Western Digital Corporation has announced financial results for the third quarter of FY2025, ending on 28 March 2025. In the first full period of reporting since the SanDisk split, revenue declined 5% sequentially to $2.29 billion but was up 31% compared to Q3 FY2024, based on restated data that excludes the SanDisk business. However, shipped units show a decline. So, as Seagate’s data already shows, is the HDD refresh cycle with hyper-scalers now over?

Background

Western Digital Corporation has published financial data for Q3 FY2025 (the period ending 28 March 2025) on 30 April 2025. This is the first full quarter after the floatation of SanDisk as a separate legal entity. Some SSD revenue could remain in the published data. However, Western Digital has not separated out Flash and HDD revenue for this period and indicates that any residual SanDisk revenue is treated as discontinued business. This makes historical comparisons somewhat difficult, so we are driven by the restated data provided by Western Digital during the announcement.

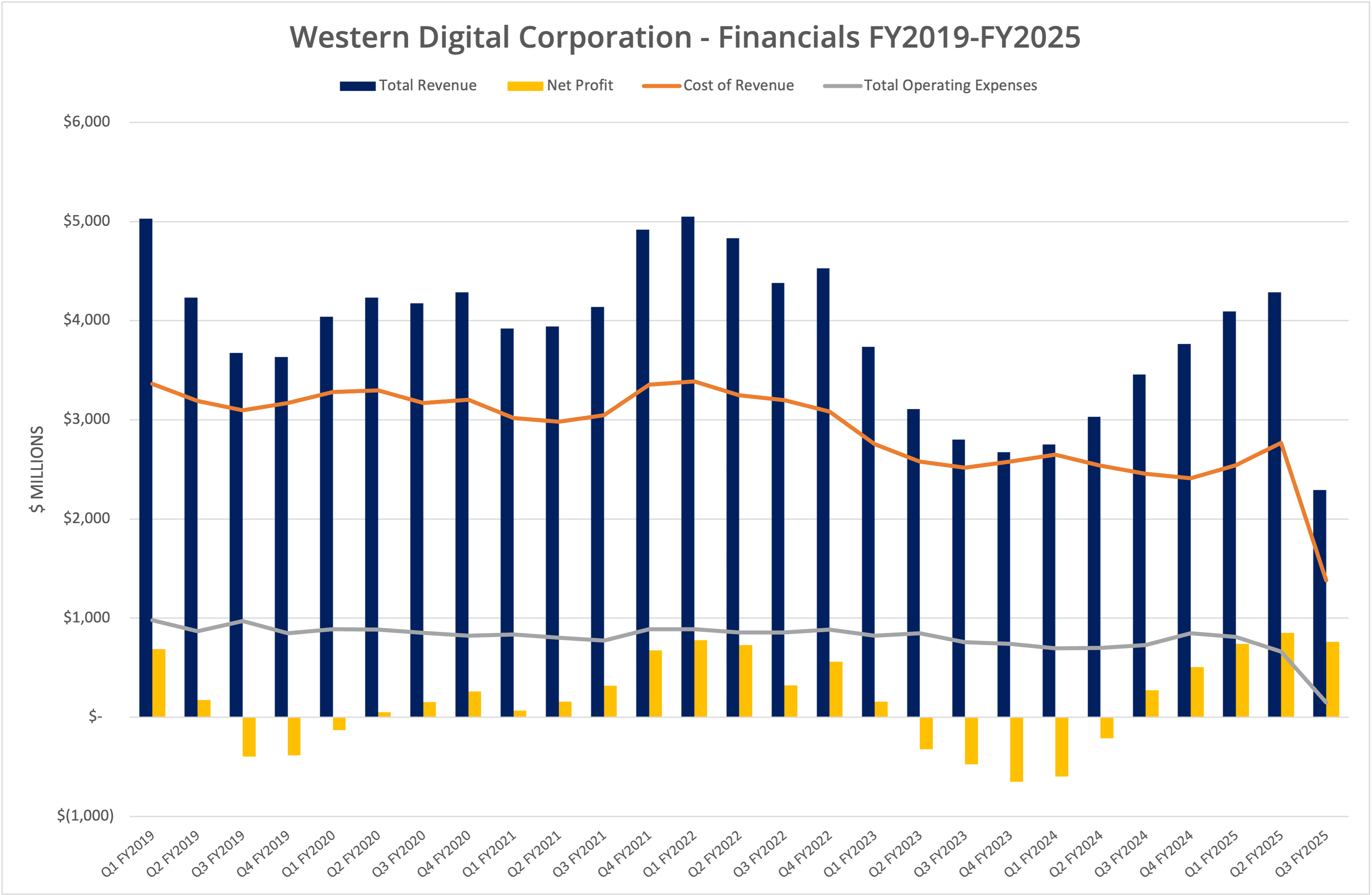

Revenue for the period Q3 FY2025 was $2.29 billion, compared with $2.41 billion for Q2 FY2025, representing a 5% decline sequentially. Restated data for Q3 FY2024 shows a 31% increase in revenue (from $1.75 billion).

