Pure Storage, Inc. has announced financial results for the third quarter of financial year 2025. Revenue for the period is up 9.5% at $831 million (which we believe is a company record for a single quarter). Subscription revenue increased by 21.6%, while product revenue was flat. More importantly, Pure Storage has announced the previously previewed hyper-scaler deal is signed and will be accretive to revenue from FY2027.

Background

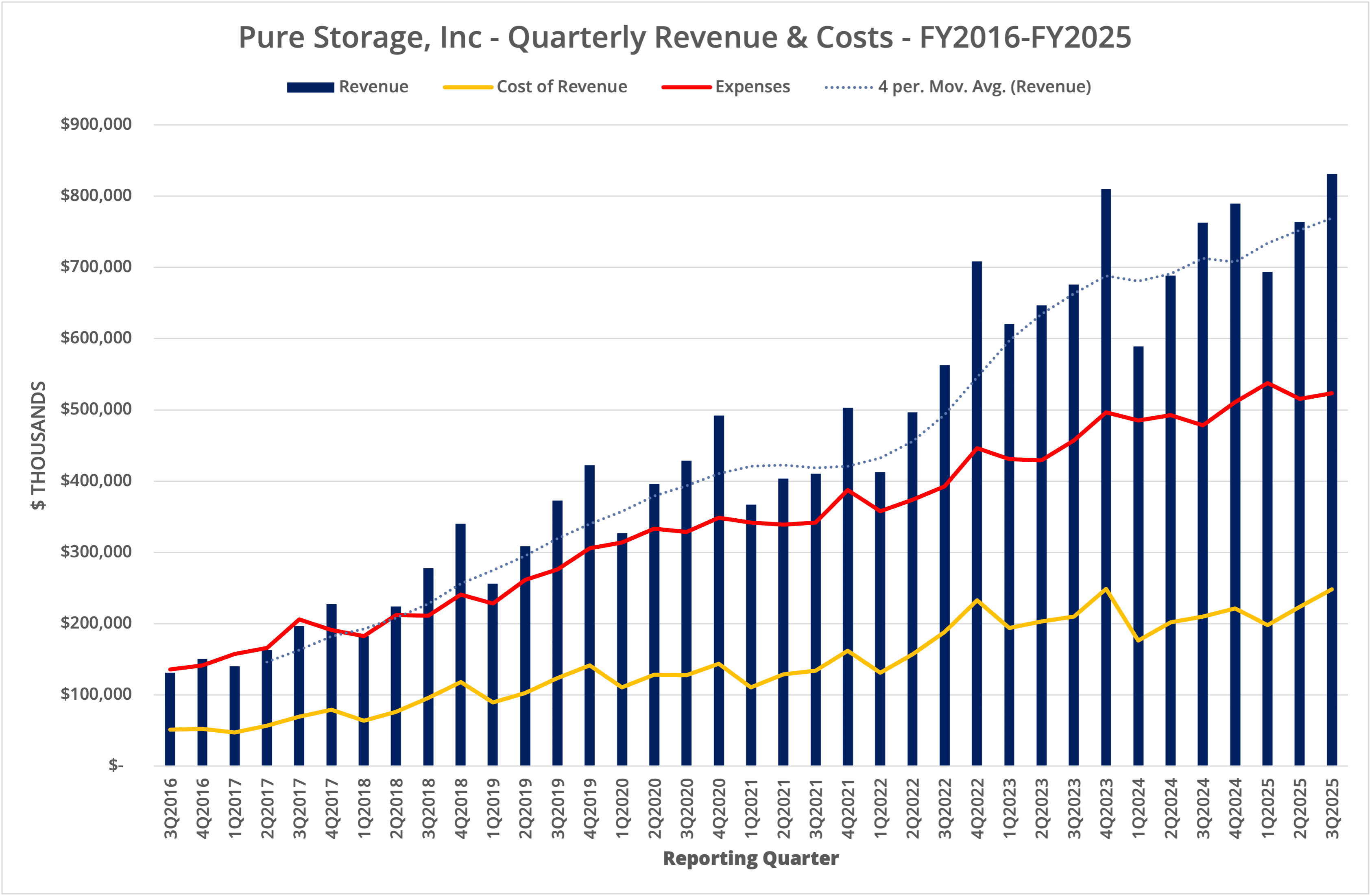

Pure Storage, Inc. announced financial results for Q3 FY2025, the period ending 3rd November 2024, on 3rd December 2024. Compared to Q3 FY2024, revenue increased by 8.9% to $831 million, with a pre-tax profit of $59,687. Within the revenue numbers, subscriptions increased by 21.6%. Subscription ARR was up 22% at $1.6 billion.

We present the data in six graphs, labelled Figures 1 to 6.

