HPE has announced Q3 results for FY2022. Revenue is up barely 1% year-on-year (although HPE claims 4% with currency adjustments), while server and storage revenue looks flat. With so much focus on transforming the business to an “as a service” model, is all the effort making any difference to the bottom line?

Background

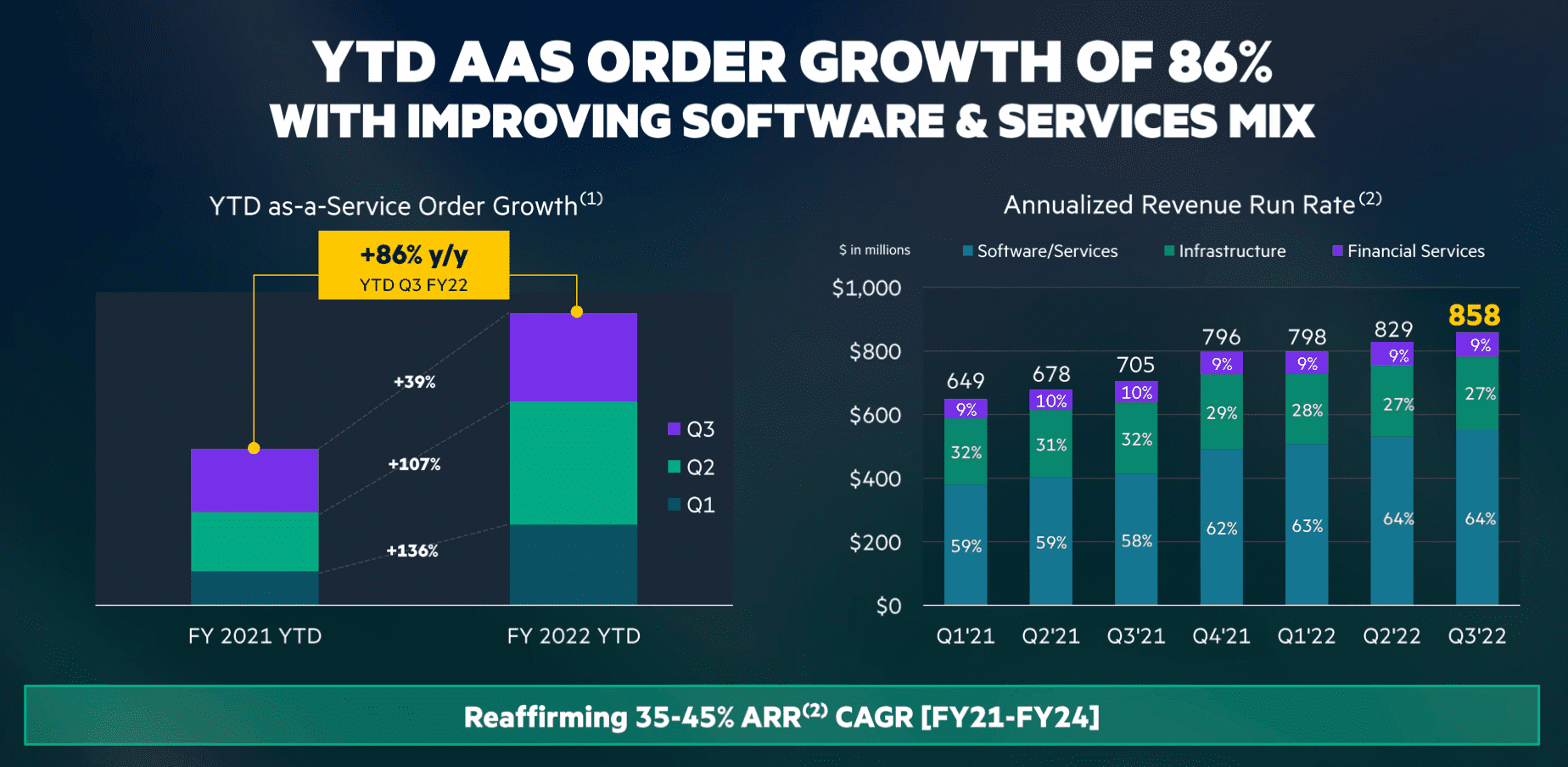

Back in June of this year, we took the opportunity to review HPE’s financials with respect to the announcements made at HPE Discover 2022. The company is on a multi-year journey, reinventing the purchasing “experience” to one that’s based on an “as a service” (AAS) model – AKA GreenLake. As shown in figure 1, AAR is at a compound annual growth of 35-45% and up 86% year on year, with the comparable three quarters of 2021.

However, despite the improvements in ARR, the core Storage and Server business units have seen little to no growth, compared to the Intelligent Edge (networking) and HPC & AI business divisions. As a further indication, the “AAS Enablers”, namely HPE Financial Services and Corporate Investments are also flat.

