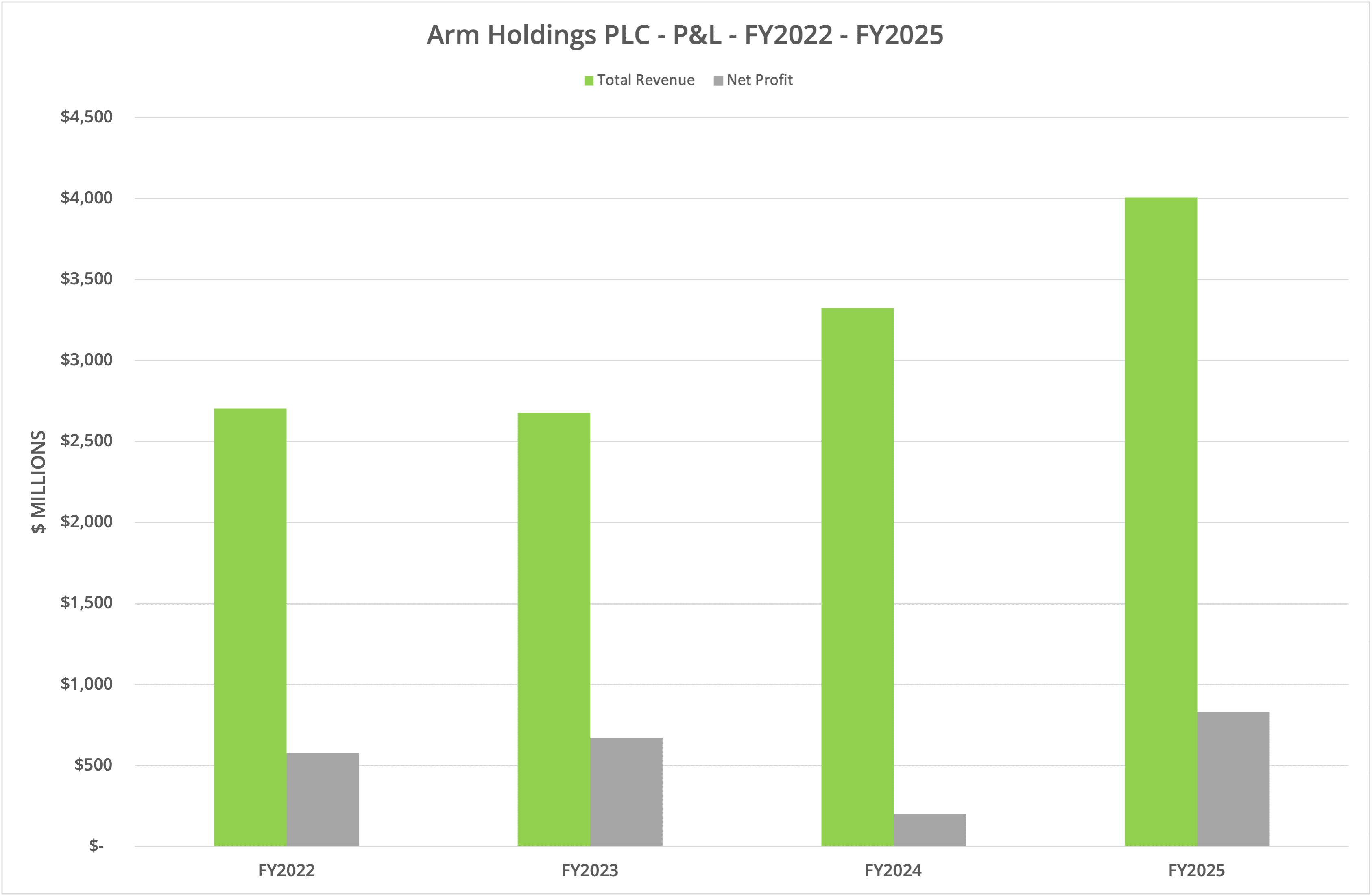

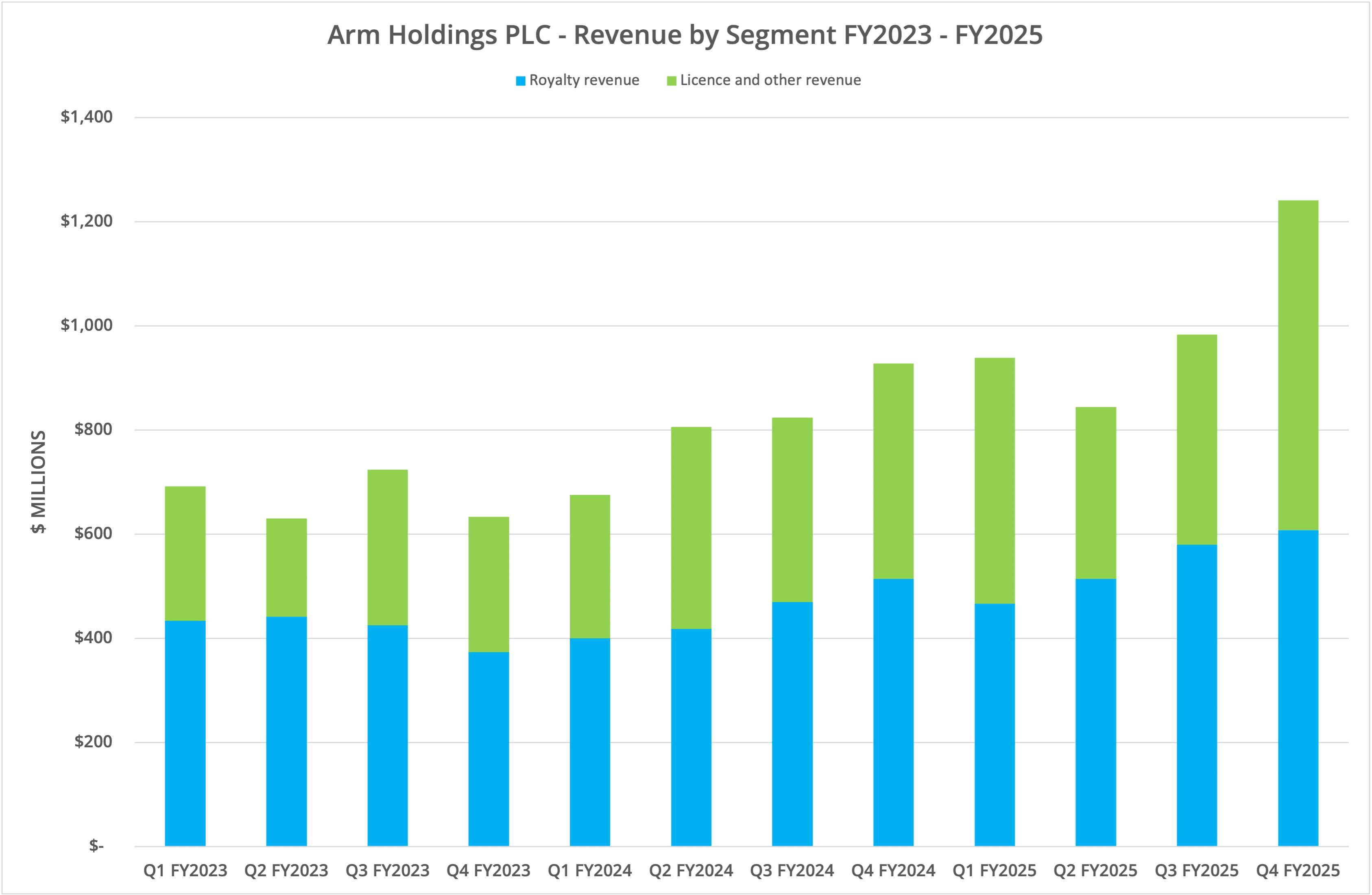

Arm Holdings PLC has announced financial results for Q4 and the full year FY2025 (ending 31st March 2025) on 7th May 2025. For the quarter, revenue rose 33.7% to $1.24 billion compared to Q4 FY2024, and for the full year, revenue was up by 20.6% at a record $4.007 billion. Net profit rose 313%. With continued growth in both Licence and Royalty revenue, Arm is profiting from the boom in AI.

