Western Digital Corporation has announced financial results for the second quarter of FY2025, ending on 27 December 2024. Year-on-year, revenue is up 41.3% at $4.3 billion and up 4.6% sequentially. However, this improvement was driven almost entirely by a 119% increase in sales in the Cloud business. As the company has now split off the SanDisk SSD division, what does the future of WD as an HDD business look like?

Background

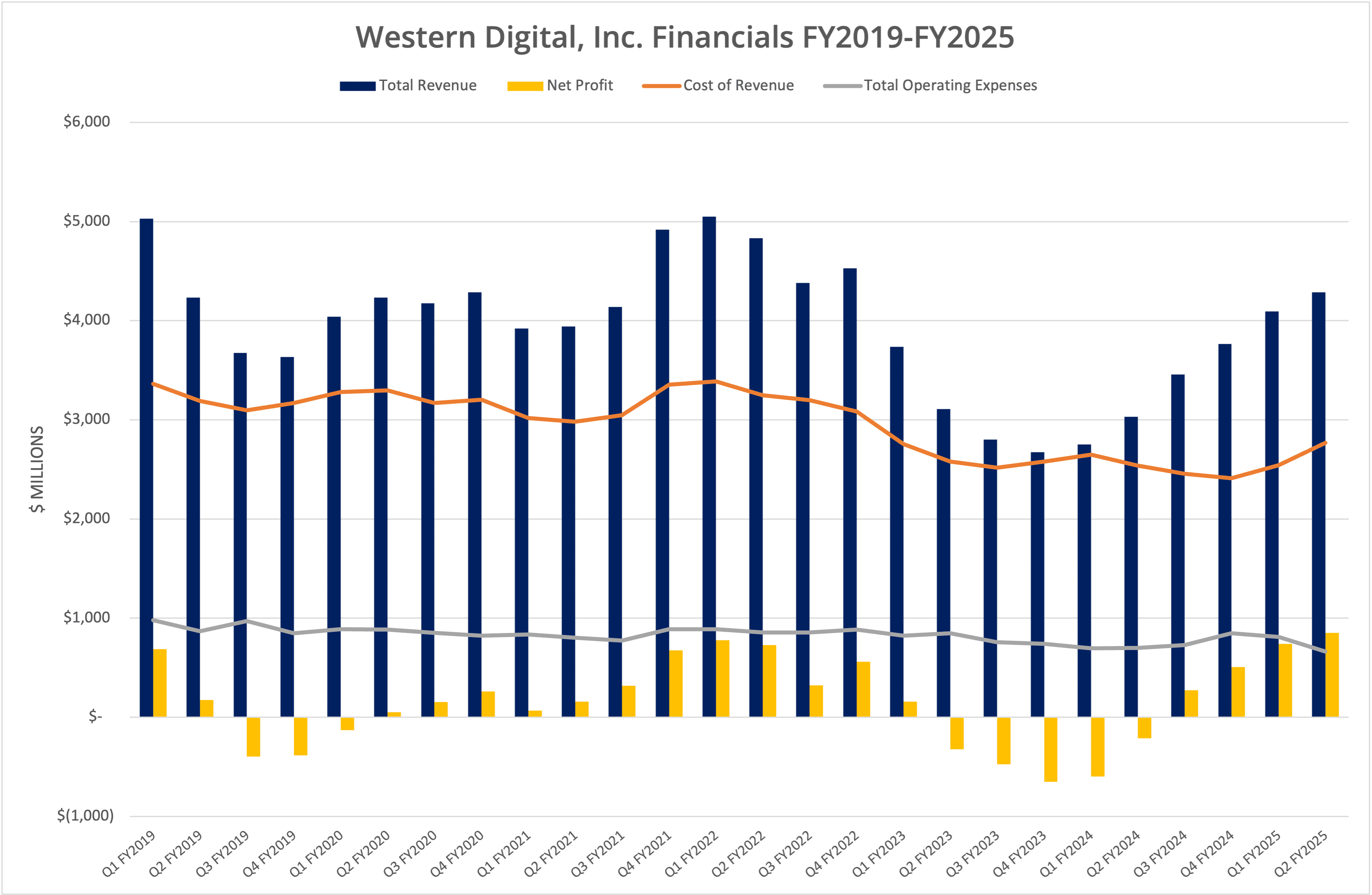