Margin

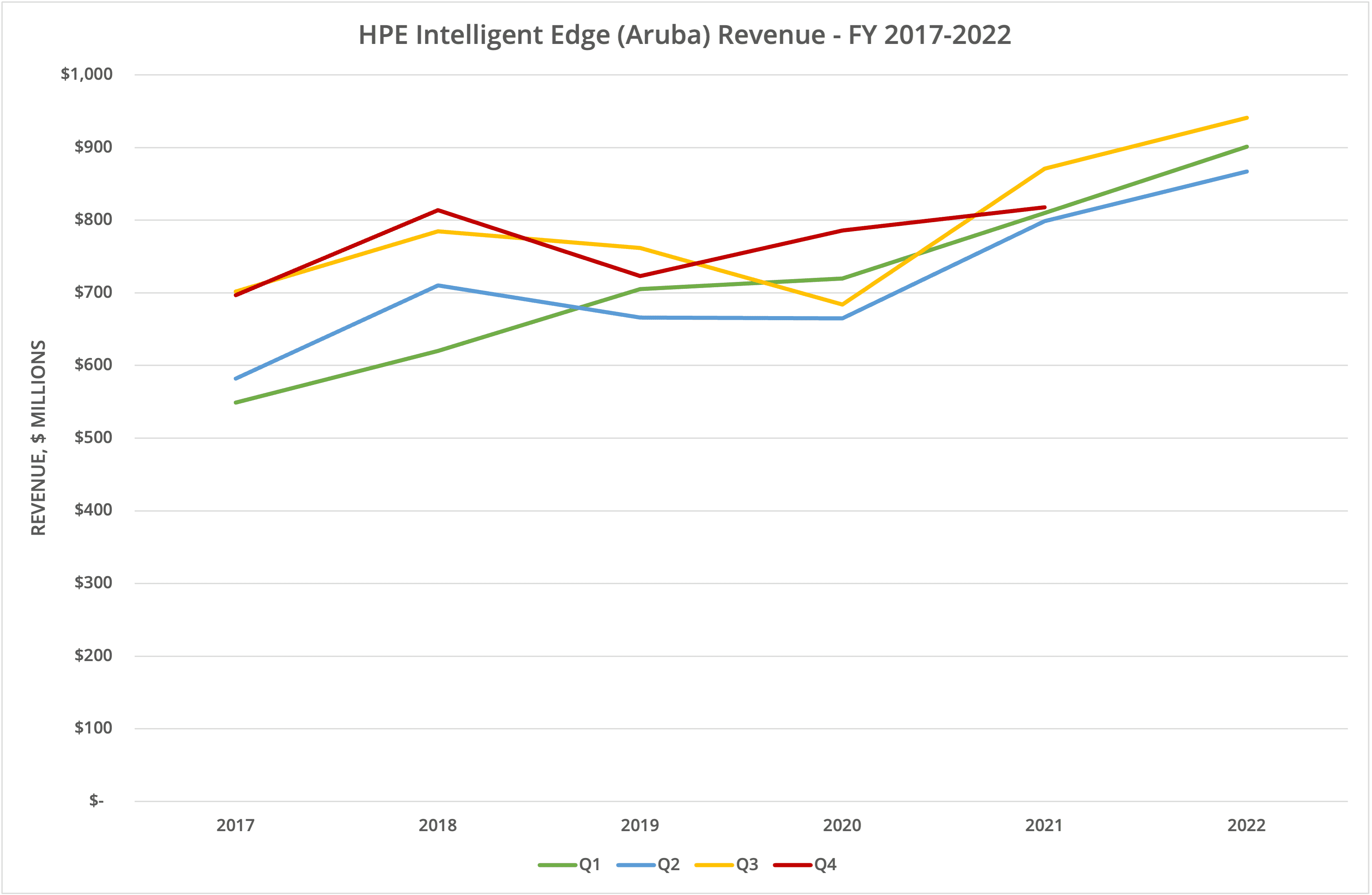

It’s worth noting that Servers & Storage still make up 60% of HPE’s revenue and 70% of operating profit (based on the data in this quarter’s statement, available here). In the reported quarter, Corporate Investments lost money, while Intelligent Edge delivered above average profit (16.5% of revenue) and HPC & AI significantly below the average (3.4%). What this means is HPE’s core businesses are still essential revenue streams that won’t be quickly superseded by the growth engines. Intelligent Edge is definitely the start performer here. The “by quarter” data for that BU is shown in Figure 2.