Background

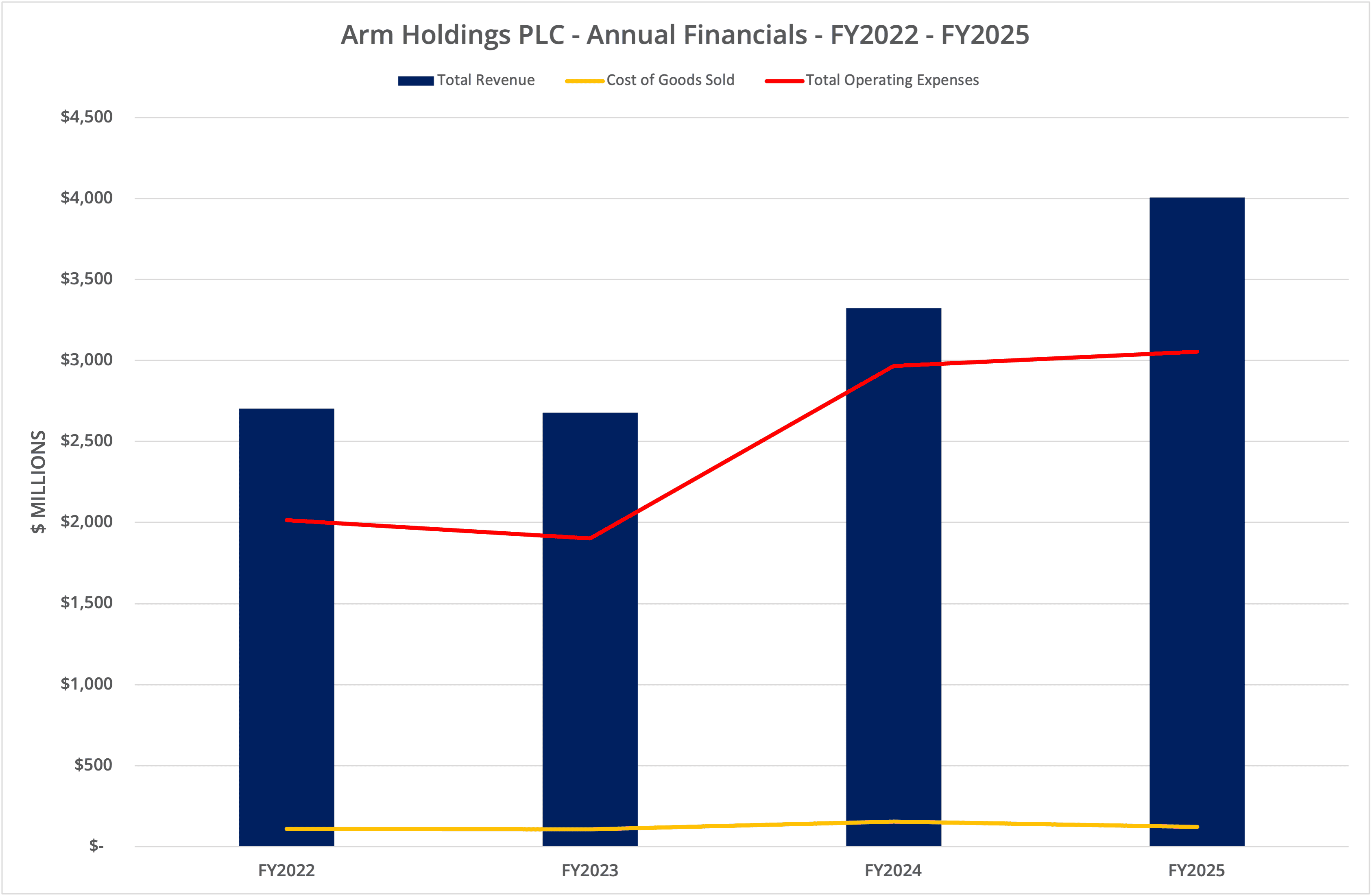

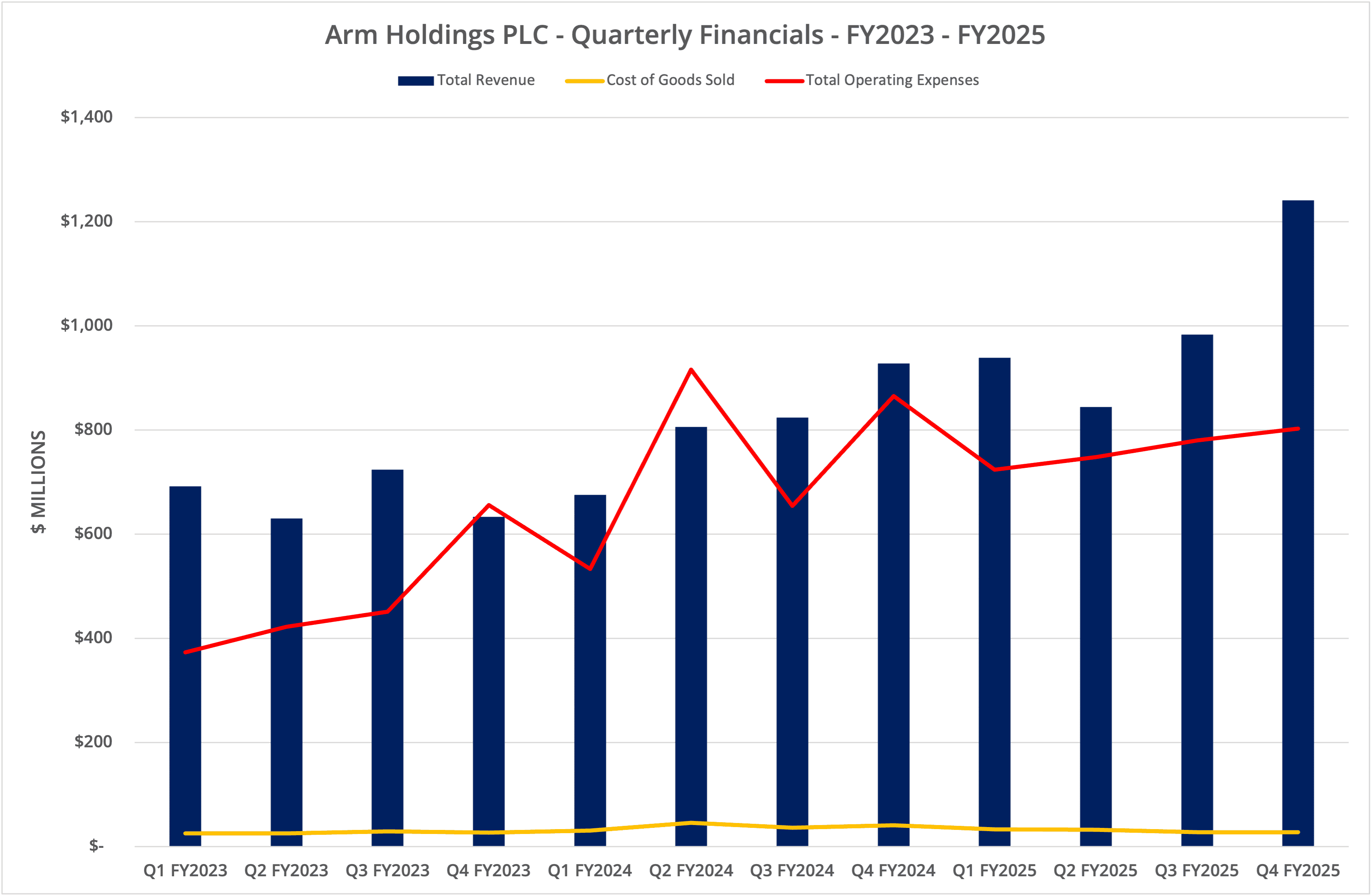

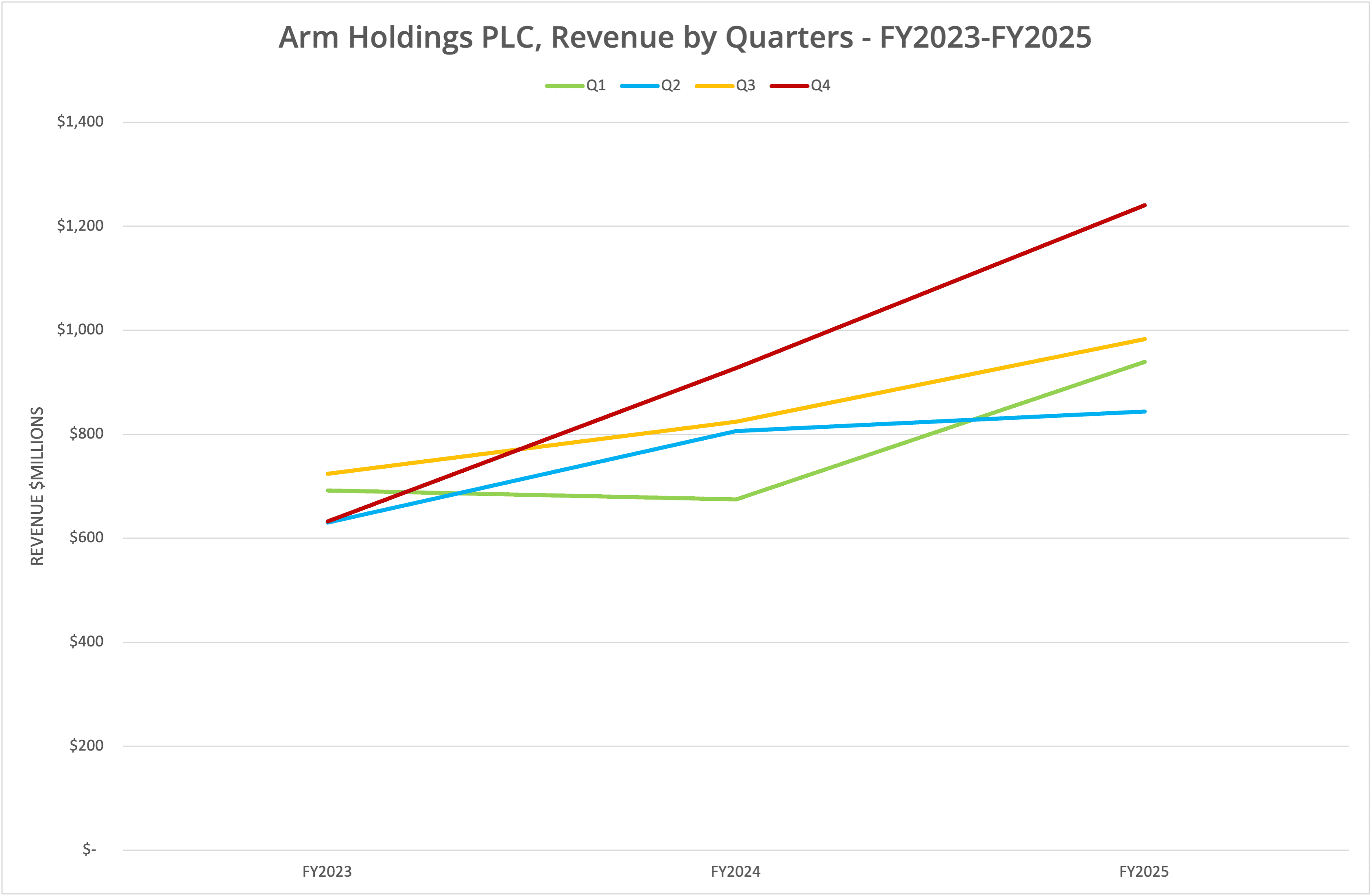

Arm Holdings PLC published financial results for the final quarter of FY2025 and the full year (ending 31st March 2025) on 7th May 2025. For the quarter, revenue rose 33.7% to $1.241 billion year-on-year, led by a 53.1% increase in Licence and Other Revenue. For the full year FY2025, revenue increased by 20.6% to $4.007 billion, again led by Licence and Other Revenue, which increased by 28.5%. By all metrics, the quarter and full year produced record results.

