Intel Corporation has announced financial data for the first quarter of FY2025, ending on 29 March 2025. Revenue was essentially flat, declining 0.4% year-on-year to $12.7 billion, with a loss for the quarter of $301 million. Intel Products declined by 1.5%, while Foundry improved by 7.1%. The prospects for growth look poor, with significant cost-cutting on the horizon.

Background

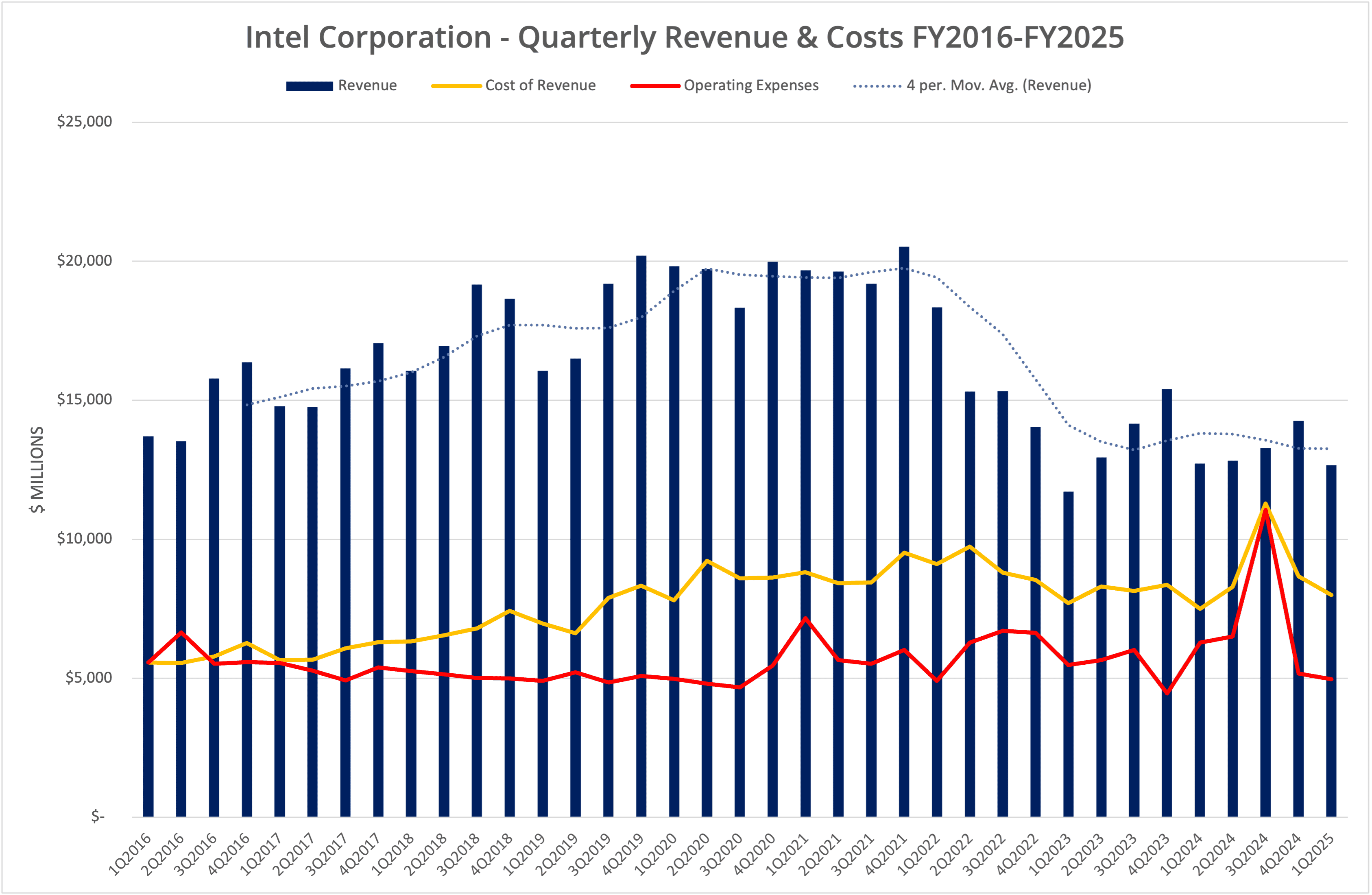

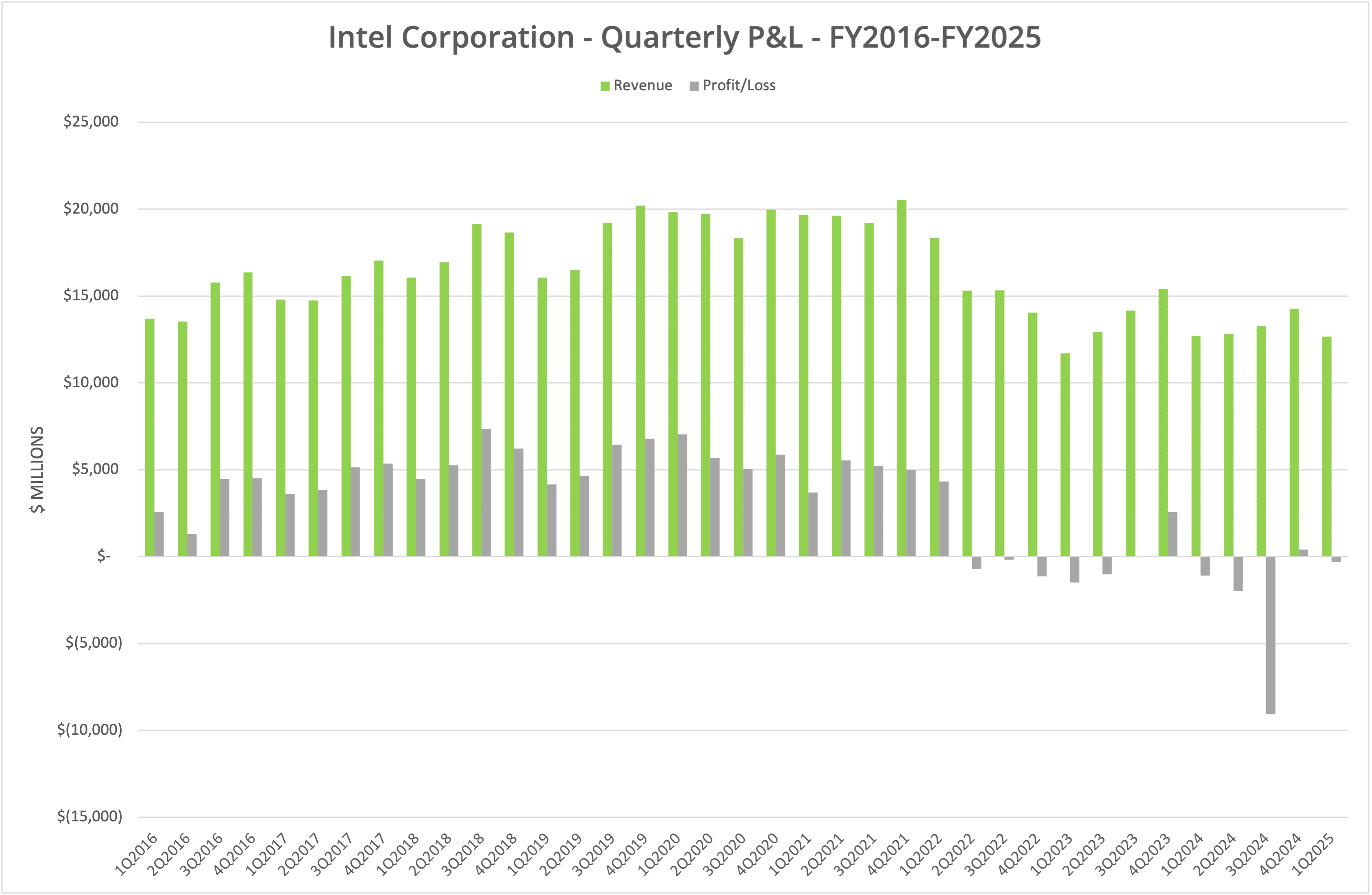

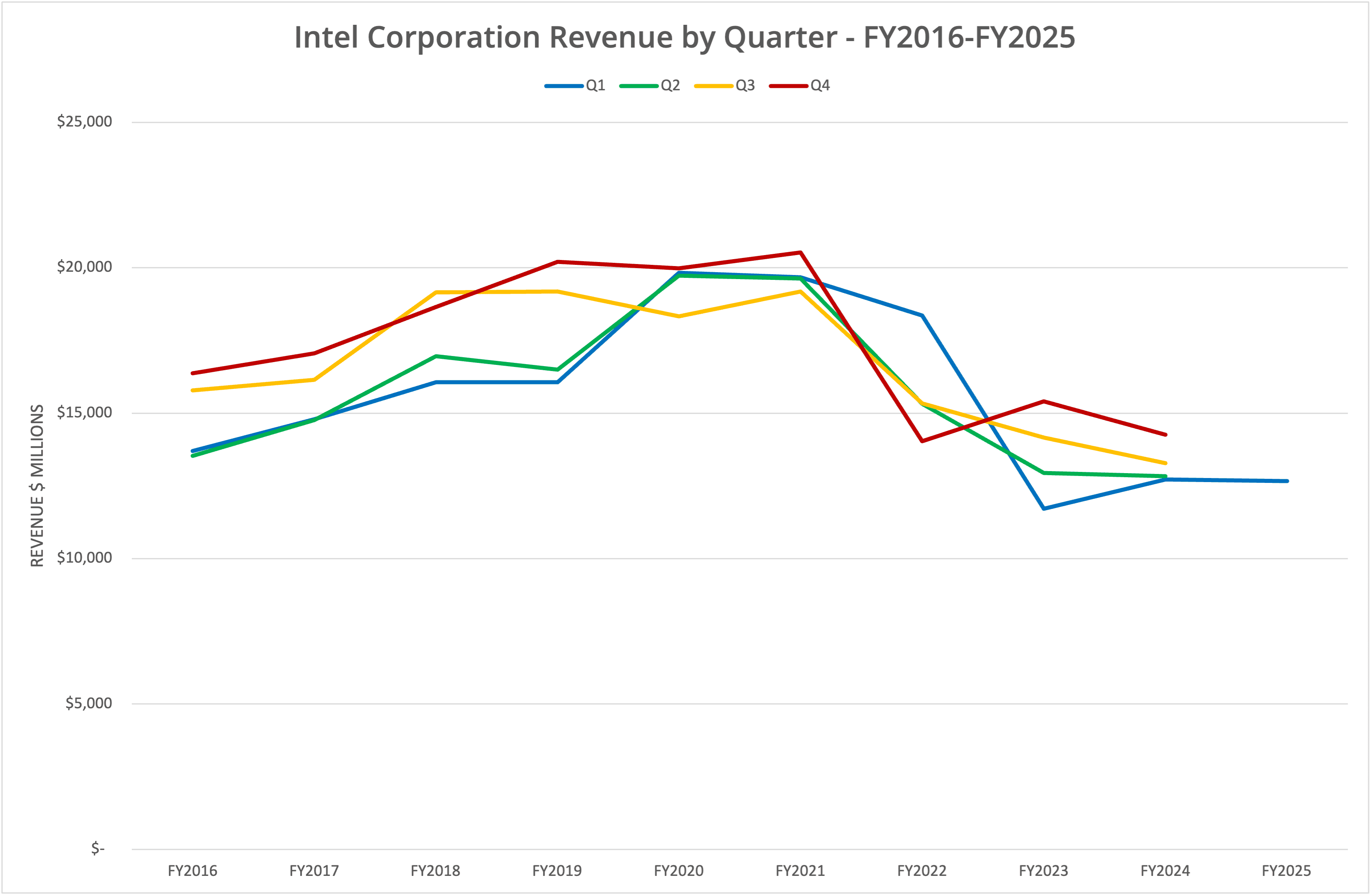

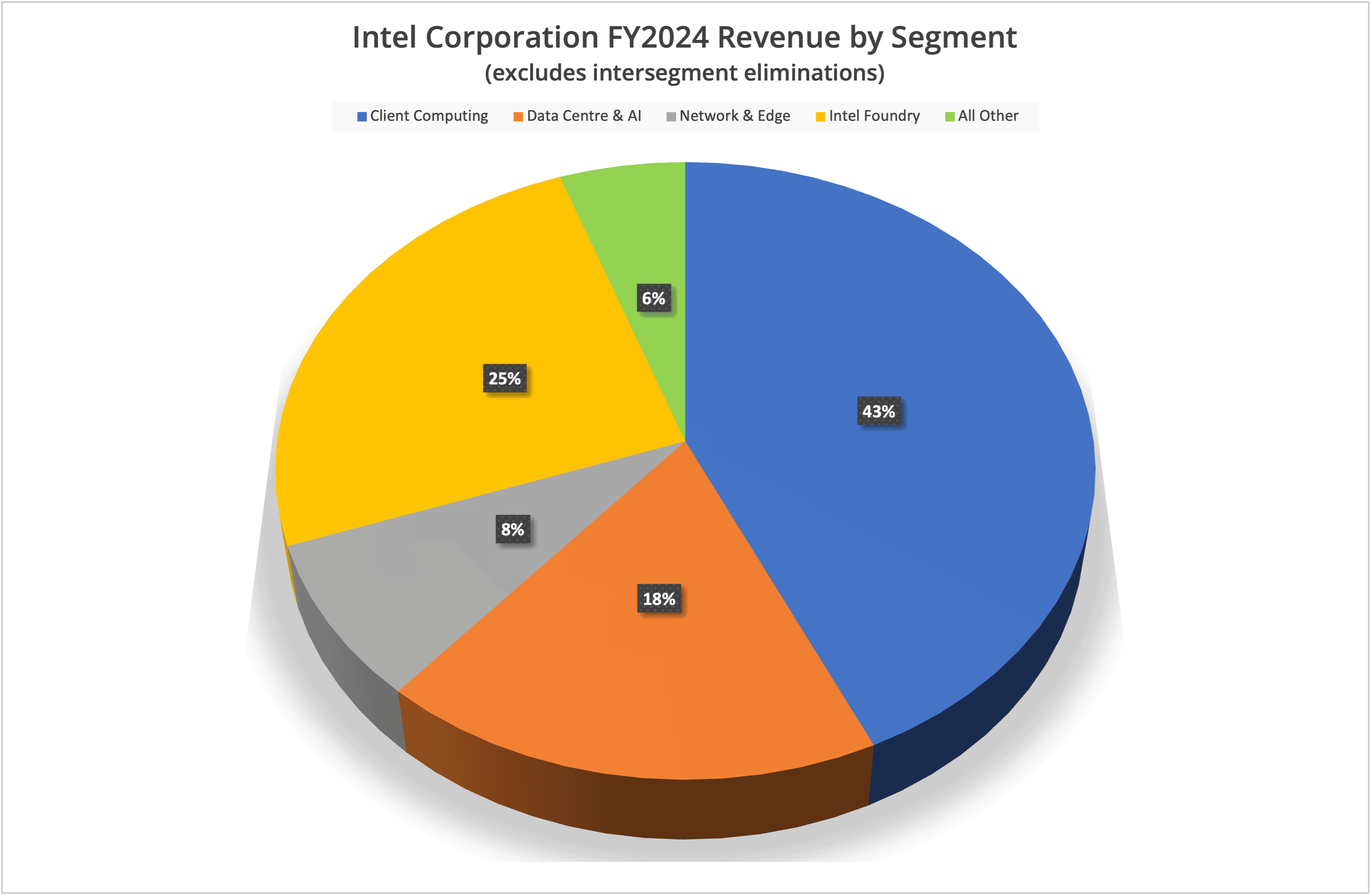

Intel Corporation declared financial results for Q1 FY2025 on 24 April 2025. Revenue was down 0.4% at $12.7 billion, with a $301 million loss. By division, Intel Products declined 1.5% to $11.8 billion, while Foundry improved revenue by 6.8% to $4.7 billion.

