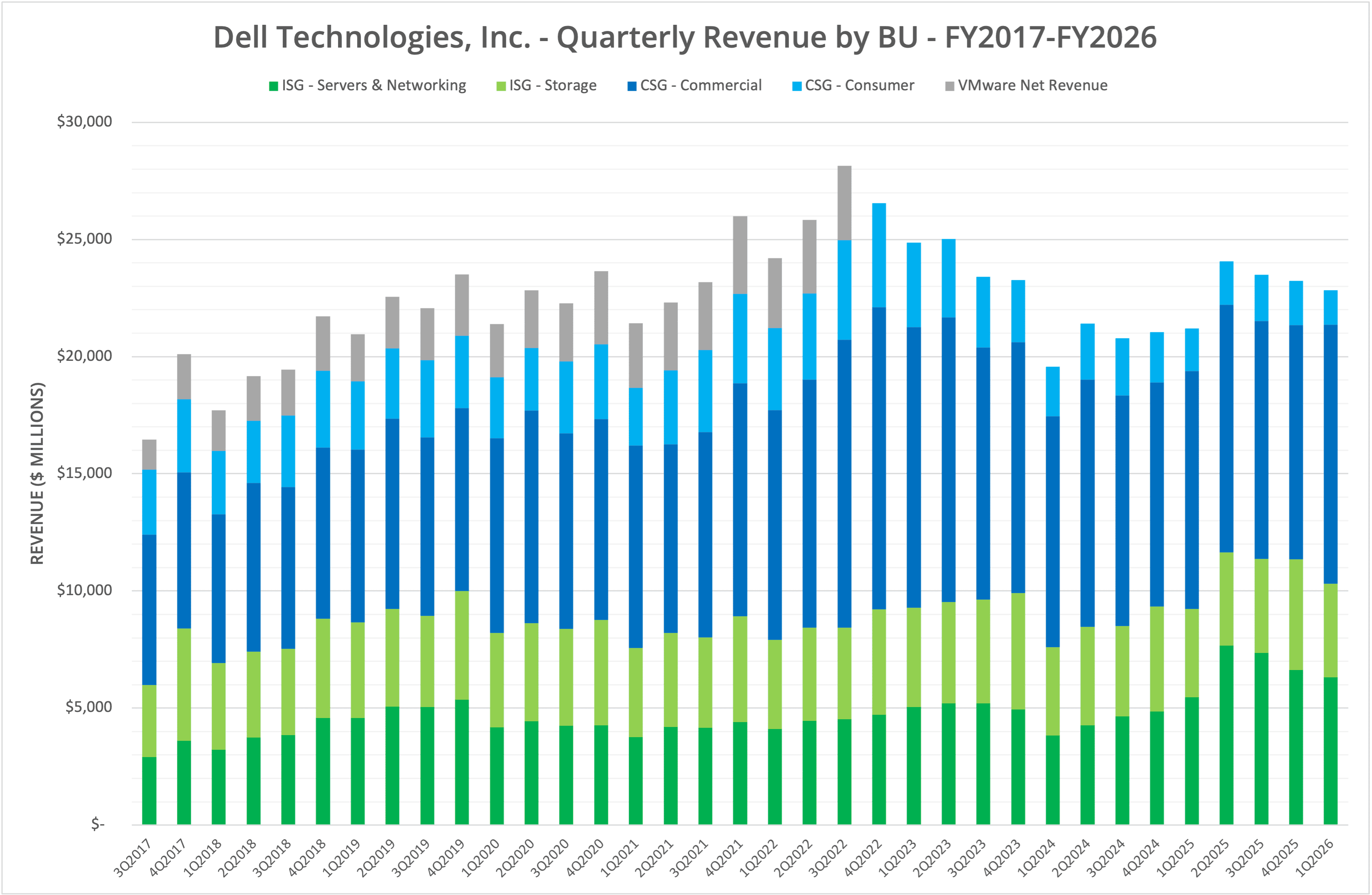

Dell Technologies, Inc. announced financial results for the first quarter of FY2026 (ending 2nd May 2025) on 29th May 2025. Revenue for the quarter rose 5.1% to $23.4 billion compared to Q1 FY2025. By division, ISG was the bigger contributor, with an 11.8% rise, compared to 4.5% for CSG. Of all lines of business, Servers & Networking was the strongest performer, as AI continues to dominate sales.