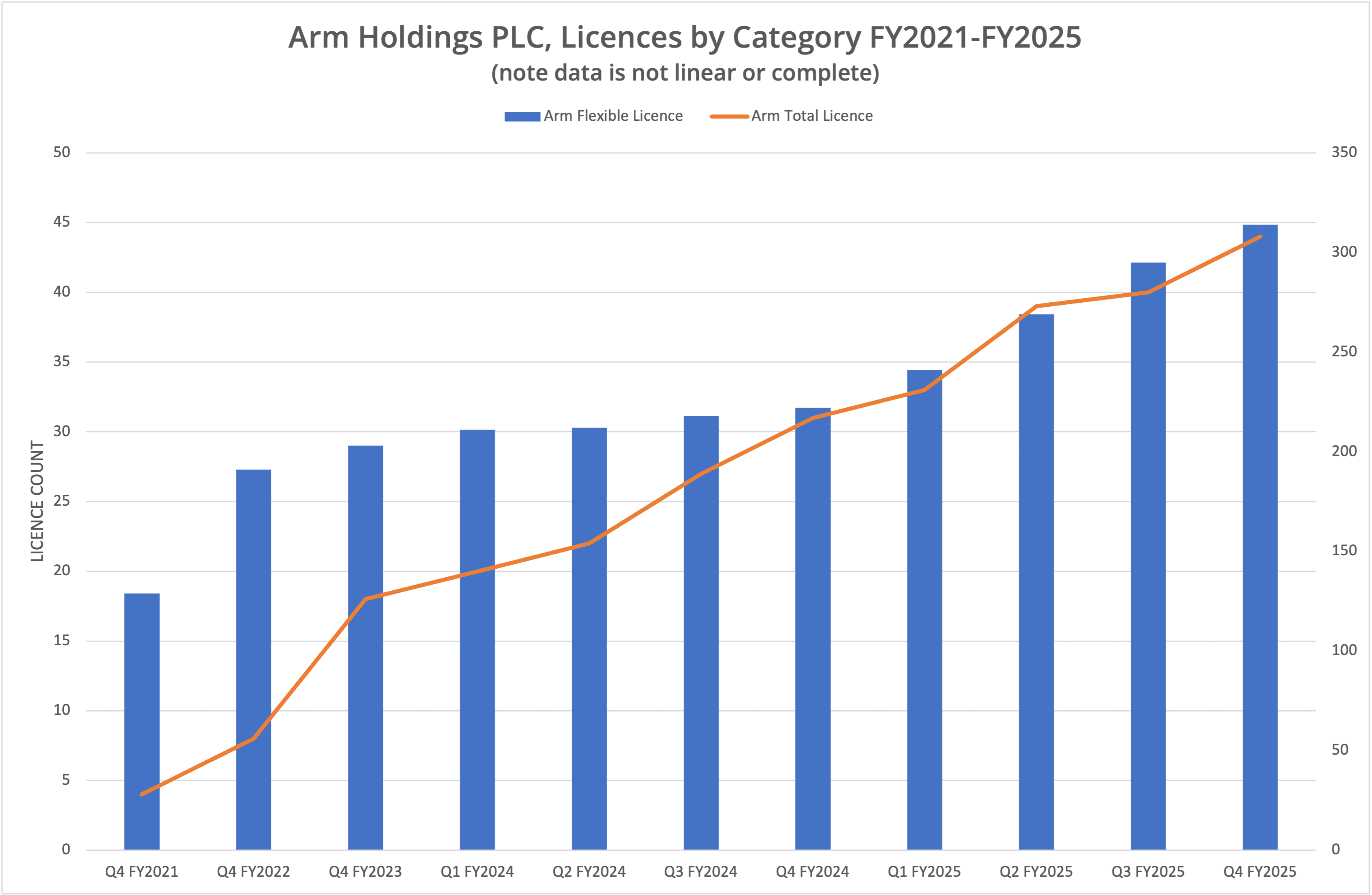

We present the data in six graphs, labelled Figures 1 to 6.