Service Model

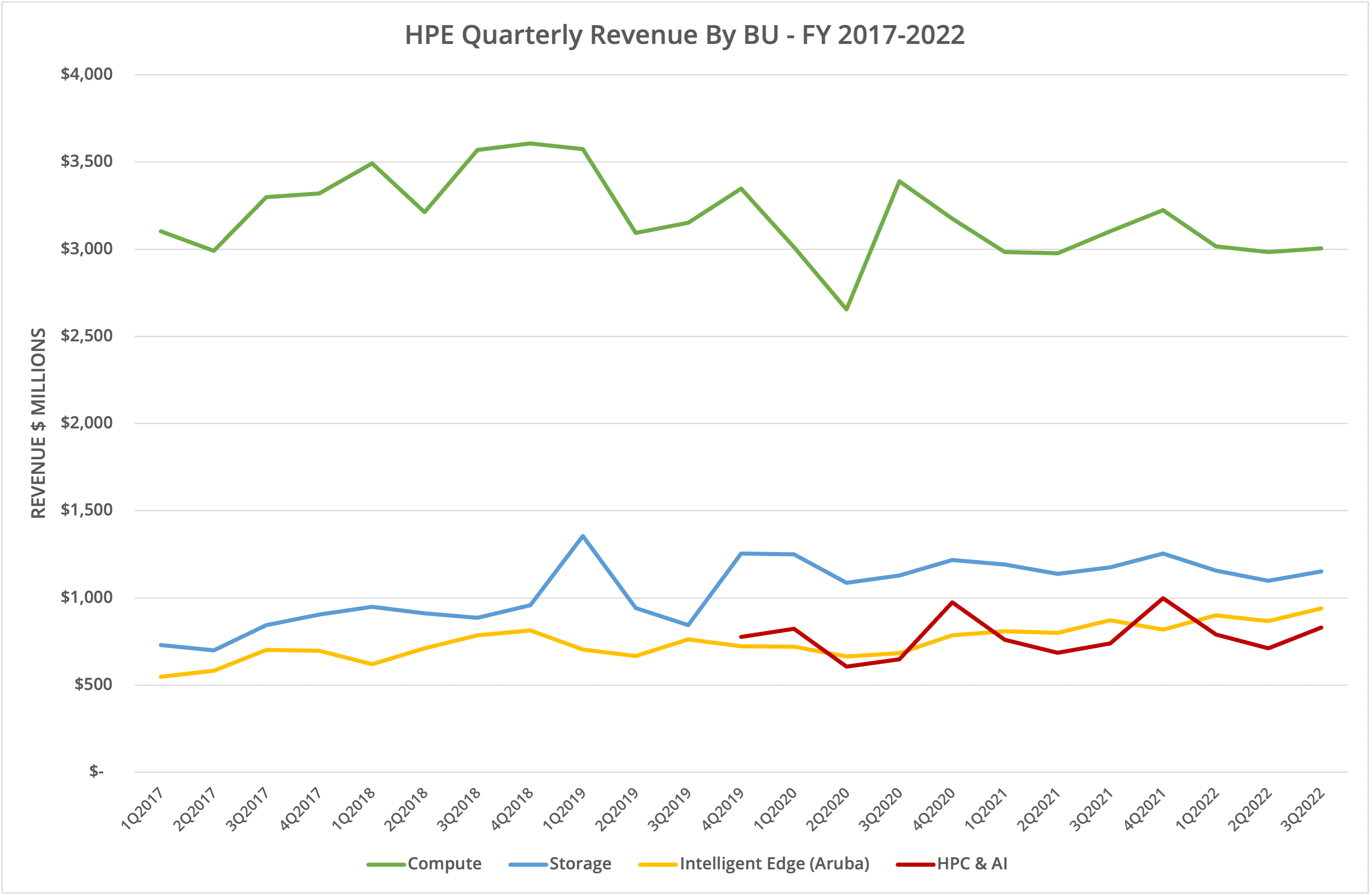

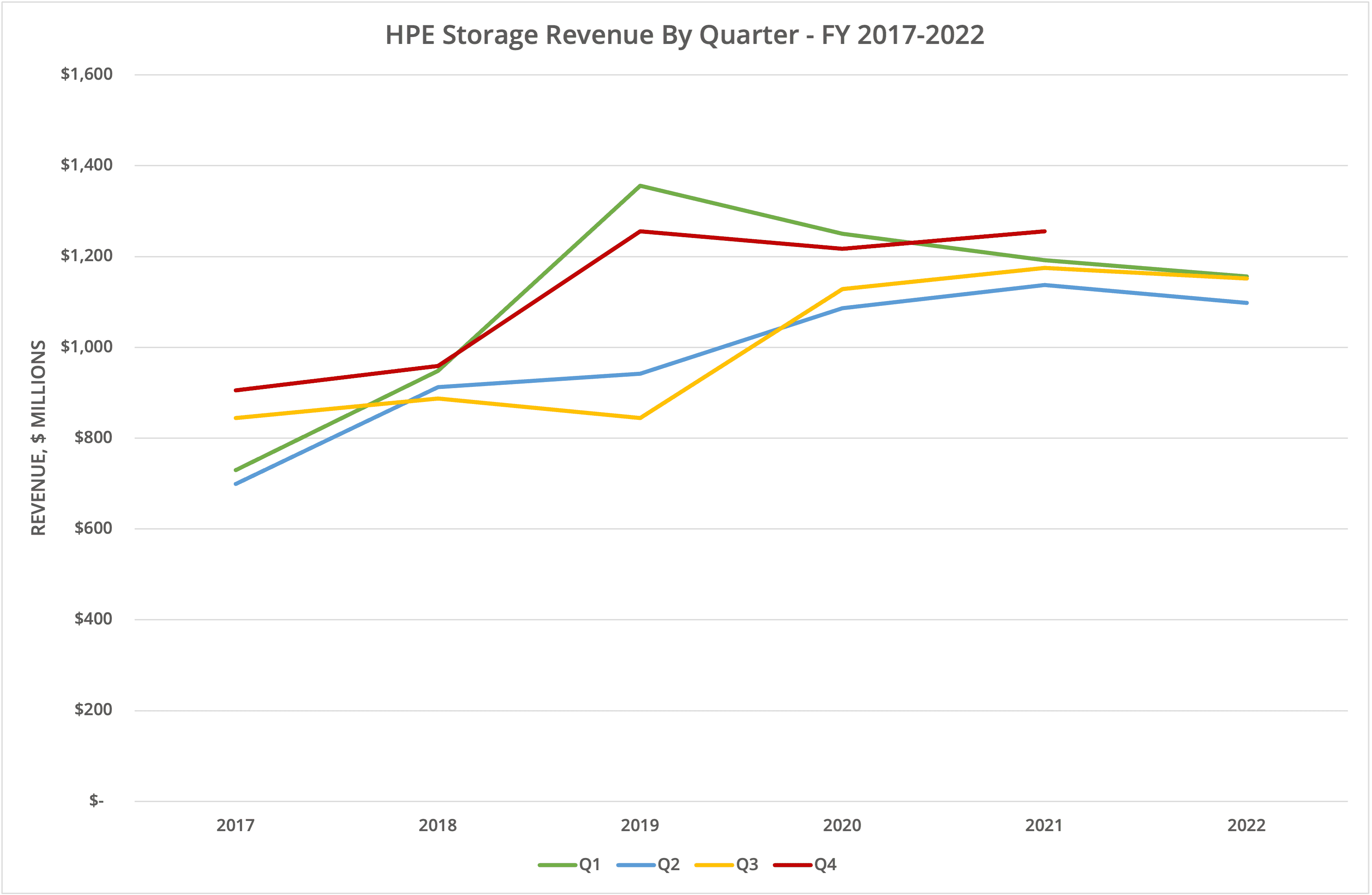

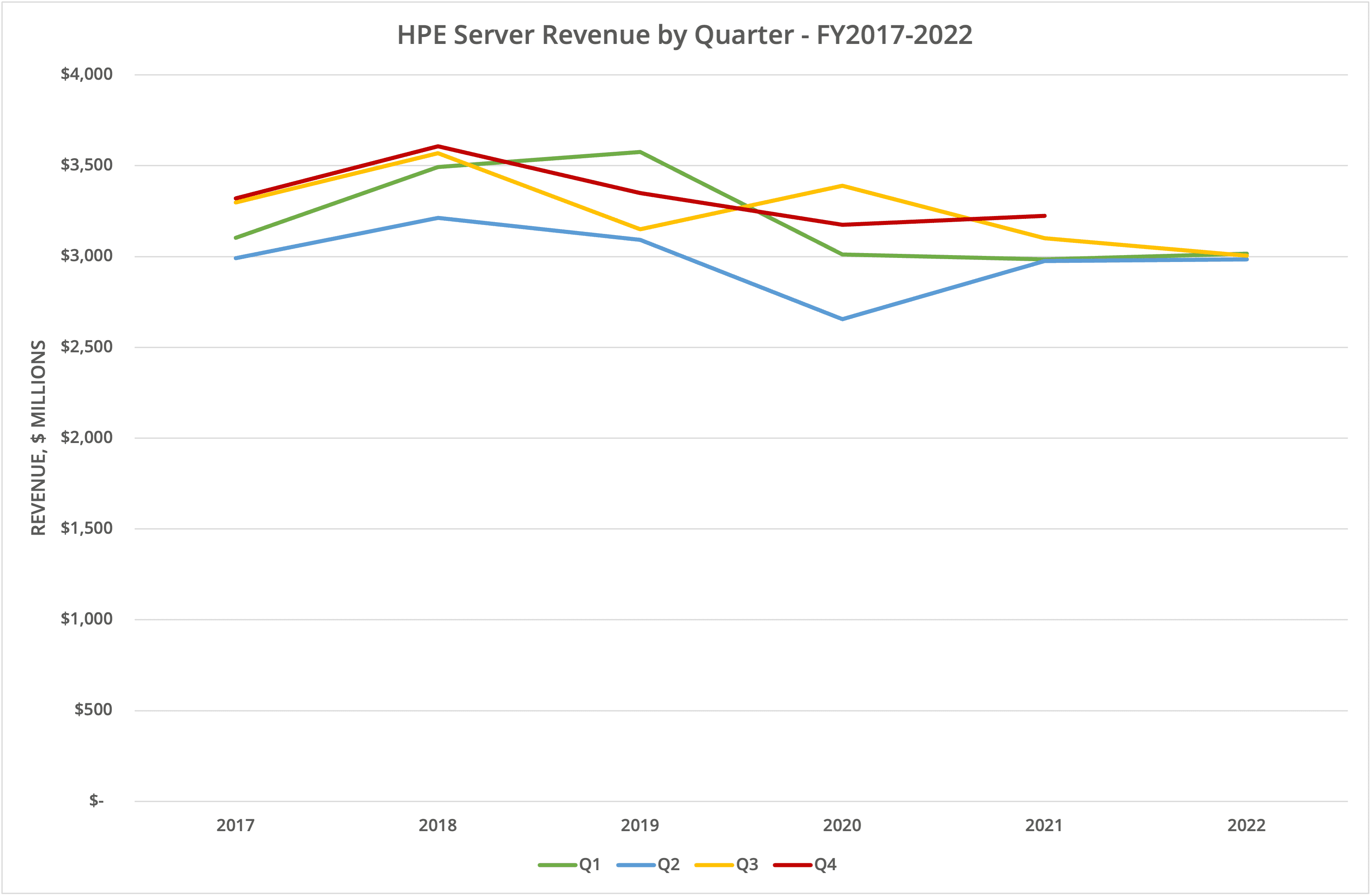

When we look at the data for the Storage BU with respect to ARR and a service model, HPE claims 44% ARR growth year-on-year and double-digit growth for Nimble and HCI product lines. However, revenue year-on-year is flat and operating profit is also down due to higher supply chain costs. A similar story also plays out for the Server BU. Figure 3 show more of the detail.