Background

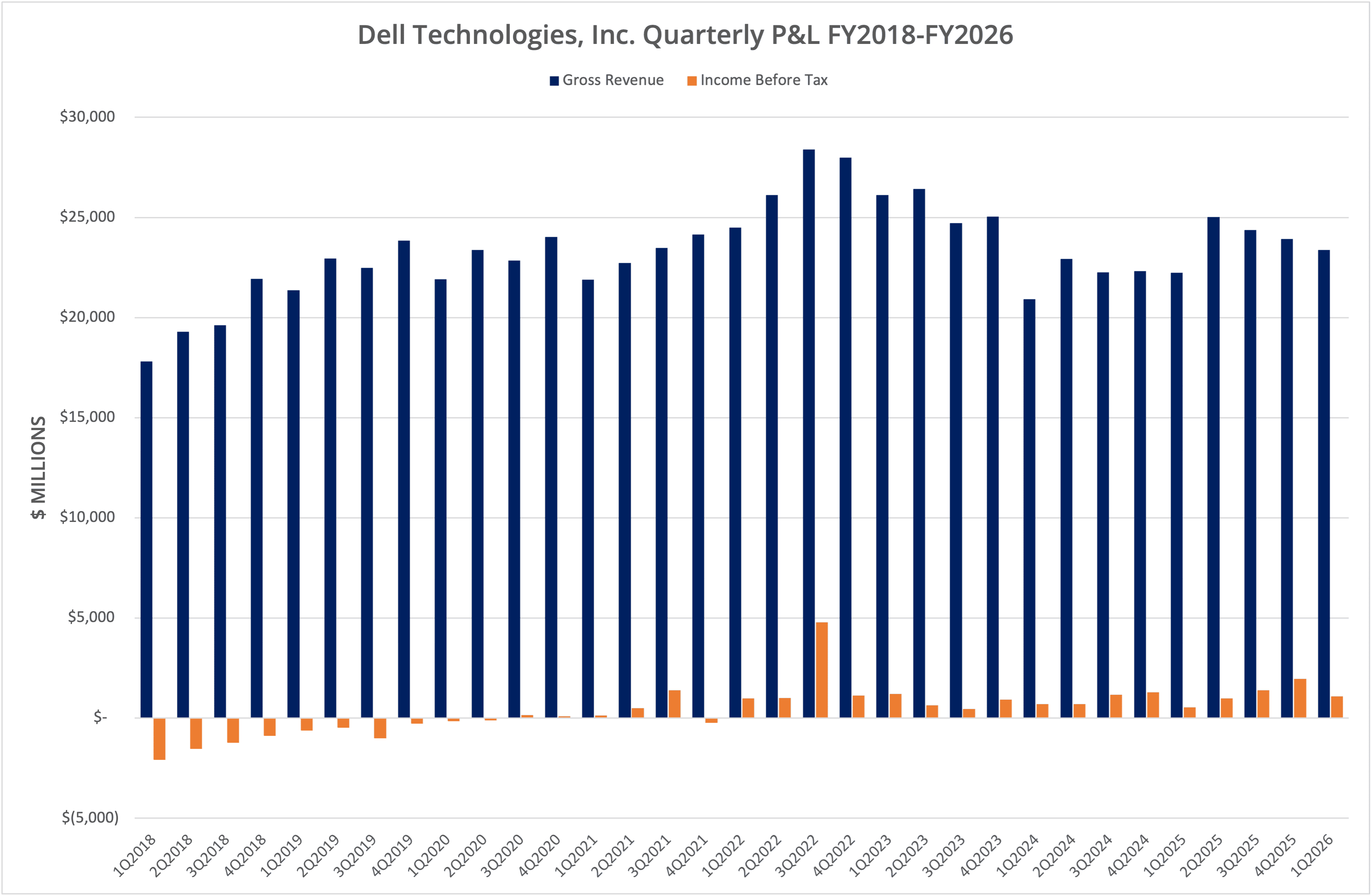

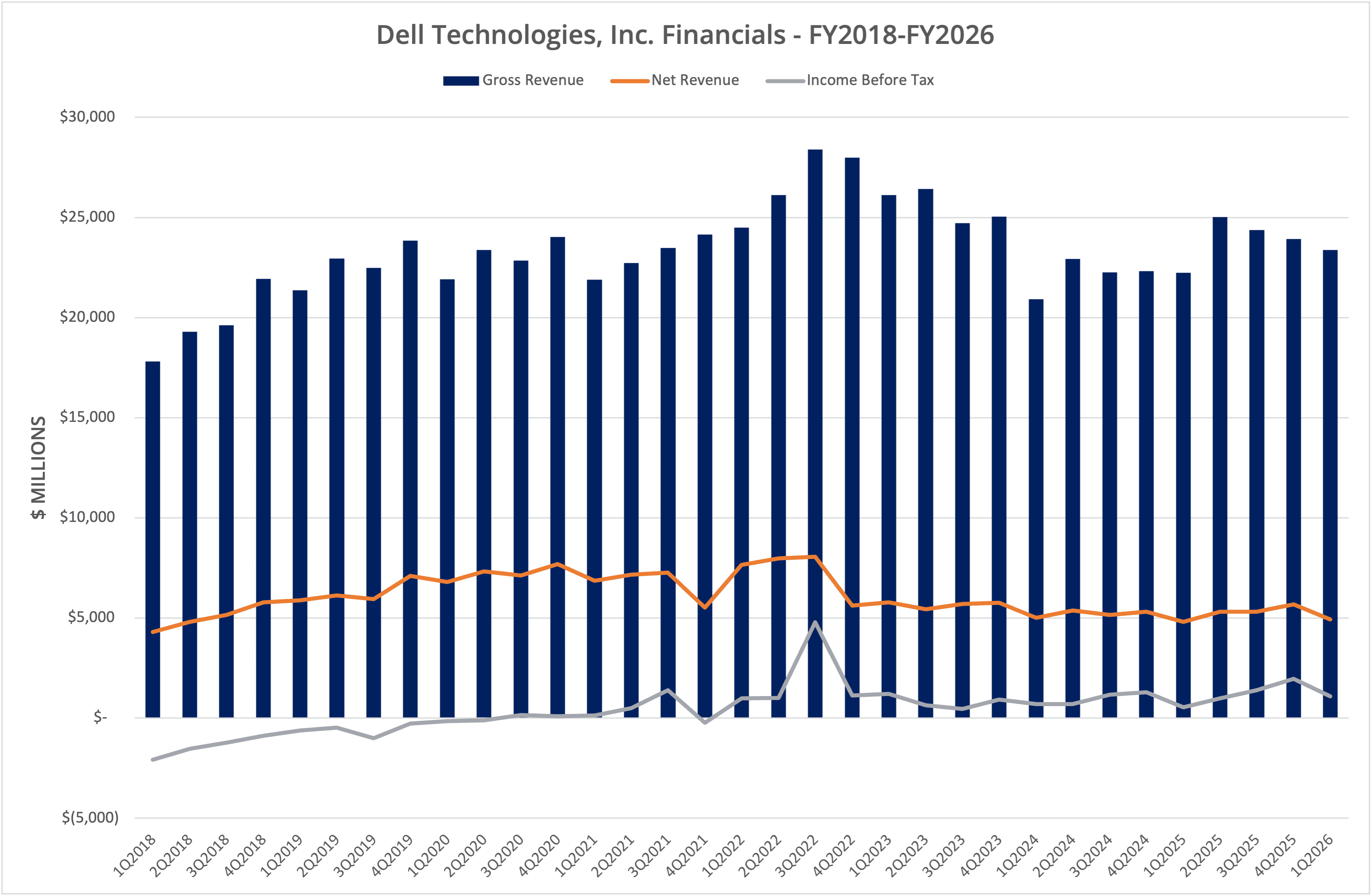

Dell Technologies, Inc. declared financial results for Q1 FY2026, the period ending 2nd May 2025) on 29th May 2025. Total revenue was up 5.1% to $23.4 billion for the quarter, with net income of $1.2 billion ($920 million in Q1 FY2024).

