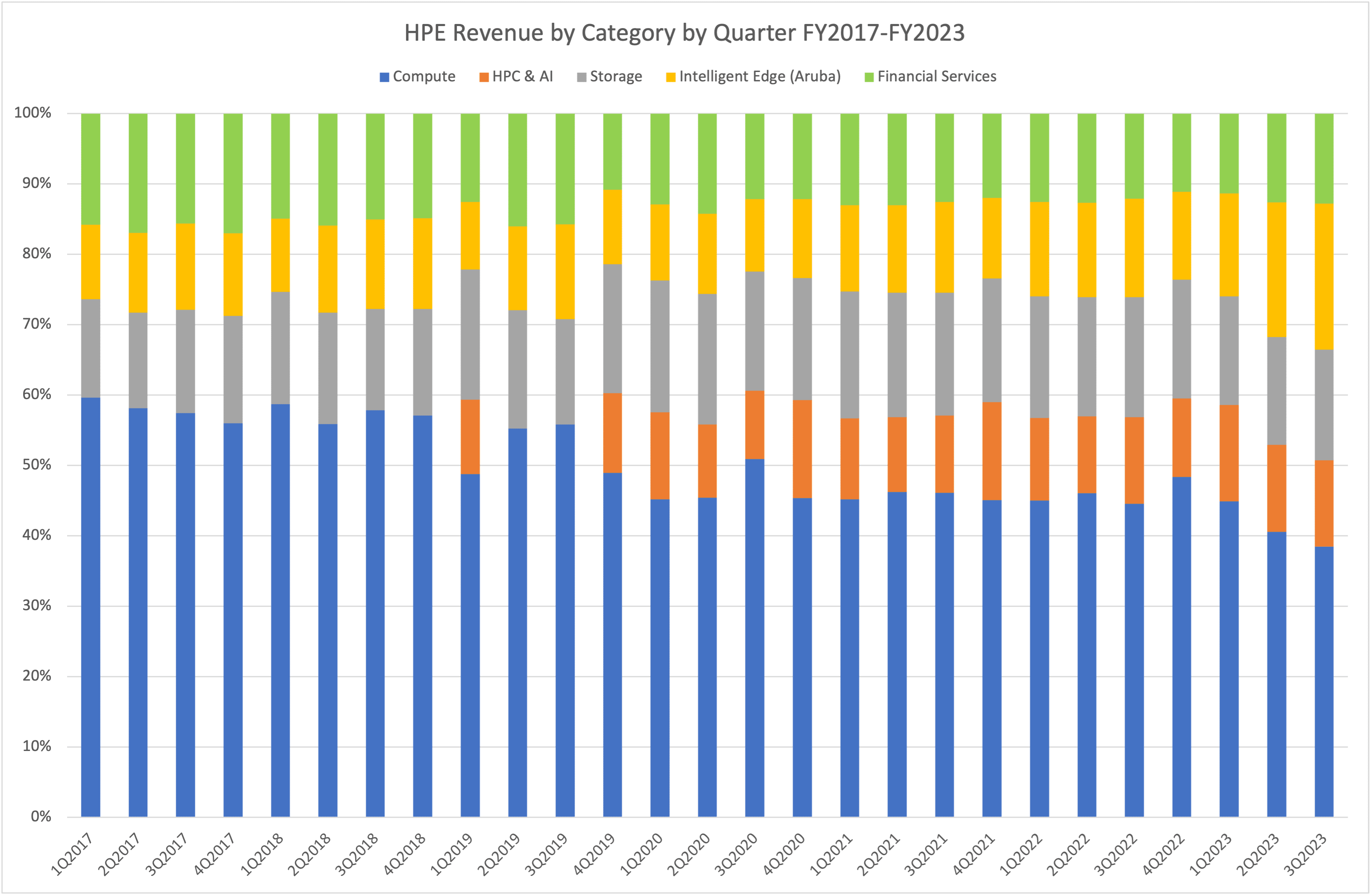

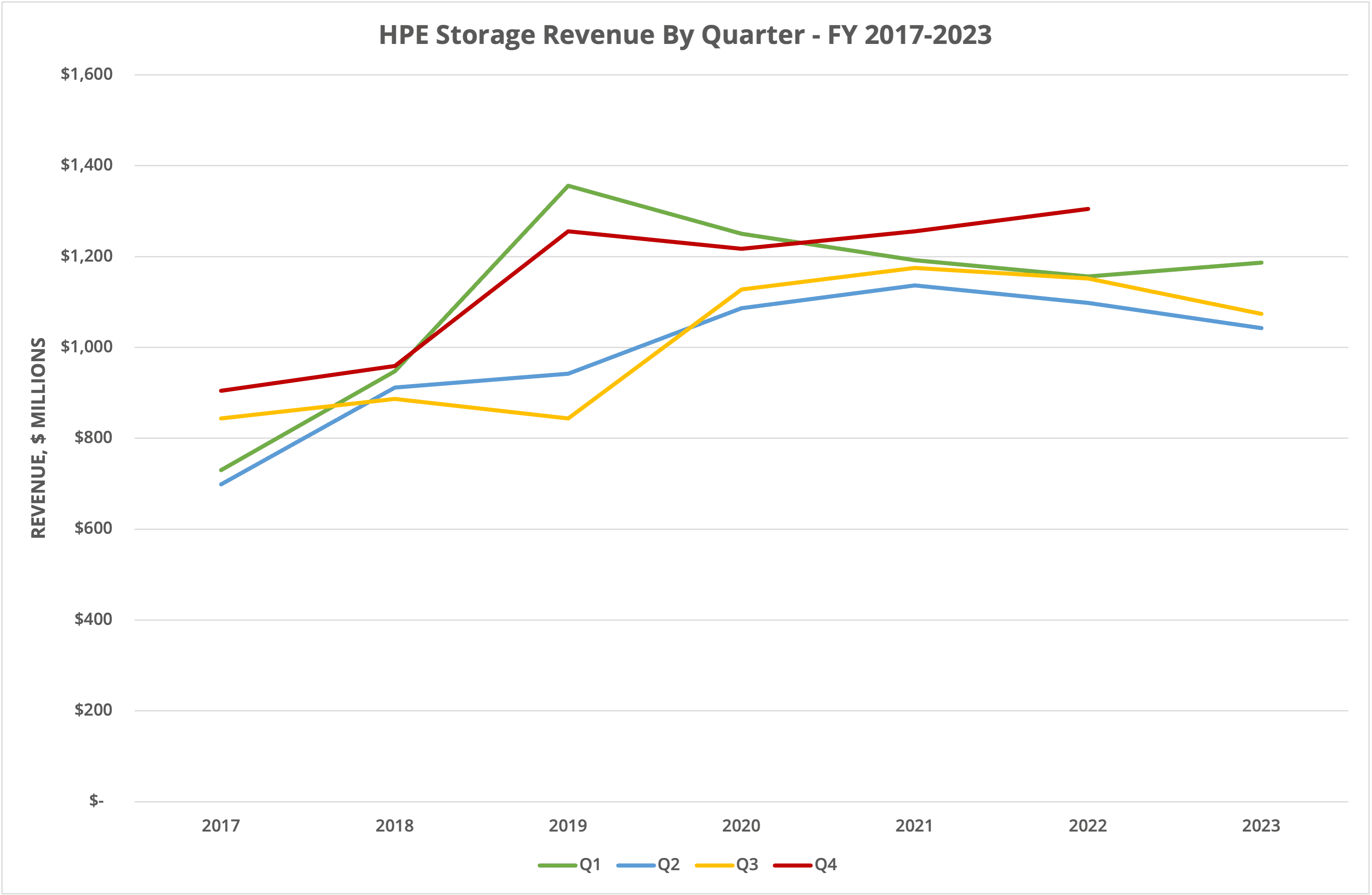

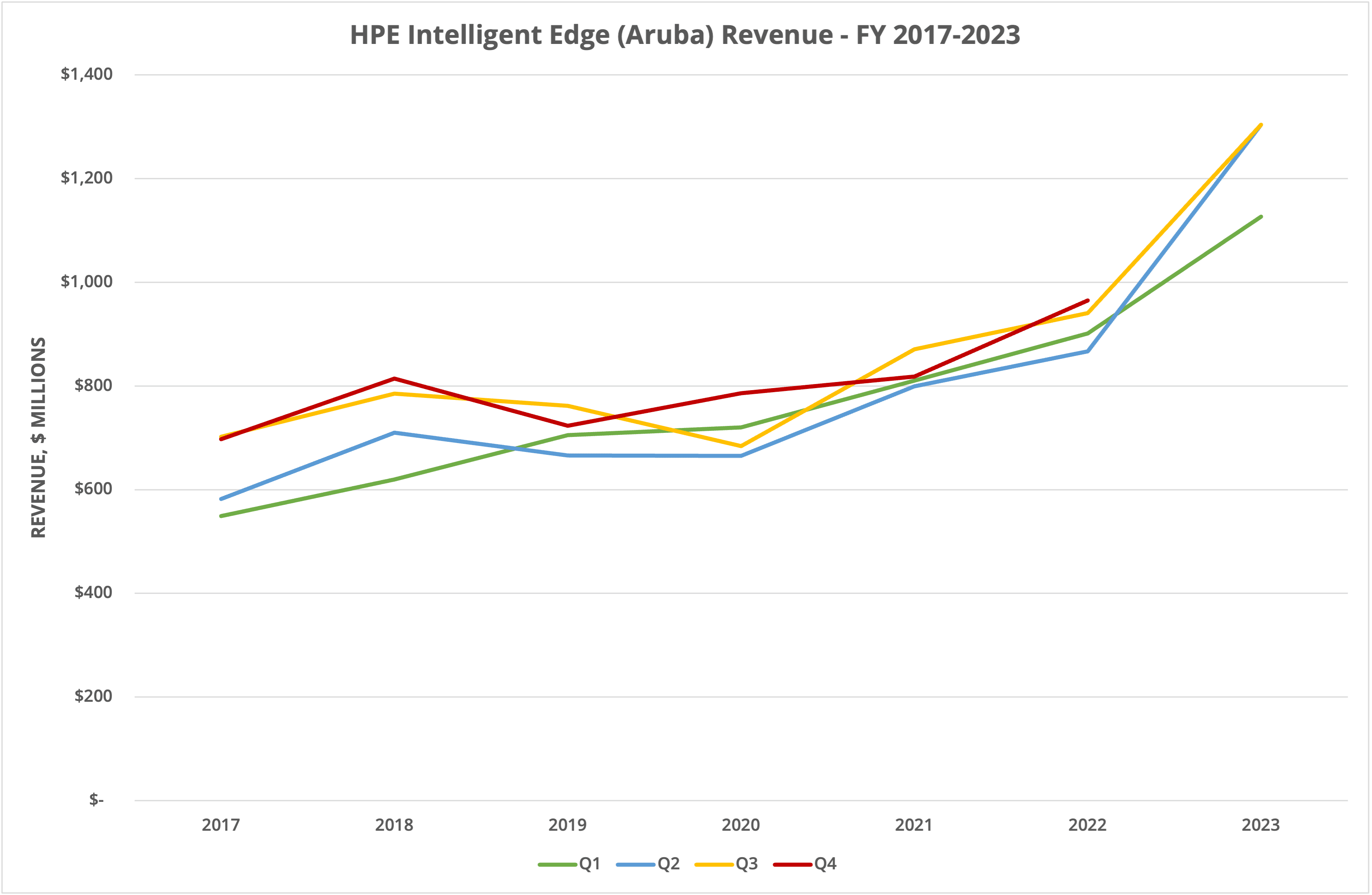

If we examine individual lines of business, Intelligent Edge increased its operating profit margin from 16.5% in Q3 FY2022 to 29.7% in the current period. However, the operating profit margin for Compute, Storage, and HPC/AI were all down. Once again, it seems that Intelligent Edge kept the business afloat, with a 50% increase in revenue compared to Q3 FY2022, while Compute and Storage were down 13% & 5% and HPC/AI was up only 1%.

Changing Model

It’s easy to assume that the recent downturn is affecting HPE’s revenue, but the longer-term data shows otherwise. Figure 2 shows revenue data for the last six years in a percentage-stacked format. At the start of 2017, Compute contributed around 60% of revenue. Today, that figure is approximately 40%. Storage has been constant at about 15%, with Financial Services contributing about the same. Intelligent Edge and HPC/AI make up the remainder, with the former now 21% of revenue and the latter 12% from a starting point of zero.