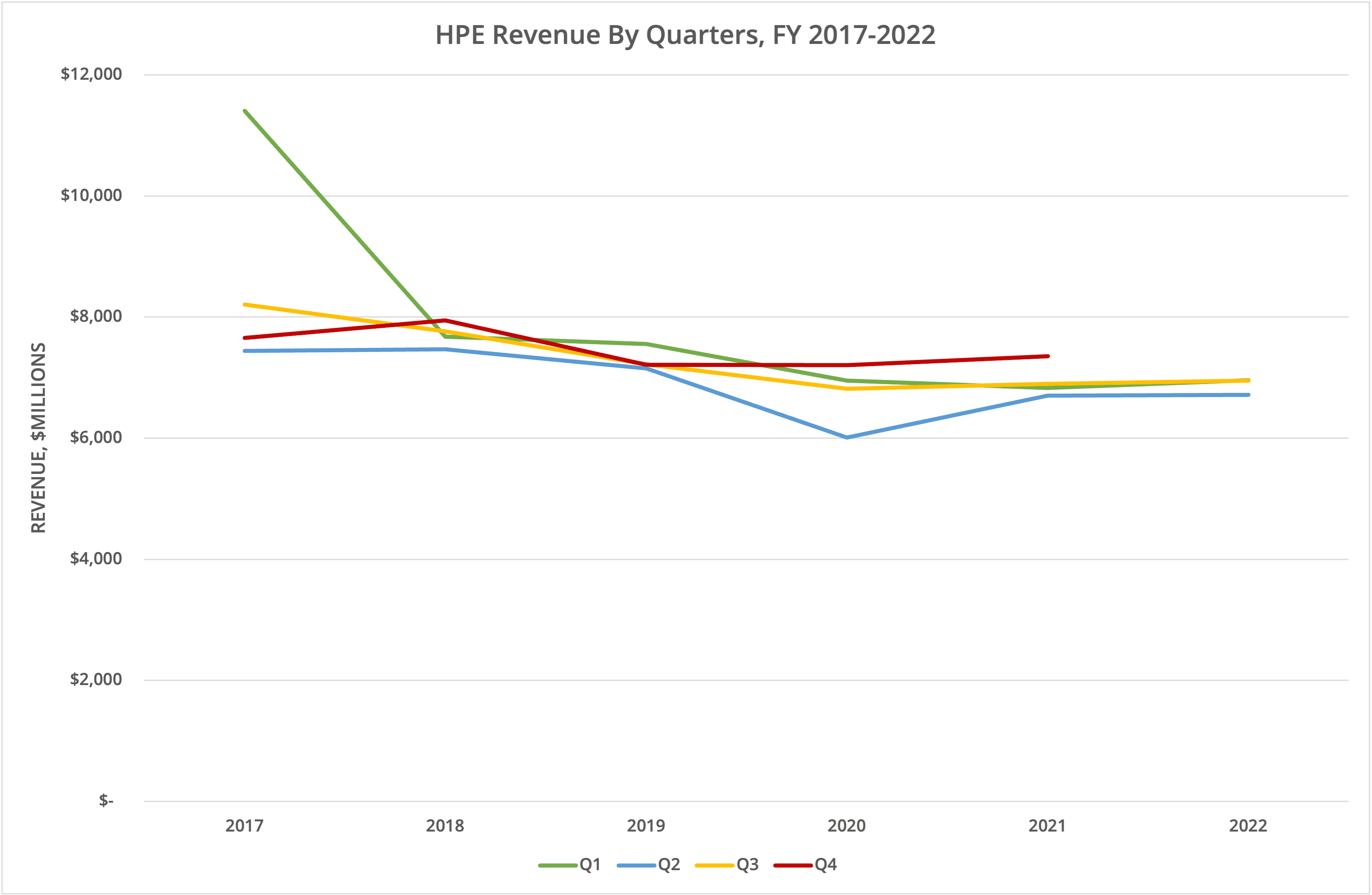

Here’s where things get a little confusing. The service-based model is meant to smooth out the peaks and troughs of quarterly purchases and looking at the data in figures 4 to 6 that could be argued to be true. Server revenues are trending to the $3 billion/quarter mark, with storage around $1.1 billion. The question is, are these figures significantly constrained by supply chain challenges and by how much?

If the figures are constrained, then selling through a service model seems to offer HPE no additional benefit in terms of increased revenue. This seems odd because customers shouldn’t be on a 3-4 replacement/refresh cycle, but be buying on abstracted metrics like performance and capacity. If the figures are not constrained, then again there’s a problem as this model hasn’t increased revenue.

Public Cloud

HPE has no obvious public cloud storage story. The closest the company offers is Cloud Volumes, which puts HPE storage into a co-located data centre connected to a public cloud provider. Unfortunately the videos on the HPE website that would provide more detail (here) appear to have all been deleted or moved. If supply is constrained, there are no offerings for customers to use public cloud-based resources, either permanently or on a temporary basis. As a result, HPE’s revenue from services based around storage will continue to be based on supplying hardware and constrained by any supply chain issues.

The Architect’s View®

From a vendor perspective, what is the point of converting to an “as a service” model if the transformation increases neither revenue nor margin? Financial data from HPE shows that quarterly peaks and troughs are being smoothed out, but this isn’t helping the bottom line. To date, this seems to be all that GreenLake has delivered, although we acknowledge that within the delivery of certain capabilities (like block as a service), value has been added to the workflow process for customers.

By definition, product lines that are based on hardware will generally have no equivalent public cloud offering, unless the software component can be abstracted and run separately. Conversely, services based on software have direct cloud applicability. This portion of the HPE business was sold off in 2017.

In the storage arena, HPE partners with the likes of WEKA and Scality (both storage software solutions), but wouldn’t receive any revenue for cloud-based deployments, where HPE offers no additional value. This is the risk of partnering, rather than acquiring software solutions and vendors.

HPE needs to find alternative cloud-friendly revenue streams that mitigate the lack of growth being experienced in the hardware-based BUs. Can the company afford another series of acquisitions? It may be the only route forward to continued and guaranteed revenue growth over the long term.

Copyright (c) 2007-2022 – Post #8c2d – Brookend Ltd, first published on https://www.architecting.it/blog, do not reproduce without permission.