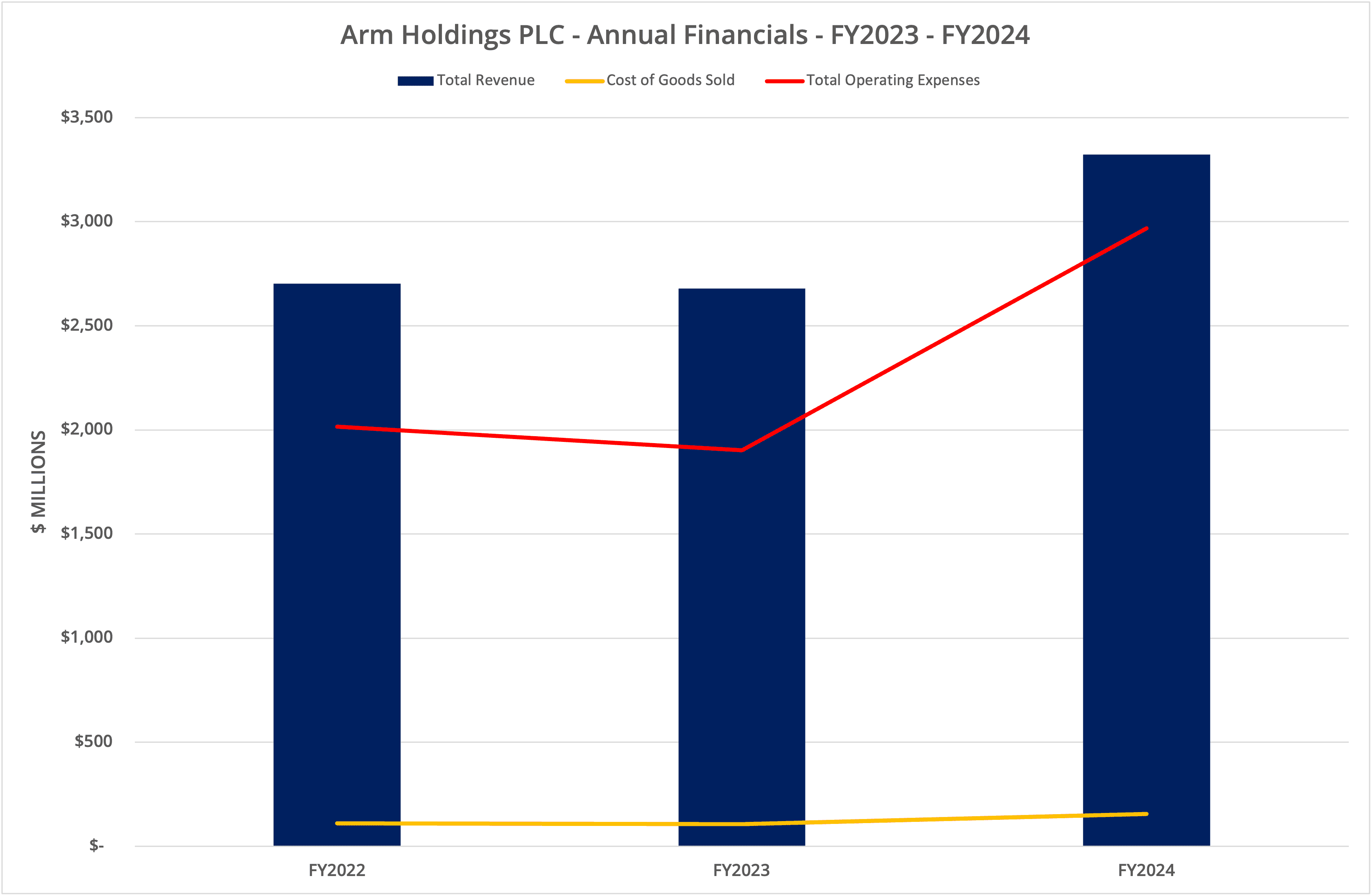

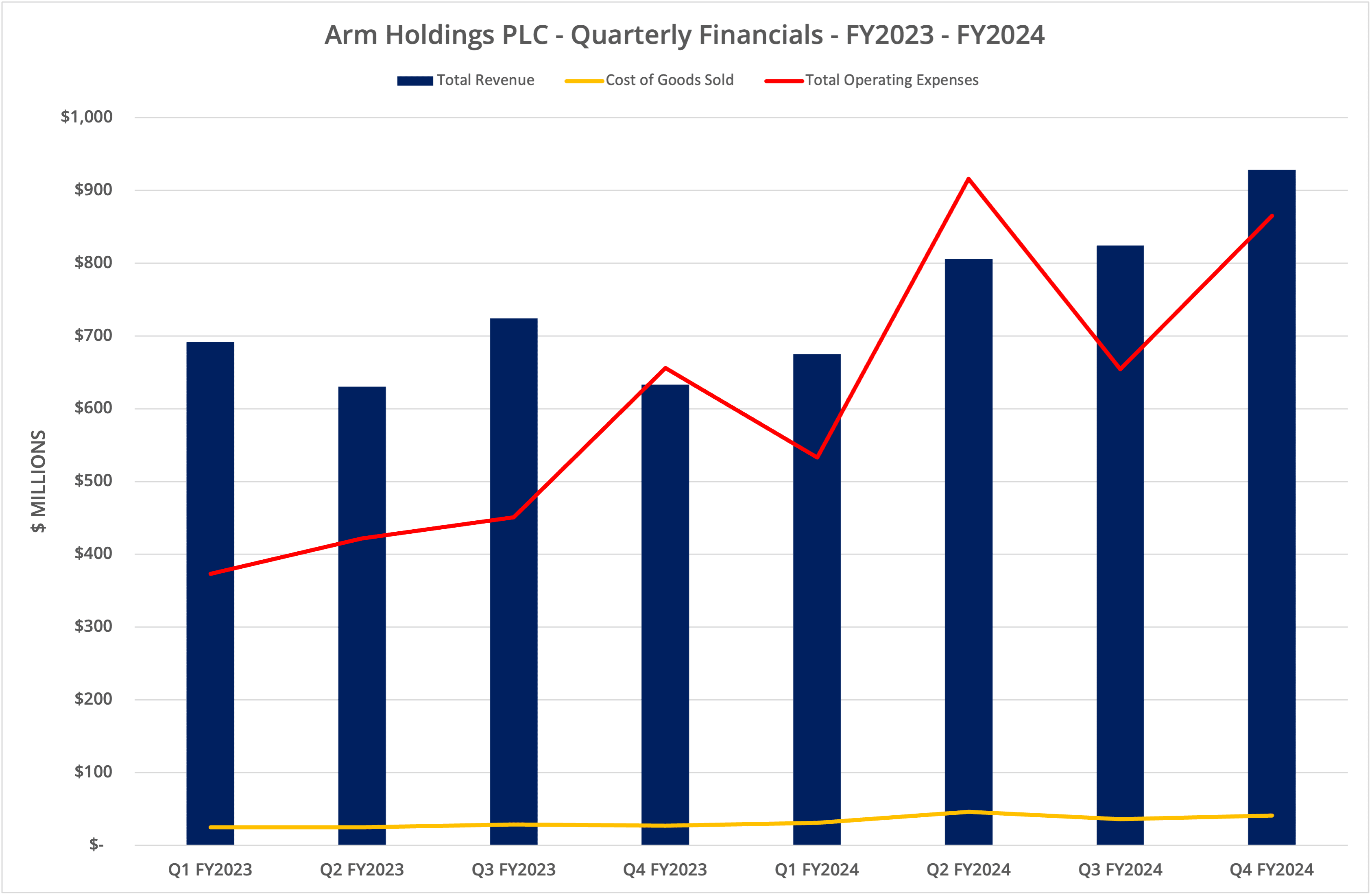

Arm Holdings PLC has announced Q4 and full-year results for financial year 2024. Revenue for the quarter was up 47% year-on-year, with 21% annual growth. License revenue grew 43% over the year, while royalty revenue was up 8%. These data look good and demonstrate the broader applicability of Arm technology in the enterprise.

Background

Arm Holdings PLC is now a public company, and although data can be pieced together from UK Companies House filings, only approximately two years of data have been made available through results announcements on the corporate website. We’ve shown three graphs, the first highlighting annual revenue and the other two showing quarterly data.

As a company that licenses intellectual property rather than manufacturing technology, Arm has a healthy gross margin, typically 95% or higher. Significant investment goes into research and development at around 60% of revenue in the last reporting period, with the remaining overheads mostly selling and administrative at approximately 30%.