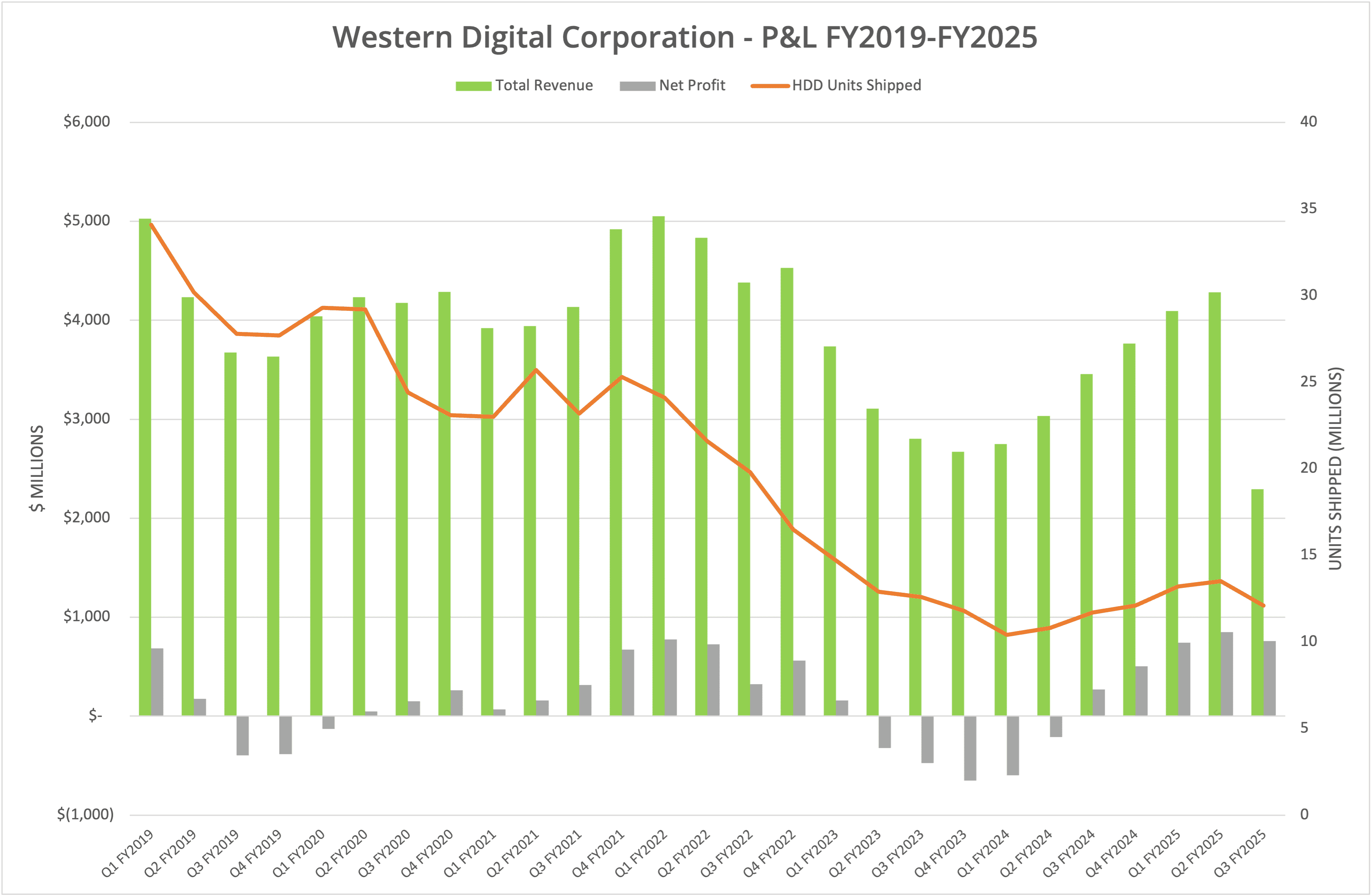

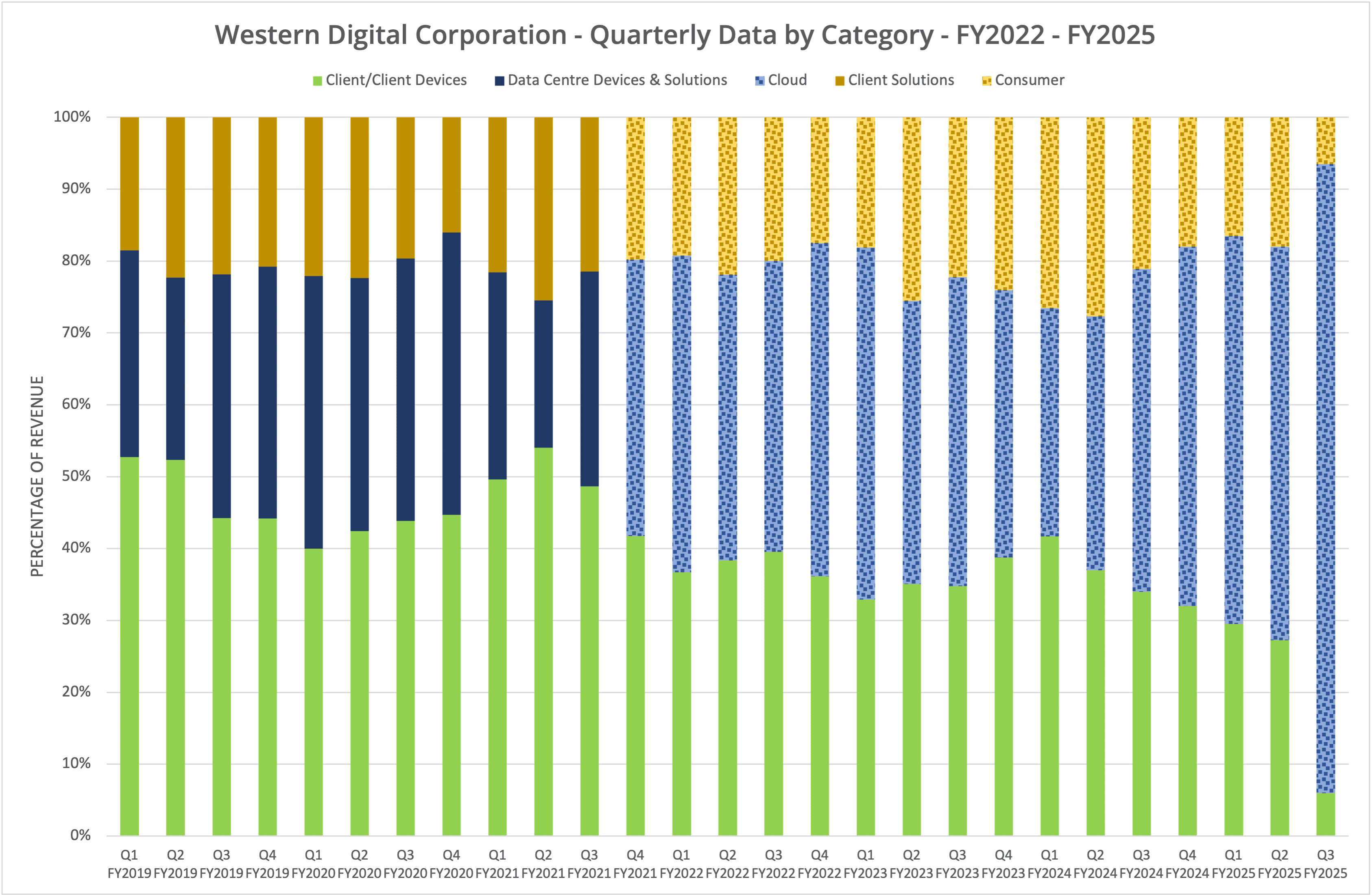

We show the data in four graphs labelled Figures 1 to 4. However, once again, we caution that the data now shows financial results minus the value brought by SanDisk, which needs to be considered in that context.