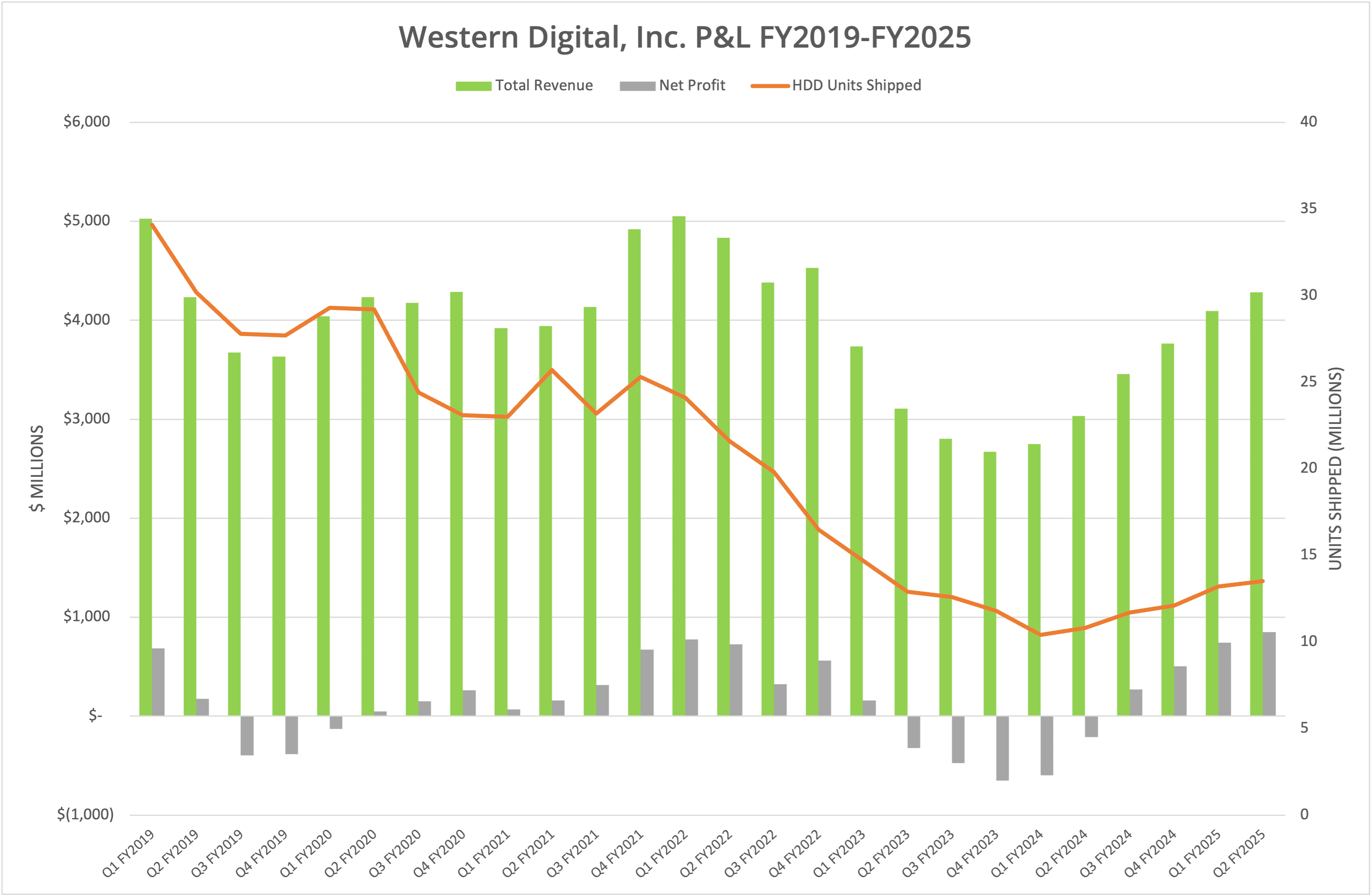

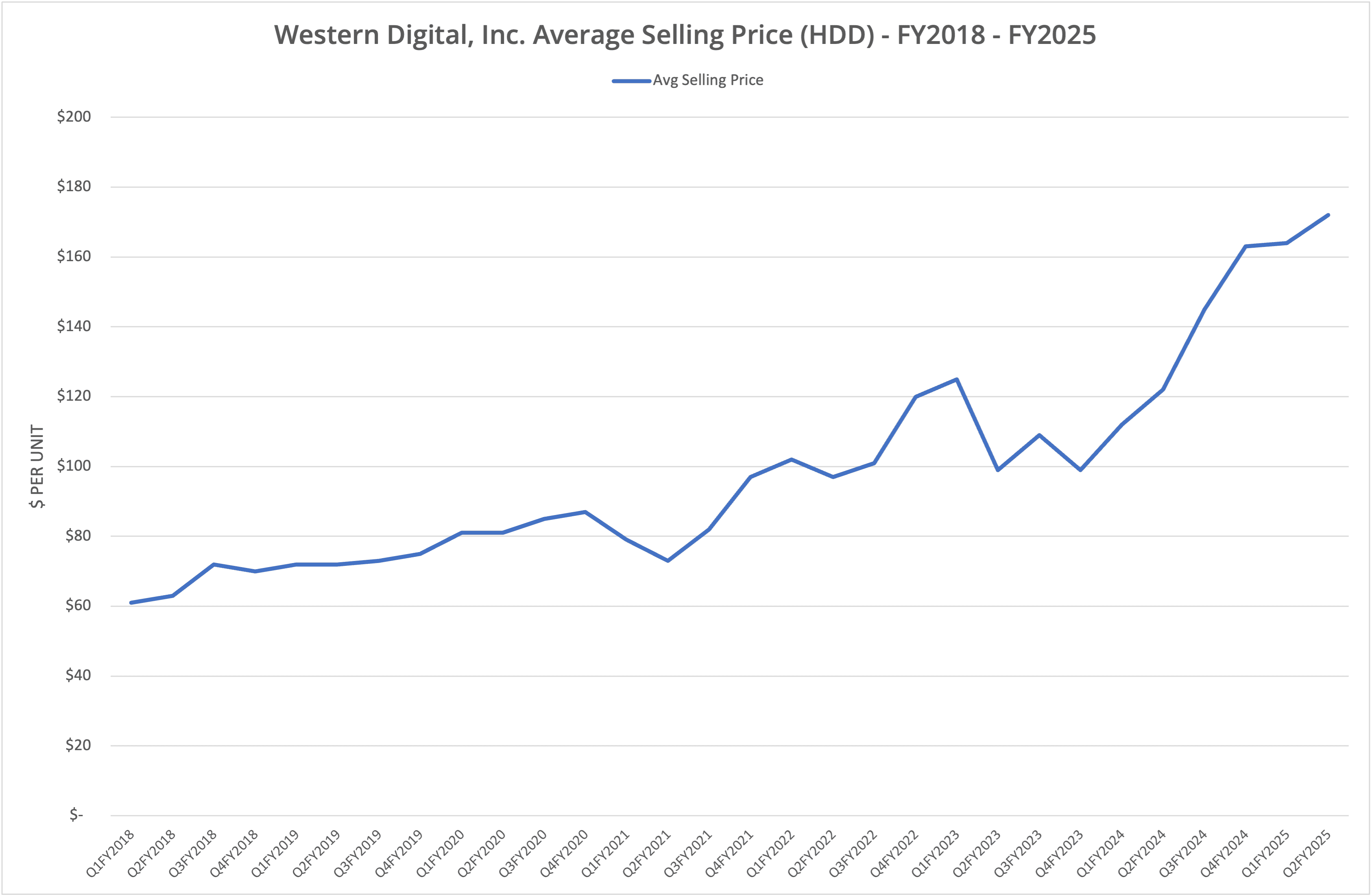

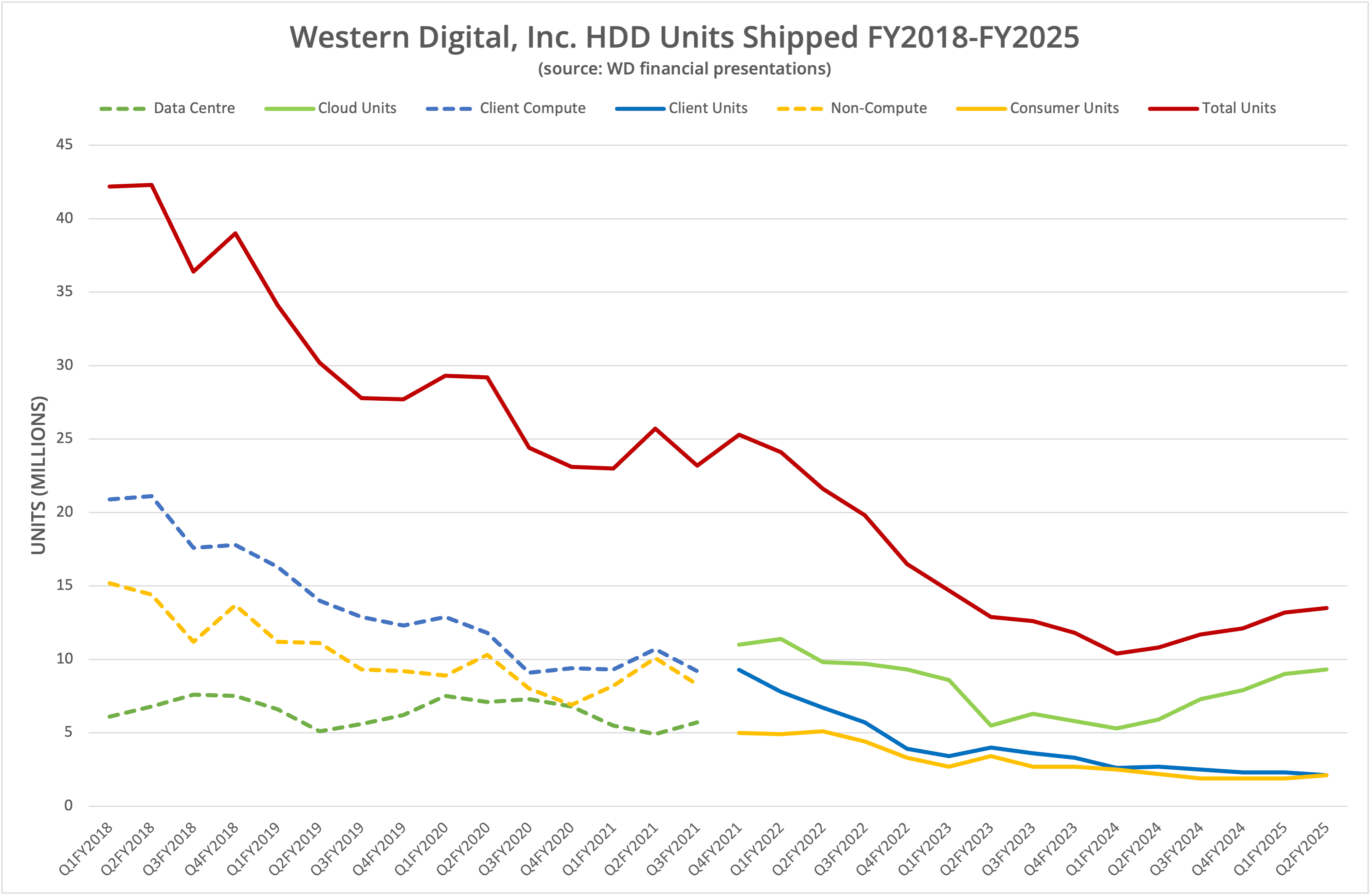

Western Digital Corporation has published financial data for Q2 FY2025. Revenue rose sequentially by 4.6% and year-on-year by 41.3% to $4.3 billion for the quarter. The company declared a quarterly profit of $852 million, shipping 13.5 million HDDs. We present the data in six graphs labelled Figure 1 to 6.