Revenue Model

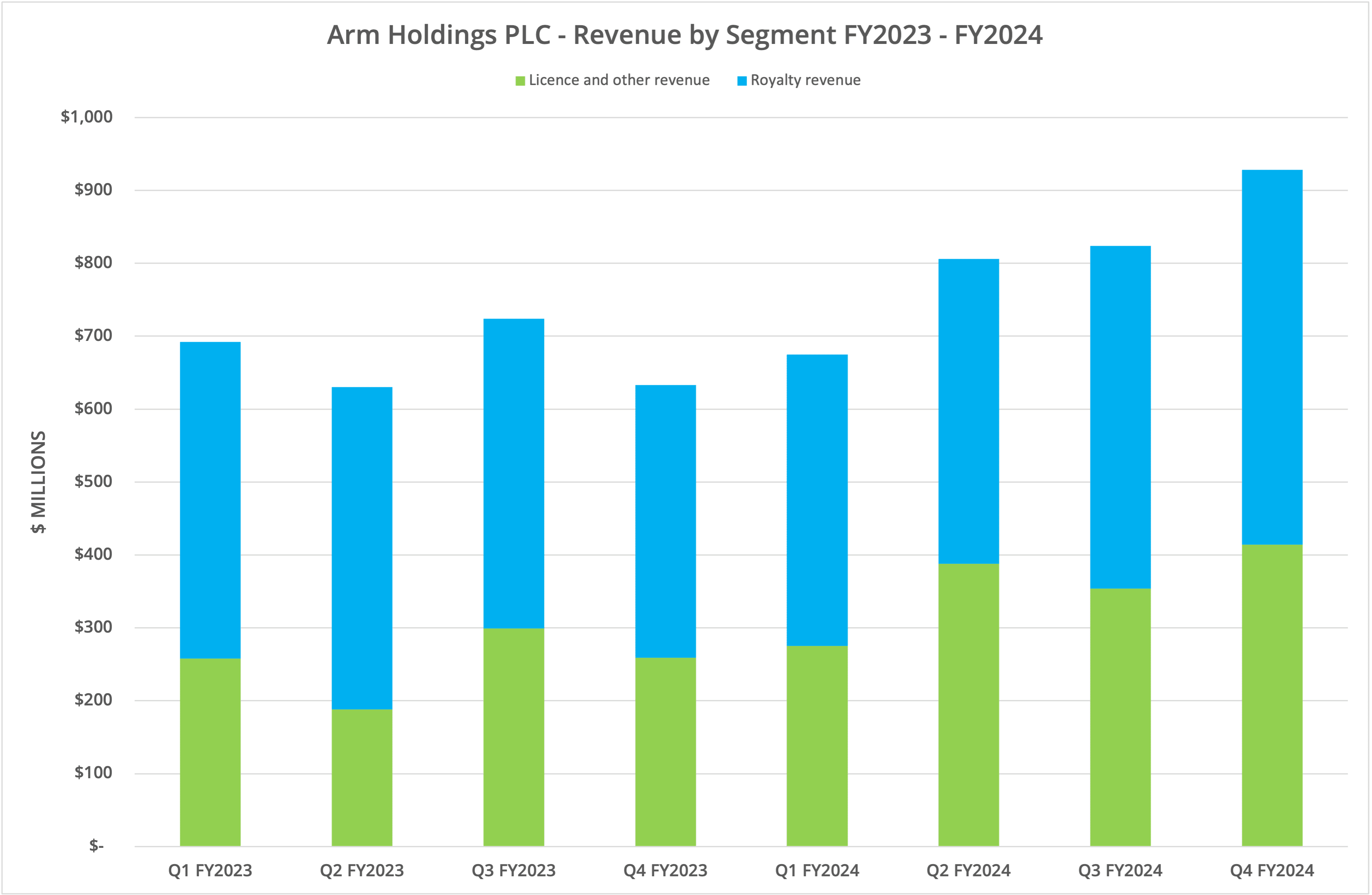

Arm both licences intellectual property and charges royalties derived from the IP. In general terms, “Licence and other revenue” covers contracts that provide unlimited use of IP, support services and professional services. The “Royalty revenue” category generally covers income from licensed IP aligned to customer shipments (such as units sold). The split of royalty versus other licences has been consistent at around 60:40, respectively (data shown in Figure 3).