Growth

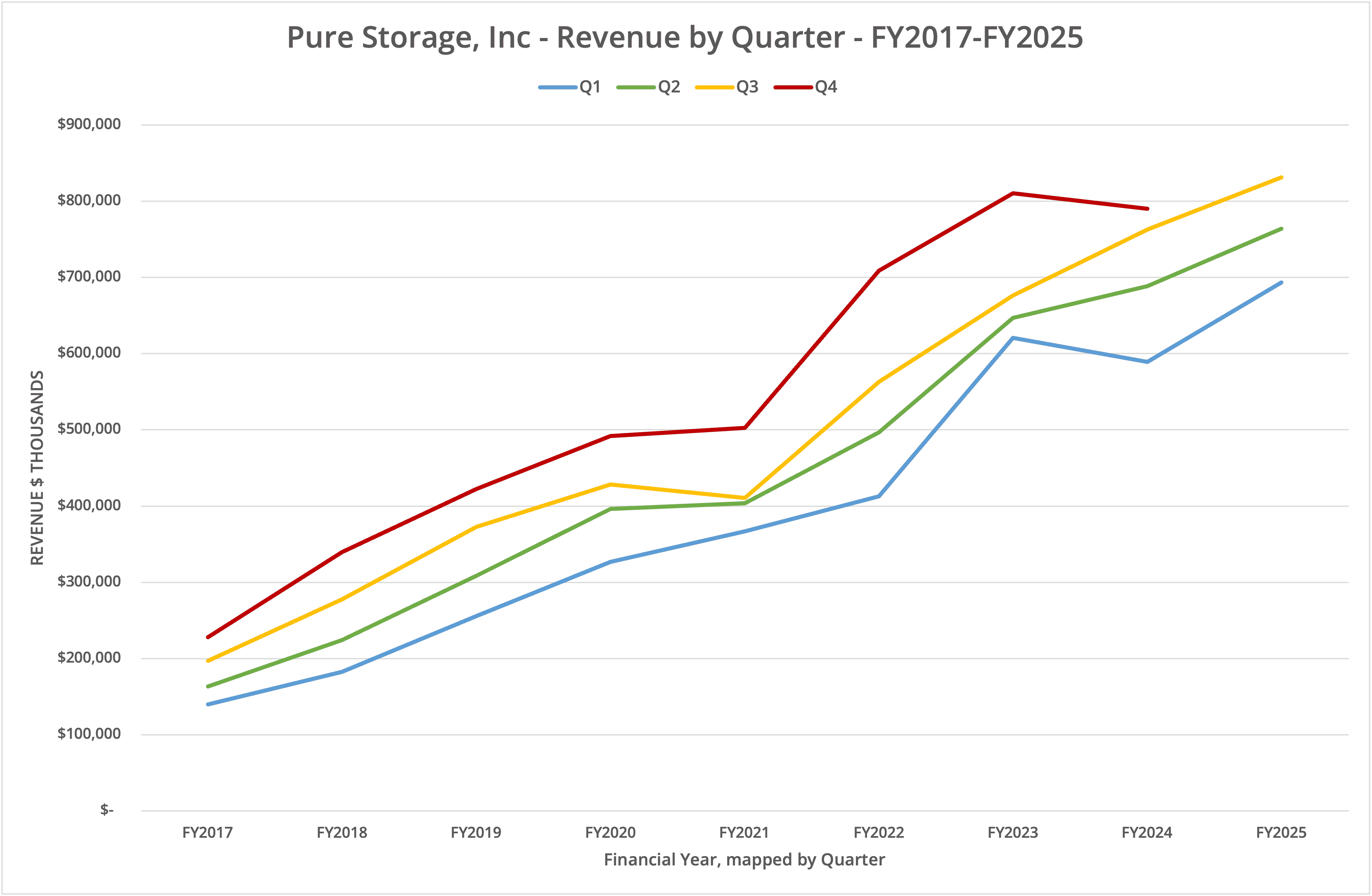

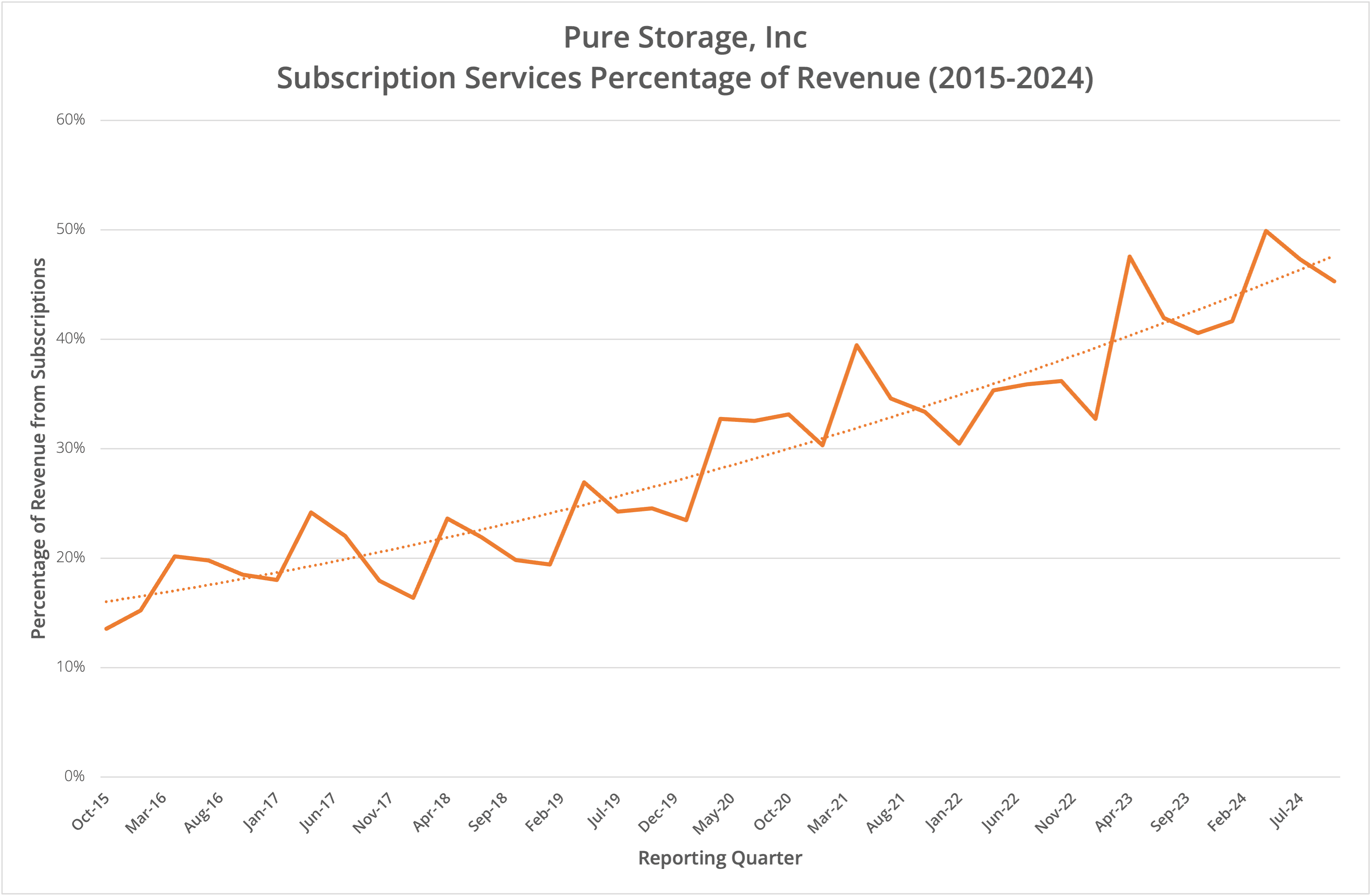

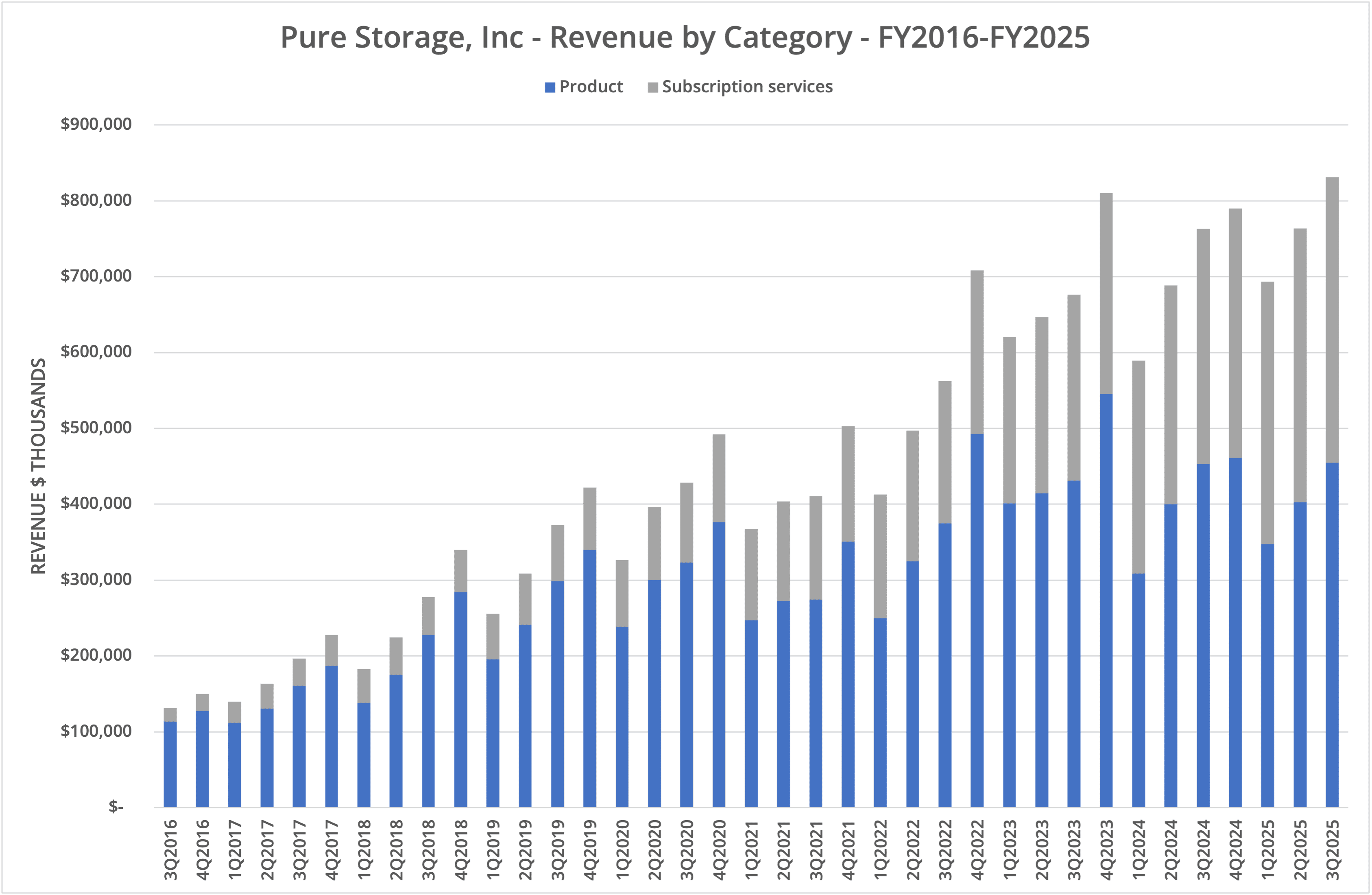

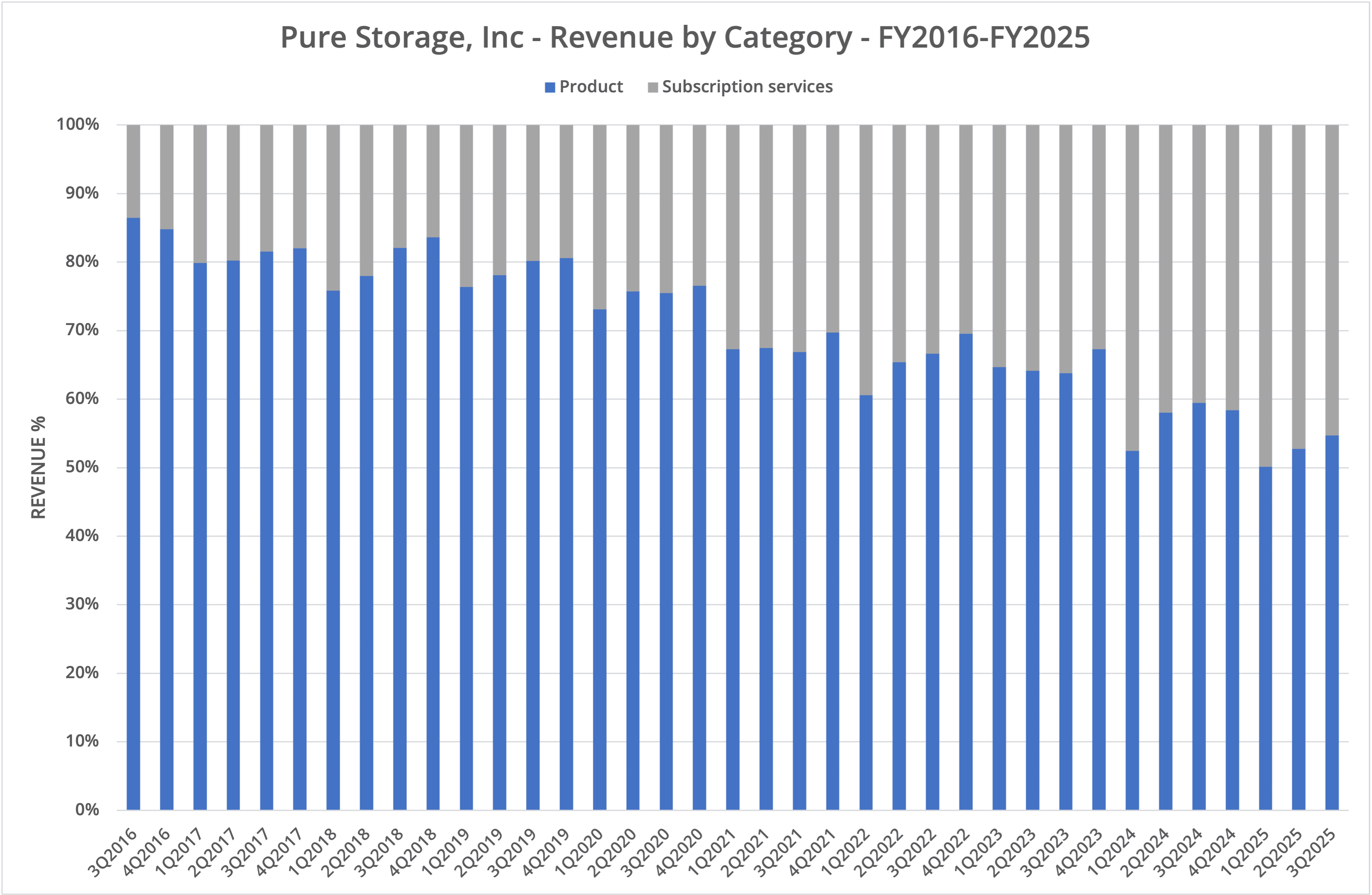

Pure Storage continues to deliver impressive growth in revenue that has been remarkably consistent since the first period we started tracking the company in FY2016 (see Figure 1). Within that period, subscription revenue has grown as a percentage of overall revenue from around 14% to almost 50% today (Figure 5). However, Pure Storage is still primarily a hardware company focused on the FlashArray and FlashBlade products. These two core platforms have been augmented with SaaS capabilities that have assisted in fuelling the growth in customers and revenue.

Cloud