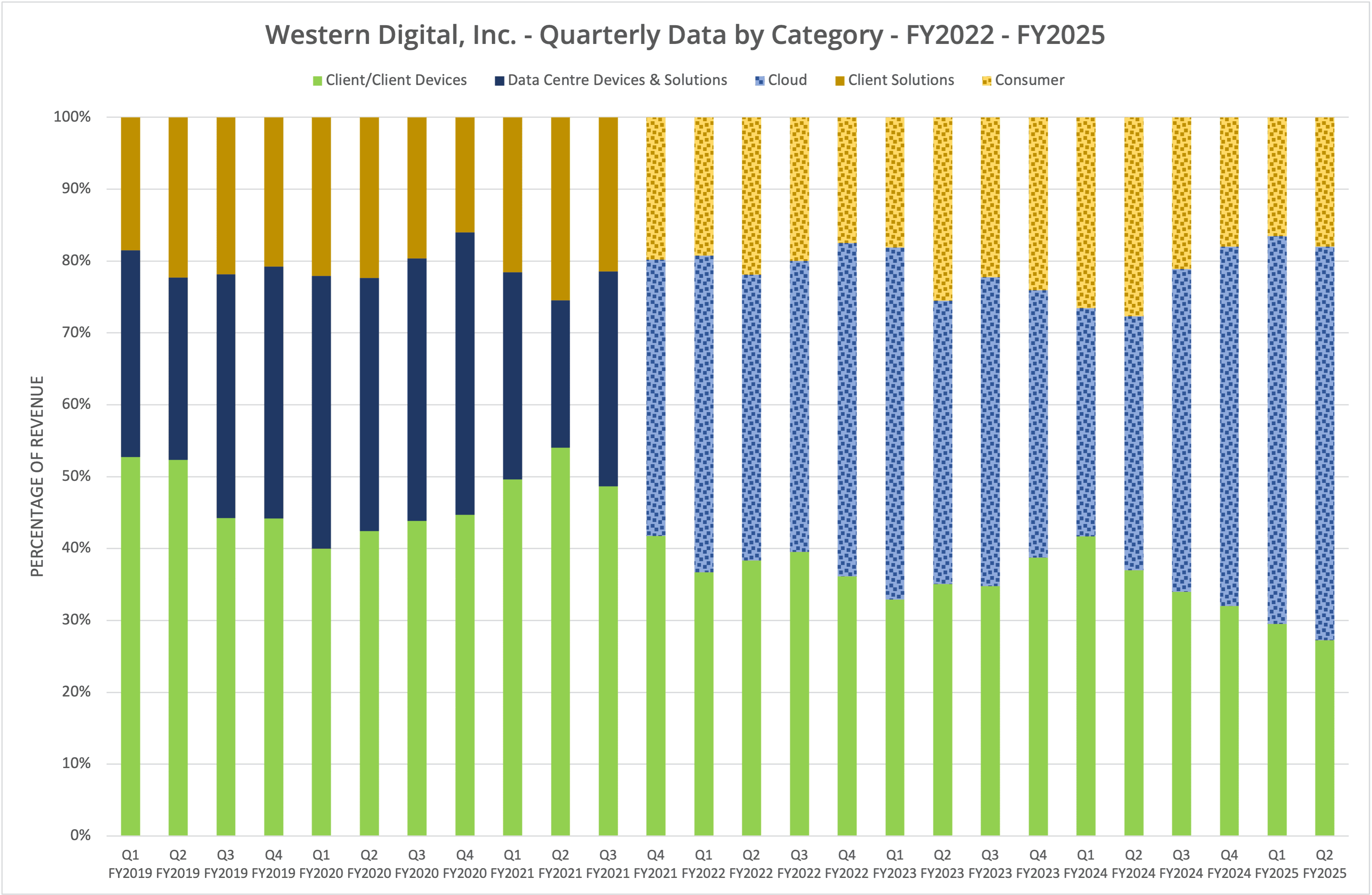

The turnaround in fortunes for Western Digital continues, with a sixth sequential quarter of revenue growth. Of course, the details are important and as we can see from Figure 3, the improvement is being gained from additional Cloud business sales. The Client business continues to decline, while Consumer is relatively flat. Bear in mind that this data includes both SSD and HDD sales, which could look significantly different now the split into two companies has completed.