Architecture

Arm is a RISC-based and proprietary instruction-based architecture (ISA). The company makes money by licensing designs to customers that then incorporate key components (such as CPU cores) into in-house customer-specific solutions. Arm has evolved from a low-power and mobile-focused market into a set of solutions that also addresses enterprise requirements,

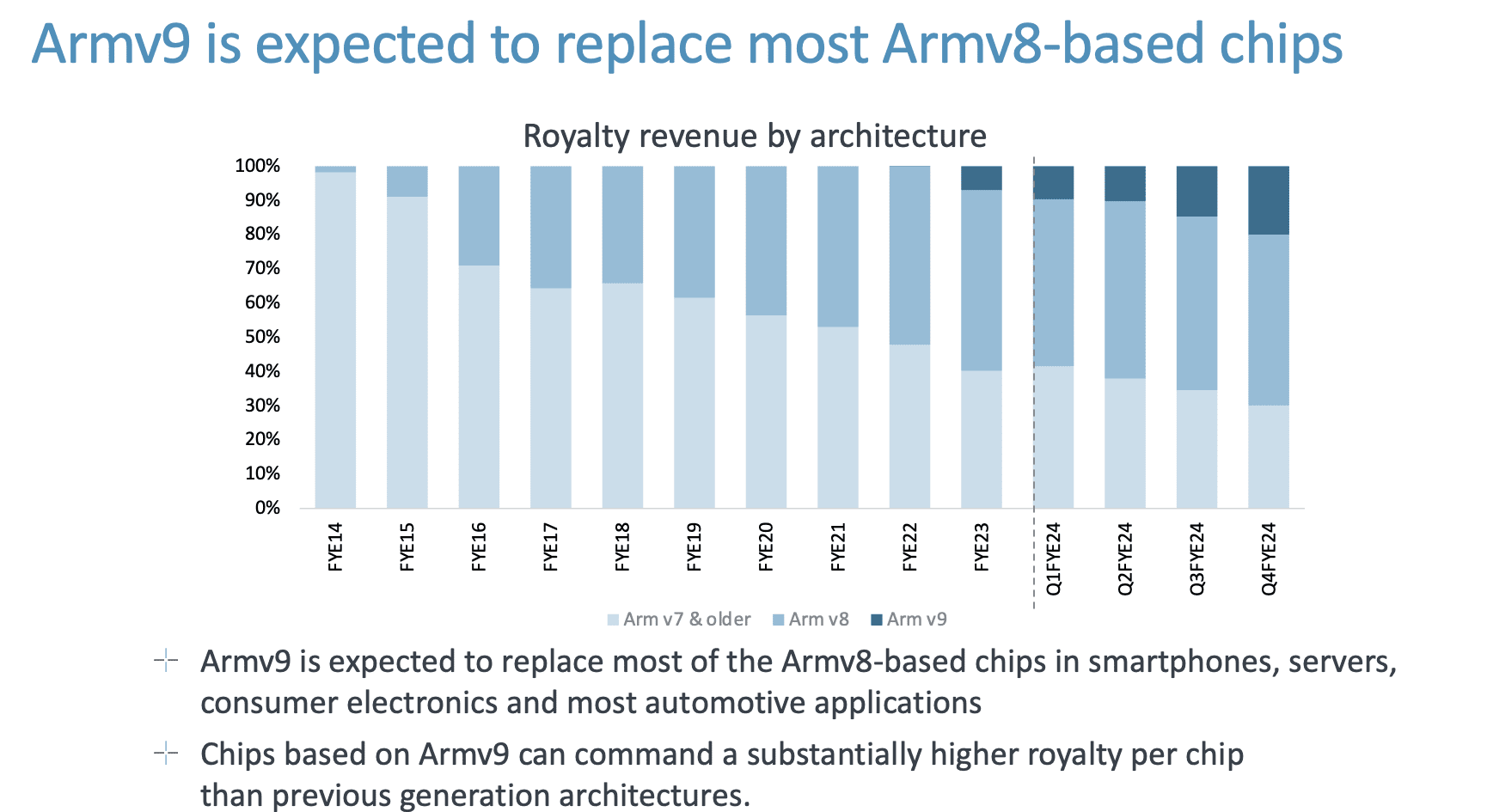

Figure 4 from the Q4 FY2024 press release shows the transition of shipments to the latest architecture designs (Armv9), gradually replacing Armv8 and Armv7 solutions. It’s interesting to note that Arm expects to see higher royalty per chip from Armv9 compared to previous generations of the architecture, presumably because these solutions target higher-end capabilities such as virtual instances in the public cloud.

Enterprise

Arm targets four main categories of solutions that include Automotive, IoT, Mobile and Infrastructure. The Mobile division includes solutions licensed to Apple for mobile devices (including iPads) and other smartphone and tablet manufacturers. We’re also starting to see other solutions enter the market, such as Qualcomm Snapdragon X Elite, which is based on the Arm instruction set (the Oryon CPU).