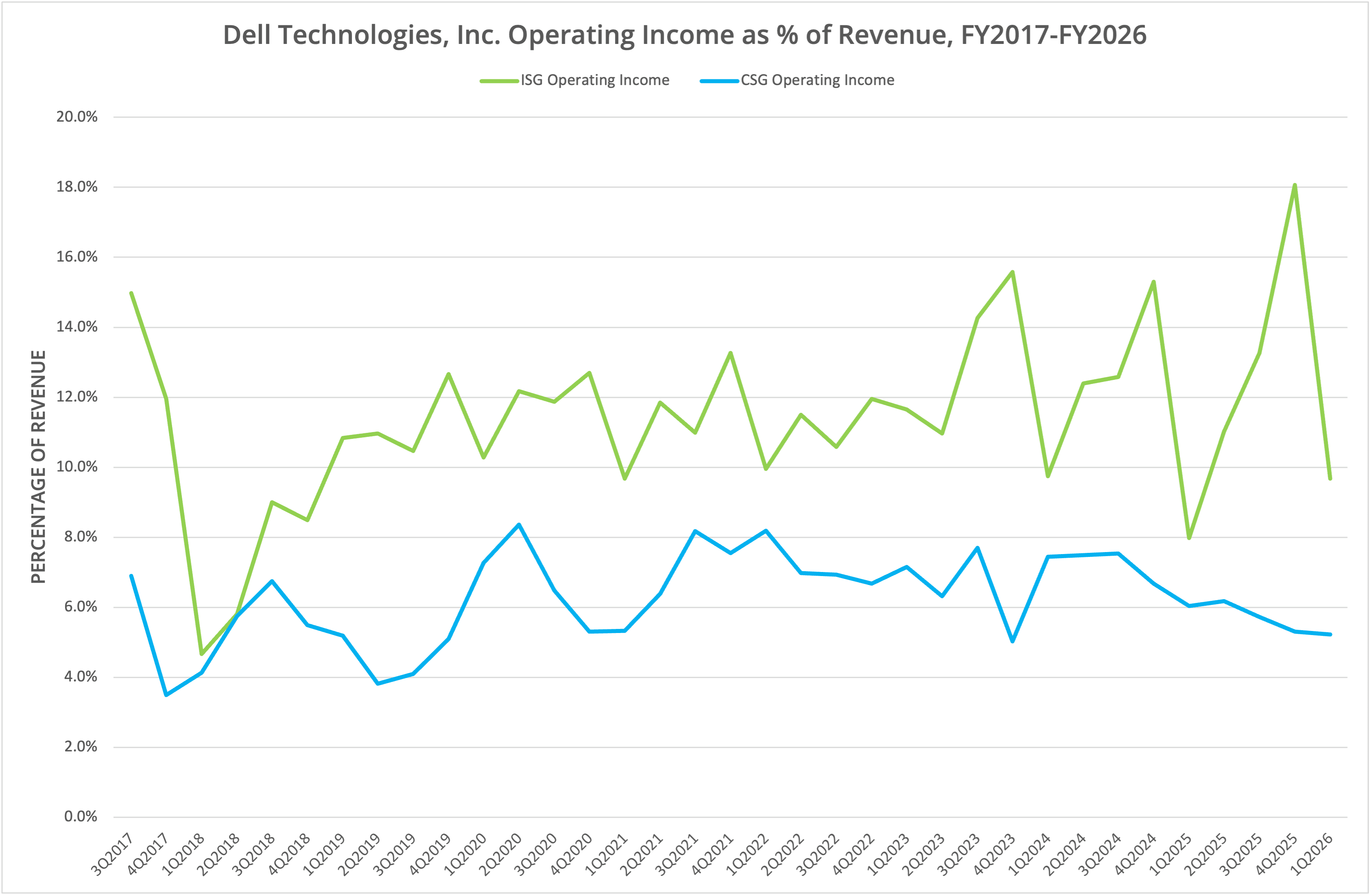

By business unit, ISG (enterprise storage and servers) rose 11.8% year-on-year but fell 9.1% sequentially, the third quarter of consecutive decline (overall revenue has also declined for three quarters). CSG (consumer) rose 4.5% year-on-year and 5.3% sequentially, driven by a 10.5% sequential improvement in CSG (Commercial).

In the ISG (Storage) division, the area we track against other vendors, Dell published a 6.2% increase year-on-year but a 15.3% decline sequentially.