The big question for businesses like Pure Storage is where the opportunities lie for future growth. With competitive products, the company could continue to take market share from competitors, but the on-premises market in total is not where IT is experiencing growth. A significant part of new IT spending is directly on the public cloud, as witnessed in the development of AWS, Microsoft Azure, Google Cloud, Oracle Cloud and a host of other smaller second-tier providers.

Cloud vendors have developed their own storage offerings while engaging with some vendors to create more integrated solutions. The leader in this market is currently NetApp, with cloud-native integration of ONTAP into the top three public cloud vendors. While companies like Pure Storage have cloud solutions, no other vendors currently offer fully integrated cloud-native capabilities. (Note that Pure Storage has announced Pure Storage Cloud for Microsoft Azure VMware Solutions, while AWS provides FSx implementations of Lustre and Microsoft Windows).

Hyper-scaler

With relatively little penetration of the hyper-scale market by traditional infrastructure vendors, the pre-announced partnership with a hyper-scale customer by Pure Storage has naturally generated significant interest. With massive potential for growth, getting a conventional infrastructure product adopted in the public cloud could be a huge win for Pure Storage, depending on the scope of the arrangement.

In the latest earnings call, CEO Charlie Giancarlo indicated that Pure Storage had signed an agreement with a “Top 4 hyperscaler”, which would see the partnership move into field testing in 2025 and produce revenue by 2026, or Pure’s financial year 2027.

As usual, the devil is in the details, which, as yet, aren’t 100% clear.

Top 4

Firstly, the earnings release prepared remarks continue to reference the term “top 4 hyperscaler”, but what does this mean? There are no strict criteria for which companies are included in this definition. Chris Mellor at Blocks & Files, for example, assumes the list includes AWS, Azure, Google and Meta. This cohort is taken from another article in Data Centre Magazine. Hyper-scale just implies a large user of IT resources, which today could include Elon Musk’s xAI or Apple (the former building out GPU infrastructure, the latter building on its services business).

So, we’re not clear whether “top 4 hyperscaler” refers to a company offering public cloud resources to its customers (AWS, Azure, GCP), using infrastructure to deliver services (Apple, Meta) or simply building massive LLMs (xAI). We don’t know if the company in question is even one of those we’ve listed – or another we haven’t.

Infrastructure

What we can be clear on are the reasons for choosing Pure Storage products to be deployed in the hyper-scale data centre. The Q3 FY2025 prepared remarks highlight some of the benefits that will be achieved using FlashArray and/or FlashBlade:

- Data centre power/space/cooling savings.