Back in 2020, we questioned whether Apple’s move to Arm-based silicon would have an effect on the enterprise data centre. AWS had already introduced Arm-based Graviton processors into the public cloud, and as this article explains, Graviton3 continued the use of the Neoverse architecture to improve the capability of Arm-based EC2 instances. There is also some additional background information in this blog post we published in 2020.

Neoverse

Most recently, we discussed the third-generation Neoverse designs in this research note. We also covered the announcement by Google Cloud of Axion, an Arm-based processor that will power future GCP virtual instances. Most recently, Arm was reported to be starting an AI chip division, which could result in a corporate spin-out, although the details are scarce at this time.

Evolution

Why is Arm gaining success in the current market at the expense of other CPU architectures such as x86? We see several factors influencing the transition.

- Efficiency – Arm solutions are low-power and more efficient compared to (for example) x86 CPUs. This factor has been a driving force for the public cloud, where infrastructure cost savings translate directly into increased profits. Similarly, with mobile devices, improved efficiency means longer battery life and/or lighter and cheaper products.

- Customisation – the licensing model from Arm enables its customers to build custom solutions that more precisely fit their needs. The public cloud vendors can choose (for example) to create product generations based on specific core counts and configurations while incorporating exact amounts of DRAM and I/O processing.

- Integration – the current wave of computing has evolved towards the use of AI and ML, looking more like HPC than traditional OLAP or OLTP architectures. With efficiency and customisation capabilities, vendors can build integrated solutions, such as the NVIDIA Grace Hopper superchip that focuses on application requirements rather than conforming to traditional design. The Grace Hopper design is a good example as it shows how NVIDIA can incorporate proprietary technology such as NVLink into its processor designs.

One final point worth considering is cadence. Product vendors such as Apple, Dell and HPE have been dependent on the release cycles of Intel and AMD to bring new product generations to market. Intel, for example, suffered significant delays bringing Sapphire Rapids products to 3rd party manufacturers, which in turn, affected the timeline of new servers designs.

The Arm model mitigates those issues, providing a more reliable cadence of designs and pushing the manufacturing responsibility elsewhere (where it could be managed more effectively). We’ve witnessed how quickly Apple, for example, has introduced the M1, M2, M3 and M4 architectures in recent years. AWS has followed a similar story book with the incremental improvements to Graviton.

The Architect’s View®

The rise of Arm is a classic example of the Innovator’s Dilemma. What was initially seen as a niche for low-power mobile devices has become the heart of millions of smartphones and tablets. Arm is now extending the power of the architecture, first targeting desktop and consumer devices, then the enterprise.

The enterprise market has been arguably harder to crack, as we’ve seen few (if any) Arm-based server solutions in general availability. HPE did offer Arm servers as part of the Moonshot architecture (in 2014), but the solution never really gained sufficient traction.

Through adoption in the public cloud, there are now O/S distributions readily available for 64-bit Arm, including Linux and Windows. This support extends to popular database applications, making it possible to migrate traditional workloads over to an Arm solution.

We believe that the public cloud will be the driving force that eventually pushes the adoption of Arm in private data centres. The hyper-scale platforms have already realised the efficiency benefits of Arm, both for themselves and their customers. At some point, the corporate world will come to the same conclusion and gradually adopt Arm for niche use-cases.

The challenge for private cloud is where to buy the technology. We know SoftIron already uses Arm in its hardware solutions, but apart from Bamboo Systems (which failed), no mainstream server vendor offers Arm-based solutions to our knowledge.

Part of the problem with adopting Arm is the requirement to build custom ecosystems around the Arm intellectual property. Intel, for example, will build the chipset to support its latest processors. Arm expects customers to do that work themselves. However, that process is arguably quicker today with Arm Neoverse Compute Subsystem (CSS) a process to bring Arm-based designs to market more quickly.

The second challenge is the grip on the market held by Intel and AMD. Vendors such as Dell and HPE may not want to risk favourable terms with their suppliers, which include early access to products. Development with Intel at an early stage, for example, allows products to be brought to market in line with the release of new processors.

For the end user, Arm will be an alternative architecture that introduces efficiency and cost savings. We recommend starting with public cloud instances and gaining an understanding of the operational differences (for example, O/S and application support) while benchmarking typical workloads. This process will enable the right solution to be deployed where appropriate for cost and efficiency rather than for historical precedent.

Copyright (c) 2007-2024 – Post #ccd3 – Brookend Limited, first published on https://www.architecting.it/blog, do not reproduce without permission.