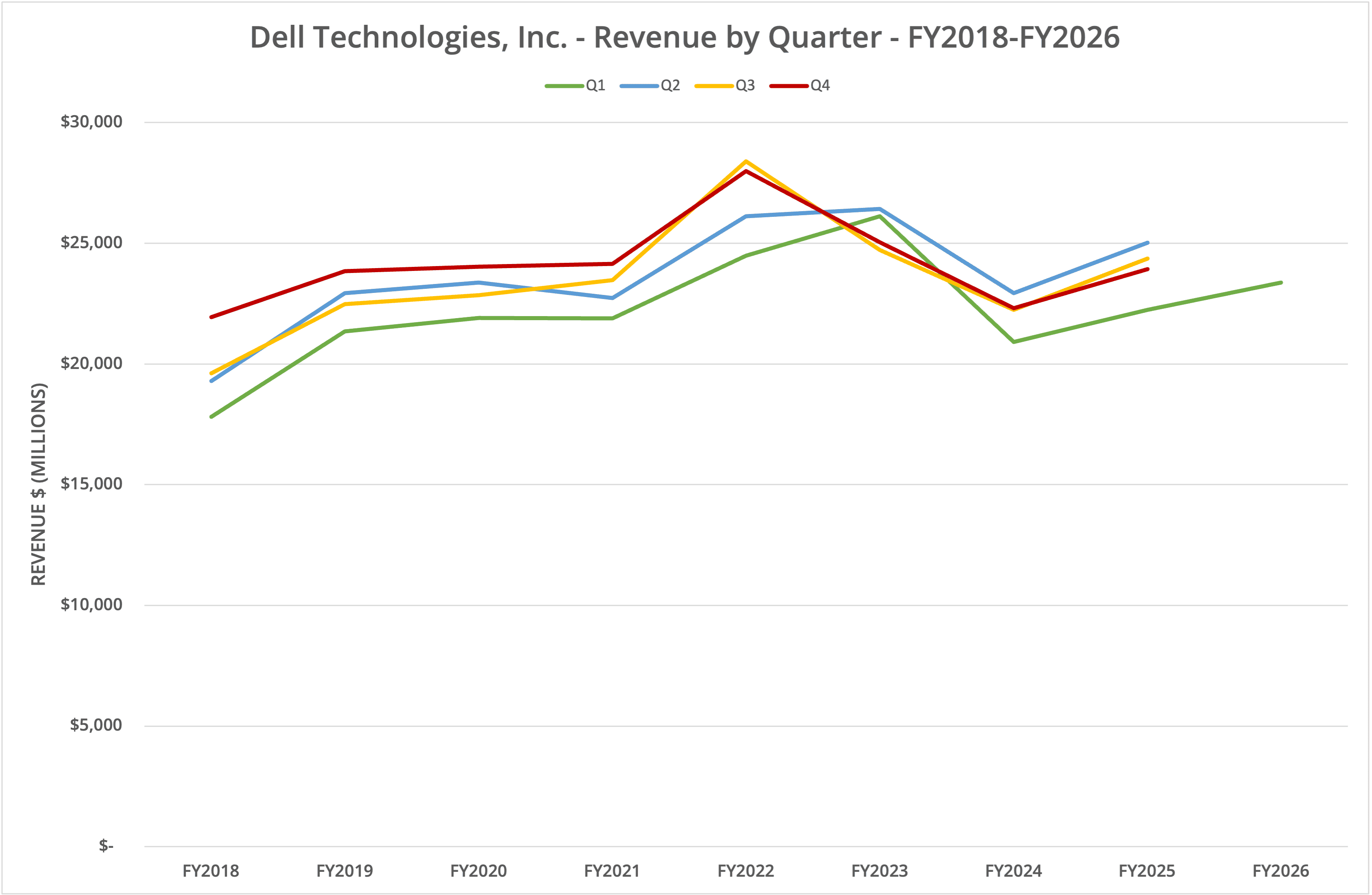

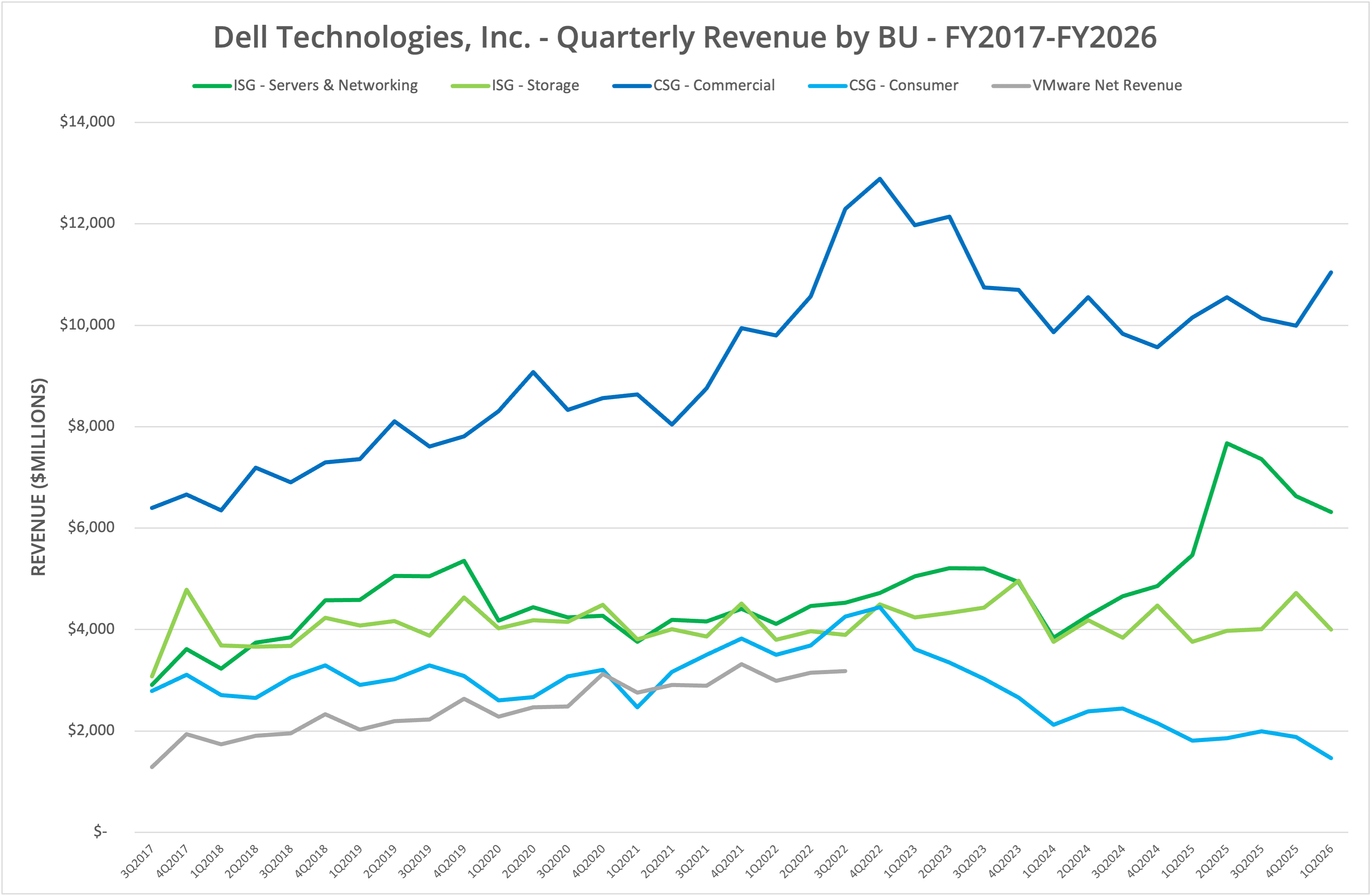

We present the data in six graphs labelled Figures 1 to 6.

Flatline

As Figure 6 shows, the Storage division has hovered around the $4 billion quarterly revenue figure since Dell returned to public ownership in Q3 FY2017 ($4.1 billion average over 35 quarters). That start date is approximately the time at which the EMC acquisition was completed (7th September 2016). However, since 2017, US inflation has risen 30%, representing a revenue decline in absolute terms.

Idling

Looking at the announcements from Dell Technologies World, the problem becomes apparent. There were no storage product announcements made at the event, except for the future promise of Project Lightning, a parallel file system enhancement to PowerScale (the Isilon platform first developed 25 years ago). The last PowerStore announcements were released in February 2025 but didn’t include new hardware revisions. Instead, the software enhancements continue to catch up with features already offered by the competition.

In contrast, we see Pure Storage continuing to gain market share (up 12.3% year-on-year), while new entrants such as VAST Data are claiming around $500 million in annual revenues and growing.

Stickiness