Of course, it could be argued that the restructuring of business units moved some sales from Compute to HPC/AI, but even taking that into account, the revenue for those lines of business combined would still be static. When we get the data for Q4, we will revisit this stacked graph with the annual data.

ARR and GreenLake

It’s too early to say if the announcements from earlier this year and at Discover 2023 (covered in the last quarter’s blog and also here) are adding to the bottom line. However, it’s now four years since HPE CEO Antonio Neri announced that all HPE solutions would be sold under the GreenLake model. Even assuming Q4 revenue at the top end of guidance, this would mean a full FY2023 figure similar to FY2019 and below FY2018.

Our opinion is that GreenLake has either only stemmed the decline or has been a failure with respect to increasing revenue. Without the growth in Intelligent Edge, this data would look much worse.

The Architect’s View®

HPE is in a holding pattern. Intelligent Edge is doing well, while the remainder of the business is slowly declining. The GreenLake story is a marketing approach attempting to reinvent the company, but it hasn’t worked.

- HPE Announces Q2 FY2023 Results

- HPE announces new GreenLake storage solutions with new hardware

- HPE Announces Q1 FY2023 Results

We can’t see any change in outlook in the foreseeable future. HPE needs to address the need for a hybrid cloud strategy while looking at brands such as Ezmeral and HPE Software that have no clear message or value. Perhaps somewhere within HPE, there is a strategy for modern cloud-native application deployments, Kubernetes, and CI/CD. If they exist, we can’t see them, and if we can’t see them, neither can prospective customers.

Copyright (c) 2007-2023 – Post #83e1 – Brookend Ltd, first published on https://www.architecting.it/blog, do not reproduce without permission.

This post is only available to Individual, Vendor or Enterprise subscribers. Restrictions on distribution are based on those licensing terms. Check our Terms of Service for details.