Units

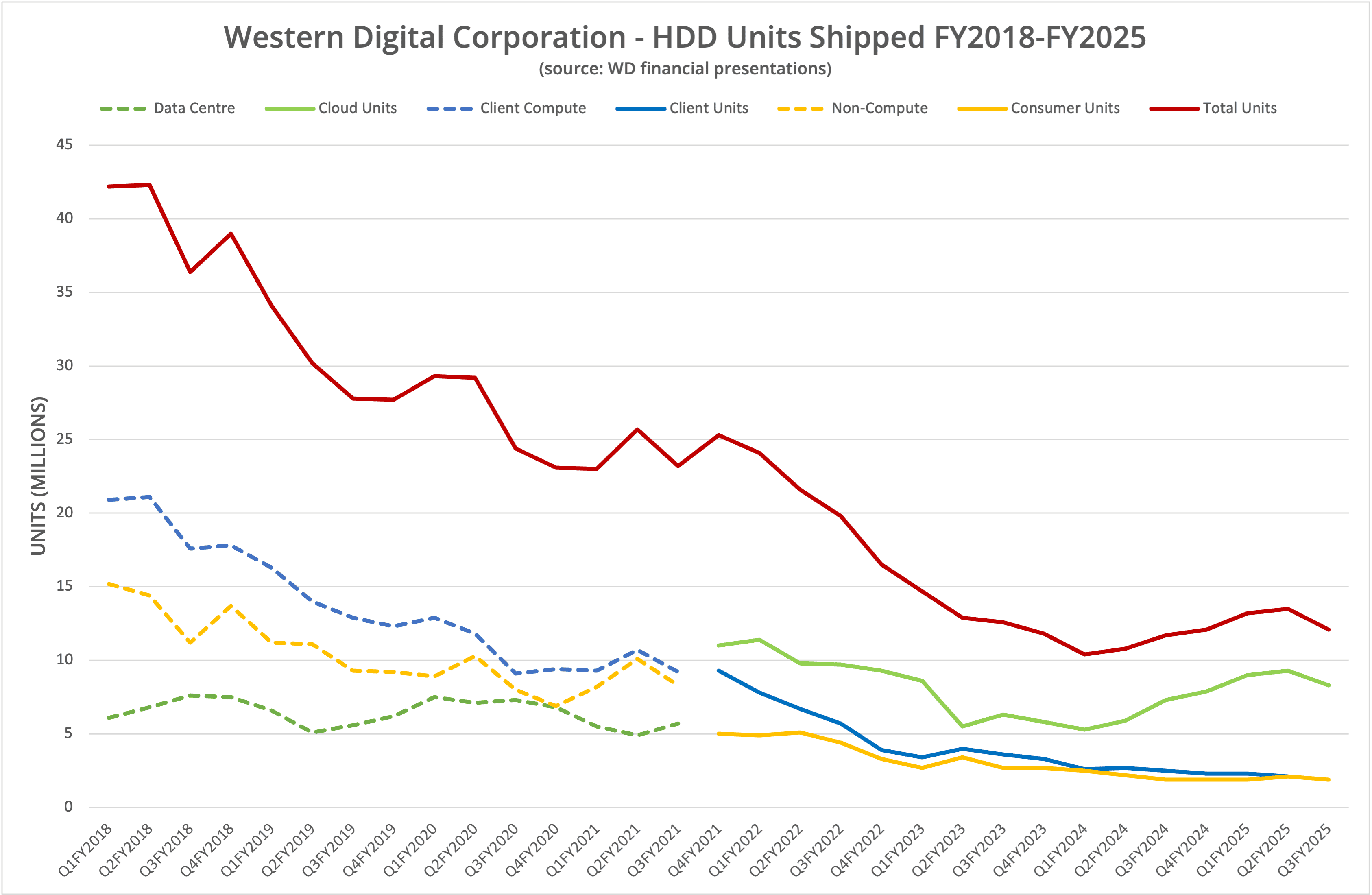

Rather than focus on financial data, which will make little sense until a few quarters are completed (and we do not give financial advice), we should look at unit numbers and the division across customer types. This data is shown in Figures 2, 3 and 4.

Figures 2 and 4 show units shipped by quarter, which declined 10.4% sequentially to 12.1 million and was up slightly year-on-year by 3.4%. In a similar trend to that seen for Seagate (see this Q3 FY2025 analysis), units shipped have peaked and are starting to decline.

Western Digital offered no specific reasons for the shipping decline (whereas Seagate suggests supply constraints and manufacturing issues). Therefore, we can only assume that the Cloud business, which now comprises 87.5% of revenue (see Figure 3), has seen a reduction in demand.

Separation

Although the separation of the SanDisk business does make Western Digital’s financials look more attractive (looking at expenses and net profit), we’re not regarding the company from a financial analysis perspective. Instead, we are interested in how the HDD business will fare, post separation from SanDisk.

The Architect’s View®

Like Seagate, Western Digital has become entirely dependent on the Cloud market, meaning hyper-scale customers specifically. This position must be seen as a significant risk to the future of the business for several reasons.

Firstly, increasingly larger volumes of workloads are being moved to SSD (see the Seagate report for a link to a Meta blog discussing the use of QLC NAND), which will only continue as a trend.

Second, maximum read-optimised SSDs currently offer 120TB+ capacities with low power and space efficiency. Even with HAMR, the gap between HDD and SSD density will continue to grow, with a consequent implication for TCO.