- Elimination of legacy infrastructure based on HDDs.

- Improved availability/resiliency, with reduced failures.

- Reduced maintenance costs.

- Simplified performance offerings based on “logical tiering”.

In hyper-scale environments, these metrics have a huge impact, compared to smaller infrastructure deployments. This is especially true if the hyper-scale customer is continuing to expand its business. Moving to an all-flash solution, for example, might also result in significant cost-avoid savings from not building new data centre infrastructure, or extending the life of existing equipment.

Hardware

Again, from information in the Q3 FY2025 prepared remarks, we learn that the hyper-scale customer will license Pure Storage technology and consume support services. The arrangement is not a deal to sell hardware but does include Purity (the O/S running FlashBlade and FlashArray hardware) plus DirectFlash.

DirectFlash is the technology that delivers DirectFlash Modules (DFMs), the custom SSDs inside all Pure Storage products. It manages the NAND flash and abstracts the Flash Translation Layer across all devices within a system rather than within a single SSD. Again, it is not clear whether Pure Storage is selling DirectFlash modules or simply licensing the IP behind the DirectFlash technology.

Licensing

In many respects, selling software or licensing IP looks like a better deal than selling hardware products (whether on subscription or not). The margin for Pure Storage is much greater, without the additional overheads of managing inventory, variable NAND pricing, hardware recycling and so on. This approach is one taken by many other vendors in recent years, most notably VAST Data.

Let’s assume that there is no hardware of any type included in the hyper-scaler deal. This implies that the hyper-scale company is sourcing its own hardware, including NAND chips. Building server infrastructure is no problem for those companies, but what about building DirectFlash Modules? This is where things get interesting.

Today, Pure Storage sells DFMs up to 75TB in capacity, with 150TB announced and 300TB drives expected within the next two years. Picking the most appropriate capacity for DFMs is a balancing act of many factors. Bigger drives offer the ability to reduce costs and be more efficient. However, if a minimum footprint of seven drives is required, a 300TB system is 2.1PB as an entry point. This isn’t practical for a significant portion of customers, which is why smaller 18, 37 and 75TB drives still exist.

In the hyper-scale market, large capacity drives aren’t an issue. Hyper-scalers, by definition, benefit from economies of scale. These solution vendors will be looking for drives or infrastructure of 300TB and greater, in order to maximise the efficiency of flash and replace traditional spinning media (HDDs) on a TCO basis. This technology just isn’t available from traditional SSD vendors.

If we look at the technology deployed by hyper-scale vendors in recent years, we can see custom processors, custom server hardware, custom network chips, custom accelerators, but (as far as we are aware), no custom storage media. We believe that the deal with Pure Storage could change that dynamic, introducing another wave of custom hardware built explicitly for hyper-scale environments.

The Architect’s View®

Gaining a foothold in the hyper-scale market is a win-win for Pure Storage. The company continues to sell to traditional infrastructure customers while licensing the IP at a greater margin to the hyper-scalers. In parallel, knowledge gained from managing large-scale customers can be fed back into improved on-premises products. This move opens up another market for the company, one that only NetApp has managed to embrace so far (currently bringing in about $160 million per quarter).

Are there any downsides to this deal? Hyper-scalers could develop bespoke versions of Purity and DirectFlash technology, but that’s a long-term game that has taken Pure Storage fifteen years of development to reach. For now, it seems like Pure Storage has managed to achieve what many legacy storage vendors can only dream of.

Related Posts

- Pure Storage Microsite

- X-Ray: Pure Storage, Inc. (Second Edition)

- Analysis: Pure Storage announces Q2 FY2025 financial results

Copyright (c) 2007-2024 – Post #c5p8 – Brookend Ltd, first published on https://www.architecting.it/blog, do not reproduce without permission. Pure Storage is a Tracked Vendor by Architecting IT in storage systems and software-defined storage.