We note that the figures for Client Computing Group (CCG) and Data Centre & AI (DCAI) show an increased revenue of 1.3% and 35.9% respectively, but these are on the basis of previously quoted Q1 FY2024 data. Using the revised figures in the current earnings release, CCG declined by 7.8%, while DCAI improved by only 7.8%.

We present the data (using the original figures) in four graphs labelled Figures 1 to 4.

Holding Pattern

Intel’s results are disappointing but not unexpected. The company is in a transition period where the previous co-CEOs kept the ship afloat and operating while a new CEO was sought. As we now know, Lip-Bu Tan was appointed on 12 March 2025, so has had only a few weeks to enact the turnaround Intel needs. So far, this has entailed appointing a new senior leadership team and starting the process of operational rationalisation.

Under New Management

As expected, the initial changes implemented by Lip-Bu Tan are focused on operational efficiency. In his open letter to employees (and the Q1 FY2025 prepared remarks), Tan highlights excessive levels of management, wasted time in meetings and the lack of engagement driven by a maximum of three days onsite for staff.

Initial structural changes include flattening levels of management, which will undoubtedly result in unspecified redundancies from Q2 onwards. Rumours claim around 20,000 staff could be released, but this isn’t yet confirmed.

In addition to operational efficiencies, Intel is expected to reduce overheads with 2025 operational expenditure of $17 billion and a 2026 target of $16 billion. Capital investments for 2025 will reduce from $20 billion to $18 billion.

Product Focus

Of course, operational efficiency is only one side of the coin when it comes to making a profit and driving growth. Customers need to buy what Intel makes, and that seemed to be a problem in Q1 FY2025. As highlighted in the prepared remarks, AI PCs are not attracting customer attention at the level desired or expected by Intel, with more interest in older Raptor Lake products. Elsewhere, the data centre business saw an increase in Xeon sales, but that is predicted to be due to advanced sales ahead of US tariffs.

The tariff situation is causing uncertainty across the business in general, with Q2 forecasts weaker than the market expected.

The Architect’s View®

It’s worth stepping back a moment and remembering what a giant of the IT industry Intel continues to be. The x86 processor remains at the heart of both consumer and enterprise computing solutions, with Intel selling the vast majority of those components versus its competitors.

However, as Lip-Bu Tan himself proclaims, the company is “playing from behind” and needs to change to be a future leader. Like changing the path of a giant oil tanker, the results of existing reorganisations will not be realised overnight. Those changes represent only one part of the story.

As we’ve repeatedly highlighted, Intel products are not competitive in the market. The company faces the triple threat of AMD, Arm and RISC-V. Outside of the processor segment, NVIDIA is the market leader, followed by AMD. Intel barely registers as a rounding error in terms of GPU revenue.

So, we see several aspects that need to change.

- Improve internal efficiency to deliver new products to market faster.

- Reinvigorate belief in x86 as a data centre leader.

- Revise the AI PC strategy and focus on the TCO of desktop and laptop refreshes.

To achieve these goals, Intel needs to demonstrate reliability in the 18A process and beyond. The company also needs a solution that can compete with the efficiency of Arm processors in both the data centre and the desktop. This could conceivably mean evolving the x86 architecture into something new or taking a risk on an entirely new design.

We believe fixing a lethargic Intel isn’t enough for the company to regain a leadership position. Something new and radical also needs to appear from the product side. Taking that risk may be a step too far, but without it, Intel could be resigned to be another “also ran” legacy company slowly heading for irrelevancy.

Copyright (c) 2007-2025 – Post #2ac5 – Brookend Ltd, first published on https://www.architecting.it/blog, do not reproduce without permission.