The Split

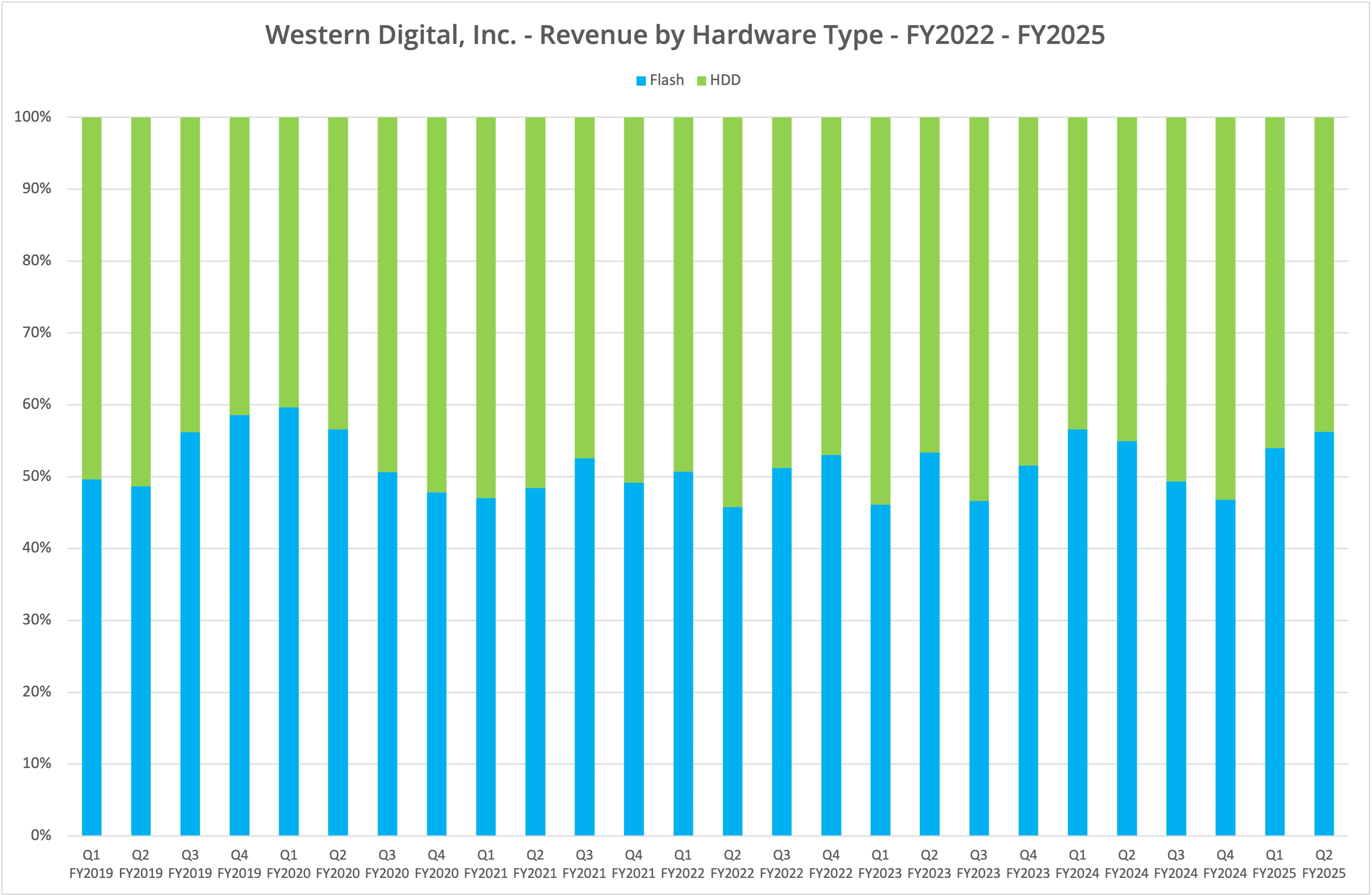

As we show in Figure 2, the HDD units shipped have started to level out, representing 13.5 million units in the current quarter, of which 69% are attributed to the Cloud business. Figure 4 shows the division of SSD and HDD sales, which currently sits at 55% in favour of flash storage.

On 24 February 2025, Western Digital announced the completion of the separation process to float SanDisk as a separate company. The data for Q3 FY2025 will include some SSD business revenue, while Q4 will represent the HDD business in its entirety.

Short & Long Term

The Q2 FY2025 presentation deck presents an insight into the long-term and short-term opportunities for both SSD and HDD markets. HDD gross margin in the current period was 38.6%, while SSD gross margin was lower at 32.5%. The Western Digital legacy HDD business certainly looks healthier in the short term, with several quarters of increasing exabytes shipped.

However, the data presented in Figure 6 shows a flattening of the curve in terms of Cloud units shipped, with a declining trend for Consumer and Client. Although there may be some capacity growth, the current media refresh cycle for the public cloud looks to be peaking, or at least levelling out.

The opportunities for the newly created SanDisk are less certain to ascertain from the data. However, we do know that flash is gaining a greater proportion of the cloud market over time, as high-capacity drives start to encroach on the space previously filled by HDDs. Meta, for example, has identified a gap in the storage hierarchy, which justifies additional spending on QLC storage. The future certainly looks better for SSD growth than HDD, as the cost per GB of storage continues to decline for both media.

The Architect’s View®