Of course, Dell Technologies continues to claim leadership in the storage market, and almost 10 years after the EMC acquisition was first announced, the company still leads in revenue terms. EMC was so far ahead of its competitors that even after 10 years, Dell Technologies can continue to claim the #1 position.

Storage is a sticky business. Companies (particularly the smaller ones) like to stay on a technology they feel comfortable with, which is one of the reasons Dell decided to revamp rather than replace VNX a few years ago. This market quirk has served Dell well, sweating the assets acquired from EMC.

The Architect’s View®

We view Dell Technologies as an opportunistic player in the enterprise infrastructure market. Currently, the biggest revenue generator for the company is to assemble and sell servers with embedded GPUs. Meanwhile, Storage and the Consumer division have taken a back seat, either declining or adding little incremental value to the bottom line.

With such a significant market share in storage, Dell can afford not to prioritise R&D on the storage platforms. Yes, there are enhancements being made, with new features and extended functionality. But crucially, the hardware isn’t being incremented as fast as the competition.

As we highlighted four years ago, Dell’s storage products are probably “good enough” to stop the majority of customers from defecting elsewhere. But the company isn’t taking the technology leadership position that EMC once did.

For Dell Technologies, the lack of growth must be disappointing. However, for customers, this trend is a red flag. It demonstrates that being on Dell Storage might not be the most advanced or efficient solution available. For thousands of small PowerScale customers, this may not be a problem. For larger enterprises, it might be time to look elsewhere.

It would be a shame to see the legacy of EMC decline to nothing. However, “every dog has his day”, as the expression says. Whereas the IBM mainframe is still a platform that offers some benefits to the dwindling customer base, there’s nothing unique in PowerScale, PowerStore or PowerFlex. Perhaps only PowerMax offers enough differentiation to be worthwhile keeping in the enterprise.

We believe Dell Technologies will keep delivering incremental improvements to the Power storage range of solutions but will decline in relevance and eventually be surpassed as the market leader. That transition may still be many years away, but one day, it will come.

Post #bcdc. Copyright (c) 2025 Brookend Ltd. No reproduction in whole or part without permission. Dell Technologies is an Architecting IT Tracked Vendor.