AI

In the shareholder letter accompanying the results publication, CEO Rene Haas highlighted two reasons for the continued growth in revenue and licences. First is AI, where the company believes the Arm architecture will benefit from the expansion of AI inferencing, particularly at the Edge. Second, is the growth of Arm in the public data centre.

Staying with AI for a moment, we see Arm being used in hybrid processors, such as NVIDIA’s Grace Blackwell “superchip”, combining traditional processing with GPUs. While the demand for AI continues to grow, Arm has several parallel growth channels, supporting GPU deployments across diverse locations.

Cloud

Of course, the entire computing world isn’t powered by AI, and traditional applications still represent the majority of infrastructure in use today. In the public cloud, the major platform vendors all have Arm-based offerings (AWS Graviton, Azure Cobalt, GCP Axion).

It is interesting to note that the shareholder letter indicated rapid expansion of Arm in the public cloud, with Google Axion now used by 40% of its top customers. Arm claims that close to 50% of all new server chips shipped to hyper-scalers in 2025 will use the Arm architecture.

Desktop

On the desktop, NVIDIA announced DGX Spark at GTC25, a compact development environment with over one petaFLOP of AI performance. At WWDC 2025, Apple announced the end of support for Intel desktops, which will no longer be supported in MacOS 27. Arm appears in increasing frequency in desktop solutions.

The Architect’s View®

The Arm architecture currently offers better price/performance and power/performance than x86-based processors. In the most cost-sensitive environments of the public cloud, Arm is gaining quickly over Intel and AMD. Arm claims that an increasing percentage of AI software is being written first for Arm, reducing the “friction” of migrating from one processor family to another.

Where operating systems and software are fully supported by the architecture, Arm is an easy choice for consumers of the public cloud running traditional applications. Vendors, including AWS, Microsoft Azure and Google Cloud, have done the integration work to support Arm in their ecosystems, making the choice of Arm or Intel just a click of a button.

Whether Arm gains significant success on the desktop is essentially in the hands of Microsoft. Windows on Arm works, but any wholesale migration needs an equivalent programme to that delivered by Apple (including Rosetta 2). Apple has seamlessly delivered hybrid binaries for Apple silicon and Intel, eventually shipping Arm-only binaries in a remarkable migration process.

Similarly, the data centre adoption of Arm has Microsoft dependencies, but not to the same degree as the desktop. Instead, Arm needs vendors such as Dell, HPE and Super Micro to develop and ship Arm-based hardware solutions. This process has yet to start in any meaningful way.

If we extrapolate from today’s Arm gains in the public cloud data centre, we can see several scenarios.

- Arm becomes the primary platform for new deployments, pushing x86 aside. Customers gain confidence and trust in Arm-based instances, which become the preferred choice due to price/performance.

- The public cloud becomes more competitive than on-premises infrastructure, as the cloud vendors can pass savings on to their customers. Self-built infrastructure on-premises using x86 starts to look relatively more expensive and is de-prioritised by businesses, except for sovereignty use cases.

- Eventually, one of the leading server vendors makes the leap to Arm, starting an arms race (no pun intended) to offer the most comprehensive and scalable solutions.

In the current market, once one vendor adopts Arm, then we believe the game is over for Intel and AMD. However, competition is never linear. If this were a game of chess, we would say Arm is on the attack while Intel/AMD are defending. A chess game can change in an instant, and so could the data centre processor market if Intel or AMD choose to deliver competitive products (from a price/power/performance perspective).

At this point in time, we don’t rule Intel or AMD out of the game. But unless some radical change is made to x86, we can only see x86 being pushed into being a niche and, eventually, legacy architecture.

Meanwhile, Arm continues to go from strength to strength, a position we see repeating itself for many quarters to come.

Copyright (c) 2007-2025 – Post #2aa3 – Brookend Limited, first published on https://www.architecting.it/blog, do not reproduce without permission.