We will cover SanDisk financials in a separate set of posts, once they start to become published. In the meantime, we should focus on what the future holds for Western Digital as a standalone HDD business. The company is bullish about the future (as we would expect). But does reality match the enthusiasm?

Two technologies are on the horizon for future improvements in HDD capacity. These are HAMR, which is in production with Seagate and in evaluation by Western Digital customers. Drive capacities should reach up to 100TB with this technology.

Second is HDMR (heat dot magnetic recording), which will deliver 100TB+ drives, but not until the 2030s. This technology requires a new approach to platter substrates that creates a uniform alignment of recording bits on a disk’s surface. Further gains will (as typically occurs) be gained by combining HDMR and HAMR.

100TB and greater capacity drives will take another five years to appear. By that time the SSD market could have achieved 300TB+ drives or greater. The gap between SSD and HDD density looks only to increase. In parallel, HDDs don’t gain an improvement in performance with capacity compared to (read-biased) SSDs. This issue pushes the HDD more into the archive market.

We will cover the technical aspects of the battle between SSDs and HDDs elsewhere. However, in our opinion, while exabyte shipments may improve in the near term, we believe that the long-term future for HDDs is one of declining unit shipments, as SSDs incrementally replace more use cases.

While the industry can continue to put forward a case for HDD efficiency over SSD, the TCO justification for many workloads continues to be biased towards SSDs. Hard drives will not disappear overnight, but they will be a diminishing market for both Seagate and Western Digital.

Copyright (c) 2007-2025 – Post #663a – Brookend Limited, first published on https://www.architecting.it/blog, do not reproduce without permission.