Third, HDDs have not increased in performance for many years. Nearline drives operate at 7,200 RPM, which means fixed rotational latency delays on each I/O, while generally, we have seen no improvement in seek time (time for the head to move to the appropriate track for read/write). Performance gains have been achieved by the increase in bit density under the read/write head, but this is a linear gain, whereas bit density increases by area. SSD performance continues to improve, limited only by PCIe bus speed.

Fourth, techniques such as SMR introduce complexity to the writing process, further reducing the performance of HDDs (although vendors have looked to mitigate that problem with onboard NAND & DRAM cache). Over time, HDDs will become increasingly worse in I/O performance compared to NAND/SSD, further increasing the disparity between the two solutions.

As we have highlighted before, HDDs are not going away anytime soon, as there is significant investment in the technology across the IT industry. There is insufficient capacity for HDDs to be entirely replaced by SSDs, while the cost economics of doing so do not currently add up.

But the migration away from HDDs is one of attrition. Over the history of the public cloud, we have seen the top hyper-scalers look for any opportunity to both reduce costs and take ownership of the technology they depend upon. We believe the same process will happen with storage that has already occurred with processors and server infrastructure.

At some point, the hyper-scale community will build bespoke storage solutions and have much less dependency on HDD vendors. When that time comes, it’s game over for the likes of Seagate and Western Digital. The biggest challenge is putting a timescale on that existential event.

Copyright (c) 2007-2025 – Post #fc33 – Brookend Limited, first published on https://www.architecting.it/blog, do not reproduce without permission.